Life underinsurance – from gap to chasm, the advice challenge

Financially, Australians are therefore more vulnerable than ever before.

Life underinsurance has been a much discussed – and debated – topic for more than a decade. Denounced by some critics for the perceived self-interest of those seeking to shine a light on the issue, recently released data[1] confirms the underinsurance gap is not only real, and significant, it is also widening. Structural developments within the sector are likely to exacerbate the problem further, posing challenges for advisers and their clients, as well as regulators, governments, and the community overall.

The gap hasn’t always been increasing

Regarded by many as the definitive authority on underinsurance, Rice Warner have been monitoring and quantifying the issue for many years. But whilst their recently released 2020 report[2] found the gap had increased over the previous three years, the trend wasn’t always in this direction. In 2016, commenting on their 2015 report, they observed[3] “tracking of the life insurance gap over the past 10 years indicates a narrowing of the shortfall, particularly for low-income earners. This results from higher levels of default cover within superannuation, increased focus on insurance by financial advisers and superannuation fund trustees, and an active direct insurance market.” How times have changed!

Defining and quantifying the gap

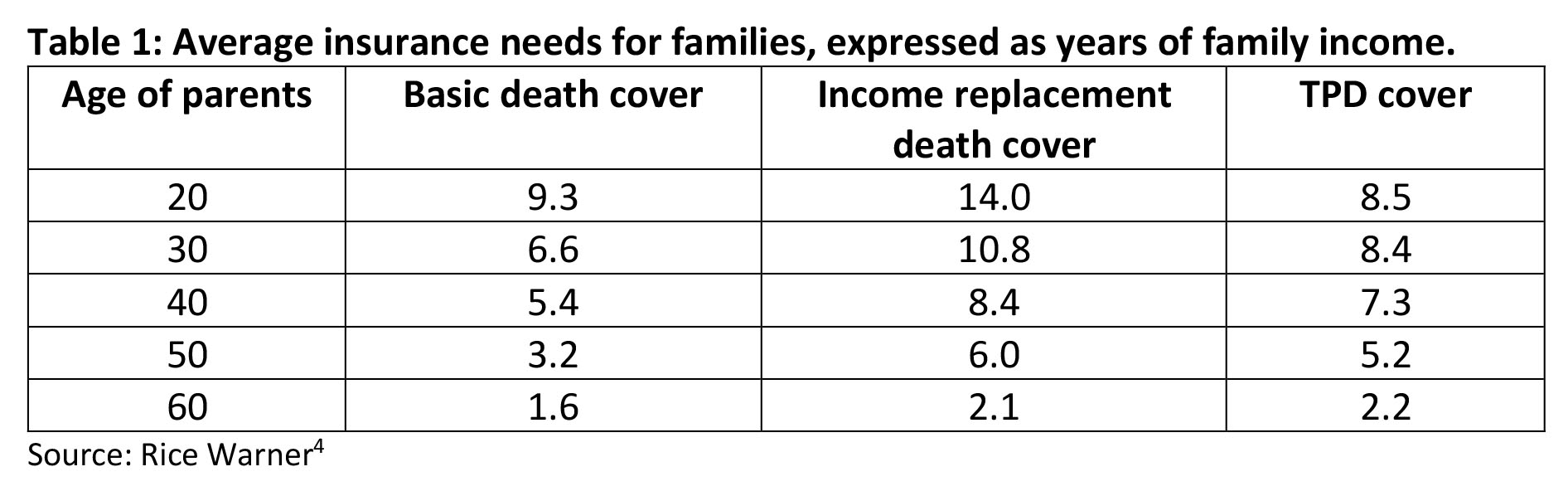

Rice Warner’s approach to quantifying the underinsurance gap has been to compare actual insurance levels (across all channels) with notional benchmark levels of adequate cover. They define two benchmarks for death cover:

- Basic – the amount required to extinguish all non-mortgage debt and sustain current living standards until age 65 or until children reach age 21; and

- Income replacement – the level required to replace the expected net income of the insured and maintain current living standards until the insured would have reached age 65.

Using these benchmarks, they then express cover needs in terms of years of income. Different benchmarks were calculated for different life stages. Table 1 below, as an example, shows notional benchmarks for families with children.

