US 2020 presidential election: What policy means for infrastructure investment

Sarah Shaw

The November 2020 US presidential election is between two polarising individuals in Donald Trump and Joe Biden, who represent very different views and approaches to leading the US for the next four-year presidential term. The policy positions of the two parties are likely to have far-reaching impacts on the US and global economy; and specifically, infrastructure investment.

In this article, Senior Investment Analyst Peter Aquilina and Global Portfolio Manager Sarah Shaw analyse the positions of each of the Republican and the Democratic parties on key policy issues. We then go on to analyse the potential impacts these policy outcomes could have on US infrastructure investment and specific sub-sectors.

1. The most polarising presidential election in recent US history

The presidency of Donald Trump has been one of the most polarising in America’s recent history. In the past 70 years there has never been a greater divergence between Republican and Democratic voter approval ratings of the sitting president, as depicted in Chart 1 below. This difference in voters’ perception of the sitting president along partisan lines seems to be a trend which began with the Clinton presidency in 1993 and has grown since.

This election is likely to have significant ramifications domestically, but also at an international level. The United States’ approach to managing and mitigating the COVID-19 pandemic and its ongoing relationship with rising super-power China are likely to have far reaching global implications that could be heavily influenced by this election.

The ability of either party to exercise its policy objectives and pass its own legislation, without cross-party negotiation, is reliant upon winning the majority of seats in both chambers of Congress – the Senate and the House of Representatives (the House).

The most likely outcomes at this stage appear to be:

- Mr Biden wins the presidency but fails to win the Senate – resulting in split Congress with required negotiation in passing legislation;

- Mr Biden wins the presidency and also wins the majority in both the Senate and the House – providing a ‘Blue sweep’ and allowing for greater implementation of policy;

- Mr Trump retains the presidency but doesn’t win the House – making negotiation with Democrats necessary to implement legislation.

The other possible outcome, but considered unlikely at this stage, is Mr Trump retaining the presidency and winning back the House. This would see a period similar to Mr Trump’s presidency before the midterm elections, where the Republicans had sufficient power of Congress to implement their policy.

Unfortunately getting clear, concise policy positions has been difficult during this election. In this article, we try to cut through the politics of personality and the populism embedded in the campaign, to focus on communicated and implied policy, and what impact we believe it will have on infrastructure investments in the US. While our policy comparisons may not be exhaustive, we hope this highlights the important and fundamental differences between the candidates.

