John Lobb

The past 12 months has provided an interesting short-term phenomenon where Covid-19 accelerated the flight to online shopping and remote communication technologies and food delivery services.

Many growth managers exposed to these stocks performed well. On top of this, many value managers have also done well on the back of the underpriced asset opportunity since the market tumbled about 30%. That said, choosing undervalued stocks was made a little easier in the wake of this ruction and even blue chip stocks were trading at prices not seen since 2008.

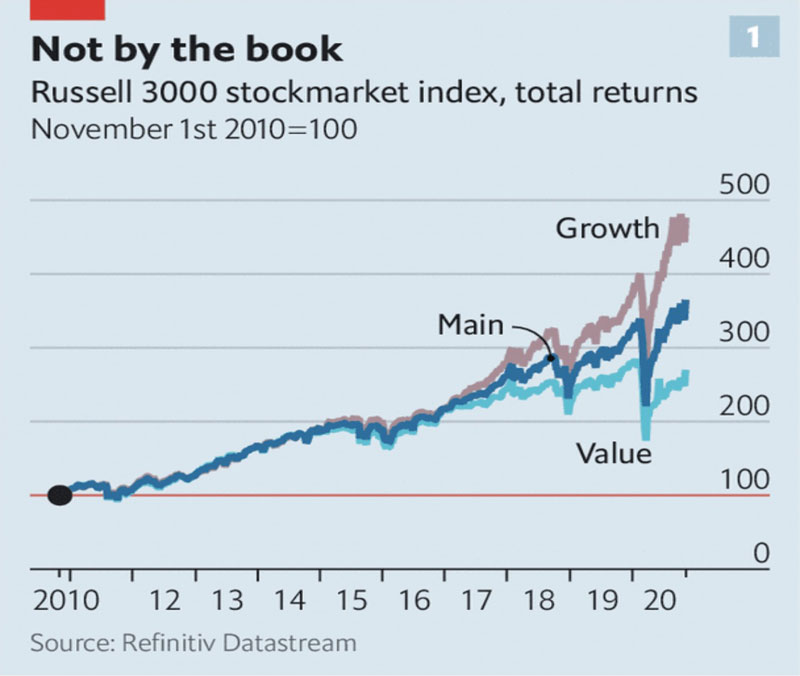

This all begs the obvious question, should investors and advisers tilt toward value management given the apparent ‘time in the sun’ they are enjoying, or focus on growth style firms that have generally outperformed over the past 10 years?

It’s hard to argue with the above data, but recency is a powerful motivator. We know that value management traditionally performs well through periods of economic activity and potentially rising inflation, yet this is not what we are seeing globally, in spite of the excessive central bank stimulus in the wake of the pandemic. Pundits generally agree this is mainly due to the nature of the government spending, which has largely been targeted at welfare and job security rather than economic stimulus and infrastructure. The velocity of money in respective economies has not significantly increased as a result, and there appears structural headwinds to the reflation story which would otherwise benefit value managers. This would suggest betting on growth managers may be the sensible option, and as we are conditioned to expect, the cycle always turns right? Perhaps, but any assumption that we are just in the regular economic cycle that favours one investment style then the other may be flawed thinking.

It is hard to see economic activity increasing massively in the medium term, and any expectation that it will underpin a sustained period of broad growth is very unlikely. Even more so, consumer demand is not bridging the excess in production capacity.

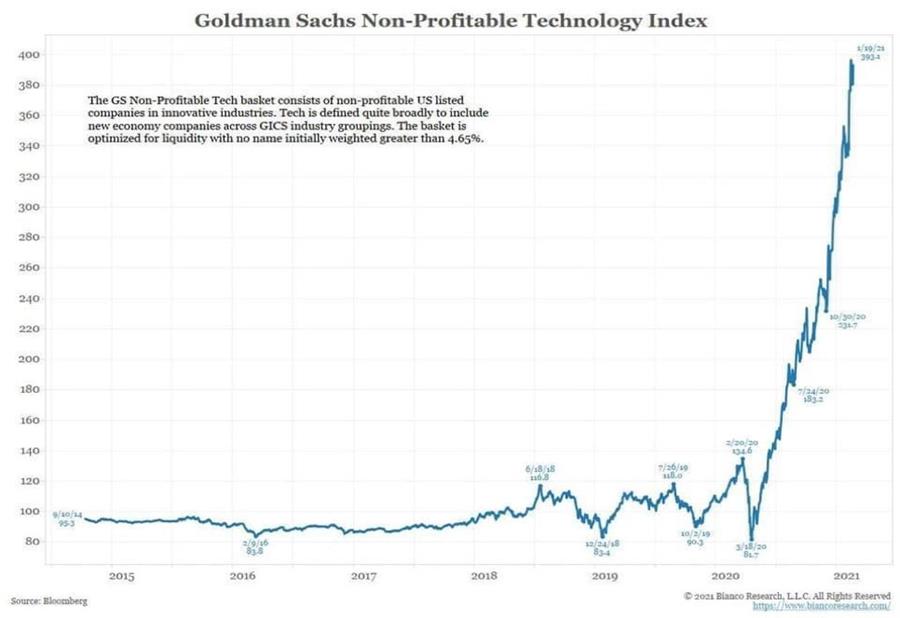

As we noted, 2020 delivered outstanding results for some pure growth managers that were heavily tilted toward quick growing but often low profitability stocks, as borne out by the graph below. It is hard to believe such results will continue given the multiple many of those stocks are now trading on, given the level of prevailing economic activity. So there may be a risk in aligning your portfolio with pure growth stocks focussed on sales acceleration, over sustainable growth and profitability.

Searching for the highest growth stocks based on sales uplift is not how Insync approaches stock selection. “We invest for longer duration than most managers, and our sustainable growth metrics are second to none. This is almost entirely due to our focus on global megatrends,” said John Lobb, Senior Portfolio Manager at Insync Funds Management.

Mr Lobb suggests that it is not purely a choice between value managers or growth managers. The decision is more nuanced than that. “There will be winners and losers from both styles, and the firms most likely to succeed long term through challenging economic times are those positioned for the long term”. Pure growth firms focussing on short term sales expansion will likely be most affected by a market correction, what went up must surely come down at some point as liquidity makes more secure stock choices.

Insync sees a bias toward robust, highly profitable businesses that are congruent with the global themes driving the accelerated changes around us will do best. In that sense investors should consider leaning toward defensive or sustainable growth and quality may be a better option given the uncertain economic times ahead.

By John Lobb, Portfolio Manager