The value of sustainable dividends

To access a sustainable dividend style portfolio find an active manager that specialize in this style.

Companies that exhibit sustainably growing dividends do not seek to generate a high income stream, nor do they try to be the fastest growing businesses. Sustainable dividend growth is a total return focused equity strategy with defensive characteristics. Dividend growers tend to preserve capital relatively well in downturns and this low volatility approach can lead to considerable outperformance over a market cycle. They seek superior downside protection and an attractive risk/reward profile.

Dividends are paid to shareholders from company profits. So, for long-term investors, profit after tax is the material metric in any set of accounts because that figure is essentially the amount of new equity capital that has been generated in the course of the business plying its trade.

One of the most important decisions for a company’s board and management team is how best to deploy that new equity capital. Broadly speaking there are two options: distribute it to shareholders; or retain it in the business and put it to work in fueling expansion, making acquisitions, developing products and services, or repaying debt.

Companies with growing demand for their products need to retain most of their net income to fund expansion, with the majority of high-growth businesses reinvesting all their profits in the early years, and sometimes even asking investors for extra capital to supplement it. More established, successful companies will achieve the happy outcome of generating sufficient amounts of cash to fund their growth with enough surplus to pay dividends to shareholders.

Those dividends reward investors for the risk they took in buying shares in the company and the payments have come to be accepted by both parties as a virtual covenant. Dividends are the ultimate expression of faith in the future prosperity of a company. As such, once they have been embarked upon, boards and management need to be confident those payments can be sustained.

Company Executives need to manage their businesses wisely to be confident that their future cash flows can maintain and grow dividends. Once a dividend stream is underway, the market will punish any company that cuts their dividend. It is a self-imposed discipline on executives and boards to place cash back to shareholders. Their other options would be to fund acquisitions which may have an uncertainty of outcome, buyback shares, usually to improve executives’ payments and bonuses or sit on cash. Dividend growers have a highly loyal shareholding base that is less susceptible to market price volatility.

