Life Insurance 2030 – the products of the future

As the industry faces into unprecedented levels of change, it is likely that the future focus of innovative effort will increasingly be in the area of product development.

Introduction

Competitive forces within the Australian life insurance market have long underpinned a strong culture of innovation amongst insurers. Recognising an imperative to improve the way customers and financial advisers access – and engage with – life insurance, the last decade has seen extensive insurer investment across areas such as process automation, data analytics, and customer experience.

As the industry faces into unprecedented levels of change, it is likely that the future focus of innovative effort will increasingly be in the area of product development, as insurers adapt to the powerful forces of disruption we are witnessing in regulation, customer demographics and healthcare. Advisers must adapt to these forces too, as consumers, and the risks they seek to protect against, continue to evolve rapidly.

In this article we will examine the key forces of disruption impacting life insurers, and their implications for both product design, and risk management strategies more broadly.

The nature of risk is changing

Broadly speaking there are two types of life insurance; those designed to pay benefits when the life insured suffers a particular health event, such as death, terminal illness and trauma (cancer, heart attack etc), and those where a health event impedes the ability of the life insured to work (income protection and TPD). To the extent that people around the world are living and working longer, and the nature of work itself is changing rapidly, the fundamental risks that life insurance protects against are therefore themselves undergoing immense, irreversible change.

On a global basis, life expectancy continues to improve, driven by seemingly continuous advancements in medical science. In Australia[1] for example, a boy born in 2015 – 2017 can expect to live to the age of 80.5 years and a girl would be expected to live to 84.6 years compared to 47.2 and 50.8 years, respectively, in 1881–1890.

Conditions which were once fatal are increasingly treatable and survivable. The death rates from stroke[2], for example, decreased by 70% between 1979 and 2010, whilst heart disease death rates[3] decreased by a staggering 600% between 1968 and 2015. Cancer survival rates have improved dramatically too, as illustrated in Figure 1, below.

As we live longer, and recover better, so too are we spending longer in the workforce.

As well as a healthier population, the evolution of the workforce towards more service – based, less physically demanding, jobs, coupled with more flexible working arrangements and the growth of the gig economy have opened up more opportunities for older workers, and this has been reflected in ever increasing workforce participation for those aged 55 and over. (The raising of the age pension age, not reflected in the data below, will only seek to increase this trend).

There are many pointers here to the life insurance of the future.

Whilst maximum entry ages of 60 are currently commonplace for trauma and disability products, these will need to raise over time, to cater for the increase in demand for cover at older ages. (Similarly, policy expiry dates will likely be extended too). Whilst there are obviously pricing and risk management implications from such changes, a more granular approach to pricing and underwriting will likely act as an enabler. Similarly, more flexibility in contract lengths and terms, as flagged by APRA for income protection policies, will allow insurers to mitigate risk and offer cover on a more sustainable basis to those previously considered too risky, either because of their age or health history. As survival rates for serious illnesses continue to improve, and sufferers are able to return much more quickly, expect trauma cover to evolve in both coverage and benefit structure. Increased access to cover for gig workers and freelancers should also be expected, and again big data, coupled with an ability to offer more flexible contract terms, will be crucial enablers of such innovation.

Consumer behaviours and expectations are changing too

The globalisation of media and brands, turbo charged by the digitalisation of our lives, has redefined and reset the benchmarks for customer experience.

For financial services brands, evolving consumer expectations in a number of areas are especially relevant:

Health and wellness

As an antidote to more unhealthy, stressful lives, people are turning more to yoga and meditation, and demanding healthier food options from supermarkets and restaurants. Wearables and mobile wellness content are growing in popularity, and the wellness economy is now estimated to be worth nearly USD 5 trillion[4]. The link between good health and life insurance is obvious, and many life insurers now incorporate wellbeing into their offerings.

