Client engagement in the new world – Adviser toolkit

A number of providers have developed downloadable toolkits to enable advisers to map out the client experience.

Client engagement – it’s time for new tools

Financial advisers have been dissecting the topic of client engagement for decades, and with good reason; client engagement is the bedrock of effective and sustainable adviser/client partnerships, and those who crack the code can enjoy spectacular business success and rewarding relationships.

But while some fundamental aspects of the engagement code remain unchanged (understanding the psychology of your client, active listening, remembering their milestones, generally being interested in their lives), others have evolved, disrupted by digital technologies, increasing consumer expectations, and even a pandemic.

The time is now right for financial advisers to reassess their client engagement strategies and review the tools they have at their disposal to drive next level engagement in a COVID world.

Satisfied clients aren’t always engaged clients

As we are regularly told, engaged clients are more satisfied, more loyal, more trusting, more likely to refer, and, ultimately, more profitable. In the absence of any universal metric of client engagement, it is not uncommon to infer engagement levels from measures of client satisfaction. And, on that basis, one could assume Australian financial advice clients are incredibly engaged. After all, in a 2019 survey[1], 94% rated their advice experience either good or excellent. And 95% said they trusted their adviser.

But dig a little deeper and we see the picture is a little less rosy. Only two thirds said they would recommend their adviser to friends and family, and, even more alarmingly, more than half said they didn’t have definitive loyalty to their adviser (Figure 1 below).

Many advisers have themselves admitted client engagement is something they struggle with; a study of over 200 advisers found that 60% were spending less than 3 hours per week on client engagement, with many citing a lack of time and a lack of expertise as major impediments to client engagement activities[2].

So, is the solution to better engaged clients as simple as spending more time on engagement activities?

Or does our concept of client engagement – and what drives it – need rethinking?

Client engagement as ‘co-creation’

Successful, engaged marriages do not result from fulfilling discrete ‘engagement’ tasks in some tick-box fashion; they result from the ongoing, two-way connection between two parties.

Similarly, rather than thinking of client engagement as being a standalone process – distinct from other elements of the advice process – and something to which we need to allocate specific time, perhaps we should think of client engagement as being the outcome of a philosophy, one we embed into every interaction and touchpoint that exists between the advice practice and the client.

So, what actually is client engagement? Among the extensive literature on the topic, this definition from 2011 is particularly useful:

“A psychological state that occurs by virtue of interactive, co-creative customer experiences with a particular agent/object (e.g., a brand)”.[3]

As well as conveying the idea of interactivity – important because it suggests someone is actually interested and invested – this definition suggests engagement is an outcome of ‘co-creation’; in other words, the customer experience is one that they feel they have had a role in designing.

While to many readers the idea of a co-created advice experience may seem far-fetched and impractical, when reframed as personal relationships and tailored service offerings, the concept becomes far more accessible.

Is advice really customer centric?

The term ‘customer centricity’ is thrown around so cheaply these days that it’s almost irrelevant. After all, what company would say customers aren’t at the heart of their business?

In a financial advice context, the regulatory requirement that personal advice be truly tailored to the clients’ needs, and that the adviser always acts in the best interests of the client, could be seen as ensuring a base level of customer centricity. But if we take a step back and view the financial planning process from the client’s perspective, is it truly customer centric? And is it really designed to encourage engagement?

Table 1, below, breaks down the typical steps in an advice relationship, and how it could be seen from both perspectives.

Even allowing for minor variations, the obvious point is that this process is not truly customer centric. No amount of cloaking the process with espresso machines, funky boardroom presentations and complimentary umbrellas gets away from the fact that it’s a modern-day version of Henry Ford and his Model T Ford (which only comes in black).

Re-imagining and co-creating the advice relationship

Advisers seeking to create a framework for more engaging advice relationships now have a variety of tools at their disposal. By using these tools and making some important strategic decisions (in areas such as business vision and target customers), advisers can lay the foundations for a genuine two-way partnership between themselves and their clients, ultimately leading to better advice outcomes. Engagement expert Julie Littlechild[5] summarises the steps to embed these tools and decisions as:

- Clarify your vision for the client experience and align with target market

- Bring your staff and clients to the table to co-create this experience

- Design the communication and other processes to support this experience

- Gather and use feedback to constantly monitor and refine.