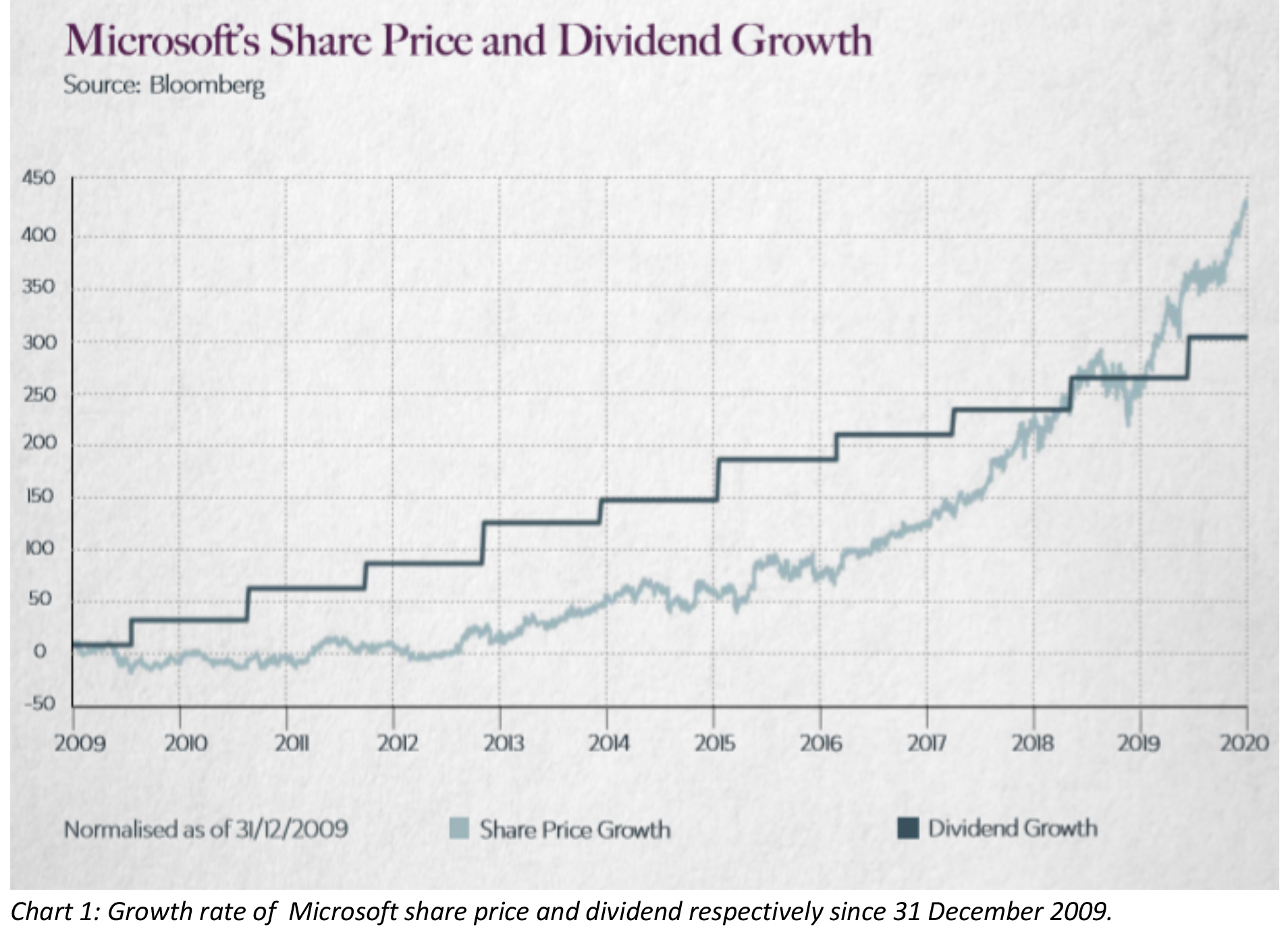

Microsoft is a case in point. The company has proven resolutely committed to growing its dividends, while simultaneously maintaining a high growth profile with new investments in the cloud business. Its solid fundamentals and strong governance make it extremely unlikely that the company will forego on its commitments. Its positioning at the edge of cloud computing, meanwhile, makes its stock an exciting growth prospect.

Interestingly, dividend growers do not typically provide the highest yield in the market. Many of the highest yielding companies are in mature industries and are companies with lower prospects of capital growth, offering a higher payout ratio to income hungry shareholders. This is at the detriment to future growth of our client’s portfolio. A dividend trap is a stock that lures investors with a high yield only to result in a potential dividend cut or financial distress. Buying stocks with high yields can lead investors into troubled sectors. When a stock’s price declines, its yield will rise.

The company’s payout ratio is a proportion of profits paid out to shareholders in the form of dividends. A high payout ratio may not be sustainable and may lead to the dividend being cut. The payout ratio should be a disciplined ratio of reinvesting into the company for future growth and then rewarding shareholders after a margin of safety or business risk has been established.

During down markets dividend growers typically outperform and this was evidenced in the 2007-2009 financial crises. The dividend growers preserved capital better than the general market. It is during a severe downturn that strong balance sheets will weather the storm better than most.

Over the long-term, dividend growing companies typically hold up well in down markets and are capable of excess return over the full cycle.

A lower volatility portfolio with shorter draw down will have a better risk-adjusted return than a highly volatile portfolio. Over time, minimizing drawdowns can result in significant gains to investors. Combined with the compounding effect of reinvesting dividends this can provide a stabilizing core to an overall equity portfolio. Ned Davis Research Group provided a paper discussing why minus 1% plus 1% does not equal 0%. A 20% loss in our portfolio would require a 25% gain in order to recover. For example, if a $100 portfolio loses $20 the capital base has shrunk to $80. This requires that investment gains must be larger to offset the now smaller capital base. This is shown in the following equation:

Recovery gain (%) = drawdown loss % divided by (100% – drawdown loss). The drawdown loss is more costly for larger drawdowns than for smaller drawdowns. The larger the drawdown the longer the recovery time. This reinforces the importance of drawdown reduction strategies in active portfolio management to minimise the pain and time experienced from drawdowns. If an active strategy can reasonably reduce drawdowns, there are good gains to be made.

