Mental health and financial services – delivering better advice, service and care

With roughly one in five Australians suffering poor mental health at any given time, the human and economic cost burden to society is significant.

Introduction

It’s hard to pick up any news publication today and not find some discussion on the topic of mental health. This ubiquity isn’t a recent phenomenon; the increasingly poor state of mental health across communities – and the associated social and financial impacts – has been documented for several years now.

In Australia – despite being considered one the happiest countries in the world[1] – the growing incidence of mental illness has been the topic of a Royal Commission and has become one of the biggest challenges our sector has ever encountered.

Life insurers in particular are grappling with the impact of mental illness, as the rapid growth of mental health related claims has threatened the sustainability of some benefit types, drawing a concerted response from insurers, regulators and industry associations.

This response will likely include significant changes in the way insurers price and design products, underwrite cover, and manage claims. But this isn’t just about insurance. The way our entire sector engages with sufferers of mental illness will necessarily undergo a complete overhaul, as our ability to understand and recognise the signs of mental ill health improves, and our capacity to deliver appropriate types of advice, service, and care, grows.

As the conduit between client and product and service providers, Financial Advisers are therefore at the forefront of this ‘mental health revolution’.

By understanding the current context of mental health in Australia, the associated challenges faced by our sector and the ongoing response to these challenges, Advisers will be better equipped to take an active role in driving better advice outcomes for sufferers of mental illness, and in maintaining positive mental health across all their clients.

What we mean by mental health

According to the World Health Organisation, mental health is ‘a state of well-being in which every individual realizes his or her own potential, can cope with the normal stresses of life, can work productively and fruitfully, and is able to make a contribution to her or his community.

In terms of poor mental health, there are two broad categories:

- High prevalence conditions such as anxiety (including phobias), depression and substance abuse disorders; and

- Low prevalence chronic and complex conditions, including severe depression, schizophrenia, bipolar disorders and other severe psychosocial disabilities.

Community context

A variety of indicators suggest our mental health continues to deteriorate. In particular, anxiety and depression rates are continuing to increase[2].

Key findings from Australia’s 2017/18 National Health Survey include:

- 13% of adults experienced high or very high levels of psychological distress in 2017/18 – up from 11.7% in 2014/15;

- 20.1%of Australians reported a mental or behavioural condition in 2017/8 – an increase from 17.5% in 2014/15;

- 13.1% had an anxiety-related condition in 2017/18 – up from 1.2% in 2014/15; and

- 10.4% had depression or feelings of depression in 2017/18 – compared to 8.9% in 2014/15

One of many explanations put forward for the growth in reported mental health sufferers is an increased preparedness of people to openly admit to such conditions. The more mental health is discussed, the lower the associated stigma.

We certainly see evidence of this in a number of areas, whether that be in the media3, where journalists write about mental health being a crisis issue for ‘robust’ professional footballers, or in the data showing the rate at which everyday Australians are seeking mental health treatment and advice from their doctor.

According to Australian Institute of Health and Welfare (AIHW) data[4], the proportion of the population using Medicare subsidised mental health specific services grew from 4.3% in 2008/9 to 8.7% in 2018/19. The number of GP consultations to prepare mental health plans has grown from 813,257 in 2012 to 1,191, 786 in 2016.

The cost of mental health conditions

With roughly one in five Australians suffering poor mental health at any given time, the human and economic cost burden to society is significant.

Poor mental health can be linked to Increased rates of divorce, domestic violence and substance abuse.

Economic costs are borne across a number of categories, including loss of productivity due to absenteeism and presenteeism (estimated to cost over $11 billion per year[5]) and the substantial cost to the health system.

The Australian Institute of Health and Welfare (AIHW) estimates[6] that spending on mental health-related services in Australia from all sources (government and non-government) was around $9.0 billion in 2015/16, funded by states and territories (59.8%), the Australian Government (35.0%) and private health insurers (5.2%). Government subsidisation of mental health related prescriptions in 2016/17 was estimated[7] at $511m.

And of course, there is the cost to insurers – particularly life insurers – who are seeing the cost of mental health claims continue to grow, more rapidly than any other cause.

Industry context

Mental health is one of the biggest challenges facing the financial services sector.

We see a financial challenge, especially in the form of claims costs and their flow on effect.