Aligning vision with audience – time for some hard decisions

One of the great truisms in life is that you can’t be all things to all people. In a client experience sense, this means it is nearly impossible to offer a truly differentiated and deeply meaningful service experience to all types of customers. And yet different people do engage with people and brands differently.

Differentiating a practice on the basis of client experience therefore involves making important – and difficult – decisions about what type of client the adviser would like to target. This decision can be high level (small business owners, pre-retirees, young professionals) or specific (doctors, pilots, sports professionals, military personnel).

This is a complex decision involving the analysis of many factors, including:

- The adviser skill set and interests

- Geography

- Size, growth and profitability of different segments

- Competition for those segments.

Having decided on the target audience for the business, the adviser then needs to check the high-level alignment between their vision for the client experience and the likely needs of the target audience.

Does a high touch face-to-face experience suit the needs of young professionals? Is your vision of a low touch, minimalist digital experience likely to appeal to an older audience?

The ability and need to change audience and/or the client experience vision will obviously depend on where the practice is in the business cycle – for example, more established businesses may well decide their target client is fixed, and the vision is variable. Newer practices may have more flexibility.

Map your clients’ journey – feel their pain

Once you’re clear about your target audience, it’s time to bring them to the table to start designing the client experience.

This co-creation can occur at two levels. At a basic level, it covers the individual personalisation that occurs when the client makes choices across a variety of service elements (including advice type, review frequency, remuneration mechanism, communication frequency and preferred engagement channel).

However, a higher level of co-creation results when we gather deep insights into the customer journey, and then build a process around those insights. This process is called customer journey mapping, and typically involves these steps[6]:

- Define your ideal/existing client profile

- Develop a client persona (a detailed description of who they are, what they do, think and feel)

- Define phases of their journey with the category and with your business (think of all touchpoints)

- Identify steps the client is taking in each phase to solve their problem

- Identify what the client is thinking throughout the journey

- Quantify their emotional journey.

Although journey mapping has typically been done by large brands and organisations, there are tools available that make it scalable to the needs of smaller advice practices.

A number of providers have developed downloadable toolkits [7]to enable advisers to map out the client experience – from the client’s very first interaction with your business (perhaps via your website or your office reception) to ongoing engagement.[8]

By identifying customer frustrations and pain points in their journey, service experiences can be adjusted to minimise or eliminate these pain points going forward.

Step 6 in the above process recognises the emotional benefits clients derive from financial advice and the advice process. Research[9] suggests that participating in activities aimed at developing goal setting and planning skills can increase subjective wellbeing and personal growth over time (in particular, life satisfaction). Appreciating the emotional benefits derived by clients from each stage of the advice process allows advisers to consider whether the experience they deliver clients at each stage is optimising this wellbeing effect.

As valuable – and important – as this process of stepping into the clients’ shoes is, a truly engaging experience needs to be based on real customer insight and input, and delivered consistently by all staff across the entire business.

For this reason, the optimal process is one where staff and customers have been involved in both mapping the journey and designing solutions to the pain points.

Communication, marketing and engagement channels

COVID-19 significantly accelerated the shift to digital engagement models across many categories, including financial advice. Indeed, some experts claim the pandemic pushed forward 10 years of technological progress in areas ripe for innovation[10].

To the extent that technology can drive efficiencies and make it easier for advisers to offer personalised and tailored experiences in a scalable way, this is a clear silver lining for advisers and clients alike. A 2020 report by KPMG into financial services customers[11] found a consistent increase in support for digital contact methods during the COVID era across consumers – whether they had previously preferred this approach or not. Email was preferred (36%), with live chat and mobile app next (28%) and then online portals (27%); with convenience, accessibility and saving time the key benefits, especially for older Australians.