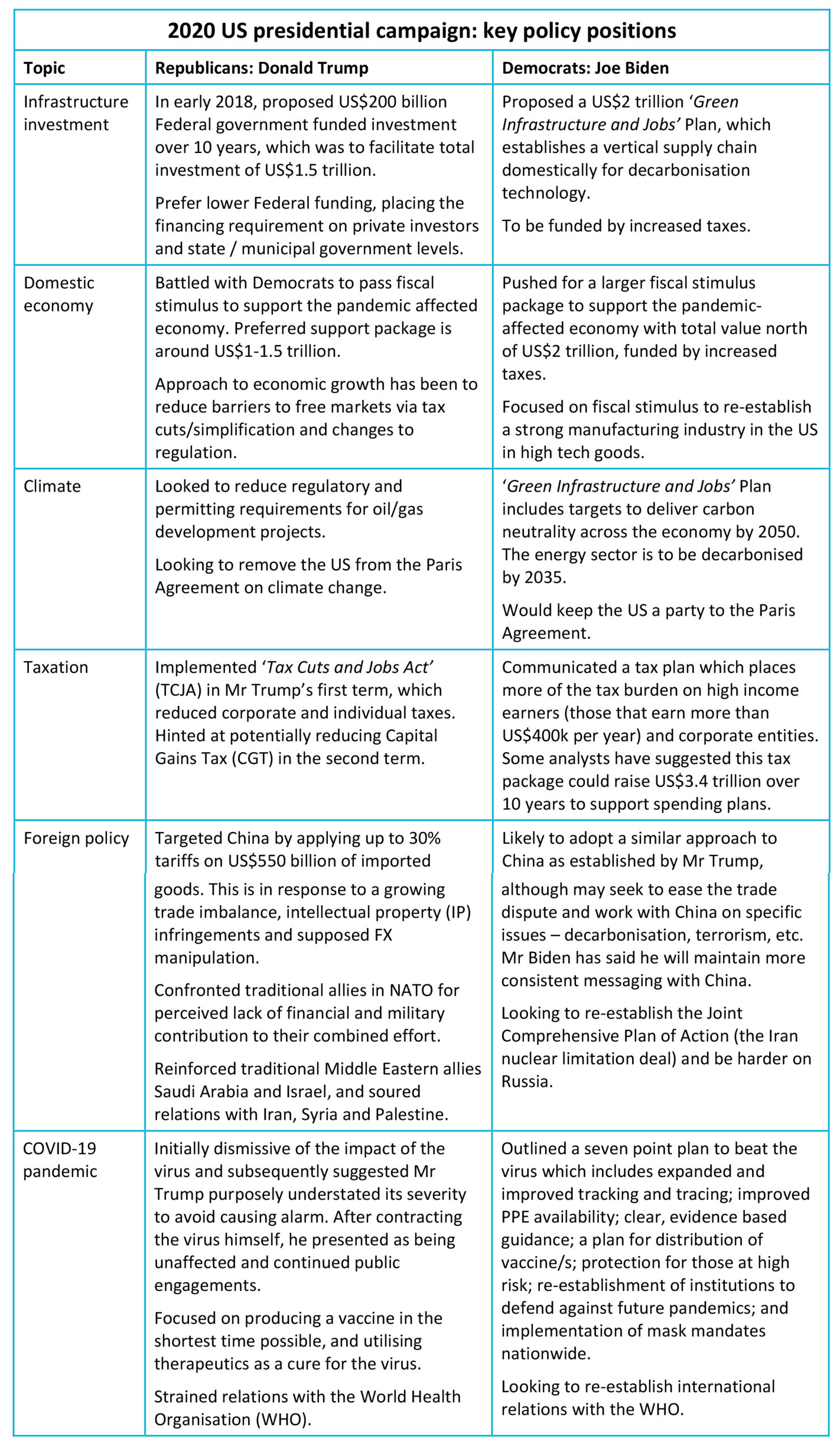

2. Summary of key policy positions

3. Detail on the key policy positions

Support for infrastructure investment from both the Republicans and the Democrats

There is general agreement between the Republicans and the Democrats that the US is in dire need of spending to upgrade ageing infrastructure and invest in new infrastructure to support future generations. However, no major infrastructure legislation has been passed in Mr Trump’s first term as a result of disagreements over what projects to spend on, how much to spend and how to pay for it. Mr Trump has focused on reducing permitting requirements, incentivising private investment and supporting the oil/gas sector, where the Democrats are more supportive of larger fiscal programs focused on decarbonisation.

Republican plans

In February 2018, President Trump released details of a long-awaited infrastructure plan which included federal spending of US$200 billion over 10 years, but was designed to facilitate investment of US$1.5 trillion over the same period. The plan involved focused spend on areas that incentivised state, municipal and private investment. Within the proposed legislation was the call to expedite the federal permitting process for projects – creating a ‘One agency, One approval’ process. This was to eliminate redundancies and duplication between state and federal authorities. The plan couldn’t attain cross party support in Congress, as the Democrats felt Mr Trump’s plan ‘shifts the burden onto cities and states’ and didn’t actually facilitate considerably more spending[1] .

Since the mid-term elections, where the Republicans lost control of the House, Mr Trump has had to manage infrastructure directives through executive orders. These directives are largely aimed at reducing and expediting perceived overly onerous regulation and approval/permitting processes. The effectiveness of these orders has been limited due to state-based permitting requirements and long, expensive legal processes initiated by project opponents – often environmental lobby groups. Mr Trump is likely to continue efforts to minimise regulation and red tape in a second term as President.

Democrat plans

In July 2020, the Democrat-led House passed the ‘Moving Forward Act’. This bill looks to facilitate US$1.5 trillion of investment to create roads and transit; reduce pollution; support water projects; build affordable housing; roll out universal broadband; develop schools; and upgrade hospitals. Criticisms from Republicans centred on the debt burden created by the spend; it didn’t seek ‘market-driven, collaborative, bi-partisan solutions to improve our infrastructure’; and it was too focused on green initiatives. Although this bill will not make it past the Republican-controlled Senate, it does show the likely policy trajectory that the Democrats will pursue with infrastructure legislation.