Underinsurance is thus the extent to which the actual life insurance levels held are less than these benchmarks.

In 2020, Rice Warner estimated[5] that actual levels of cover held across Australia were sufficient to only meet 92% of basic death cover needs (the lower of the two benchmarks) and 29% of TPD needs.

In aggregate dollar terms, the shortfall is immense; in 2017 Rice Warner estimated[6] a $471 billion shortfall for death cover adequacy at the basic level and $3.43 trillion at the income replacement level. The TPD shortfall was estimated at $10.87 trillion, and the income protection shortfall at $611 billion (assuming a benchmark replacement level of 85% of salary).

An alternative methodology – community expectations

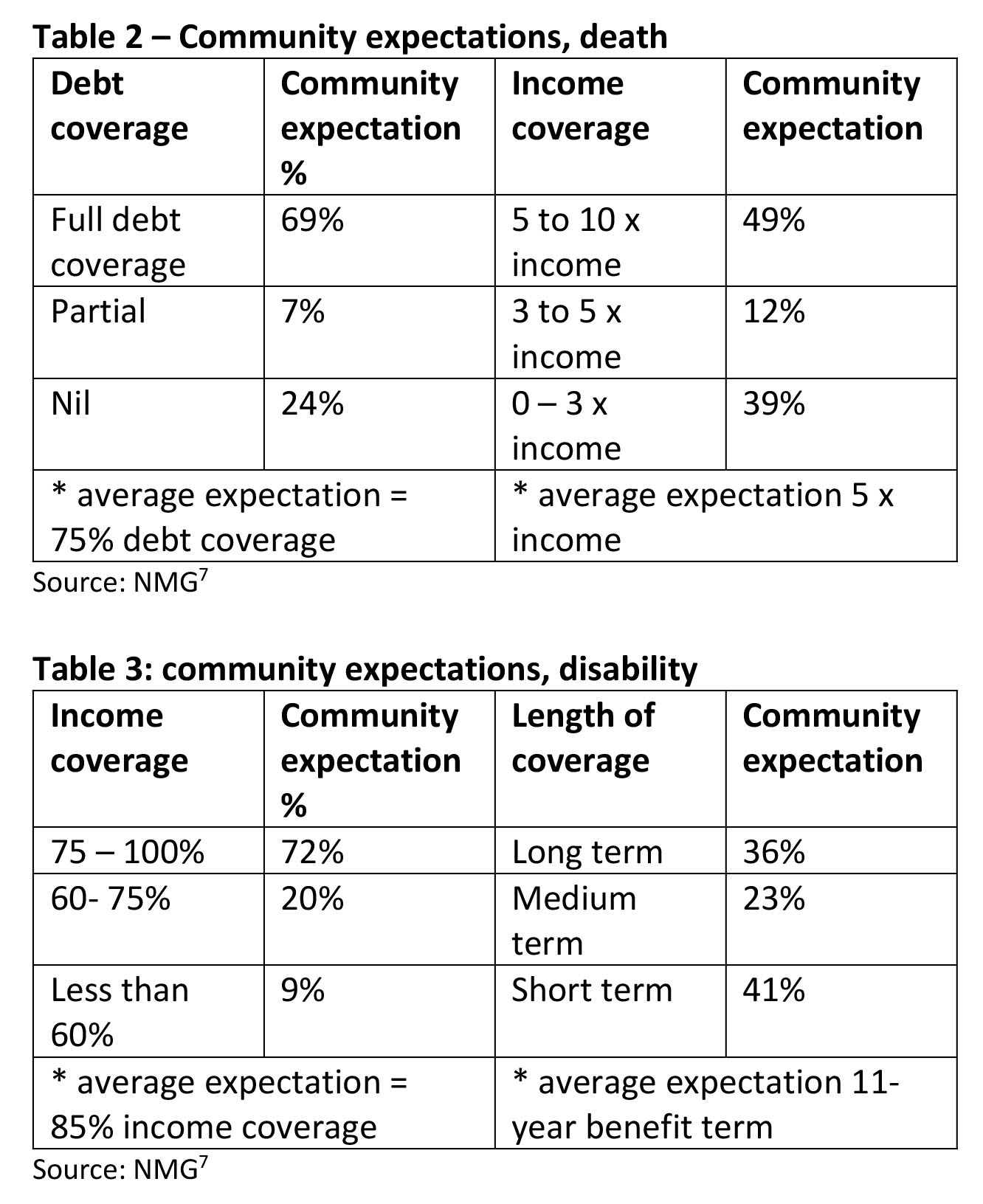

The term ‘community expectations’, heard so frequently during the Hayne Royal Commission, became the basis for an alternative methodology for assessing underinsurance in 2019, when NMG surveyed consumers about their expectations on ‘adequate’ amounts and types of protection. Any shortfall or gap would therefore be relative to what the community expected was necessary to avoid financial hardship (rather than an industry calculated benchmark).

Their research[7] found widespread consumer endorsement for private sector insurance – rather than government funding – as the preferred protection mechanism. They also found consistent- and modest – expectations around what this protection should look like:

- They are anchored in avoidance of hardship, rather than fulfilling long term lifestyle or security ambitions;

- Focused on children (education), the family home (paying off debt), meeting costs of living and allowing independent futures for beneficiaries; and

- Fulfilling mid-term living standards and supporting an orderly restructuring of costs of living, debt, and employment arrangements, rather than providing financial security for life.

To the extent that debt and income dependency levels vary by lifestage, NMG were able to illustrate how levels of cover expected by the community vary over time, as shown in Figure 1, below.

By converting these consumer expectations to risk premiums, NMG were then able to compare premium levels with the ‘status quo’ (i.e., existing coverage). This comparison found substantial variation between community expected levels of cover and actual levels, across lump sum and income replacement, and especially in the ‘peak dependency ages’ of 35 – 55.

Regardless of methodology, the conclusion is the same: most Australians don’t have adequate life insurance, whether that is measured by expert opinion, or their own.

Why is the gap growing?

Simplistically, a gap can be driven when both sides are moving in opposite directions. In a life insurance context this can happen when the need for cover increases while the take -up or placement of cover decreases.

From a demand side perspective, the need for cover is increasing, in line with rising levels of community indebtedness.