Online meetings

One of the most obvious and immediate changes seen in adviser/client interactions during this time was rapid uptake in online meetings. According to Investment Trends research[12], Australian advisers were quick to pivot, with 83% of advisers saying they were conducting all meetings online at the end of March 2020. While handshakes and face-to-face meetings will undoubtedly return, much of this shift will be enduring as both advisers and clients recognise the convenience and efficiency benefits:

- The ability to connect with clients across a variety of devices makes it viable to rethink the traditional contact strategy, such as scheduling shorter but more frequent meetings instead of the longer, annual catch up.

- Most video conference platforms enable calls to be recorded. In conjunction with simple transcription programs, advisers can produce a video and text file which can be appended to advice records, strengthening their ability to meet compliance and regulatory obligations.

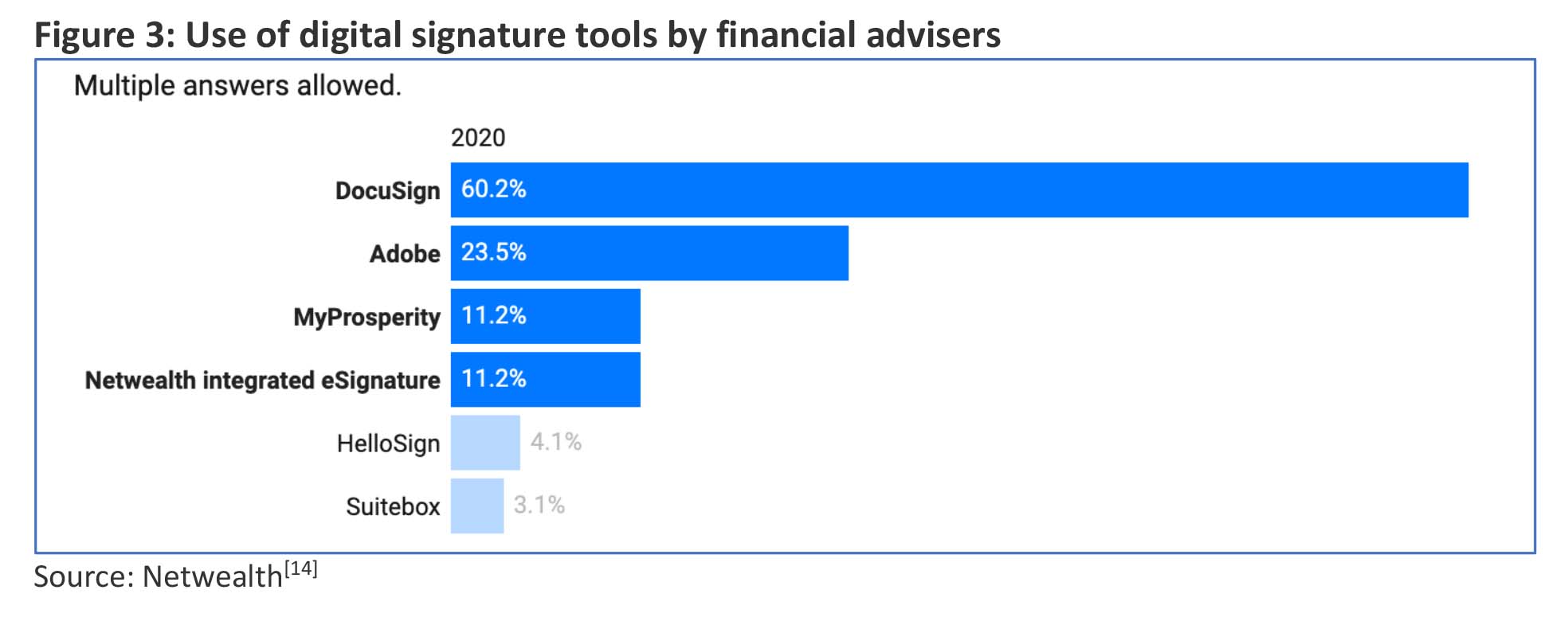

Digital signatures

A variety of digital signature tools are now available, enabling signatures to be easily captured online. Obviating the need for clients to sign and return paper forms (either by post or in person) not only enhances the client experience, but also helps increase the speed at which applications are completed and SOAs and ROAs are accepted, significantly improving practice efficiency.