If the Democrats win the presidential election and control of Congress, they are likely to take steps to implement legislation based on their ‘Green Infrastructure and Jobs’ Plan. This plan has many common elements with the ‘Moving Forward Act’, but places more of an emphasis on decarbonisation and establishing supply chains within the US. It envisages spending US$2 trillion over the first four-year term of a Biden presidency, looking to build modern infrastructure facilities with a focus on locally developing clean, technologically advanced energy generation, storage/batteries and electric vehicles (EVs) to facilitate decarbonisation. In addition, Mr Biden’s plan again talks about rebuilding roads and bridges, improving the rail network, developing schools, improving water networks and rolling out universal broadband. This vast investment in infrastructure is intended to create at least five million US jobs and be financed by higher taxes for corporates and high income earners.

Managing climate change

Republican position

Based on public statements, Mr Trump appears to feel climate change is a secondary concern. He announced his intent to leave the 2015 Paris Agreement on climate change mitigation soon after taking office in June 2017 – the US will formally leave the agreement on 4 November 2020 if the withdrawal notice is not retracted prior.

In his first term as President, Mr Trump has also signed numerous executive orders, presidential memorandums and taken other actions to reduce environmental regulations and protections, and support the traditional oil and gas industries.

Democrat position

In contrast, Mr Biden has announced ambitious carbon reduction targets and a spending plan heavily anchored to the implementation of ‘greener’ energy solutions such as renewables, batteries, energy efficiency technologies, and other state of the art technologies.

According to the Democrats’ Unity Task Force (a group established to unite the moderates and progressives within the Democrats) memorandum ‘The Unity Task Force recommends re-joining the Paris Climate Agreement and seeking higher ambition on Day One’, Mr Biden and the Democrats have committed to achieve carbon neutrality across the US economy by 2050. The task force’s recommendations include:

- Eliminate carbon pollution from the power sector by 2035 through the utilisation of carbon neutral technology standards and energy efficiency;

- Dramatically expand solar and wind energy development through community-based utility scale systems;

- Build a modern electric grid that connects communities and powers them with clean energy;

- Adopt scaled-up tax credits for renewable energy projects that meet certain labour standards;

- Achieve net-zero carbon emission from new buildings by 2030;

- Within five years make energy savings upgrades to two million households and affordable/public housing units;

- Reduce methane emissions through robust federal standards and targeted support for repairing and replacing ageing distribution systems;

- Invest in R&D to develop technologies focused on reducing and removing carbon from industrial processes, often through the expansion of cutting-edge technologies such as carbon capture and hydrogen development; and

- Accelerate the adoption of zero emission vehicles through incentives and subsidisation.

The required investment associated with these targets is included in the ‘Green Infrastructure and Jobs’ Plan. This will be financed on the Federal government balance sheet.

Economic growth and taxes

Republican position

The economic focus of Mr Trump during his first term as President has been to minimise regulation and reduce taxes for corporations and individuals, believing this facilitated job growth and economic prosperity prior to the outset of the COVID-19 pandemic in the US.

