Financial consumer protection – part 1 – practical framework for financial advisers

Leading advisers think about consumer protection in a different way.

Strengthening consumer protection continues to be the underpinning theme for much of the ongoing scrutiny and regulatory change seen within the financial services industry in recent years. And, at high level, measures which increase confidence and trust in the sector can deliver meaningful benefits both customers and advisers. However, such measures can become problematic, even counterproductive, if they reinforce the perception that consumer protection is all about procedural compliance.

Leading advisers, however, think about consumer protection in a different way, understanding that an advice philosophy – supported by the right processes – that is built around protecting customers is less about avoiding complaints and meeting compliance obligations, and more about opening up deeper, more trusting client relationships, in turn allowing more effective advice and better client outcomes.

This article is the first in a two-part series in which we explore the concept of financial consumer protection, and examine the practical steps financial advisers can, and do, take to protect the interests of their customers, as well as the benefits of doing so. We will see that, rather than being discrete ‘consumer protection actions’, these steps are in fact woven into the fabric of the services, customer interactions and processes seen in leading financial advice practices every day.

Understanding financial consumer protection

The increasing complexity of financial products, and the potentially devastating consequences of poor decision making around these products, create an impetus for protecting customers which is perhaps greater than in other categories of goods and services.

Indeed, the 80,000 plus complaints received by the Australian Financial Complaints Authority (AFCA) in the 2019/20 financial year[1] illustrate the significant quantum of unmet customer expectations across the banking, superannuation, investment and insurance sectors. (Advice complaints represented a mere one third of one percent – around 280 – of these[2]).

But whilst a significant number of these unmet customer expectations can be attributable to shortcomings (including poor product design, bad service and ineffective communication) on the part of financial services providers (as evidenced in the $185 million in compensation[3] paid in relation to these complaints), in many cases it is customers’ own (understandable) lack of knowledge that predicates the complaints, and in this sense, it is true that consumers also need protecting from themselves.

To the extent that customers choose to compensate for this knowledge shortfall by seeking the help of a financial adviser, it has been argued that expert financial advice is in itself a form of consumer protection. Dr Richard Sandlant, for example, in his paper ‘Financial Consumer Protection: future directions[4]’, identified advice as one of the four pillars of financial consumer protection, along with financial literacy, financial product regulation, and financial product disclosure.

For the purposes of this paper, we believe that a philosophy of consumer protection can inform the design of several foundational advice processes, including financial literacy and education, and informed client consent.

Financial literacy in Australia

Notwithstanding Australia’s relatively high levels of financial literacy when ranked globally (a 2014 survey[5] put Australia in the Top 10 most financially literate countries), a recent Household Income and Labour Dynamics in Australia (HILDA) survey estimated nearly half (45%) of all Australian adults to be financially illiterate[6]. Such widespread financial illiteracy is of great concern within the context of highly complex financial markets, high levels of personal and household indebtedness and easy access to credit opportunities (from increasingly non-traditional sources).

The HILDA Survey gauged financial literacy via a series of basic questions – known as the ‘Big Three’ – relating to interest rates, inflation, and diversification, and found that just over half of all adult Australians (55%) are financially literate. A large gender gap in financial literacy was also identified; two-thirds (63%) of Australian men were found to be financially literate, compared to only 48% of Australian women (as shown in Figure 1, below). Financial literacy levels were also found to be lower for other socio demographic groups, including those from non-English speaking backgrounds and those without tertiary education.