Research from the Netwealth 2020 AdviceTech Report[13] shows that the top suppliers of digital signature tools used by wealth professionals and financial advisers include DocuSign, Adobe and MyProsperity.

Online portals

Digital client portals enable advisers to provide detailed, tailored reporting with the most up-to-date portfolio information. They can drive better engagement in a number of ways, including:

- Investors have access to their portfolio 24/7 on any smart device, enabling them to stay continually informed about its status

- Meetings or calls can be less focused on portfolio updates and more on strategy, life event planning and progress against advice objectives, enhancing overall client satisfaction.

The social media renaissance: is your website still the best place for content?

Given the omnipresence of social media in every aspect of our lives it seems far-fetched to talk about a renaissance, but COVID has seen the social landscape change dramatically, with increased usage, new platforms and a transformation in the usage of some old favourites.

According to a recent Social Media Census conducted by L&A Social[15], the average time spent on social media has increased a staggering 30% since the start of COVID (coinciding with the meteoric rise of TikTok). Those tempted to dismiss these channels as trite, vanity fuelled, and inappropriate for serious (e.g., financial) communication could well end up with egg on their face, as we see Australians of all ages turn to social channels to discuss and learn about financial matters.

High-profile examples include the Reddit finance community which took the Gamestop stock price on a wild ride in the US and the #moneytok and #stocktok channels on TikTok, which have been viewed 3.8 billion and 361 million times respectively[16]. On Instagram, once filled with pictures of shoes, cars and holiday snaps, you’ll find no end of slideshows offering guides on topics ranging from straightforward household budgeting to diversifying your income, and what an ETF is. Every day on Facebook there are multiple live videos from ‘experts’ discussing financial topics. (LinkedIn continues to be a popular channel for Australian financial advisers to post content, including videos.)

These channels seem to have resonated particularly with a younger, more tech savvy audience and with females, many of whom feel disconnected to a financial advice sector perceived as male dominated (in this case perception may be reality – the FPA estimates around 80% of financial advisers are male[17]). In Australia, one of the most successful ‘financial influencers’ is the She’s on the Money podcast, produced by financial adviser Victoria Devine of Zella Wealth. Central to the podcast’s success is the engagement Devine drives through the @shesonthemoneyaus Instagram group. The group is private, so followers must request to join, and interactivity is encouraged, both with the host and between other group members, who share their experiences and post questions.

While the deluge of poor-quality content from some of these financial influencers is a major concern (advisers, on the other hand, must comply with strict ACCC guidelines[18] on social media), the massive audiences they are attracting suggest that consumers absolutely see these channels as appropriate for discussing financial topics.

