Protection in times of disruption – reframing the context for life insurance advice

Life insurance is a vital part of the ecosystem that helps protect the financial, emotional and physical wellbeing of individuals.

Introduction

In Australia – and around the world – life insurance is a vital part of the ecosystem that helps protect the financial, emotional and physical wellbeing of individuals.

That ‘protection’ ecosystem includes privately provided life and health insurance, superannuation, and social protection mechanisms (such as Medicare, Centrelink, the NDIS and workers compensation) and the people who provide advice and care within these mechanisms.

In this sense, financial advisers should think of themselves as being part of a system much broader than the financial services sector or the financial advice profession.

And by thinking about protection in a wider sense – for example, the way superannuation is designed to protect one’s lifestyle in retirement – it is possible appreciate both the way different financial products interrelate to each other, and also the higher purpose of life insurance advice.

The protection ecosystem, like many others, is undergoing immense disruption in the face of many social, technological and scientific advancements. Increasingly, we will see people living and working longer and differently, and the ramifications for employers, insurers and governments – as well as individuals themselves – will be enormous.

For Financial Advisers helping their clients navigate this ecosystem it is vital to understand the dynamics at play, and in this article we will explore the current protection context – the existence of protection gaps and the drivers of those gaps – and examine the psychology underpinning consumer decision making about protection. The importance of financial literacy, and the role advisers have as educators, will also be discussed.

By reframing the concept of protection and the role for advice within that concept, financial advisers will be better placed to evolve their thinking and approach in the face of ongoing and significant change and will ultimately be able to facilitate a more ‘agile’ form of protection for their clients.

The concept of protection

The interruption of household income, due to death or disability, can be devastating.

Numerous statistics point to people losing their homes and being thrust into poverty as a consequence of inadequate protection[1]. The associated toll on family structures and mental health is well documented.

In terms of barriers to achieving one’s financial goals – whether they be saving for a house deposit or securing a comfortable retirement – ill health is generally one of the biggest.

A little understood but significant economic cost of inadequate protection comes in the form of presenteeism, where workers with health challenges are forced to attend work, even though their productivity and engagement levels are significantly reduced. In Australia the cost of this ‘presenteeism’ has actually been estimated at 4 times the cost of absenteeism[2].

Fortunately, there have long been protection mechanisms available to mitigate against these risks. Today these programs encompass public schemes (social security), private sector offerings (life and health insurance) and public-private partnerships, delivering protection within a broad ecosystem of which financial advisers and life insurers are important members.

But many of these mechanisms of protection are facing disruptive forces.

Disruption in the protection framework

Within the developed world, demand for government support – a traditional source of such protection – is rapidly outpacing supply. Disability levels are increasing to ever more challenging levels, due both to an aging population and medical advancements which see us increasingly live with – rather than die from – serious health issues.

Faced with an ever-increasing cost of funding pensions and supporting healthcare systems, Western governments are forced to cut their spending on – and reduce access to – social protection mechanisms.

At the same time the workforce is evolving away from full time employment in ‘traditional industries’, to more part time, freelance and casual work in the growing ‘gig economy’, with diminished entitlements to annual and sick leave and superannuation. These workers are particularly hard hit by the reduction in government and employer support.

In terms of private sector offerings, many traditional approaches to product design, pricing and underwriting haven’t kept pace with the evolving nature of work and are playing catch up.

And of course, there is the explosion in mental health claims which is threatening the viability of many protection mechanisms.

Just when the government needs individuals to be doing more to protect themselves via private options, a combination of structural and psychological factors is dampening the appetite and ability of individuals to take these options up. As a result, we are seeing a number of protection gaps opening up and growing, with potentially serious consequences.

Protection in Australia – the context

To understand the protection ‘state of play’ in Australia and around the world, Zurich partnered with the Smith School of Enterprise and Environment at the University of Oxford on a pioneering research study[3,4,5] into protection gaps.

This three-phase study involved a survey of over 11,000 working age respondents in 11 countries and examined their anxieties, their vision of the future, and their ownership and understanding of – and attitudes towards – life insurance protection.

The results were enlightening, revealing many structural and cultural differences between countries and highlighting some particularly concerning issues in Australia.

Setting the Australian baseline

Two important baseline findings help set the protection context for Australia.

