Claims Advocacy – from ‘value add’ to core advice offering

What are the growth drivers for Claims Advocacy services in the context of the evolving life insurance landscape?

Introduction

Compounding the impact of ongoing licensee consolidation and new professional development requirements, the LIF driven reshaping of adviser remuneration for life insurance advice – in the form of lower up-front commissions and higher renewal commissions – has left many advisers no choice but to rethink, and, in many cases, fine tune their business models.

Typical adviser responses have included a heightened focus on the efficiency of advice delivery (and the role for technology in driving this efficiency) and the refining of target markets towards higher value customer segments.

Another strategic response has been to broaden the potential revenue base of the practice, by expanding the services offered, a powerful example of which can be seen in the growth of Claims Advocacy services.

Beyond the assistance of existing clients at claim time (which most advisers see as a vital and highly satisfying part of their role) the articulation of Claims Advocacy as a specific, standalone component of the advice offering opens up the opportunity to (a) provide such a service to new clients, and (b) charge for such a service.

In this article we will explore the growth drivers for Claims Advocacy services in the context of the evolving life insurance landscape and the financial dynamics underlying life insurance advice. We will also provide practical tips for those advisers seeking to make Claims Advocacy a more central part of their advice proposition.

Life insurance claims – in the news

In any form of insurance, the ultimate barometer of value is in the payment of claims. As such, life insurance claims data has always been of paramount interest to both advocates and detractors of the industry.

This spotlight became even more intense following the 2016 ASIC review[1] of claims practices across the retail, group and direct life insurance sectors.

The report made many findings which were positive for the life industry generally, and financial advisers specifically, observing that across the board 90% of all admitted claims were accepted, and on a channel basis, ‘Advised policy’ claims had significantly higher acceptance rates.

However, the report also identified a number of improvement opportunities, particularly across claims reporting and data transparency, the legal framework covering claims handling, the dispute resolution framework for life claims, and the strengthening of various standard and practices.

Many of ASIC’s recommendations in these improvement areas have subsequently been addressed, for example:

- the Life Insurance Code of Practice[2] limits the use of surveillance and sets out standards around the communicating of claims decisions;

- Claims dispute resolution mechanisms, standards and reporting are also addressed in the Code; and

- After widespread industry consultation, Treasury has issued an Exposure Draft[3] in relation to Royal Commission recommendation 4.8, to include all claims handling services within the definition of a financial service.

Another – more public – example of significant industry progress can be seen in the joint collection and publishing of claims data by APRA and ASIC.

Following extensive work to standardise the way claims outcomes were reported, life insurers now provide regular data to APRA, which is then regularly released to the public in a way allows comparisons to be made – between insurers and channels – on metrics such as acceptance rates and turnaround times. Each fresh data release is also reflected in the Life Insurance Claims Comparison tool on ASIC’s moneysmart website.

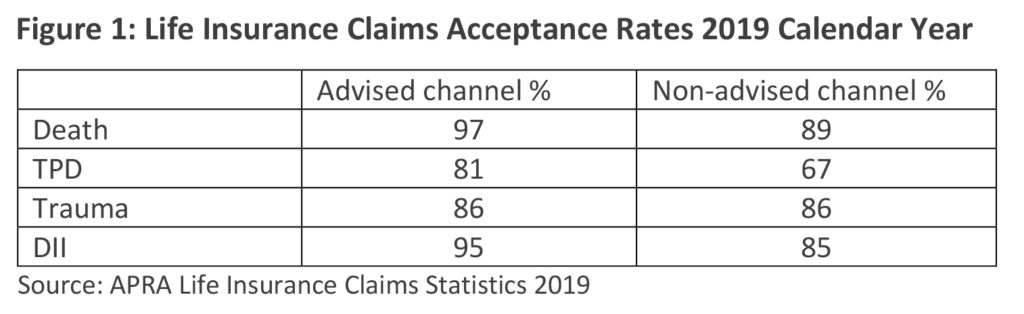

2019 claims data

APRA’s most recent claims data release[4] was in April 2020 and it showed that Australian life insurers admitted over 108,000 claims – worth over $9 billion – during the 2019 calendar year.