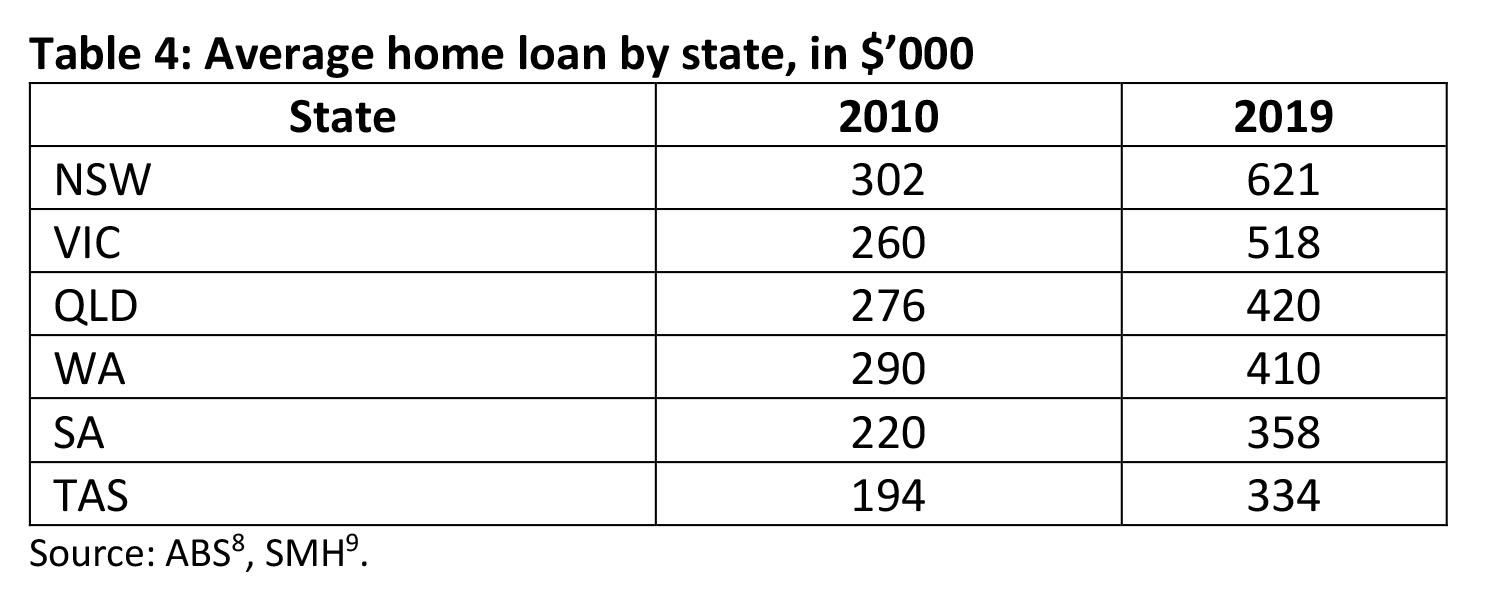

To put this in perspective, between 2010 and 2019, the average mortgage doubled in New South Wales and Victoria, and rose by over 50% in Queensland.

On the other hand, average income levels – as measured by Average Weekly Ordinary Time Earnings (AWOTE) grew by approximately 37% over the same timeframe[10].

Taken together, we now see the ratio of household debt to household disposable income sitting around 185%, (compared to around 68% in 1990). It’s an area where we unwittingly lead the world[11], and is driven mainly by mortgage debt, which represents around 76% of all household debt[12].

Financially we are therefore more vulnerable than ever before.