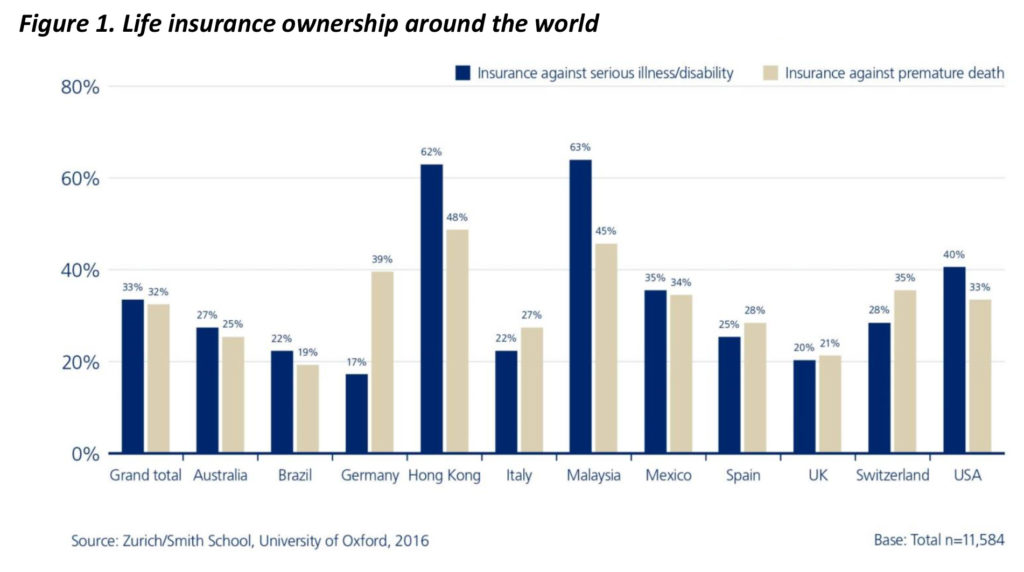

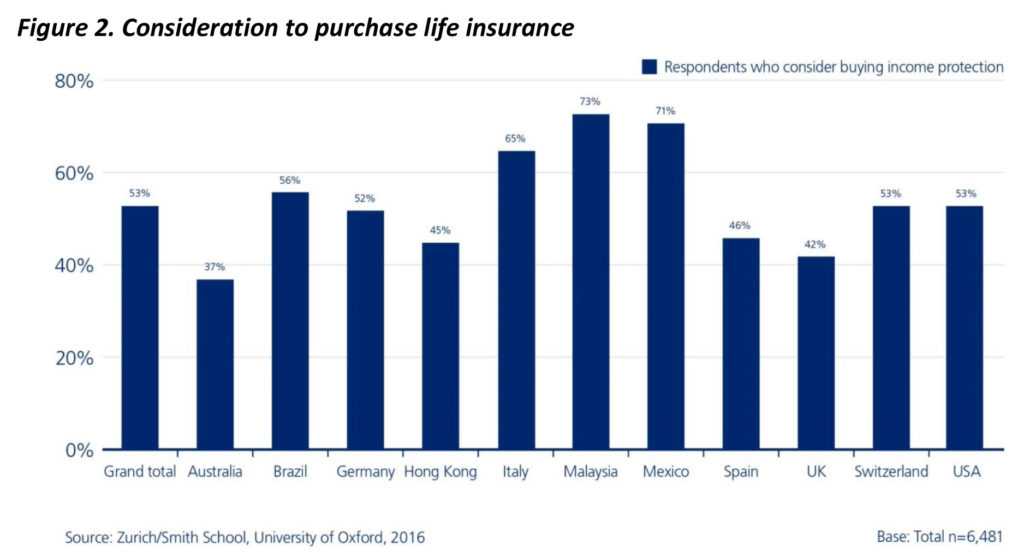

Relative to our global peers, Australians demonstrate more limited appetite for private life insurance cover, for death and disability. This is borne out in Figure 1 – which shows individual ownership of death and disablement cover – and Figure 2, which shows respondents’ willingness to consider purchasing life insurance in the future.

(This ownership figure excludes default cover provided through superannuation – which is largely not an outcome of an active choice – and is consistent with several other Zurich research studies, including its 2015 Report[6] into Insurance Literacy in Australia.)