There is a significant reputational challenge, with insurers attracting scrutiny from regulators, the media[8], and consumer groups, for claims and underwriting practices which are perceived to be discriminatory and hard to access.

For the broader financial sector there is also an engagement challenge – the ability to optimally interact with customers suffering poor mental health is impeded by an overall lack of relevant training and experience amongst those at the frontline, limiting their ability to understand and recognise the signs of mental ill health, and subsequently their capacity to deliver appropriate types of service and care.

The financial cost

In terms of its contribution towards people with a mental illness, the life insurance industry is second only to Government, paying over $700 million in mental illness related claims in 2018[9]. As a primary cause of claim, mental Illness related claims are the second most common cause of claim overall; being the most common cause for Total and Permanent Disablement (TPD) claims and third most common cause for Income Protection (IP)[10].

But rather than being a cause for celebration, the spiralling cost of mental claims in life insurance is a cause for significant concern, with an alarming sustainability challenge arising because of a growing gap between the premiums collected and claims paid out in disability products (life insurers and reinsurers have lost $3.4 billion on individual disability products over the last 5 years[11]).

The threat is viewed by APRA as so significant that felt it necessary to intervene[12], mandating a raft of changes to the design and pricing of income protection products, designed to put them on a much more sustainable footing.

(The most obvious and immediate manifestation of these changes was the banning of Agreed Value IP policies after 31st March 2020.)

If the poor claims experience of existing policies continues then further upward revisions to premiums are likely across the market, creating further affordability challenges for customers (and their advisers).

So how exactly did we get to this point?

The Australian life industry, by many measures, is regarded as one of the most effective in the world. Relative to their global peers, Australian customers can generally access higher levels of cover, at lower cost, and with a higher likelihood of their claims being paid[13].

But the industry has faced many systemic difficulties in dealing with mental health coverage.

Challenges faced by insurers

There are many factors that have made it more difficult for insurers to deal with mental health in the same way they deal with other health conditions. In this article we will explore three of the most significant.

Arguably the biggest barrier to meeting the mental health challenge has been the hitherto lack of usable data.

A highly detailed understanding of the prevalence of a given risk amongst a population is a core requirement to predicting likely future incidence of that risk. Put another way, pricing risk requires very granular data, and lots of it.

But up to now, data on mental illness – relative to other health conditions – has been problematic, for a number of reasons:

- Compared to mortality tables, constructed by Insurers over centuries, the collection of mental health data of value to insurers is in its infancy;

- There has been little consistency in definitions and language used around mental illness, making a consolidated data set hard to compile;

- There is a reliance on sufferers to articulate their feelings and the impact on their lives, and the clarity and reliability of this self-reporting can be highly variable;

- Rather than being one homogenous condition, there are many different mental health conditions, each with their own symptoms, prognosis, recovery profile and treatment. Gathering statistically valid granular data on individual conditions thus takes longer;

- Historically, sufferers of mental illness have been reluctant to openly acknowledge that fact, leaving many cases undiagnosed.

Over the last decade or so, this lack of data has manifested itself in several ways.

The lack of understanding of the many different types of mental disorder previously saw a blanket ‘one size fits all approach’ by insurers, which lead to many sufferers being inappropriately having exclusions applied or denied cover altogether. (This also fuelled the criticism that people were effectively disincentivised from seeking professional help for their condition).

In the absence of suitable data, it was hard for pricing actuaries and underwriters to differentiate between sufferers of situational depression at one end of the scale (for example, due to bereavement or divorce) and sufferers of schizophrenia or bi-polar disorder at the other. It is now recognised that the profile and inherent risk factors for these conditions are vastly different.

It should be noted that lack of data is also a problem for other stakeholders in the health ecosystem. The ability to judge the impact of a mental disorder on a sufferer’s life and livelihood remains a relatively imprecise science, and in some respects the medical sector is learning just as much as the financial sector.

Another factor at play is the sometimes-subjective nature of mental health diagnoses, which can cause complications at both underwriting and claim time. Although mental health conditions are recognised in the international classification of diseases (the ICD-10), there are currently no reliable biomedical markers to indicate the presence or severity of most mental health conditions.A third major factor is that insurance claims processes can themselves reinforce, or even be the catalyst for, mental health conditions. The evidential requirements for complex and high value claims can be substantial, and this can be overwhelming for some claimants, due to the sheer volume of work involved and the nature of the process itself which some perceive as adversarial.