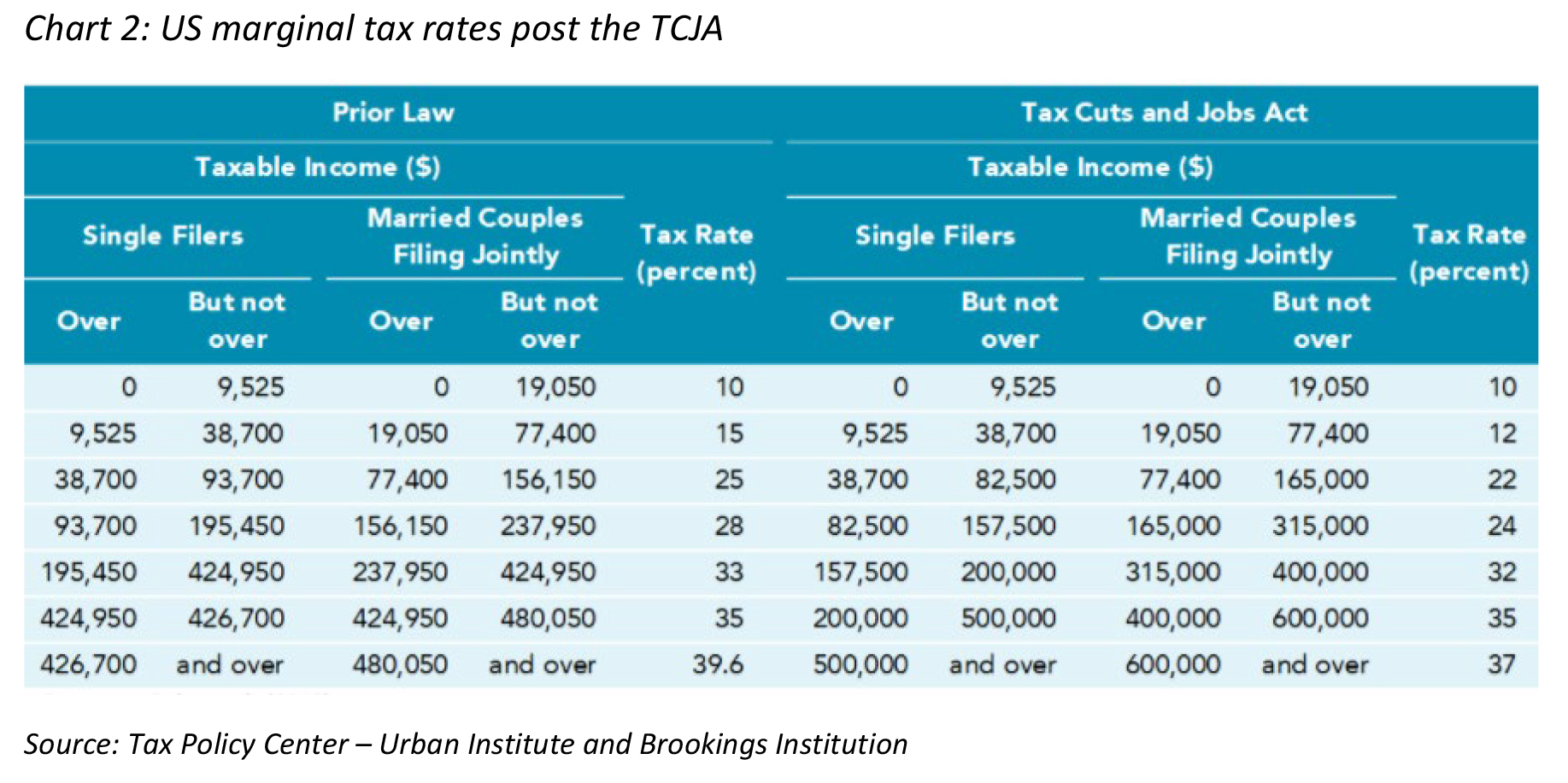

Prior to the midterm elections, the Republicans controlled Congress and were able to pass the TCJA legislation and have it signed into law in December 2017. The TCJA represented the most significant reforms to the American tax code since 1986, cutting the level of taxes across the board and simplifying the filing of tax returns. The TCJA:

- Cut the headline corporate tax rate from 35% to 21% – in doing so reducing the amount of itemised deductions for state and local taxes and other deductible taxes such as mortgages;

- Maintained seven tax brackets but reduced the marginal rate on all but the lowest – Chart 2 shows the updated marginal tax rates[2] ;

- Increased the size of the standard deductions by 85% – therefore incentivising less people to undertake itemised deductions, which simplified the filing of tax returns; and US

- Increased the income thresholds for different levels of Capital Gains Tax (CGT) – this reduced the tax burden of higher income earners (with incomes above $400,000) from CGT.

Since the passing of the TCJA, Mr Trump has hinted at further tax reform legislation, but to date hasn’t provided specific details. He recently suggested he may look at CGT again. Cutting the 20% highest marginal CGT rate would require a change in legislation, but advisors have suggested he could execute an executive order which indexes the original purchase price of an asset, reducing the capital gain liability when the asset is sold[3] .

Democrat position

Mr Biden’s plan to rebuild the economy post the COVID-19 pandemic sounds similar to Mr Trump’s ‘America First’, with a focus on US-based manufacturing and anti-globalism ideals. Mr Biden’s website[4] states: ‘Biden does not accept the defeatist view that the forces of automation and globalization render us helpless to retain well-paid union jobs and create more of them here in America. He does not buy for one second that the vitality of U.S. manufacturing is a thing of the past’. His economic plan incorporates developing and supporting manufacturing and innovation through the development of supply chains in the US, in doing so creating employment opportunities which will be heavily influenced by unions, including:

- Make “Buy American” real with a US$400 billion procurement investment – this will power new demand for American products, materials and services;

- Re-tool and revitalise American manufacturers – with a particular focus on smaller manufacturers, through specific incentives, additional resources, and new financing tools;

- Make a new US$300 billion investment in Research and Development (R&D) and breakthrough technologies – to be spread over numerous sectors but with a focus on those that will support the decarbonisation process, such as the development of EVs.