Privacy and data protection

People are becoming smarter and more selective about sharing their data, appreciating the benefits that come from sharing with trusted sources, but equally clear that not protecting it can have serious consequences. Research conducted by OIAC[5] in 2017 found that 69% of Australians were more concerned about their online privacy compared to five years prior. More positively however, ADMA research[6] published in 2018 found that 44% of us were now more comfortable exchanging personal data with companies than in the past. The more customers are willing to share their data, the more products, including insurance can be truly customised, and the more they can be priced accurately.

Personalisation

From fashion to automobiles to food and beverages, more brands are giving customers the opportunity to build their own products online. Whilst product modularity may not seem new, the levels of optionality expected are.

Corporate behaviour and authenticity

News travel fast, and put simply, in the age of the internet and social media, there is nowhere to hide. Brands not only need to be transparent and honest; they need to reflect the evolving views of their customers. Increasingly this means getting more involved in local communities and publicising their position on social issues.

Responsive, accessible service

Put simply, people have become accustomed to accessing help through the channel, and at the time, of their choice. Help from a 24/7 AI powered chatbot is no longer science fiction.

Of course, overlaid on all of this is the ubiquity of digital devices in our lives, and herein lies the opportunity for financial services providers.

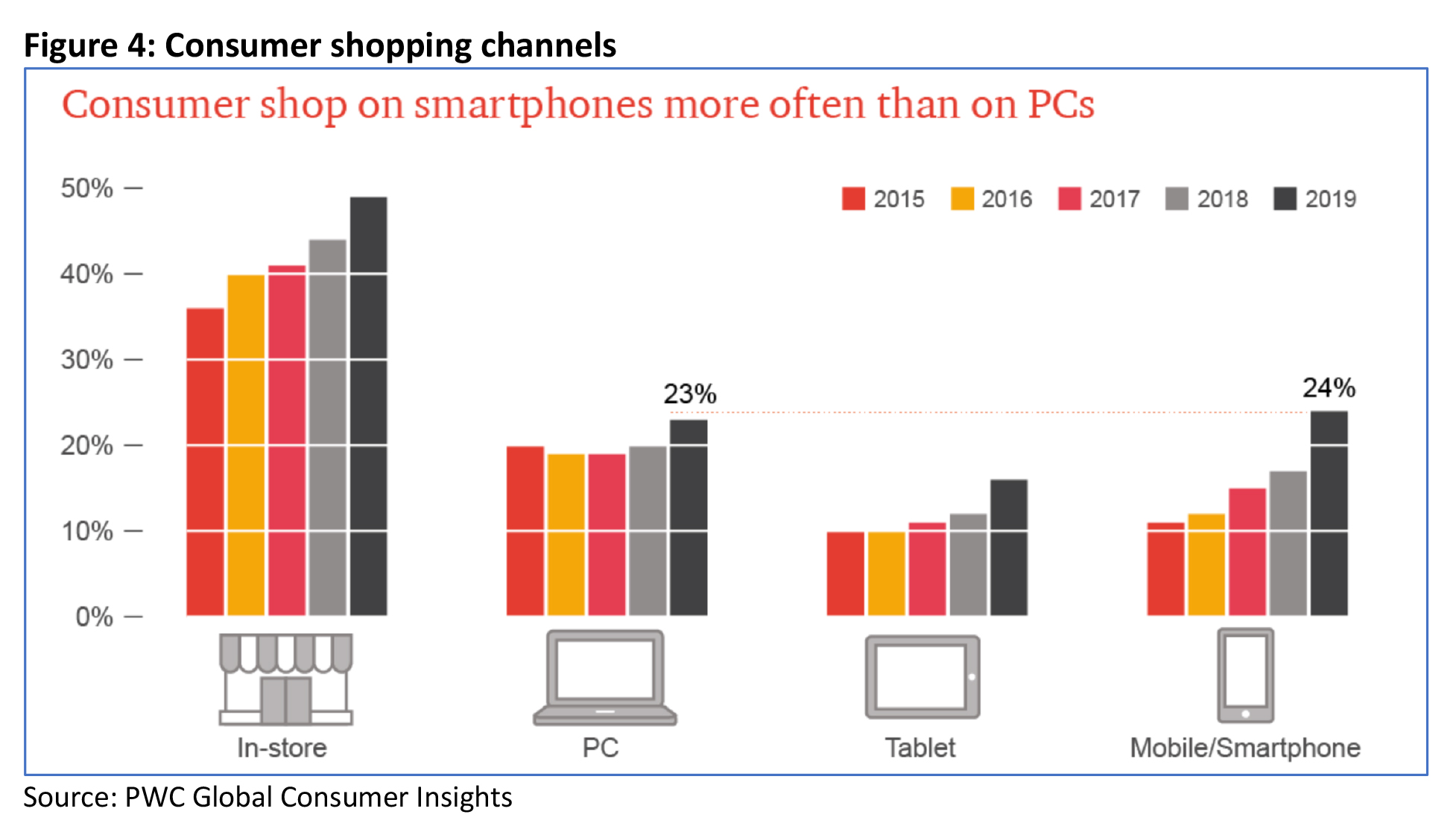

As Figure 4, based on PwC research[7] shows, online shopping now outstrips ‘bricks and mortar’ shopping, and more purchases are made via mobile phones than via desktop computer.

However, the same research also concluded that brands needed to have a good mix of technology and staff, and in particular, have technology that empowered employees to provide superior service.

This was seen to be especially true for financial services, where only 15% had purchased insurance via a digital channel, only 13% had obtained a loan and only 12% made a financial planning decision online. It was observed that the financial services category is one in which consumers would benefit from more education, and thus “a blended experience, where in-person interaction is mixed with digital experiences throughout the journey, can prove far more fruitful.”[8]

CoVid 19 has undoubtedly acted as a further catalyst for the digitalisation of the advice offering, with virtual meetings becoming the norm for many. In the future, expect the power of mobile technology to be leveraged not just for customer communication, but to bring unprecedented speed, and convenience to the claims and underwriting processes too.

