Togetherness drives us apart – rethinking estate planning in a COVID 19 world

Decisions, decisions, decisions…

COVID 19 has certainly brought families together. Massive job losses, mandatory working from home, and ongoing lockdowns and border closures mean Australians are spending more time together – and at home – than ever before. The composition of those households is also being reshaped across the country, as an estimated 300,000 adult children move back into the family home[1], bringing a buzz of activity back to previously empty nests.

But many of us aren’t happy about it.

Spending more time together can often magnify any relationship issues, turning small cracks into gaping fissures, and this certainly seems to be the case since COVID 19 first swung its wrecking ball in Australia. A study conducted in May 2020 by Relationships Australia[2], the leading national provider of relationship support services, found that 42% of people had experienced a negative change in their relationship with their partner during the previous few months. The Australian Financial Review reported that divorce rates were expected to double[3], and that family disputes between adult children and their parents over ‘home-sharing’ arrangements were an increasing cause of expensive, and bitter, court battles[1].

Amplifying some disputes, and undoubtedly making their resolution more complicated, is the strengthening of a trend that has been growing for some time – the blended family. Blended families – including stepfamilies – now account for around 10%, or 600,000, families, and according to experts, this reshaping of family structures is the main driver of an 80% increase[4] in legal disputes about estates and Wills over the last decade.

Proper estate planning, it seems, has become even more important.

Estate planning – a matter of life AND death

While the need for estate planning is driven by the increasing complexity of family structures, tax laws, and superannuation regulations, the essence of estate planning remains simple.

Estate planning is about an individual’s decisions – the making of those decisions, and the mechanisms designed to ‘enforce’ or enact those decisions and intentions when that person isn’t present themselves, due to either death or incapacity.

Many of these decisions relate to assets – such as homes, investments, and businesses –and who ownership of those assets is to be transferred to in the event of death. Guardianship of young children in these circumstances also needs to be considered.

Other decisions relate to a person’s residential, health care and financial arrangements in the event they lose their capacity to make those decisions themselves, perhaps, for example, of a condition like dementia.

Death, taxes, and other certainties

It is often said that the only two certainties in life are death and taxes. But that’s not strictly true. Because of the absolute certainty of death, we can also be reasonably certain that over the coming three decades we will see around $2.4 trillion in wealth passed down to Generations X and Y[5]. Similarly, we can be certain that around 80% of businesses (mostly small) will change hands over the next decade[6], representing an exchange of wealth of over $1.5 trillion.

There are two more certainties we can add to that list. The first is that, without robust estate planning, many of these transfers and exchanges will not go smoothly. The second is that if they don’t go smoothly, the time to resolve the inevitable disputes will be lengthy, and the associated legal bills will be very, very expensive (three days in court currently costing around $100,000[1]).

Indeed, research conducted on over 3,250 families who transferred wealth found that 70% of intergenerational wealth transfers fail because no preparation of the successors was taking place[7]

And yet despite this, it is estimated that close to half of all Australians do not have a valid Will[8].

Decisions, decisions, decisions

Having spent a lifetime building wealth, it’s only natural that we would want to direct how it is passed on after our death, whether that be to our surviving spouse, our children, or even to charities we support. But beyond decisions about ‘who’, we also need to consider the ‘how’, bearing in mind the following objectives:

- Ensuring that our wealth is passed on to intended beneficiaries, and not unintended beneficiaries;

- Minimising or avoiding taxes on wealth transferred;

- Allowing for any special future needs of our beneficiaries;

- Protecting our beneficiaries’ inheritance in the event of their divorce or bankruptcy ;

- Protecting beneficiaries’ inheritances from their own vulnerabilities, such as age, addictions, gambling and mental health issues; and

- Giving special consideration to a family owned business, in terms of the ability/desire of family members to carry on the business, and any complexities relating to multiple owners.