It is believed these planned investments are encapsulated in the proposed US$2 trillion of fiscal stimulus to be spent over the first four-year term of a Biden presidency. According to the website, this overall plan is targeted to deliver at least 5 million jobs in addition to those lost this year through the pandemic.

The obvious question is how Mr Biden plans to finance this massive investment, and it seems clear that high income earners and corporations would fund the bulk of the cost. The Penn Wharton Budget Model’s report estimates that Mr Biden’s tax plan would raise an additional US$3.4 trillion in tax revenue over the next 10 years, with specific components of the plan including:

- Increasing CGT from 20% to 39.6% (the highest personal tax bracket) for high income earners – Mr Biden is suggesting taxing capital gains at the highest tax bracket for individuals who make more than US$1 million in gross income per annum;

- Increasing the marginal tax rate for the highest income bracket from 37% to 39.6% – this essentially reverses the income tax reduction allowed as part of Mr Trump’s TCJA legislation for citizens with gross incomes above US$400,000;

- Capping the value of itemised deductions to 28% – the preparation of US tax returns allows for the option of a standard deduction or itemised deductions for things like state level taxes, mortgage interest, charitable donations and medical expenses. Higher earners overwhelming elect to use itemised expenses as it is more advantageous for them to do so; and

- Increasing the corporate tax rate from 21% to 28% – partially reversing the corporate tax rate reduction implemented by the Republicans through TCJA. Prior to TCJA the rate was 36% but allowed for the deduction of state level taxes, which is unlikely to be the case in the Biden proposal.

Foreign policy

Republican position

In 2017, Mr Trump came into office promising to disrupt the status quo and introduce an ‘America First’ foreign policy. This approach has had far-reaching impacts for the likes of Iran, North Korea, Syria, Afghanistan and Iraq, as well as traditional allies such as some European states and other North Atlantic Treaty Organisation (NATO) partners. However, the greatest focus for the infrastructure sector is the relationship with China.