Financially literate consumers are better protected

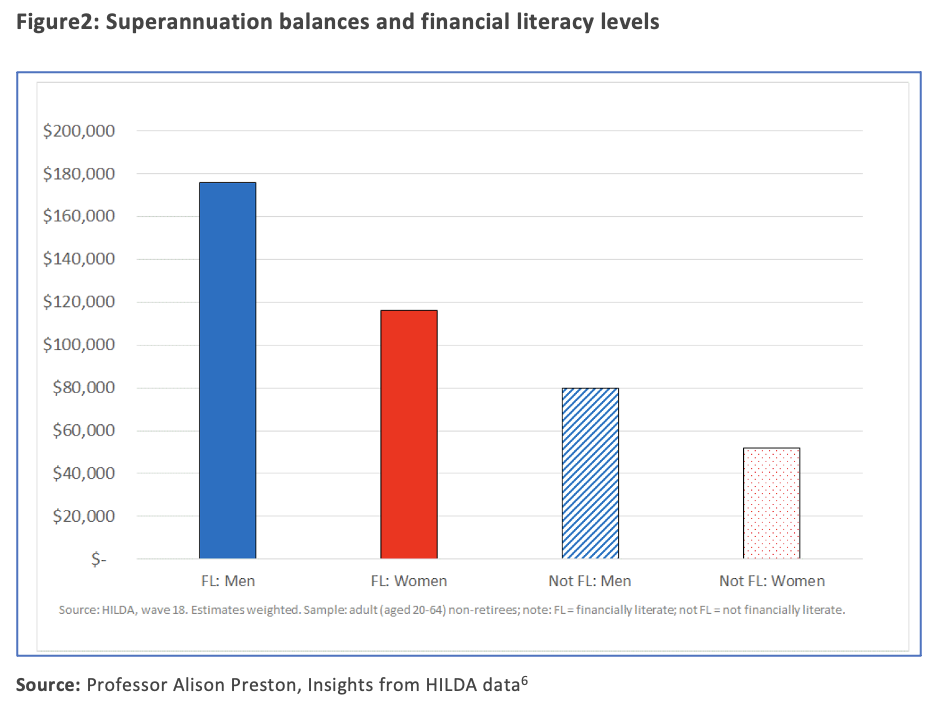

There is increasing recognition of the importance of financial literacy to consumer protection in Australia and internationally. The growth in both the range and complexity of financial products and services requires individuals to have sufficient financial literacy to make sound investment decisions and to understand their consumer rights and identify when these have been infringed. Financially literate consumers are more likely to be informed and confident and therefore better able to participate in economic life. Indeed, research confirms that financial literacy is an important determinant of a range of outcomes including wealth accumulation, superannuation savings (see Figure 2 below), retirement planning, and women’s economic empowerment and domestic violence.

The higher emotional and physical wellbeing associated with increased financial confidence and control – identified across much research[7] – is also noteworthy and of value to the community overall, not just the individuals.

In simple terms, financially literate consumers are better protected and equipped to benefit from, rather than fall victim to, our financial system.

Financial advisers and financial literacy

For financial advisers, the financial literacy of their clients represents both an obligation and an opportunity.

The obligation relates to the understanding one must have of the client – including their level of financial literacy – in order to satisfy the best interests duty.

The opportunity is to impart their own knowledge and experience to the client so as to improve the client’s overall financial literacy, which in turn is likely to have the following benefits:

- Clients will have a greater understanding and appreciation of the value of advice

- They are more likely to trust the advice and the adviser, meaning they remain committed to the advice rather than making frequent changes

- They are more forthcoming in what they disclose to their adviser, allowing the advice to be more targeted and more effective and deliver better outcomes

- They are less liable to panic in the face of market volatility

- Client expectations around advice outcomes will be more aligned with reality, leading to lower levels of complaint and higher levels of satisfaction

- The overall client adviser relationship is likely to be deeper, longer, and more profitable.

How advisers can educate their clients

Advisers are uniquely qualified – and positioned – to improve the financial literacy of their clients. Many advisers specifically incorporate financial education into their advice processes, especially in their early client engagements. Others make it an important part of their ongoing service offering, at check in and review meetings, and communicated via regular newsletters and events. Some advisers even use financial education programs as lead generation mechanisms in their own right.

Whilst there are many tried and tested approaches advisers can use to deliver financial education in a scalable way, ultimately education, like advice itself, needs to be tailored to the different needs and learning styles of individual clients (although in call cases it should avoid jargon!).

Case study 1: Award-winning adviser makes financial literacy central to business

Against the orthodoxy of a profession that predominantly segments clients based on monetary value or investment worth, one former AFA Adviser of the Year segments her clients individually, based on their practical financial knowledge. That level of knowledge dictates what gaps she needs to fill, via an array of self-developed tools including flipcharts and glossaries.

She does not charge for this time believing that time spent educating clients is never a burdensome cost, but rather an investment in her clients.

The adviser says her new clients generally fall into three basic types: learners, self-directed and delegators. But regardless of sophistication, each new client experiences the same proprietary approach, beginning with a one-hour initial meeting and the presentation of a blank 128-page journal.

The journal represents the beginning of self-responsibility for the client. It is in here that a client makes notes, jots ideas, drafts questions – it is a living and engaging record of their growing understanding of the advice process, and the rationale for the portfolio or strategy constructed in partnership with the adviser.[8]

Advice and informed consent

Financial literacy is also the foundation on which another important consumer protection mechanism – informed consent – can be built. If financial literacy is about clients understanding financial matters in general, informed consent is about them understanding their own specific financial circumstances and decisions.

The concept of ‘Informed Consent’ is at the centre of every meeting between a doctor and their patient. Informed consent means that the patient understands their options, the risks of each alternative and the reasons why their doctor thinks a particular treatment is best. That understanding means the patient can consent to the treatment in an informed way – with their eyes genuinely open.