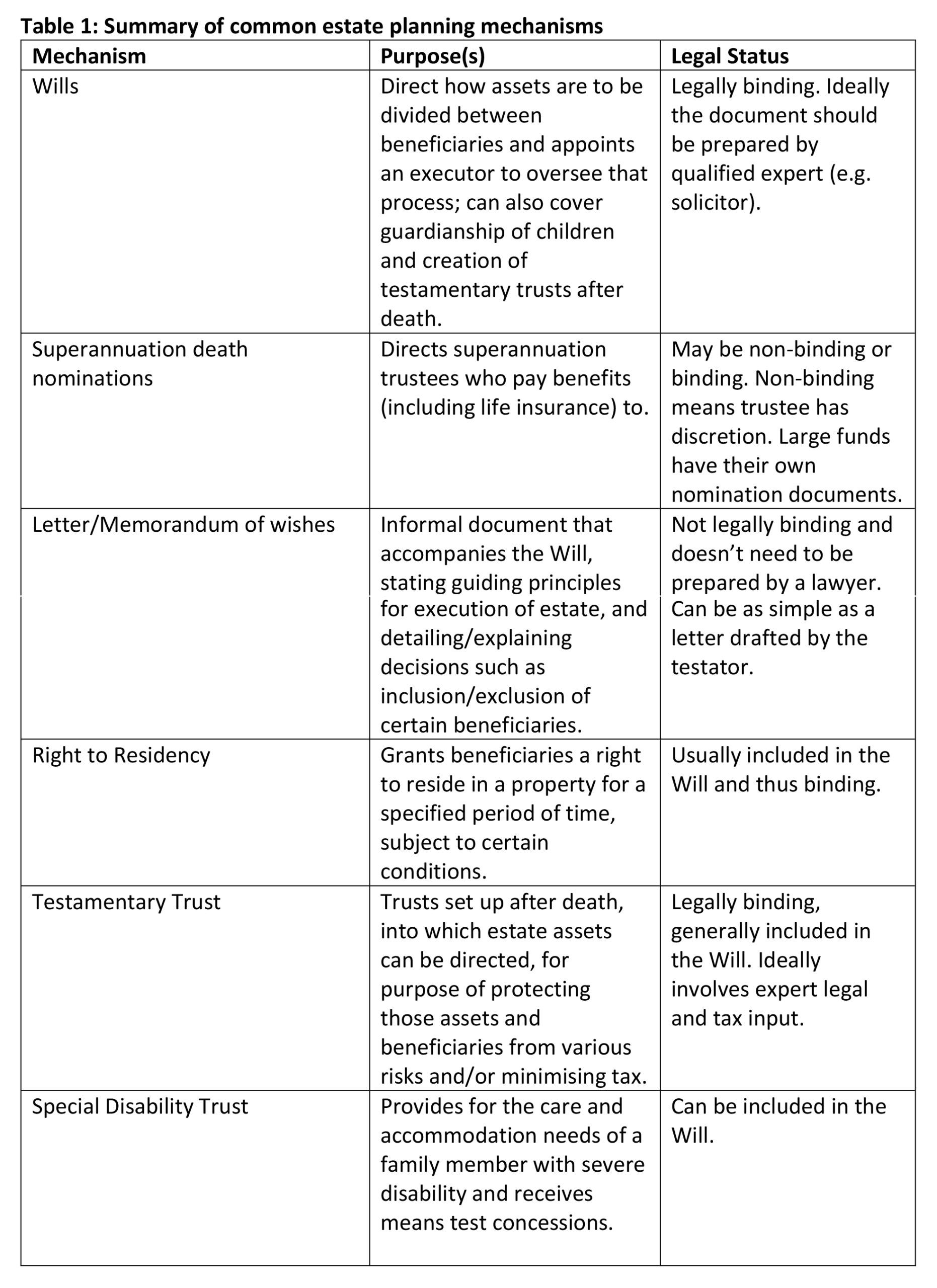

Typical estate planning mechanisms

There are a number of mechanisms, varying in formality and legal enforceability, that can be used to ensure a person’s intentions are acted upon after death. Some of the most common are summarised below:

