The pool’s lovely, come on in! An essential guide to life insurance underwriting in Australia

Managing the [risk] pool is a delicate balancing act.

The gatekeeper to the pool

In an earlier article we explained risk pooling, a foundational concept in insurance.

By aggregating together people with similar risks, those risks can be spread. A frequently cited example is that of ancient shipping merchants [1], who would come together and effectively pool and share the financial risks of one of their boats and/or cargo being lost at sea. A key enabler for life insurance pools was the creation of the very first life tables in 1693, by mathematician and astronomer Edmund Halley[2] (yes, he of the comet).

Managing the pool is a delicate balancing act.

As a pool grows, the more the risks are shared and the lower the contribution (premium) each participant in the pool needs to pay for the pool to remain sustainable. That’s clearly a good thing. However, if people are admitted to the pool who aren’t paying their fair share of premiums – because their risk profile is higher than other members of the pool – then that’s a problem, as it means over time the pool isn’t collecting enough funds to cover potential claims. If the pool is forced to shut down, everybody loses.

Enter the underwriter. Their job is to decide whether to admit someone into the pool, their cost of entry, and whether they are subject to any special rules while they are in there. This responsibility makes them very important indeed!

The basics of underwriting 1 – know your client

The basic premise of life underwriting is to assess the risk profile of an individual, relative to the likelihood of them claiming on a life insurance policy. In order to do that they need to understand the circumstances of the individual across a number of criteria, including:

- Age and gender (simplistically, the likelihood of claim increases with age, and females have lower mortality but higher morbidity);

- Occupation and income (needed to determine whether the job itself has higher risk of death or injury, and also to judge appropriateness of sums insured and likelihood of return to work).

- Pastimes and sports (mountain climbing, motor racing and scuba diving are risky, and footballers have high rates of injury)

- Lifestyle (alcohol, tobacco and other drugs are linked to higher mortality and morbidity)

- Health history (current state of health, any past health issues and any family history of hereditary conditions).

The main way to gather this information is of course to ask the client themselves, although this process is not without flaws, as sometimes people omit information, mostly through forgetfulness, but occasionally by design. Information across the above categories will initially be gathered by a form (a Personal Statement), completed by the individual online, over the phone (tele-underwriting), or using an old-fashioned paper and pen.

Depending on how they answer the form, the underwriter may decide to seek further information, either through additional questionnaires (for hazardous pursuits for example), by writing to the client’s doctor, or even by requiring the individual to undergo medical tests ranging from simple blood tests to full medical examinations (which the insurer pays for).

Even at this early stage of the process, underwriters have an important economic decision to make.

The financial cost and time delay in seeking medical tests can be substantial, and for this reason insurers generally set a threshold below which they will generally not require such tests. These are known as non-medical limits, and they generally work on a tiered system, where age and sum insured will determine what, if any tests, are needed. As an example, Table 1 shows Zurich’s guidelines for death and TPD cover, as taken from their 2020 Adviser Guide.

As can be seen, for clients up to the age of 45, seeking $2.5 million in cover or under, no mandatory tests would be needed (this does not preclude the insurer asking for tests if the client’s health history is not ‘cleanskin’).