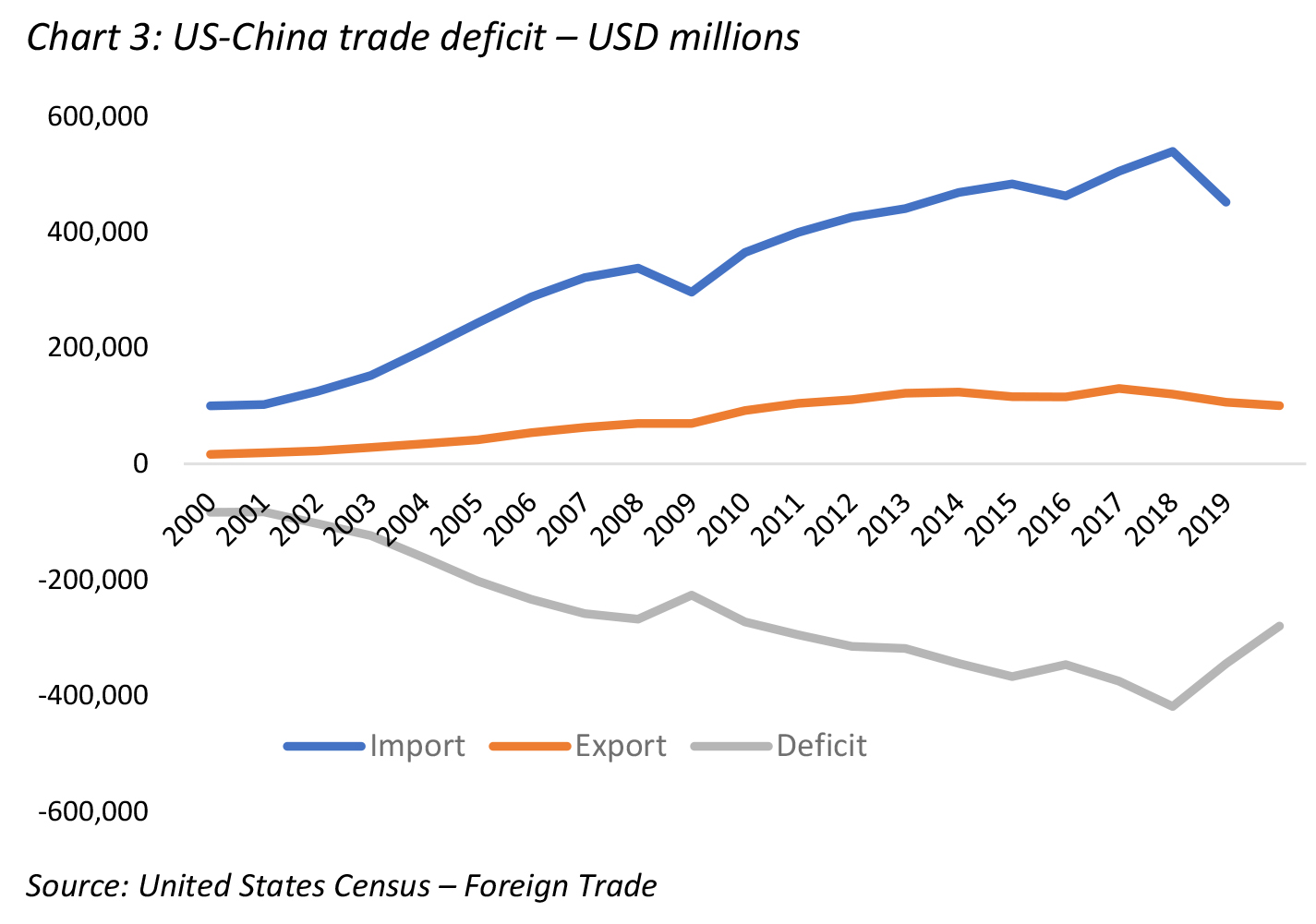

Mr Trump has always dissented from the ‘free trade consensus’ to which China is central, and this was arguably the basis on which he was elected to office in 2016. China has now become one of the central foreign policy topics in the 2020 campaign, heightened by the US/China trade war as well as questions of China’s handling of the COVID-19 pandemic.

To date there has been little sign of economic decoupling from China. The US trade deficit with China peaked in 2018 at net imports of US$429 billion. Significant progress was made in reducing the trade deficit in 2019, reducing it to US$345 billion (see Chart 3 below). Interestingly, the overall US trade deficit in 2019 actually increased compared to 2018, implying Mr Trump shifted the imports away from China to other countries and highlighting that the US remains dependant on the global economy.

Trade relations between the two countries were arguably on the mend following the signing of Phase 1 of the US-China trade agreement in January 2020. Phase 1 requires the Chinese to purchase at least US$200 billion in US products over 2020 and 2021 – Chart 3 below indicates this is not a significant ask, with the US export of goods to China having been above US$100 billion per year since 2011.

China’s role in the outbreak of COVID-19 and its perceived mishandling of the situation has soured already tenuous relations between China and the rest of the world. Although tensions are high, both countries understand the debilitating economic impact of their feud. A 2019 report from Bloomberg Economics estimates the trade war and tariffs placed on the import/export of goods and services between the countries cost the US economy $134 billion by December 2019, and will likely cost $316 billion by the end of 2020. Ultimately we see economics prevailing, but not without ongoing tension and flexing of muscle by the two superpowers.

Democrat position

The adoption of a tougher, more adversarial stance towards China is likely to be maintained by a Biden government. It seems the Democratic Party establishment has come around to Mr Trump’s approach on an array of issues relating to China, pledging to continue curbing China’s influence in high-tech sectors; and even refusing to revoke Mr Trump’s adopted heavy tariffs on Chinese imports. As such, we do not see the ‘China policy’ as a swing for the election.

4. What does this mean for infrastructure fundamentals?

It’s hard to find a middle ground between the majority of Democratic and Republican party policies on which to pass legislation. However, the exception could be legislation supporting investment in much needed infrastructure, as both parties can agree on the need for it.

A second Trump term

In an environment where legislation stalls, it’s possible Mr Trump will continue to use executive orders and other powers available to him. However, this scenario would likely not vary the fundamental earnings of infrastructure companies compared to the status quo environment. Below we analyse the impact on specific infrastructure sub-sectors should Mr Trump retain the presidency.