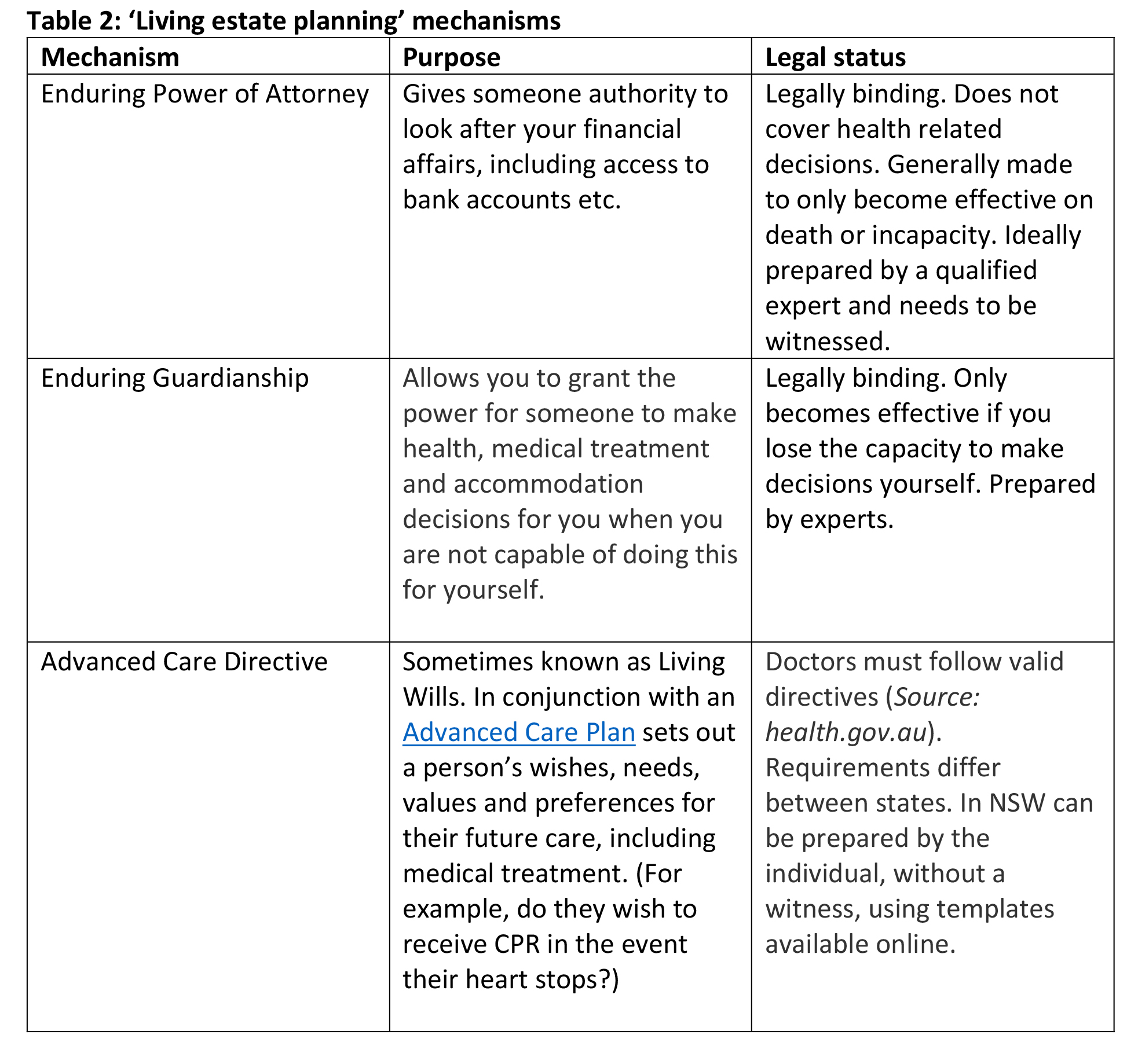

When we lose the ability to make our own decisions

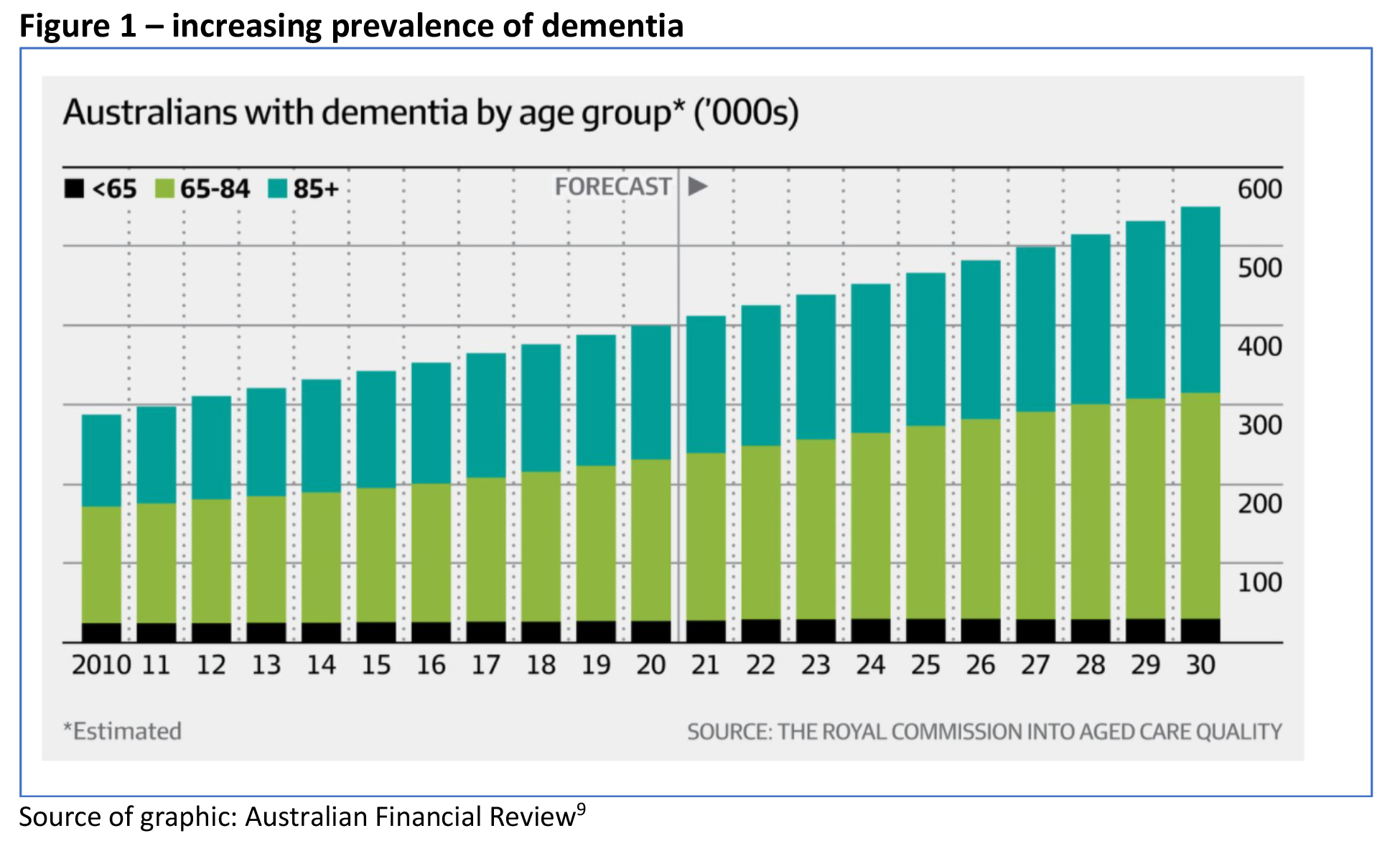

Robust estate planning isn’t just about what happens after death, it’s also about putting mechanisms in place should accident or illness rob us of the ability to make current decisions ourselves. This is becoming particularly important in the context of our ageing population; whilst we are living longer, the prevalence of dementia is also increasing (see Figure 1).

The essence of ‘living estate planning’ is the ability of spouses and children to easily – legally – make decisions on behalf of a person who has lost their capacity to do so themselves. Those decisions could relate to financial affairs, accommodation arrangements, and health care.

Sadly, another benefit of estate planning is becoming increasingly important. The right plans can prevent the likelihood of elder abuse, the increasingly common scenario where older people are taken advantage of by someone – often a family member – seeking to take control of assets such as homes, savings, investments and other possessions. Experts believe COVID 19 has exacerbated this phenomenon[9], as lockdowns see the elderly increasingly isolated, and younger people come under financial pressure.