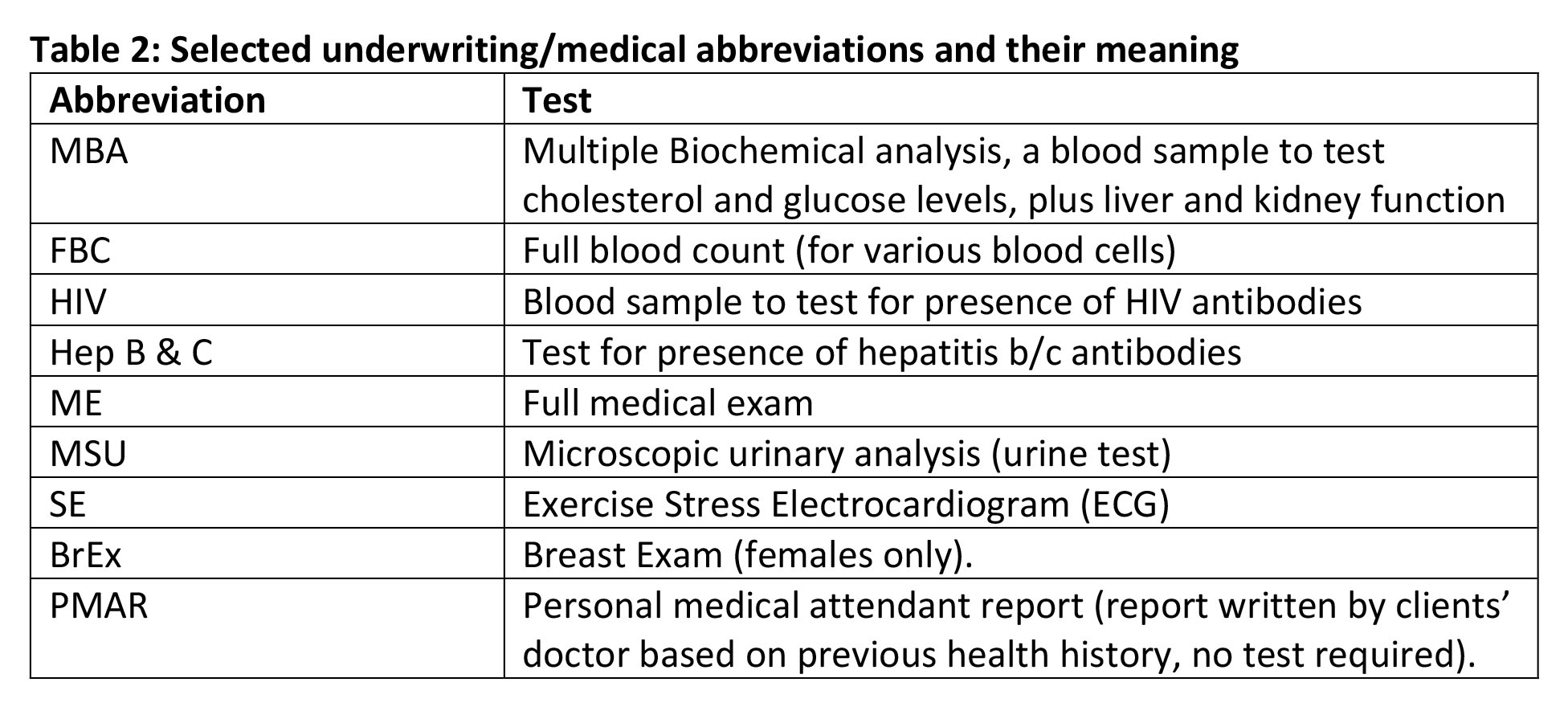

On the other hand, once you are seeking in excess of $10 million in cover, you will be required to undertake a number of tests, regardless of your state of health. These tests include:

Further, more specialised tests may be required if the client is applying for trauma cover. And, reflective of the higher claims frequency with trauma policies, the thresholds for the various tests testing are generally much lower.

The basics of underwriting 2 – assess the risk

Having gathered all the information they can about the client, the underwriter then has to assess the risk, and whether to admit the client to the pool, and if so, on what terms.

This assessment will be done in the context of the insurer’s underwriting philosophy, risk appetite, and detailed underwriting guidelines.

Underwriting philosophy is an overall approach that an insurer will take to assessing and accepting risk, and it can mean different things to different insurers, including service standards, innovation, and quality of its people. A philosophy should be consistent and unchanging, whereas risk appetites within that philosophy may vary from time to time

An example of where these two concepts may overlap is in the quality of lives the insurer is prepared to accept. A ‘select lives’ approach is one where only those clients who would qualify for ‘standard rates’ are accepted. This obviously improves the quality of the risk pool but comes at the cost of limiting the number of potential entrants. Other insurers may be prepared to take on more risky clients, perhaps to help them establish market share, or for other strategic reasons.

The detailed rules applied by underwriters are known as underwriting guidelines.

These guidelines, based on years of claims experience and health data, enable the underwriter to determine the risk of that individual relative to a ‘standard’ life. The more data and experience an insurer can reflect in their underwriting guidelines, the more accurate they can be, which in turn can allow them to be more confident in accepting risk.

Whilst larger, more established life insurers can viably use their own guidelines, many reinsurers – who are essentially insuring the insurers – will stipulate their own guidelines must be followed, In part or in full. To the extent that underwriting guidelines continue to evolve, in line with claims experience and medical advancements, working with a global reinsurer allows local insurers to benefit from more detailed claims experience data, and quicker access to insights into new trends and breakthroughs in health testing and treatments.