Gap between perception and reality

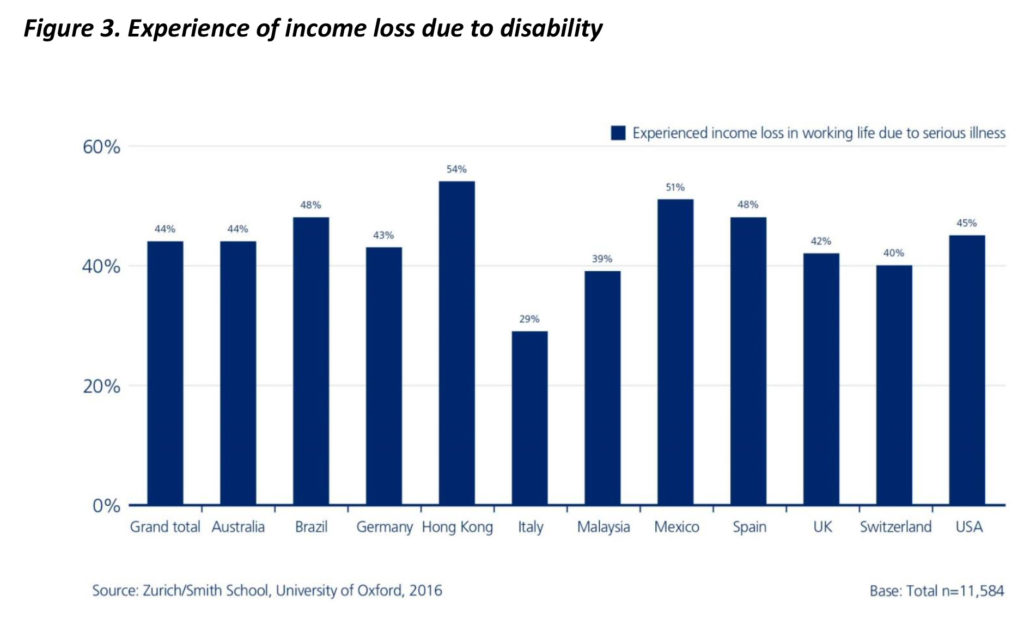

Australia’s relatively lower appetite for life insurance is even more surprising when we understand how many of us have had directly experienced income loss due to disability, and how adequate our savings are as a means to mitigate against such loss.

As highlighted in Figure 3 below, almost half (44%) of all Australian respondents reported that they had experienced income loss due to serious illness at some stage in their working lives.

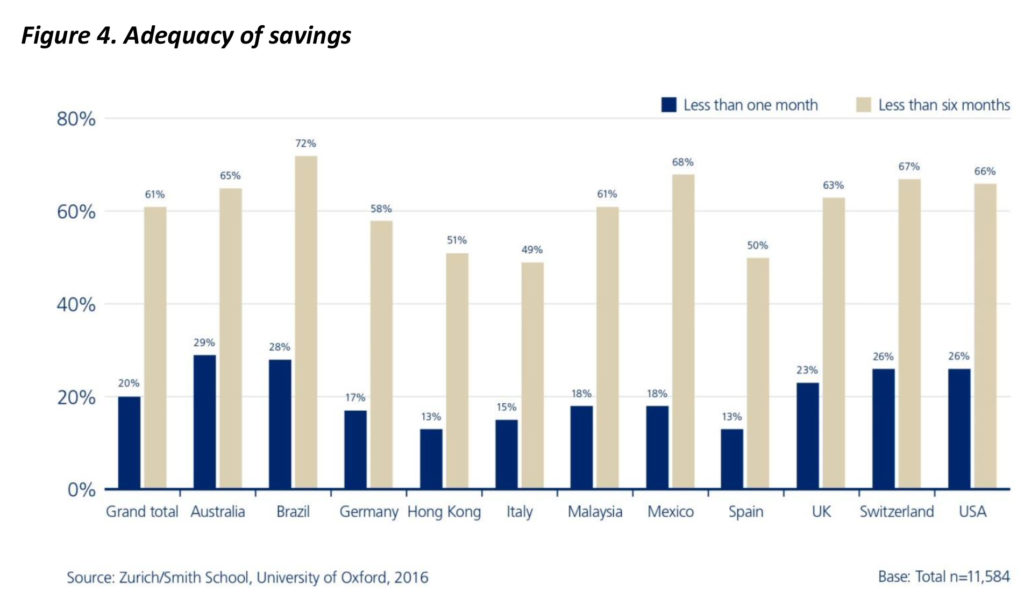

Yet as Figure 4 shows, our ability to personally mitigate against such loss appears woefully inadequate, with just under a third of respondents (29%) indicating they had savings equivalent to one month’s income or less (higher the worst of all 11 countries surveyed and higher than the overall average of 20%). Around two thirds of Australians reported savings equivalent to six months income or less, closer to, but still exceeding, the global average of 61%.

What drives our (lack of) appetite for life insurance?

There is undoubtedly a myriad of complex, interconnected factors that may explain our relatively low willingness to take our life insurance.