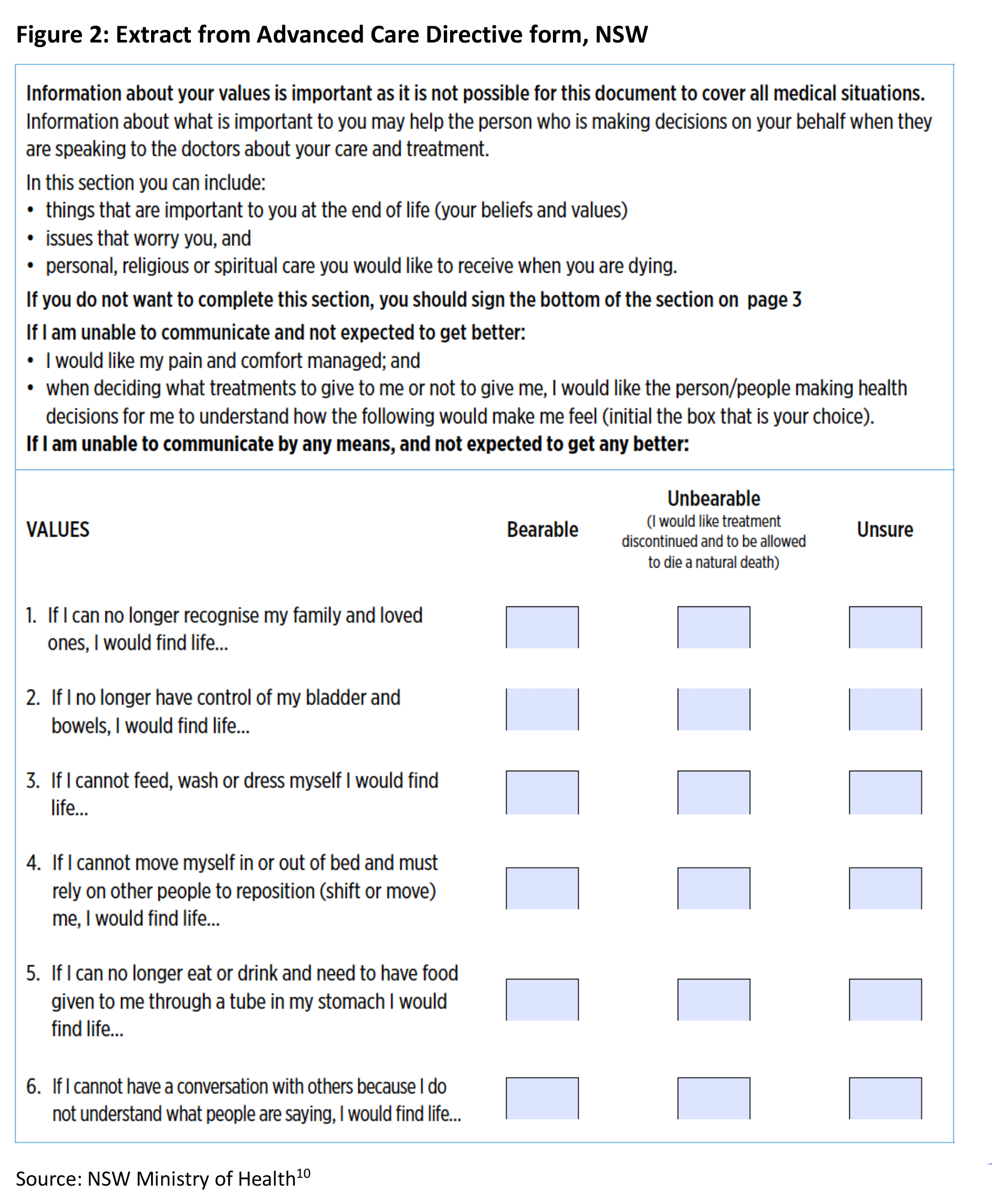

Health care and medical treatment can be a particularly sensitive issue. Each individual has their own personal philosophy on living and dying, and whilst the default objective of health care professionals may be to save a life at any cost, this may not align with the wishes of the individual themselves, for whom quality of life is more important.

The cost of not making plans

In addition to increasing the likelihood of disputes and damaging family relationships as a result, the absence of formal estate plans can also be costly, both financially, and in time taken to resolve matters and finalise legal processes. This can be especially difficult for any dependents (e.g. a spouse and/or children) who were solely financially reliant on the deceased.