Placement of cover has decreased

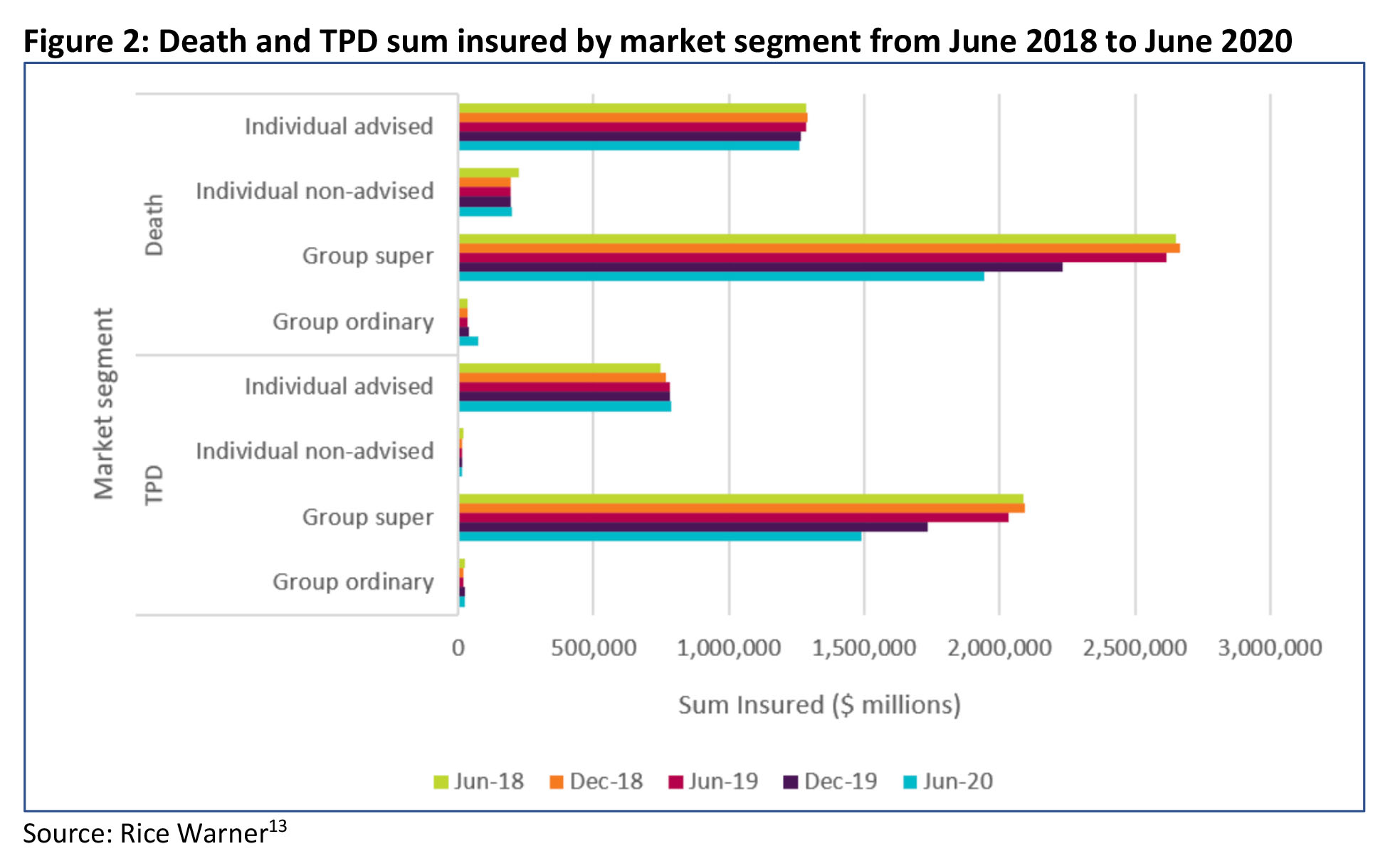

Just as the notional need for cover is peaking, however, the take up or placement of cover is decreasing, driven largely by a number of recent structural supply side developments. This is neatly summed up in Figure 2, which shows aggregate sum insured trends across the group, retail and direct channels, since 2018.

What is immediately evident is that death and TPD coverage across all channels has decreased. Specifically, we see over a 2-year period, total death and TPD cover has decreased by 17% and 19% respectively. This is a significant reduction and is driven mostly by the drop in Group insurance inside superannuation, being 27% for death and 29% for TPD cover.

If we look at new sales, rather than in force sum insured, we see a downward trend there too. According to Plan for Life[14], retail life insurance sales dropped 10% in the year to March 2020. Group lump sum premium revenue fell 12% over the 12 months to 30 June[15].

What’s driving the trend?

A number of factors are playing out across all distribution channels, the majority of which can be traced back to significant regulatory changes.

Group insurance via superannuation

Through its Protecting Your Super (PYS) and Putting Members Interests First (PMIF) legislation, the Federal Government has sought to address two issues it perceived in the context of life insurance and the superannuation system:

- The provision of cover to young people (under 25) without debts and dependents, and who, therefore, theoretically had no need for it; and

- The erosion of savings in small balance and inactive superannuation accounts by insurance premiums.

The PYS changes, which became effective on July 1, 2019, include:

- Super accounts with balances under $6,000 that are inactive – i.e., they have not received any contributions, rollovers or other transactions for 16 consecutive months – will be closed. The funds will be sent to the Australian Taxation Office (ATO), to allow it to consolidate them with a member’s active account. Any insurance would therefore be lost.