US utilities

US utilities’ earnings have held up well during the COVID-19 pandemic, with the large majority confirming 2020 earnings guidance. This is likely to be one of the few industry sectors that will continue to grow earnings in line with expectations even in the scenario of a protracted weak economic environment, which could develop under either presidency if the two parties cannot agree on the passing of a much-needed fiscal stimulus package.

In the scenario that the economy remains depressed and in the absence of significant fiscal stimulus, it could be a ‘lower for longer’ scenario for base Treasury rates. US utilities tend to perform better in these environments as debt raised to finance significant capital programs comes with relatively low interest costs, and low Treasuries are reflected in discount rates supporting company valuations.

Should a stimulus package be agreed, it’s likely that US utilities will continue to deliver on earnings and growth expectations. The strengthened economy from the stimulus package could support customers’ ability to pay for bill increases to facilitate required investment. They will also continue to benefit from state-based ‘green’ targets, regardless of Mr Trump’s views regarding the decarbonisation thematic.

US oil/gas midstream

Despite the efforts of Mr Trump to reduce permitting and regulation in the development of oil/gas pipelines, it’s likely that new developments will continue to face difficulties. State-based permitting requirements, and legal objections initiated by environmental groups, are likely to continue to impede pipeline development.

Based on current expectations for oil and gas demand in the US and globally, there will be limited opportunities for additional gathering & processing and transportation pipeline capacity across the US. The decarbonisation momentum, existential of additional federal government support (similar to that proposed by Mr Biden), is likely to limit oil/gas demand in the medium to long term.

If Mr Trump can mend trade relations with China, increased liquified natural gas (LNG), oil and other hydrocarbon exports could provide additional stimulus for demand and support growth in the midstream sector.

US rail

US rail was one of the biggest winners within the infrastructure sub-sector when Mr Trump won the election in November 2016, as his communicated tax reduction plans during the election provided a direct earnings benefit for rail companies. In the trading week of Mr Trump’s election win, the US rail index – the S&P500 Railroads sub industry index – increased 8.6%. Combined with a buoyant economy during much of Mr Trump’s first term, this has supported rail company earnings.

Mr Trump hasn’t been explicit on further plans for corporate tax cuts, so the rail sector is unlikely to directly benefit as much from his second term as President. However, it won’t be hindered. The sector will be also looking for fiscal stimulus to support the economy, as this provides a strong link to rail volume haulage and company earnings.

US toll road investments

There are relatively few opportunities to invest in US toll road assets, and the majority of those in private hands are foreign owned (e.g. Transurban owns managed lanes in the USA). It’s expected that the earnings from US toll roads will improve as traffic numbers start to return to pre COVID-19 levels, which is likely to occur as vaccines for COVID-19 are made available and the economy recovers, driving traffic volumes. An economic recovery supported by fiscal stimulus legislation would also support traffic volumes, but it’s unclear when this will be achieved if Congress remains split.

The hope for additional road assets making it into private hands is largely a state-driven directive and will be unaffected by the election outcome.

Biden wins the presidency

Polls suggest that the big question for Mr Biden’s potential term as President is whether he can win a majority in the Senate and therefore control Congress to pass the Democrats’ desired legislation. Control, or not, of Congress will determine Mr Biden’s ability to execute his communicated ‘Green Infrastructure and Jobs’ Plan, with associated spend of around US$2 trillion. Mr Biden has also communicated his intention to pass legislation increasing the tax burden of corporations, among others. Changes to tax laws will also have significant impacts on some infrastructure sectors.

In the scenario that Mr Biden wins the presidency but fails to gain the majority in the Senate, he will have to negotiate with the Republicans to pass legislation. This scenario looks more like a Trump presidency without control of Congress. A middle ground will need to be found on new legislation, infrastructure support being one area in which this could be achieved.

US utilities

Mr Biden’s ‘Green Infrastructure and Jobs’ Plan will facilitate the expedited decarbonisation of the US energy sector. This plan will be implemented through various pieces of federal legislation which will overlay decarbonisation efforts mandated by state-based governments.