These 108,000 claims comprised:

- 21,657 (20%) advised claims;

- 27, 659 (25.6%) non-advised claims; and

- 58,732 (54.4%) group (super and ordinary) claims

Once again, a difference was evident in acceptance rates between advised (retail) and non-advised (direct) claims:

In its commentary, APRA observed: ‘Generally, Individual Advised business shows higher admittance rates than Individual Non-Advised for the same cover type. This could be due to the policyholder having clearer expectations up front of what is covered by the product, or (related to the previous point) the adviser discouraging the policyholder from lodging a claim that is not covered by the policy’.

Furthermore, APRA also found Advised policy claims had significantly faster turnaround times and lower dispute rates.

Whilst a 2016 Zurich survey[5] of financial advisers found that 95% got actively managed claims on behalf of their clients, clients themselves don’t instinctively expect to approach their adviser in the event of a claim. This was highlighted in a 2013 AFA/Beddoes Institute Whitepaper[6] which found many policyholders “expect to go direct to their insurance company in the event of a claim, irrespective of the channel through which they took out their policy”.

If we apply the 95% adviser involvement figure across all retail claims, there are around 80,000 claims each year that have no adviser involvement, and untold instances where claims are never made because the client didn’t realise they were eligible, or in the case of group cover, didn’t realise they were covered at all!

A claims service gap/opportunity clearly exists.

‘Who they gonna call?’

Whilst most life insurers have invested in technology to help streamline claims processes, making them quicker and more accessible, the reality is such processes can still be complex, especially for higher value disability claims which require evidence and documentation from many different sources and which rely on input from many external specialists (medical experts, employers, accountants etc).

To an outsider – even a highly educated one – a claims process can be perceived as daunting.

As the AFA Whitepaper[7] ‘The Value of Protection, creating an advocate for life’, articulated: “Consumer perceptions of how claims are managed are overwhelmingly negative. They expect a difficult assessment process.”

Happily, consumers are generally self-aware about the areas in which they lack knowledge and where the expertise in these areas can be found.

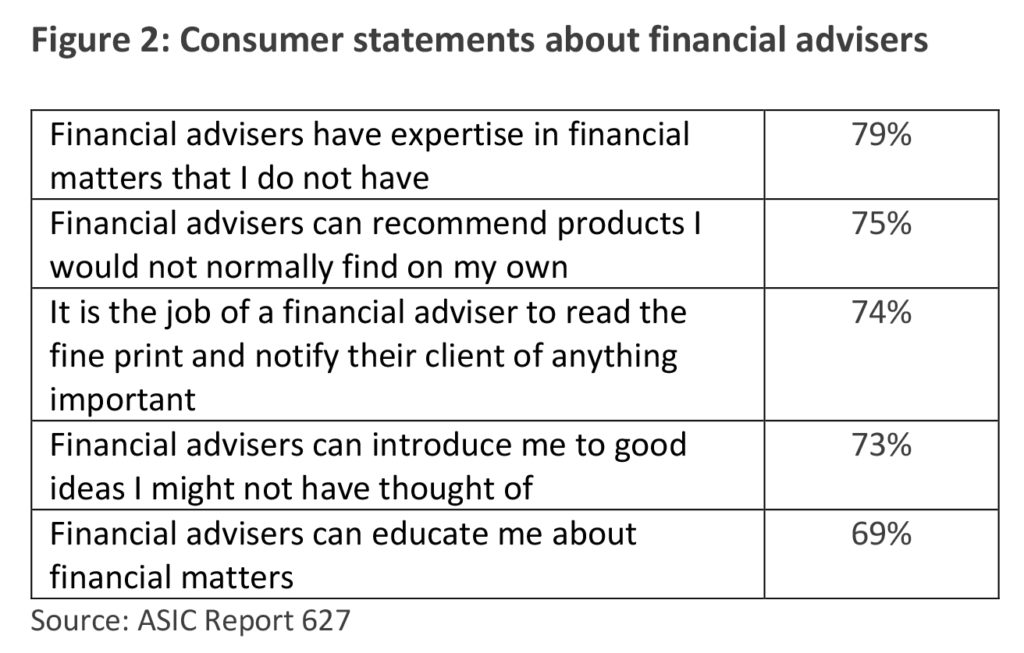

An oft quoted estimate[8] of adviser usage in Australia is 20%, although ASICs report 627 – released in August 2019 – puts the percentage of people who have received tailored financial advice at least once in their life[9] at 27%. That leaves a majority 73% who have never received advice, a surprisingly high figure given an almost similar majority agreed with the following statements about financial advisers:

In the minds of consumers, the role for advisers, it seems, is clear. But is the value?