- Super accounts (of any amount) with insurance and that are inactive for 16 months will have their insurance cancelled (unless the member has requested it be kept in place).

The PMIF legislation, which came into effect 1 April 2020, extended these changes further, essentially mandating that the default, opt out cover is only provided to fund members at the latter of:

- Receiving their first mandated employer contribution

- Their account balance reaching $6,000, or

- Turning age 25.

Regardless of whether one agrees with these changes, the impact has been immediate, and significant. Notwithstanding the exemptions which can be granted to those funds covering people in dangerous occupations (e.g., mining), hundreds of thousands of super fund members have already had their existing life insurance cease[16]. Over time, it is estimated that as many as 4.5 million less Australians may be covered, either because they lose existing cover, or they don’t enter the system in the first place[17].

Another consequence of the legislation is that the removal of so many under 25s from insurance pools has raised the age profile of remaining members, requiring substantial repricing of group cover. Premium increases of 30% and upwards for group cover have been common over the last 12 to 18 months, and over time this may drive even more members to drop their cover.

Direct insurers and anti-hawking

Even in the direct market, cover has typically been ‘sold’ rather than ‘bought’.

However, in January 2020, ASIC brought into effect tough new anti-hawking measures for direct life and consumer credit insurance. These measures banned unsolicited telephone sales of these products, pre-empting a recommendation from the Hayne Royal Commission which would – if implemented – extend to other products and to in person meetings as well.

With many large players having already withdrawn from the direct life market after sustaining reputational damage – and financial penalties – in the immediate aftermath of the Royal Commission[18], this latest change proved the last straw for many others, forcing them to cease operations due to their business models no longer being viable.