Unfortunately, financial advice processes are not universally based on such an approach.

Whilst the idea of informed consent is mentioned, explicitly, in the AFA’s Code of Conduct[9](Principle 4, Informed Client Consent) and FASEA[10] Standards 4 and 7, – and implicitly in FASEA Standard 5 – the meaning, application and enforcement of these requirements is still open to widely varying interpretations and for the most part lacking clear benchmarks and standardised practices.

This is unfortunate, as informed consent can represent a ‘win’ for both clients and advisers when applied in a financial advice setting.

Clients win because they get ownership and control over their financial lives – the ‘self-responsibility’ mentioned in the case study above – and are more likely to stick with their plan. Advisers win because their advice becomes more professionally robust. Client expectations around the implementation of the advice are better managed, disputes reduced, and adviser/client relationships can be more harmonious.

Industry expert Paul Resnik – of the Suitable Advice Institute – sees three precursors to obtaining informed consent in an advice context[11].

- Have a thorough understanding of client’s goal, circumstances and risk profile

- Have a detailed knowledge of the possible risk and return outcomes – including worst case scenarios – across the products being considered

- Present a well-reasoned argument as to why the recommended options are superior to others.

The diligent recording of client discussions and decisions takes on even more importance in an informed consent model, as does the formalising and documenting of the educational resources and techniques used in ‘informing’ the client’s decisions.

Garnering informed consent can be challenging and time consuming (and thus expensive), and unsurprisingly many standardised fact – finding, risk profiling and investor classification mechanisms used across the industry fall short of could be regarded as truly informed consent.

And whilst some advisers maintain that “clients don’t always want to be educated and understand. They just want to be told what to do”[12], such a paternalistic approach is at odds with contemporary concepts of empowerment and is more likely to leave both clients and advisers exposed to serious and unwanted risks.

Case study 2: When consent isn’t informed

Client ‘A’ was a 41 y.o. recently divorced single mother of three young dependent children and her only source of income was $30,000 per annum in maintenance payments received from her ex-husband. Her investment assets consisted of approximately $1,000,000 which was invested two term deposits and $100,000 in a savings account.

She engaged the services of a financial adviser, and as part of the initial fact-finding process was asked a series of questions designed to determine her attitude to risk and her tolerance for volatility in her portfolio. On this basis she was assigned a score, allowing her to be categorised as an investor and matched with pre-determined asset allocation.

Despite telling the adviser she regarded herself as conservative, her responses to the risk profiling questions saw her score 15, which according to the methodology used by the adviser, put her on the cusp of the ‘conservative’ and ‘balanced’ investor categories.

Whilst the client didn’t personally agree with description ‘balanced’, she took comfort in brochures and documents which described the ‘conservative’ investment philosophy and style of the investment manager.

Believing her portfolio would be invested in a conservative manner, the client signed off on the advice, which was then implemented accordingly.

Around a year later, the value of her investment had dropped considerably, during a period of extreme market volatility. At this point, she contacted her adviser indicating she was nervous and was considering switching out some of her investment. Having initially heeded her adviser’s counsel to stick with the strategy and avoid knee jerk reactions, several months later she left the practice, engaged a new adviser and subsequently lodged a complaint with AFCA, seeking various amounts including $116,000 in direct investment losses on her portfolio (this being the difference between the actual value of her portfolio and the notional value of a ‘conservative’ portfolio.

AFCA found in favour of the complainant, noting: “The fact that she had signed off on documents not objecting to the provider’s classification of her being a ‘balanced investor’ did not make her a balanced investor.”

AFCA further noted that, even if was accepted the client was a ‘balanced’ investor, it should have been apparent to her adviser that she was at the most conservative end of the balanced spectrum. A strategy should have been developed on that basis to meet her individual needs[13] .

Conclusion

Leading advisers see ‘consumer protection’ not about procedural compliance and reducing future exposure to complaints, but as a philosophy predicated on customer care and professionalism.

Two of the more fundamental protections an adviser can offer their clients are (1) improving the client’s financial literacy and (2) garnering their truly informed consent to implement strategies they have collaborated on as part of the advice process.

In this sense, rather than implementing discrete ‘consumer protection’ steps, the adviser is weaving their philosophy on consumer protection into the fabric of the services, customer interactions and processes they use every day, and which form the basis of their trusting, sustainable and profitable partnerships with clients.

Read the next articles in the series:

Financial consumer protection – part 2 – the art of the conversation (having, recording, storing, using, protecting)

Financial consumer protection – part 3 – adviser priority checklist and calendar

———