Where’s the value?

The survey[10] undertaken for ASIC Report 627 also asked non-advised participants to nominate barriers to advice usage and found the whilst cost of advice was the most common objection (35%), almost one in five said they could simply not see the value of financial advice.

Similar results have been seen across other surveys, and to the extent that our willingness to pay for a service is contingent on seeing value in return, this lack of perceived value unsurprisingly translates into lack of willingness to pay for advice.

This is especially true for life insurance advice, where a healthy client who never needs to claim will only ever derive intangible value – in the form of ‘peace of mind’ – from that advice.

Zurich confirmed this in its 2019 ‘Risk Advice Disconnect’ paper[11]. Based on a random survey of 1,000 Australian adults, the study found that:

- 28% were unwilling to pay anything for life insurance advice; and

- a further 29% were only prepared to pay up to $250.

The same survey found two-thirds of advisers would need to charge $2,000 or more for even basic risk advice, leaving a massive gap in expectations on both sides.

Of course, the perceptions of value change dramatically where there is a clear – and known – benefit, such as an insurance payout.

In the same way the Beddoes Institute found[12] that satisfaction with life cover rose significantly in the event of a successful claim, countless customer testimonials make it clear satisfaction with life insurance advice also improves dramatically in the event of a claim:

“The insurance cover recommended to me by Michelle meant next to nothing at the time but a huge amount since being diagnosed. I am very grateful for her experience and advice.”[13]

In summary, some of the main barriers to advice take up can all but disappear where there is a clear, quantifiable, financial benefit.

The idea that customers would be willing to seek (and pay for) advice at the time of a claim, not just when applying for a new policy, is the key concept on which Claims Advocacy services are predicated.

Is there a market for Claims Advocacy?

The best indicator of the need for a service is to see how many businesses exist to meet that need.

In the area of Claims Advocacy, legal firms – many operating on a ‘no win, no fee’ basis – have become more active in this space in the last few years, potentially in response to the 2017 introduction[14] of limits on legal fees chargeable for CTP claims.

Some larger legal firms have invested in advertising campaigns, many of which target superannuation fund members who may be unaware they even have any cover. Examples of such targeting can be seen on the first page of a Google search for ‘TPD claim’ which will generally be dominated by advertising by such firms.

With ‘no win, no fee lawyers’ taking anything from 15% to 40% of a successful claim payout in legal fees[15], the ethics of their involvement is the source of ongoing – often heated – debate within the financial advice profession.

Happily, we are starting to see the emergence of Claims Advocacy firms from within the financial advice profession, with a growing number of financial advisers incorporating Claims Advocacy into their service offering, some even going so far as to establish standalone businesses.

(Indeed, when googling ‘life insurance claims help’, four out of the first ten entries were for Claims Advocacy businesses).

How is Claims Advocacy different from simply helping my client at claim time?

The role of Claims Advocates is to help their client navigate the claims process with one or more insurers. A typical process could look like:

- Understand the claimable event;

- Investigate potential eligibility for claim, including examining policy terms and any applicable exclusions;

- Understand processes specific to the client’s insurer;

- Assist with the completion and submission of forms and gathering and provision of other requested documents;

- Liaison with insurers, medical specialists, employers, trustees and other external parties as part of step 4;

- Educate, update and inform the client throughout the process;

- Where appropriate advice on any tax or other financial implications of the claim payout; and

- Facilitate payment.

For some advisers, particularly risk specialists, this process may seem virtually identical to that they already follow when managing a claim for a client. And whilst that is largely true, Claims Advocacy has a few key distinguishing features:

- It is a true end – to – end service;

- It is a specialised service which requires the Claims Advocate to gain a deep understanding of the claims processes of different insurers and become an expert in dealing with medical practitioners and other experts;

- It is articulated and documented as a separate service, which the Claims Advocate provides as a core offering (rather than a value add);

- It is a service that can be provided to clients who didn’t obtain their insurance through you; and

- It is a service for which there is a clearly documented cost of provision, and for which the client is charged.

How do Claims Advocacy firms charge for their services?

As with financial advice there is a wide variety of charging models used by Claims Advocacy services, including flat fees, percentage fees and combinations of both.

One thing that is consistent is their quantum. Compared to the 15-40% charged by ‘no win, no fee’ lawyers, claimants will generally see a much higher proportion of the claim benefit end up in their own hands.