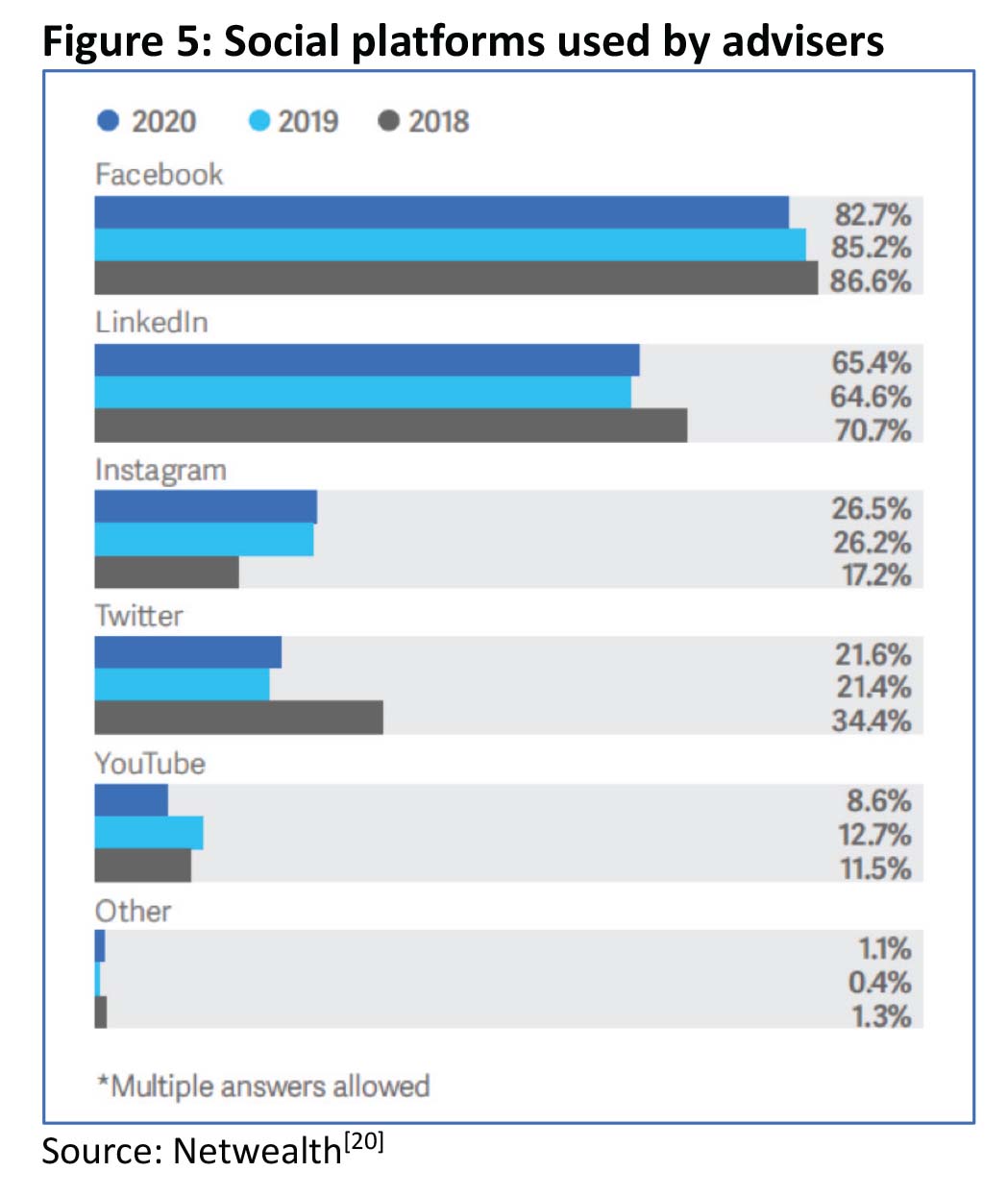

To a large extent this is likely to be a more effective way of engaging with potential new clients than a more traditional search engine/website strategy. The charts below, from research by Netwealth, highlight the importance of social media in Australian advisers’ engagement toolkit, and shows advisers’ increased usage of Instagram in recent years.

Case study – She’s on the Money @shesonthemoneyaus

Produced by Australian financial adviser Victoria Devine of Zella Wealth, the She’s on the Money podcast rocketed from 17,000 members on Facebook, and less than 500 Instagram followers, to 130,000 and 70,000 respectively by the end of 2020. The podcast offers general advice and information to a highly engaged community who actively share stories about money wins and losses, and ask questions about everything from the best gas providers to building up super funds.[21]