Utilities will be central to implementing these efforts. The process will require massive amounts of investment from utilities in the potential ownership of renewable generation/batteries to be developed; the build out and upgrade of the energy network; the replacement and upgrade of the gas networks to reduce methane leaks; and potentially the facilitation of EV infrastructure. Some of this required investment is likely to be incentivised through extended and expanded renewable energy tax credits, which could provide improved regulatory earnings growth for an extended period of time (to 2035 at least).

Mr Biden’s tax plan to increase the corporate tax rate to 28% should, all else being equal, support utility cashflows. Utilities in the US pay little in cash taxes because of the tax offsets and deferrals generated through their continued investment pipeline. The effective accounting taxes are a pass-through recovered in regulatory revenues. Under Mr Biden’s tax plan, revenues may increase for utilities (tax increase passed through to customers), while cash payment on taxes remain close to zero – improving cashflows while investment-driven tax offsets and deferrals exist.

The risk for utilities under a Biden government is that the combination of potential cost inflation associated with the fiscal stimulus, required investment in renewable generation/storage and the networks, and increased tax rates being recovered in revenues could all result in increasing customer bills. This could raise affordability issues for customers, and utilities will need to manage this by utilising any cost levers available – or in the worst case, reduce capex to limit customer rate shock.

US oil/gas midstream

The ‘Green Infrastructure and Jobs’ Plan is likely to speed up the transition from gas to renewables/batteries and potentially even hydrogen. This is likely to reduce commodity demand and utilisation by midstream assets over the medium to longer term, bringing forward terminal value dates.

To the degree that Mr Biden elects to moderate trade tensions with China, this could result in increased exports of oil/gas and other hydrocarbon commodities from the US to China. Exports of LNG are expected to utilise 7% of total US natural gas production in 2020[5] , and any increase from the opening of the Chinese market would be a significant driver of production over the near/medium term. Improved gas demand/supply would likely require midstream infrastructure support, providing a driver of growth in the sector. However, this could run into obstacles from Mr Biden’s conflicting ‘Green’ policy.

US rail

The rail sector is likely to be negatively affected by any increase in the corporate tax rate implemented by a Biden government. As the TCJA supported rail companies’ earnings when Mr Trump was elected, Mr Biden increasing the corporate tax rate would flow straight to company earnings.

Potentially providing some offset to this negative tax impact is Mr Biden’s ‘Green Infrastructure and Jobs’ Plan which, if passed, could stimulate the economy – resulting in improved rail volumes generally. However, roughly 10% of rail volumes are represented by coal, which is likely to become obsolete at a faster rate as a result of Mr Biden’s plan.

If Mr Biden can facilitate an improved trade relationship with China, this could also facilitate increased imports/exports from major US ports. Rail companies are central to transporting cargo from the shipping ports to demand centres. An improved relationship with China could therefore support rail volumes and earnings.

US toll road investments

As with a Trump presidency, a vaccine and/or fiscal plans should provide support for the economy and hence drive traffic volumes. However, Mr Biden’s tax plan would likely result in an increase in corporate taxes paid by toll road companies.

Again, the hope for additional road assets making it into private hands is largely a state-driven directive and will be unaffected by the election outcome.

5. Conclusion

The first term of Mr Trump’s presidency has been a turbulent one, but prior to the outbreak of COVID-19 the US infrastructure equity market performed well. Even through the pandemic, many US infrastructure sub-sectors delivered strong earnings and reinforced expectations for growth, highlighting the defensiveness and resilience of the infrastructure business model.

The upcoming election is filling newsfeeds domestically and globally. The Republicans and the Democrats have indicated very different policy objectives – the Republicans are focused on reducing regulation and taxes, while the Democrats want to implement fiscal policy aimed at decarbonisation. Both parties have indicated they will maintain an adversarial relationship with China, although will likely take different approaches. The big unknown is whether either president will be able to execute on any stated policies given a split Congress.

Importantly, both parties have indicated a desire to facilitate much-needed investment to replace ageing infrastructure and build for the future. Mr Trump has adopted more of a free market approach, where Mr Biden has indicated government fiscal support and subsidies. Both scenarios are likely to provide attractive opportunities for private infrastructure investment, if they can get them across the line.

We at 4D believe that during this uncertain period, with the potential for extended economic weakness, infrastructure provides a stable earnings proposition for investors. Stable growth is likely to be delivered irrespective of the election outcome, with the propensity for significant upside if fiscal programs are implemented to support the pandemic recovery and/or infrastructure replacement and build-out.

———