Loadings and exclusions

When a client, assessed against these guidelines, is deemed to be a higher-than-normal claims risk (perhaps because they suffer obesity, or high blood pressure) the underwriting manual will generally express this in percentage terms, for example, plus 50% mortality, or plus 100% morbidity (where the ‘plus’ is relative to a standard life). This in turn is generally reflected in the client paying a higher – ‘loaded’ premium. ‘Higher’ in this case is relative to the standard table of rates applied by the insurer, which already take into account factors like age, gender and smoker status (and in the case of income protection, occupation).

Depending on their risk appetite, insurers can be flexible in how they deal with loadings. They can decide an upper limit on the loaded rates they would be willing to take on (for example, they may decide that they will not offer cover to any client rated above + 300%, even if the client was prepared to pay the extra premium), and they can decide to waive smaller loadings altogether. Sometimes these decisions are made on a standalone basis, other times the overall context of the application, including the lifetime value of the client, and any competitive and strategic factors, may be taken into account.

The other mechanism the underwriter has at their disposal is the application of exclusions.

An exclusion is a specific condition or circumstance under which cover is not provided. In addition to the standard exclusions applying to all policies (e.g., suicide within 13 months, criminal activity, war), the underwriter can decide to exclude cover on an individual basis, often for pre-existing health conditions, such as a bad back, or for claims relating to hazardous pursuits (for example, skydiving).

The ability to apply loadings and exclusions enables the insurer to effectively adjust and equalise the risks of a client entering the pool, ensuring more risky lives can enter the pool without undermining its overall sustainability. Without these mechanisms, the only alternative open to the underwriter may be to deny the client entry to the pool altogether.

Direct v group v retail underwriting

Whilst individual underwriting is standard for retail cover, direct and group cover have their own nuances which dictate a different approach.

Direct cover generally involves lower sums insured and premiums, and less comprehensive personal statements (longer forms have proved ineffective for clients completing them online, without any assistance). Less information about the life insured means a higher risk to the insurer, which explains why direct life insurance rates – for short form underwritten products – generally include an extra mortality/morbidity buffer, making them higher than fully underwritten retail rates.

Furthermore, the lower average sums insured and premiums for direct can make the cost of seeking more medical evidence, through extra tests, unviable, and as a result, some direct underwriters may decide to simply deny cover altogether if a decision cannot reasonably be made without further health evidence.

Group life insurance is different again, with a number of factors making it viable to completely avoid individual underwriting and offer cover automatically:

- Default cover – granted automatically on an opt-out basis – all but removes anti-selection risk

- The larger size of group pools smooths out the risk and makes them less susceptible to lumpy claims experience

- A person starting a new job is more likely to be in good health than the overall population

- Default sums insured are relatively small.

There is also a cost driver at play, with the size of premiums for these smaller amounts of cover generally not being enough to justify the expense of individual underwriting. Hence the offering of non-underwritten cover with Automatic Acceptance Limits (AALs). These limits will vary by age, sometimes taking the form of a salary multiple (e.g., 4 x salary), other times being a specific dollar amount.

These limits are set at the level beyond which the risks to the insurer outweigh the cost savings from not underwriting cover, and once an individual seeks cover above those limits, they will be subject to an individual underwriting process.

Financial underwriting

In addition to medical underwriting, there are circumstances where an insurer will need to understand an individual’s financial circumstances before deciding whether to offer cover.

Mainly designed to avoid over insurance and associated moral hazards, financial underwriting is generally used when an individual is applying for large income protection benefits, or abnormally large lump sum amounts. Typically, it involves seeking financial information supporting the need for these sums insured, such as tax returns, and detailed business financial data (profit and loss statements, balance sheets) if the applicant is a business owner.

Mental health underwriting

The spiralling[3] of mental health life insurance claims, and the threat they pose to the sustainability of some product categories, is one the biggest challenges facing life insurers today.

A historically poor understanding of the many different types of mental disorder previously saw a blanket ‘one size fits all approach’ by insurers, which lead to many sufferers being inappropriately having exclusions applied or denied cover altogether. (This also fuelled the criticism that people were effectively disincentivised from seeking professional help for their condition).

In the absence of suitable data, it was hard for underwriters (and pricing actuaries) to differentiate between sufferers of situational depression at one end of the scale (for example, due to bereavement or divorce) and sufferers of schizophrenia or bi-polar disorder at the other. It is now recognised that the profile and inherent risk factors for these conditions are vastly different.

Another factor at play is the sometimes-subjective nature of mental health diagnoses, which can cause complications at both underwriting and claim time. Although mental health conditions are recognised in the international classification of diseases (the ICD-10), there are currently no reliable biomedical markers to indicate the presence or severity of most mental health conditions.