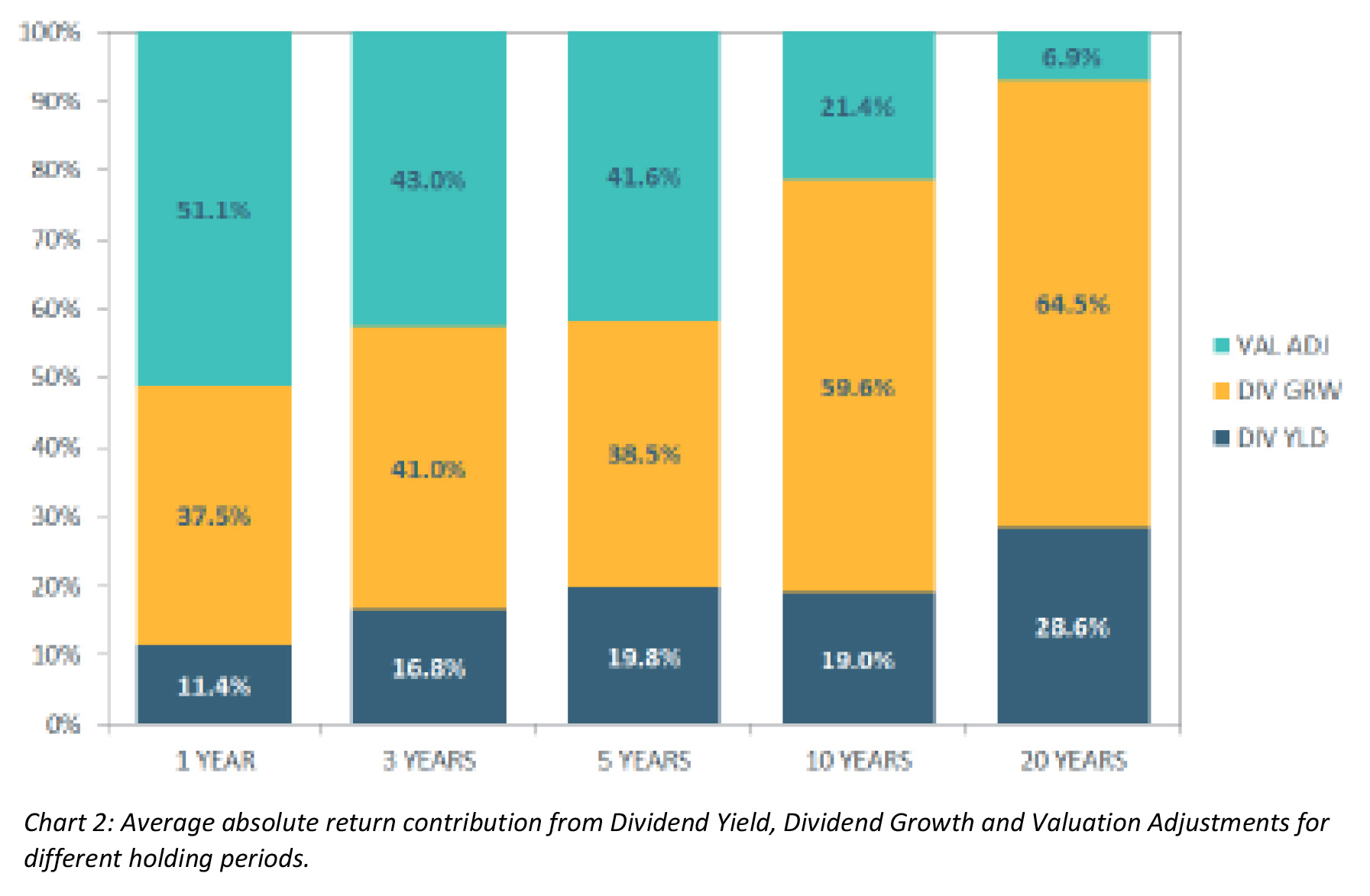

A study done by the Norwegian Ministry of Finance into global market portfolios to examine the key drivers effecting returns found the following; “The return contribution from dividend growth increased and valuation adjustments decreased with increasing holding periods during the last two decades“. Their examination covered the period of December 94 to December 2015 and found that dividend yield and dividend growth explained most of the return and risk in the long run. Over the past 20 years, global equity prices have grown approximately in line with dividends.