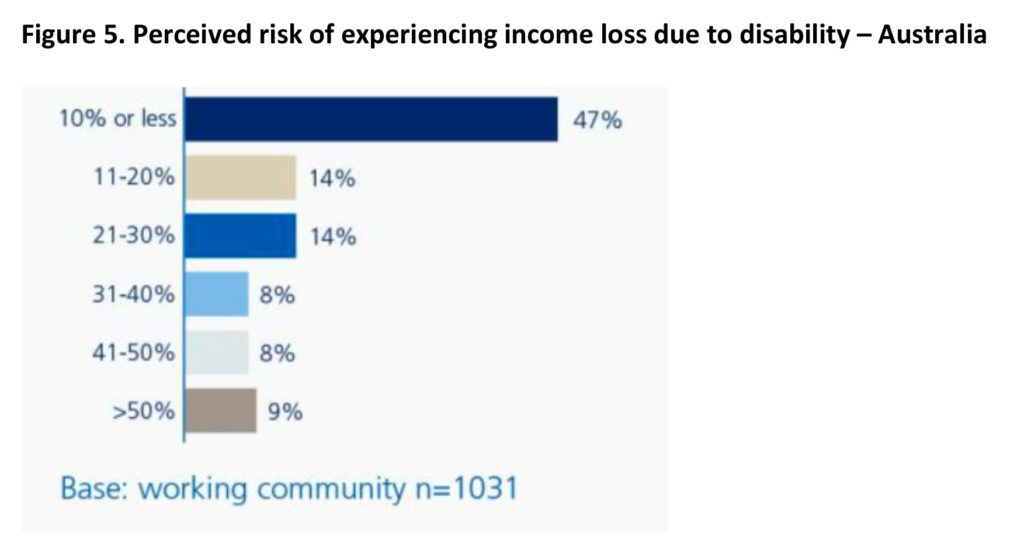

One such factor is that Australians were found to be the most confident nation, with a world leading 47 percent of respondents stating that they had a less than 10 percent chance of lost earnings due to disability or illness. This tendency to see ourselves as bulletproof is perhaps an external manifestation of our famed ‘She’ll be right’ collective mentality.

There also appears to be a misplaced confidence in the size and accessible of government support, with the Australian respondents expecting that in the event of being unable to work due to sickness or accident, the government would compensate approximately 40 percent of their income.

The expectation seems overly optimistic for higher earners, with means testing of disability benefits limiting their availability. Even those who can access social protection are likely to overestimate the adequacy of such benefits. At the time the research was conducted, the standard Centrelink disability benefit equated to roughly one third of the median weekly wage. Furthermore, workers compensation type benefits are only available to employees (not the self-employed) and only apply to work related disabilities. Such benefits are generally capped under state legislation and for many people the amounts payable will fall well short of their normal weekly income.

Perceptions about the cost of cover are likely to be another factor.

Specifically, people tend to overestimate the cost of life insurance protection, especially younger people. In 2015 for example, a group of Gen Y consumers surveyed by Zurich[7] estimated the annual cost of $500,000 of death cover to be around $1,000, significantly overstating the true cost.

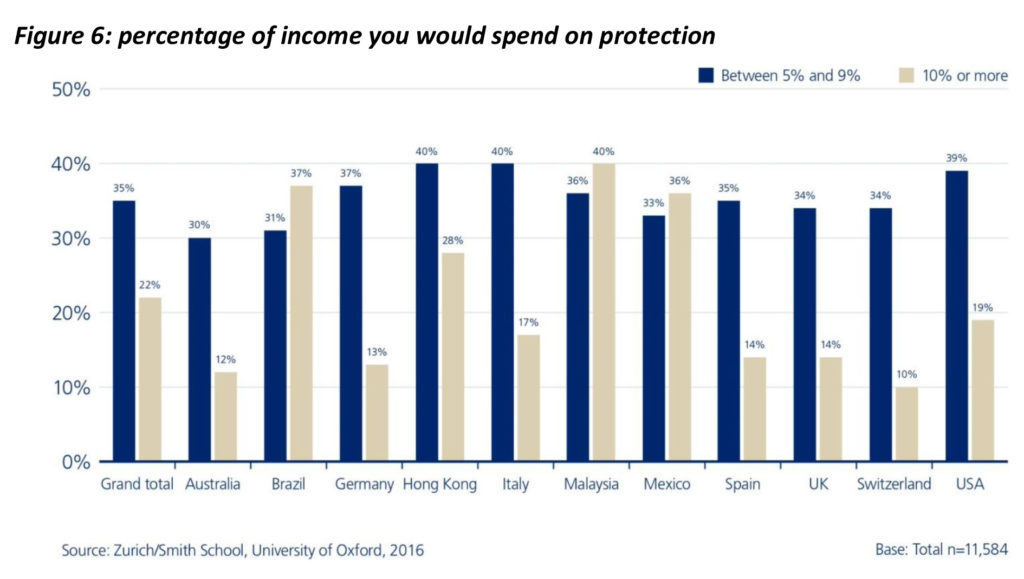

In terms of findings from Zurich’s global study[8], around one third said they would be willing to spend between five and nine percent of their income on life insurance protection, and one in five is willing to spend more than 10 percent.