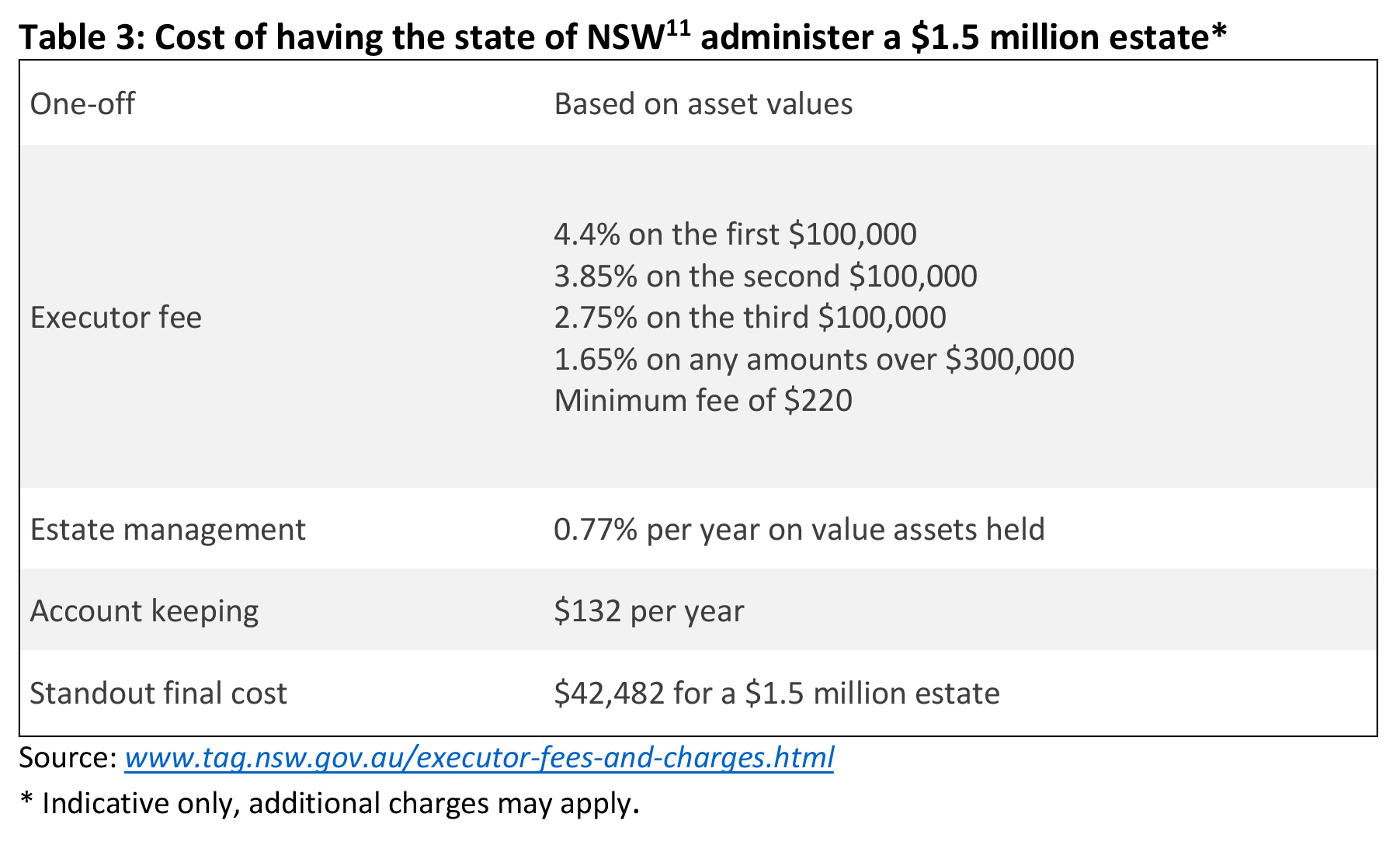

A person who dies without a valid Will is said to have died intestate. Each state and territory has its own specific intestacy rules, which include who may be entitled to the deceased assets and how much they may be entitled to receive.

In many jurisdictions, assets are generally distributed according to a predetermined formula with certain family members receiving a defined percentage of the assets. This will typically depend upon whether the deceased had a spouse and/or issue (e.g. children or other descendants). Furthermore, a cost is imposed for the state to provide this service, as seen in Table 3, below.