Taking up the challenge – the industry response

Mental health is one a small number of issues which has galvanised our sector and heralded a new area of transparency and collaboration between stakeholder groups.

And rather than the focus of this collaboration being insular – the protection of the pool of policyholders – there is an ambitious external focus on improving mental health outcomes across the entire community. The highlights of this response are summarised below.

Better data

Recognising the importance of data to understanding the nature of mental health conditions, insurers have started to collect and share more relevant data. In 2018 APRA and ASIC approved a proposal by the FSC (through KPMG) to collect industry-wide claims data[14]. This data sharing allows the creation of a much greater pool of data than any individual insurer could hope to amass, thus enabling more detailed insights into mental health and other claimable conditions.

And the quality of the data shared via that process is also improving, with individual insurers starting to collect more granular data on mental health at underwriting and claims time, and more consistency in approach.

Improved skills, training and awareness

Recognising that staff – particularly those dealing directly with customers – needed to be better equipped to support and serve those affected by poor mental health, insurers have embarked on extensive programs to improve awareness of mental health issues amongst their staff and to provide appropriate skills and resources.

In most cases, specialist external expertise has been called upon to tailor and deliver programs to staff. One of the best known of these providers is Superfriend, a national workplace mental health not-for-profit organisation which has worked with insurers, licensees and employer groups to deliver training.

Codifying commitments

A number of important commitments related to mental health that have been codified by members of the Financial Services Council.

FSC standard 21[15] requires members to provide mental health awareness training of the type described above, whilst Standard 25[16] relates to data collection and is designed to drive more frequent sharing of better quality, more consistently presented data, to facilitate better consolidation and interpretation.

The historical practice of placing claimants undertaking surveillance has also been recognised as capable of causing adverse mental health outcomes and is now subject to strict guidelines under the FSC’s Life Insurance Code of Practice[17].

Treating cases on their merits

In recent years many insurers have overhauled the way they deal with mental health from an underwriting perspective. More specifically, there has been a recognition that mental illness is not one homogenous condition, and that the causes, treatment, and prognosis differ widely across the many different disorders.

Moving away from the ‘one size fits all’ approach, underwriting processes have evolved to treat each case on its merits, thus being more equitable and facilitating a virtuous circle: collecting more data, which allows more insights, more accurate pricing, more affordable cover for many, more people taking out cover and more data being collected.

Importantly, the contemporary underwriting approach dispels the perceived discouragement of people seeking professional help with their mental health.

Zurich’s Fact Sheet, ‘Mental Health FAQ’[18] summarises the type of factors considered when assessing applicants who have indicated they suffer mental ill health:

- Any diagnosis which has been made

- Types of treatment received (i.e. medications or cognitive behavioural therapy)

- The impact symptoms have had on the ability to work or study

- The nature, severity and duration of the symptoms and how they have been managed