The return decomposition of ACWI equities is presented in Chart 2. Non-overlapping annual data for the 1-year horizon and overlapping annual data for longer horizons is used. This analysis covers the historical period Dec 1994 to Sep 2015 and shows that the average contribution of the valuation adjustment term to total returns became smaller as the investment horizon became increasingly longer. Valuation changes accounted for approximately 50% of total returns over 1-year periods while their contribution fell to 20% over 10-years and to less than 10% over 20-years, reflecting the declining importance of valuation changes over longer horizons. On the contrary, the average contribution from dividend growth increased with increasing time horizon. Dividend growth was the highest contributor to equity returns, accounting for at least 60% of total equity returns over 10-year and 20-year periods. Dividend yield is the second largest return contributor, explaining nearly 30% of the total ACWI returns over 20 years.

The above chart shows the significant contribution made by dividend growth to total return. The dividends are relatively stable component compared to valuations of stocks. Dividend growth per share accounts for 64.5% of total equity return in the long run (20 years).

During COVID, the dividend landscape has shifted. Previously, many listed companies were undertaking buyback programs, which we have observed a cessation of across the globe. We have observed government intervention by regulators to stop both buybacks and dividends for banks and those benefiting from emergency policies. We have already seen some dividend declines taking place. This may not necessarily be a bad thing during a period of uncertainty but is certainly worth keeping an eye on. Many are drawing down lines of credit to strengthen liquidity so there may be an overall deterioration of quality through this period. It will not be surprising to learn that many businesses are deeply troubled and the companies that did not have strong balance sheets before COVID will be struggling in this environment. Any company that had a strong balance sheet pre-COVID and has been able to maintain or grow their dividends throughout this period are prime candidates for investment. Unsurprisingly, these particular companies will be experiencing more stable or growing share prices.

Global dividends have fallen around 12% from 2019 run rate. This will likely be closer to a 20% decline once all declarations are known. Substantial debt issuing by companies across the globe may lead recovering cashflows.

Dividends are becoming a scarcer resource during the current COVID situation and looking into the future recessionary years but they will be an excellent barometer to assess a company’s health.

The S&P500 dividend futures contract tells an interesting story. $56 of dividend were paid on the index in 2019. In March, the futures were predicting an increase to $61.50 for 2020. By the market-low in April, that had become $40 and now sits back up at $56. For 2021 those figures were $64 in March, $35 in April and $51 now. In summary, the market is pricing in further cuts through this year and into next with 2022 being flat. The I.T. sector is certainly playing its part in keeping these dividends going accounting for around 15% of the total.

This suggests that through to the end of June, dividends have fallen around 12% on the prior year. With US dividends still having more falls to come (according to the futures anyway) and risks to the UK and elsewhere. With this is mind we might expect the 12 month run rate to get down to around $1150bn which would mean a 20% fall from the peak. That would take us back to 2016 levels but ahead of 2012.

Cross referencing to industry groups, a $150bn fall in dividends would be equivalent to around a 30% reduction in Financials and Energy dividends with all others balancing out to net zero. Looking ahead, US banks paid out dividends in Q1 which were substantially higher than profits for that quarter which was only just impacted by COVID-19, so we can expect to see more cuts there.

Many Energy companies have yet to decide on future dividend policy and with that sector accounting for 11% of global dividends there is more scope to the downside.

In summary:

- Global dividends have fallen around 12% from 2019 run rates.

- Likely this will be closer to a 20% decline when all declarations are revisited in Q1 of 2021.

- While there is potential for a European dividend rebound from politically depressed levels in 2021 (see below), recovery in US pay-outs may take longer.

- Substantial debt issuance by companies across the globe may lead recovering cash flows to be prioritised for debt repayment before dividends are reinstated or increased. It will take time to rebuild dividend cover, therefore, for dividend growth to pick up a considerable earnings recovery is needed.

In summary, a portfolio that focusses on the most stable and predictable component of return, dividends, is likely to produce a more defensive portfolio with better downside capture. Moreover, a process that focusses on the sustainability of dividends into the future has a higher probability of success than a passive, backward-looking index strategy.

Dividends are not only a reward for investors, but a statement of confidence by company management and directors; a declaration of strength and unwavering belief in the business’s fundamentals. Dividends send a clear message about the company’s current and future performance and its capacity for protecting shareholder value.

To access a sustainable dividend style portfolio, you will find there are some active managers that specialize in this style and they offer both managed investment trusts and ETFs will soon be available. Passive ETF options are also available, however they are backward-looking at historical dividends paid, rather than forward-looking to anticipate the winners and losers in the market.