Whilst most Claims Advocates don’t publish their fees, examples found online include:

- Firm A.

$550 non- refundable initial assessment fee; plus

Fees ranging from $2,125 to $4,430 for death claims, up to $7,095 for TPD,

and up to $3165 for Income Protection (plus up to $612 per month for ongoing claims). - Firm B.

$1,000 for income protection

3% of any lump sum claim

Fees only payable if claim successful

With the exception of the upfront, non-refundable assessment fee charged by Firm A, the general approach taken by Claims Advocacy firms is to allow payment upon receipt of claim benefits. This approach minimises the out of pocket burden on claimants, which is far more attractive to potential clients and removes the main barrier to the take-up of professional advice.

Charging existing clients for claims assistance

Whilst the provision of – and charging for – Claims Advocacy services may seem straightforward, there is an ongoing associated debate about whether advisers should be charging for the management of claims, for their existing clients.

Research published16 at the end of 2019 added further to fuel to the debate, revealing a considerable amount of adviser and support staff time is required for claims support but with extremely limited cost recovery. Specifically, the research found the average duration spent per claim was around 7 hours, equating to an estimated cost of $2800.

Despite the obvious costs involved, historic wisdom amongst many advisers has been that ongoing renewal commissions are effectively a form of ‘advance payment’ for such services, and unsurprisingly the research found only 7% of advisers charge their clients for claims support.

This ‘advance payment’ philosophy has two main shortcomings:

- In many cases the renewal commission will not be sufficient to cover the costs of supporting the client at claim stage (as well as the other ongoing client support it pays for); and

- Many policyholders will (happily for them) never claim, thus weakening the relationship between the fees they pay and the services they receive.

Expect thinking in this area to evolve considerably over the coming years, especially when life insurance remuneration comes under the ASIC spotlight as part of the 2021 LIF review.

How to strengthen your own claims proposition

Even for those who don’t wish to commit to a full Claims Advocacy strategy, claim time remains one of the biggest opportunities to demonstrate value and deepen your client relationships, and in this regard many advisers can benefit from strengthening their claims proposition. Here are some brief tips on how you can achieve this.

- Make yours the first number they call

Constantly reinforce with your client that you are their first port of call should they suffer any change in health (illness, injury, or worse). Rather than giving your client a normal business card, consider giving them an emergency contact card with your mobile number and make it clear that they can call you at any time; - Be proactive and talk to the insurer as soon as possible

Make yourself familiar with the nature of your client’s policy or policies. Make yourself aware of special conditions (exclusions, waiting periods etc). If you don’t have paper records of all your clients’ policies, some insurers, may provide an online archive of these records. A simple phone call can save hours of work; - Study the policy in detail

By understanding the applicable policy in depth you may be able to identify any special benefits and/or optional extras the client may be eligible to claim for; - Set expectations around timeframe and process

Each insurer may have slightly different processes, each with their own nuances. Become familiar with them all. And communicate, communicate, communicate. - Assist your clients to gather requirements

Even the most complex claims can be dealt with efficiently and sensitively when all the requirements are provided up front. It is not unusual for some insurers to pay a trauma claim within 48 hours of the correct requirements being provided. Adviser Guides are usually a good source of information on these requirements. - Know your client and go the extra mile

They are most likely experiencing physical, emotional and financial stress, so be empathetic.

Summary

Life insurance claims represent a significant opportunity for advisers to articulate, deliver and even charge for services that are well understood – and valued – by their clients.

Although over 100,000 life insurance claims are paid each year it is estimated that only 20% involve a financial adviser, leaving 80% of claimants to self-navigate processes which can be perceived as complex and daunting.

Recognising the need for specialist help – especially amongst direct, group, and orphaned clients – a growing number of advisers are starting to offer Claims Advocacy services, either as a core part of their advice offering, or as entirely standalone businesses. These services often compete with ‘no win, no fee’ lawyers, usually at a much lower cost to the claimant.

To the extent that consumers with a pending claim can more easily understand the end benefit of Claims Advocacy services, they are likely to be more willing – and able – to pay for such support, especially when those fees can be paid from the proceeds of a successful claim.As a result, the demand for specialist Claims Advocacy services is likely to grow, representing a significant opportunity for advisers looking to expand their offering and widen their target market.

![]()

——–