In conjunction with other technology, phones could be used to measure height, weight, heart rate and blood pressure, monitor moles and skin lesions, and assess injuries. And, if centralised, comprehensive online health data becomes a reality, the personal statement and claim form could well become a thing of the past. As well as the improved experience, the efficiency benefits of such innovation can be enormous. Research by McKinsey[9] estimates that this type of digitalisation of the underwriting and onboarding processes can improve turnaround times by 50 to 70% and reduce administrative expenses by 20 to 30%.

The economics of life insurance is being disrupted

The economics of life insurance has become more challenging in recent years, driven by a number of factors including a sustained surge in mental health related claims, the ageing of portfolios, and disruption to distribution models. The scale of these challenges is reflected in the financial results reported by insurers in recent periods. As the 2018/19 data in Figure 5 below shows, one year after reporting a small profit of $34.1m (after tax), the Australian life industry made a loss of almost $1.3b on risk products.

As has been extensively reported, the main driver of these results has been the claims experience of individual disability income products. The 2019 loss of nearly $1.5b adds to more than $3 billion in losses accrued over the prior 5 years and illustrates the extent to which claims experience – particularly mental health related claims – are running way ahead of the expectations reflected in premium rates.

Mental health claims

The increasing prevalence of mental health claims is unlikely to be a temporary phenomenon. A variety of indicators suggest our mental health continues to deteriorate. In particular, anxiety and depression rates are continuing to increase[10]. According to Australian Institute of Health and Welfare (AIHW) data[11], the proportion of the population using Medicare subsidised mental health specific services grew from 4.3% in 2008/9 to 8.7% in 2018/19. The number of GP consultations to prepare mental health plans has grown from 813,257 in 2012 to 1,191, 786 in 2016. This upward trend is likely to continue.

Ageing books

The ageing of the overall population is mirrored in existing life insurance portfolios, and to the extent that cover becomes more expensive with age, this in turns creates an additional pressure on lapse rates, with affordability of cover becoming a major issue for some older policyholders. Insurer data shows that whilst adviser-initiated lapses have decreased significantly in recent years, customer-initiated lapses are now increasing, and this is reflected in an increase in overall lapse rates as reported by APRA[12].