For the year ended December 2019, annual direct life sales had fallen by over 30%, and the January 2020 changes are expected to exacerbate this downward trend[19].

Retail channel challenges

Two relatively recent seismic shifts have impacted life insurance advice.

Firstly, many advisers have exited the profession altogether. According to Rainmaker Information’s Financial Adviser Report[20], the number of registered financial advisers in Australia decreased 16% through the 12 months to June 2020 to 22,334. A variety of factors are likely to have contributed to this outcome, including the new FASEA requirements, and a significant amount of disruption and consolidation amongst licensees.

Secondly, for many of those advisers still active, in addition to red-tape related increases in the costs of running an advice practice, the economics of life insurance advice in particular have become more challenging, with the LIF mandated capping of up-front commissions to 60% (+ 20% trail) dramatically reshaping potential revenue streams.

The phasing in of these caps – from the beginning of 2018 – has seen many advisers diversify income streams away from risk, the net result of which is we have not only seen downward pressure on new business, we have also seen a shrinking of the risk specialist segment.

According to Investment Trends[21], as at the end of 2019, only 15% of planners derived over 50% of their total practice revenue from providing risk advice, down significantly from 34% five years before. 2020 may well see this number fall further.

And it’s not only new business that is suffering. Recent premium increases for income protection and TPD cover – largely a response to spiralling mental health claims – are also proving challenging for advisers, with research showing that client-initiated policy lapses are on the increase[22].

Implications of a widening underinsurance gap

Aside from the consequences of underinsurance at an individual – human – level, there are some macro level impacts to consider.

The burden to the public purse is an obvious one, as people without adequate life cover are forced to draw on available government support mechanisms (as limited as they may be).

Rice Warner estimated the current total cost to the Government in social security payments of death and TPD underinsurance across Australia to be well over $600 million per annum[23]. To the extent this doesn’t include income protection underinsurance gap mentioned above), it is likely this annual cost exceeds $1 billion.

Inadequate life insurance is likely to impact employers too, as people with inadequate cover for disability are forced to work before they are fully recovered, leading to the productivity sapping phenomenon of ‘presenteeism’.

And there is also a broader economic impact in terms of the reduced spending capacity of underinsured individuals, creating a multiplier effect of reduced consumption and increased bad debts, leading to higher credit costs, and job losses.

A word about financial literacy

Whether or not the changes to group life result in a life insurance ‘underclass’, it is likely the creation of a large cohort of people not entering the life insurance system until age 25 will further exacerbate the low levels of insurance literacy in our community.

Relative to our global peers, Australians already have very low levels of understanding about insurance[24], leading to poor decision making and inadequately protected individuals and families. One advantage of the default life insurance system is that it exposes people to the concept and value of cover, helping create some level of understanding – and even positive disposition – which can carry through their lives, perhaps even acting as a prompt to seek financial advice.

The more we limit this exposure, especially for younger people, the more we will see insurance literacy levels fall further.

Closing the gap – the advice opportunity

To the extent that the largest single driver of the aggregate underinsurance gap is the changing dynamics in the group sector, the opportunity for advisers is three-fold.

Firstly, and most obviously, there are now a cohort of younger workers without cover who actually need it. This is especially true of income protection.

Policymakers and consumer advocates arguing that younger workers don’t need life cover as they generally don’t have mortgages and children seem to have forgotten that (a) some actually do and (b) those who don’t are likely to have car loans, credit card debts, and a reliance on their income to fund their lifestyle. Regardless of whether removing income protection was an unintended consequence, there are now likely to be more people who need it but don’t have it.

Secondly, those still in the system need help navigating it. Advisers can help ensure these people don’t inadvertently lose cover on inactive/low balance accounts, can help them determine the best way to plug any coverage gaps, and can help them compare group cover with retail offerings (which may actually be more affordable after recent group premium hikes).

Thirdly, advisers are best placed to help improve the overall insurance and financial literacy of the everyday Australians and should continue to deliver education and resources through online and offline channels. In doing so they will be increasing the number of people who understand and appreciate the value of the right cover, in the right amounts, and ultimately helping create a more protected community.

![]()

——–