The majority of estate planning work doesn’t require legal advice

Notwithstanding the obligations imposed by ASIC via RG 175, sections 354 and 403, many financial advisers perceive estate planning to be solely about the preparation and execution of formal legal documents, and as such, beyond their expertise and the legal boundaries of their advice licence. As a result, they tend to only give cursory attention to such discussions, generally recommending the client discusses their testamentary wishes with their lawyer.

In actual fact, neither assertion is true.

Not all aspects of estate planning require the involvement of a legal professional. Furthermore, whilst only qualified legal professionals may be able to execute certain documents, financial advisers are generally far better qualified to help clients make the actual decisions that are being codified in those documents.

This is because the financial adviser generally has a far more holistic understanding of the client’s family and financial situation, and also because most lawyers are not qualified nor experienced to deal with the vast range of estate planning issues that planners often see within their clients’ affairs. One example might be the navigation of superannuation death benefits post the 2017 reforms[12], particularly with SMSFs with pension and accumulation balances. Other areas where many lawyers lack experience and expertise include Centrelink, aged care, and taxation issues arising on death.

Arguably the most time-consuming parts of the estate planning process revolves around fact finding and decision making, based on discussions that require a familiarity with a client’s circumstances, and which do not constitute legal advice. As such these are discussions a financial adviser is well placed to facilitate:

- appointment, selection and remuneration of an executor;

- choice and selection of guardians and trust appointors;

- identification of beneficiaries and their special needs or circumstances;

- the identification of the client’s assets, ownership structures and the entities that control those assets;

- the distribution and control of assets to beneficiaries;

- superannuation interests;

- life insurance claims;

- relationship issues, including family conflicts and marital breakdowns;

- financial insolvency; and

- asset protection issues.

Financial advisers are often the best placed to facilitate the estate planning process

Financial advisers are often in the best position to estate planning issues because much of this information is usually within their files as part of their “know your client” duty, and because they already have the client’s trust. As such, advisers are well placed to project-manage and co-ordinate an entire estate planning process directly with their client.

In this process, the financial adviser is working with the client to identify estate planning issues and motivating the client to solve those issues with appropriate legal mechanisms, provided either by the client’s lawyer, or the adviser’s own legal services provider.

It is a model where the financial adviser is very much at the centre, allowing them much more control over the quality and integration of the process, minimising any disconnect between client intentions and outcomes, and allowing the adviser to deepen their relationship with the client and the client’s family.

A major benefit of moving into estate planning facilitation is that it needn’t carry any ongoing administration or compliance burden, involves minimal upfront costs to introduce within a practice, and no legal responsibility if managed correctly in conjunction with a competent estate planning lawyer.

It is also an opportunity for the adviser to demonstrate value, and charge accordingly, with upfront fees for estate planning typically ranging13 from $2,000 to $8,000.

Of course, whilst estate planning advice is not in itself a financial service, it may give rise to the provision of a financial service or product, and the usual compliance guidelines will still apply to these circumstances. Plus, there are other boxes advisers still need to tick before such a move is made:

- Does your licensee approve?

- Will your Professional Indemnity insurance still cover you and are there any limits/exclusions?

- Tax advice still requires a tax agent’s licence

COVID 19 has created further complexities for estate planning

As well as prompting a spike in people revising their Wills[14], and driving an increase in family disputes[3], the COVID 19 Pandemic has created a number of additional complexities to be considered.

For example, the fluctuation in share values and the continued drop in real estate prices may be problematic to the equal distribution of an estate’s assets, especially if the Will specified dollar amounts, rather than percentages.

Similarly, many superannuation funds have decreased in value, or have been diminished by people taking advantage of the Early Release scheme introduced by the Federal Government.

Conclusion

COVID 19 has given a new impetus, and introduced new complexities, to estate planning. Whilst many advisers believe estate planning to be the exclusive domain of legal professionals, in reality financial advisers are often far better placed than other professionals to facilitate the estate planning process, due to their holistic and more up to date understanding of the client’s financial and family circumstances.

The legal barriers to engaging in this market are also not as high as many advisers perceive. Although the preparation and execution of certain estate planning documents should be left to qualified legal professionals, this generally represents the very end of a process of fact finding and decision making which is not classed as legal advice, and as such is a process which financial advisers are generally more than capable of managing for, and with, their clients.

![]()

———