In recent years many insurers have overhauled the way they deal with mental health from an underwriting perspective. More specifically, there has been a recognition that mental illness is not one homogenous condition, and that the causes, treatment, and prognosis differ widely across the many different disorders.

Moving away from the ‘one size fits all’ approach, underwriting processes have evolved to treat each case on its merits, thus being more equitable and facilitating a virtuous circle: collecting more data, which allows more insights, more accurate pricing, more affordable cover for many, more people taking out cover and more data being collected.

Importantly, the contemporary underwriting approach dispels the perceived discouragement of people seeking professional help with their mental health

Regulatory challenges for underwriting

The essence of underwriting is being able to accurately assess – and in a sense price – risk. It relies on information symmetry; in other words, the insurer and the life insured have access to the same information. Information asymmetry, where the life insured knows something relevant that the insurer doesn’t, puts the insurer at a disadvantage and can create moral hazard.

Some of this can be minimised through the non-disclosure provisions of the application, allowing the insurer to void a contract of insurance if the life insured is found to have knowingly withheld relevant information. But sometimes, the issue is so large, conventional risk management mechanisms aren’t adequate. One such example is the rapidly advancing field of genetics.

As genetic testing becomes more reliable and more affordable, more and more individuals are choosing to undertake such tests. Some tests are for genealogical reasons (to trace one’s ancestry), and some are for research purposes. Others are for people concerned about the presence of a hereditary health condition. To the extent that genetic tests are becoming increasingly reliable indicators of future health problems, the results of such tests represent very powerful, and very sensitive, information. If a person knows they are more likely to suffer a health condition in the future and isn’t forced to disclose that information to a life insurer, they are able to effectively select against that insurer, taking out cover whilst knowing they have an increased likelihood of claiming.

This information asymmetry is something that was self-regulated by the life insurance industry in 2019 (ahead of the threat of regulatory intervention). Bowing to pressure by politicians and genetic researchers, the life insurance industry, via the FSC, agreed to a moratorium on seeking the results of any genetic tests the applicant may have undergone, provided the sums being applied for were under certain thresholds:

Life insurance genetic test moratorium limits:

- $500,000 of death cover

- $500,000 of total permanent disability cover

- $200,000 of trauma/critical illness cover

- $4,000 a month in total of income protection, salary continuance and/or business expenses cover

Other key features of the Moratorium:

- for applications over the limits, life insurers can ask the applicant to disclose the result of any genetic test they have had.

- regardless of the financial limits, applicants can disclose a favourable genetic test result if they wish and the insurers will take that into account.

- Life insurers will not ask or otherwise encourage applicants to take a genetic test as part of their application and underwriting process.

- results obtained as part of a research study are treated the same as a clinical test results and must be disclosed as part of applications for cover over the financial limits.

The moratorium is due to be reviewed in 2024, at which time the impact of this information asymmetry on claims can be examined.

A wide variety of other regulation, and proposed regulations, have the potential to further impact the dynamics of underwriting.

The government’s recent PYS and PMIF changes to superannuation have impacted the age profile of group super schemes, effectively requiring their aggregate risk profile to be reassessed.

And the 2017 Parliamentary Joint Committee (PJC) Inquiry into life insurance[4] examined limiting the ability of insurers seek further health evidence from applicants. Under this proposal, which is not currently under active consideration, insurers would potentially need to seek an individual signed consent for each health condition they wanted to investigate, and each individual medical specialist they wanted to seek that information from. The potential economic and time cost of such a proposal to the underwriting process are both obvious and substantial, and from a consumer perspective it is debatable whether the purported privacy benefits actually justify the inconvenience and likely increased premium costs.

Innovation in underwriting

As a discipline so heavily reliant on the collection and interpretation of data, much recent innovation in life underwriting has centred around automating the benefits of ‘big data’, and artificial intelligence (AI).

Data can transform underwriting by providing new sources of insight to simplify and streamline current processes of understanding risk. Examples of sources used around the world (but not yet locally) which have proved highly predictive of mortality and lapse experience, include credit scores, charitable giving, pet ownership, fitness protocols, and a range of other behavioral indicators[5].

The use of mobile technology and wearable fitness trackers also opens up new possibilities for underwriting, including the ability for tasks such as blood pressure, BMI and skin checks to be self-administered from the applicant’s mobile phone.

In conjunction with the efficiency health benefits of electronic health records and prescriptions data, the innovation outlook for underwriting is exciting from both an insurer and a consumer experience perspective.

![]()

———-