Distribution disruption

All three life insurance channels – retail, group, and direct – have faced disruptive forces in recent times.

By far the most important channel for most insurers is the retail/advised channel, a channel currently undergoing unprecedented levels of change. Licensee consolidation and new professional development (FASEA) requirements are amongst the forces that have seen significant attrition in adviser numbers, especially those specialising in risk (who are also adjusting to LIF mandated commission caps).

The group channel has also come under pressure recently, with the ‘Protecting your Super’ changes becoming law in 2019. This legislation changed the rules around default cover for under 25s and small balance accounts and reports[13] suggest hundreds of thousands of fund members have lost their cover as a result. As well as reducing the size of group portfolios, this change also saw a reshaping in their age profile, skewing them older, and necessitating the remodelling of pricing for many funds.

As to be expected when distribution capacity is removed from the market, sales volumes have been impacted, and data released at the end of 2019 showed life insurance sales to be at their lowest level in five years[14].

The combined impact of these seemingly disparate changes – in sales volumes, lapse rates, age profiles and claims experience – is to completely change the financial dynamics of life insurance portfolios. Ensuring the sustainability of risk books will in many cases require insurers to revisit not only premium rates but also benefit design.

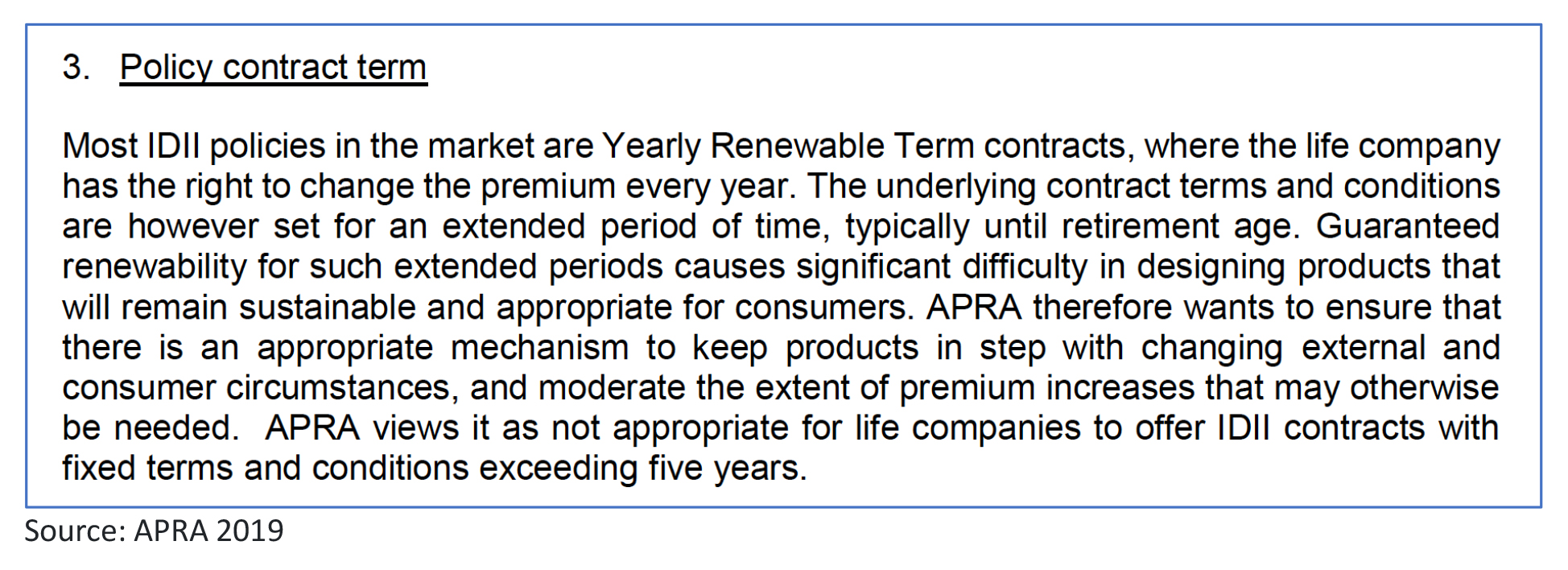

In the case of individual disability income, the urgency to address its sustainability challenges prompted APRA to intervene at the end of 2019, mandating a raft of changes to pricing, benefits, capital requirements and contract structures. Whilst the headline change from APRA was the outlawing of agreed value policies, arguably the most substantial change – and one which could be a pointer for future product design – was the granting insurers flexibility to review contract terms, including benefit periods, once a policy was already in force. An extract from APRA’s letter[15] to insurers on this topic is shown below.

Granting such flexibility across all products would be an exciting development for insurers, advisers and customers, as the ability to mitigate risk and reassess the appropriateness of benefits at periodic intervals will encourage more innovation and experimentation in new product design, and give insurers the ability to use options other than premium increases to secure the sustainability of a product and a portfolio.

The regulatory framework continues to evolve

Whilst regulatory change is nothing new for financial services, the volume of change currently faced by the industry is without recent precedent, and this is especially true of life insurance.

In addition to the LIF, FASEA, and Protecting Your Super changes already discussed above, a number of other changes are on the horizon, including a series of recommendations from the Hayne Royal Commission.

Probably the most significant of these from a product design perspective is seen in the Design and Distribution Obligations and Product Intervention Powers legislation, passed in April 2019.