In actual fact, even at a time when premiums are facing upward pressures, such protection is available for significantly less than 5 percent of earnings (of course individual costs vary by factors such as age and level of protection required).

By way of global comparison, Malaysian, Mexicans, Brazilians, and Chinese from Hong Kong are prepared to spend most on insurance protection, whereas Australians are the least willing to pay!

The fourth, and potentially biggest driver of life insurance appetite may be the lack of awareness and understanding of the risks we face, the consequences, and the options available to mitigate those risks. Broadly this could be described as financial literacy.

The OECD’s working definition of financial literacy is “a combination of awareness, knowledge, skill, attitude and behaviour necessary to make sound financial decisions and ultimately achieve individual financial wellbeing”[9].

When Zurich’s gauged respondents’ knowledge of life insurance, 7 out of 10 respondents said they know little or nothing about how they can protect their income and 4 out of 10 respondents know little to nothing about term life insurance.

Australia was once again below average on this measure, with the broader comparisons certainly reinforcing significant correlation between knowledge, consideration and ownership of life insurance protection.

Financial advisers and life insurance literacy

The role of financial advisers in improving financial literacy broadly, and insurance literacy specifically, may seem obvious. Nonetheless, in a separate study[10], The Life Insurance Literacy Gap, Zurich and the Financial Planning Association sought to quantify this role, by measuring the extent to which financial advisers were positively contributing to improved levels of insurance literacy amongst their customers and the community at large.

Based on a survey of over 500 Australians, this research made several important findings which left no doubt that advisers were highly effective at making their customers more ‘insurance literate’ (as measured against an insurance literacy index constructed by the researchers).

Key findings

- Australians who have received financial advice specifically on life insurance are considerably more likely than those who have never received advice on life insurance to be insurance literate

- While 61% of those who have been advised on life insurance demonstrated ‘Excellent’ levels of Insurance literacy, only 24% of the unadvised are able to claim this (i.e. more than twice as many advised respondents have Excellent literacy)

- The research revealed that advised Australians are more knowledgeable about a number of factors relating to life insurance, including:

- Current individual level of cover

- Knowledge of monthly premium/cost of cover

- The tax deductibility of life insurance

- Events that lead to payouts

- Types of protection that can be held via superannuation

- Availability of substitutes for various types of insurance

Education is even more important as the nature of work changes

The nature of work continues to change, spurred by the Fourth Industrial Revolution (4IR), changing work patterns and structures, social change, an ageing population, the rise and fall of entire industries, and the growth of the sharing economy. As income streams become less linear and more interrupted, the risks we face in securing our financial futures are also changing.

Adapting to this changing world requires workers to be more agile, whether that mean geographical mobility, becoming freelance, or reskilling to make a career shift.

The Zurich study found a positive correlation[11] between such agility and insurance literacy, with workers who self-reported good to excellent knowledge of income protection and term life insurance, being more flexible by measures of both intentions to freelance and willingness to move abroad.

In this sense, financial advisers can help individuals protect themselves not only with product solutions, but with knowledge, and the confidence to be flexible that comes with that knowledge. In doing so they are better equipping their clients to achieve their personal and financial goals in a rapidly changing world.

This arguably is the higher purpose for life insurance advice.

Conclusion

Financial Advisers are members of a diverse ecosystem which offers physical, mental and financial protection. Other members of that ecosystem include life and health insurers and superannuation funds, governments, businesses and other parts of the health care sector.

This ecosystem is facing enormous disruption, driven by an ageing population living and working longer and differently.

With the ability of governments to provide social protection stretched to the limit, individuals must seek out protection mechanisms from the private sector.

This protection includes not only product solutions, but also the financial knowledge which will give them more confidence to adapt to the changing landscape.

Financial Advisers have a critical role to play beyond the traditional scope of their advice, as educators, and as navigators – helping their clients find their way around an increasingly complex protection ecosystem.

![]()

——–