- General health and lifestyle, work and family history

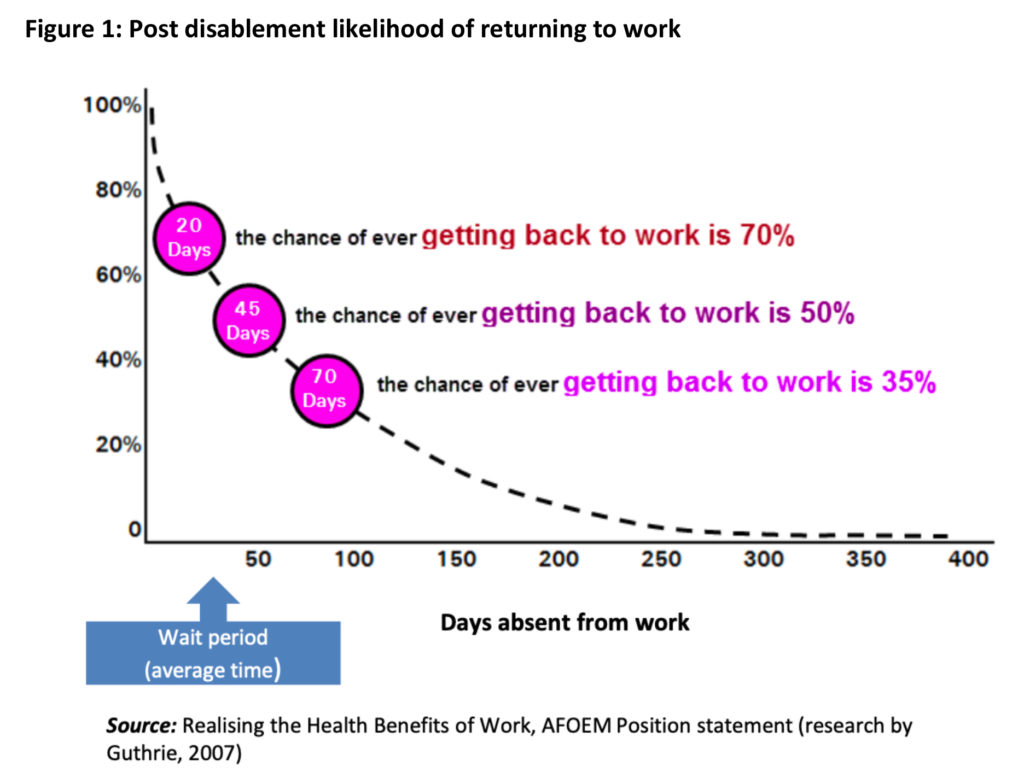

At the claims stage, insurers recognise that the vast majority of claimants are keen to return to work and we now see many working proactively with claimants on individualised rehabilitation plans to facilitate this. This approach is designed to not only help those already suffering mental ill health, it can help mitigate the likelihood of it becoming a second order effect on those unable to work for extended periods of time. As the graph below shows, speed is of the essence, with the likelihood of ever returning to work dropping quite slowly.

But there are still limits on the ability of life insurers to get involved in rehab, with legislation effectively preventing life insurers from funding medical treatments for the purposes of rehabilitation. (A recent push to have this legislation amended was unsuccessful[19]).

Advocating for better mental health

The financial services sector continues to advocate for positive mental health, with this advocacy taking many forms, including the provision of mental wellness programs and resources for staff and customers, working with employer groups, and supporting community based programs (an example being the ‘Tackle Your Feelings’ initiative, a collaboration between Zurich and the AFL Coaches and Players Associations[20]).

Greater stakeholder collaboration

The industry has sought to work more collaboratively with all stakeholder groups to share learnings and develop solutions to the complex challenges posed by mental health trends. This includes direct representation to Government ministers as well as submissions to a range of committees and enquiries. Various roundtables and forums regularly bring together stakeholders from government, regulators, the medical profession and mental health groups, including the FSC’s twice yearly Life Insurance Mental Health Roundtable.

Product design

Many insurers are considering how product design can help provide better outcomes for those facing mental health challenges, balancing access to cover with sustainable and affording pricing. An example of one possible direction would be the trialling of income style benefits for some TPD claimants, rather than paying claims as large, single lump sums. A potential outcome of such an approach is make the initial claims process itself more ‘user friendly’ (the initial evidentiary requirements would likely be lower, and benefits would be able to be paid earlier) and thus less likely to cause or exacerbate anxiety on the part of the claimant.

Conclusion

The growing incidence of mental ill-health in our community is creating a significant economic and social burden for our community.

Those bearing the economic costs of poor mental health include Federal and state governments, employers experiencing lost productivity, and health and life insurers.

Life insurers in particular are grappling with the impact of mental illness, as the rapid growth of mental health related claims has threatened the sustainability of some benefit types, drawing a concerted response from insurers, licensees, regulators and industry associations.

And, as the conduit between client and product and service providers, financial advisers are very much at the forefront of this ‘mental health revolution’.

Underpinning this multi-pronged response is improving our understanding of the nature of mental health disorders, including their symptoms, prognosis, and treatment. This greater collective understanding, to be facilitated through increased stakeholder collaboration, data sharing, and training, will improve the capacity of advisers and institutions to deliver more appropriate and sustainable types of advice, service, and care to those suffering poor mental health.

Ultimately, it is hoped the entire financial services sector can play a valuable role in improving mental health throughout the community.

![]()

———-