Applicable to all financial products including insurance, asset management, and superannuation, this legislation was in essence a response to concerns about certain classes of product – especially ‘add on’ insurances – that were seen to deliver particularly poor value to customers either because of low claims rates, restrictive contract terms or inappropriate sales practices.

Central to the legislation is the requirement for product issuers to clearly articulate the type of customers for whom the product is designed – and conversely those for whom it is inappropriate – via a publicly available ‘Target Market Determination’ (TMD).

Another key concept within ASICs draft guidance[16] on this legislation is ‘Choice Architecture’, meaning “the environment, noticed and unnoticed, that influences consumer decisions and actions”. It includes sales processes, but also design decisions regarding the bundling of products and benefits, the complexity of design, and default settings for certain features.

These new obligations on issuers – and distributors – apply from October 2021.

A further change emanating from the Royal Commission is the extension of the Unfair Contract Terms (UCT) regime to include life and general insurance contracts. This change will deem any terms to be unfair – and thus providing grounds for the contract to be voided – if they lead to a significant imbalance to the parties’ rights and are not reasonably necessary to protect a legitimate interest. This will place additional pressure on product manufacturers to not only consider policy terms very carefully when launching new products, but to also ensure those terms remain contemporary and appropriate throughout the life of a policy, for example in response to medical and societal changes.

The dawn of an exciting new era for advisers and customers

Notwithstanding the significant disruptive forces currently facing life insurers, the outlook for product design is exciting, as the breadth of change forced upon the industry is matched by powerful enablers of innovation, such as big data, Artificial Intelligence (AI) and digital technologies.

The ability to collect and extract insights from data at a more granular level – thus massively improving insurers’ understanding of micro influences on mortality and morbidity – will make it easier for insurers to price risk at a truly individual level, in turn enabling them to make cover more accessible and affordable for many older customers, or those affected by ill health.

Coupled with systems which make modular product design quicker, easier, and more economically viable, and digital interfaces which leverage the power and ubiquity of mobile devices to simplify application and claims processes, it seems likely that we are at the dawn of a new era for life insurance product design.

Spurred on by competitive pressures, this era is likely to see a genuine, deep customer focus matched with new levels of agility and innovation amongst life insurers, equipping advisers with an ever-bigger armoury of options to support their advice, via a service delivery framework which can help drive practice efficiency.

![]()

———-