Measuring engagement – feedback good, input better

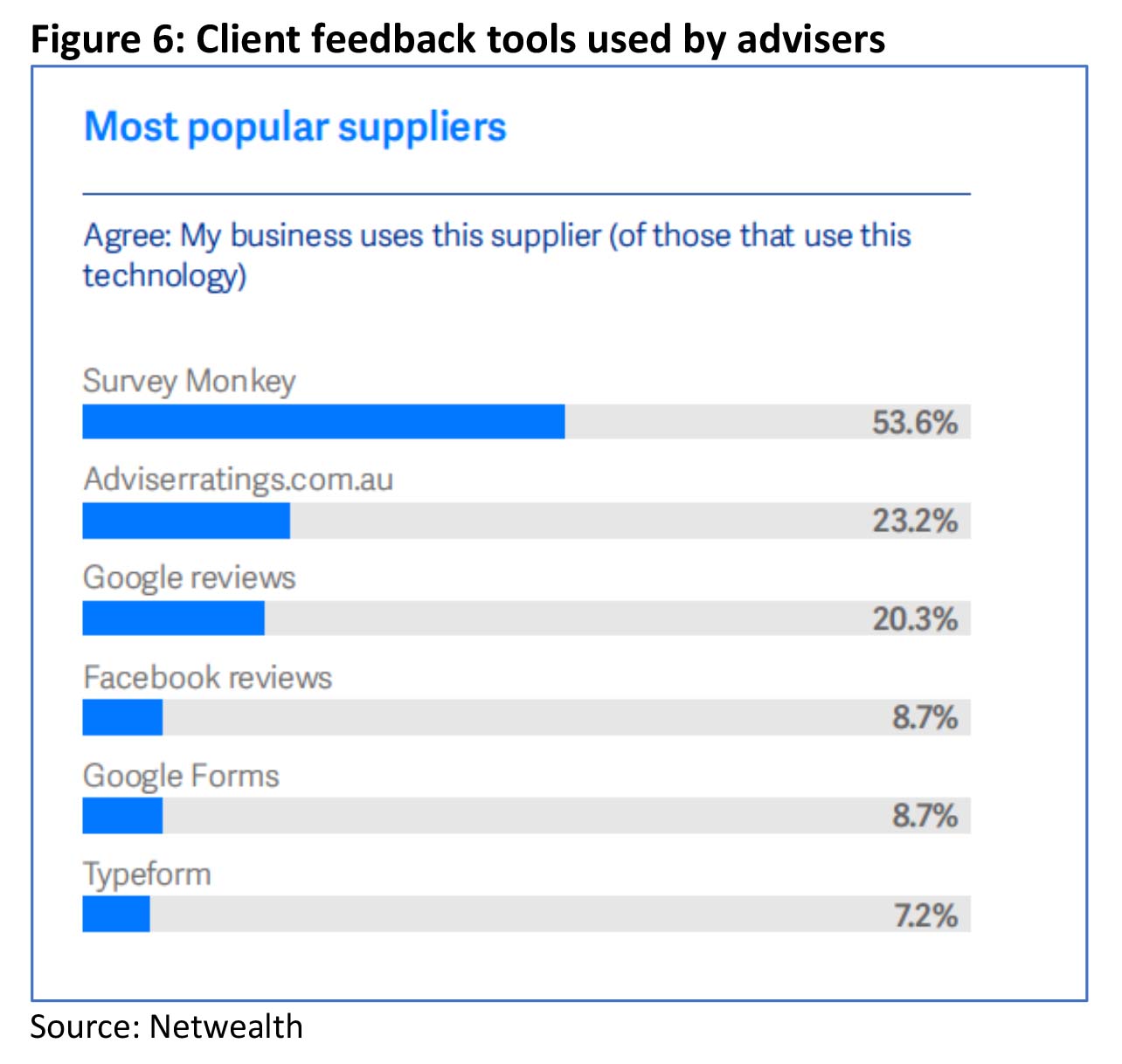

Research has found 94% of advisers feel feedback is critical to engagement[22]. Typical methods to gather this feedback range from informal conversations, through to online/email surveys, through to customer advisory boards (Figure 6 below shows some of the digital tools used by Australian advisers to gain client feedback). Regardless of method, gathering feedback helps understand:

- Overall satisfaction on specific aspects of service

- What is most important to your clients

- What activities or communications they value the most

- What clients need and expect from the relationship

- If clients are interested in other services

- If clients have provided a referral.

However, to truly involve your clients in ‘co-creating’ the client experience – and turbocharge your client engagement strategy – advisers should be seeking not just feedback, but input. This means going beyond asking them to rate a service out of 10; it means working with them on how that service could be improved to avoid their pain points and frustrations (see above). This is a two-way process, which works well in the context of small focus groups (where you invite small groups of clients to openly share their thoughts about your business).

Run your own focus groups

Focus groups ideally involve around 6 to 9 people and can be held in your offices. Plan for them to run for an hour or so, and put on some light refreshments.

To encourage clients to really open up about their experiences and ideas, it can sometimes be better to have these groups moderated by someone they don’t know. Questions need to be open-ended, and you can record the discussions (with your clients’ permission) so you can type up the notes later. The real power from this two-way dialogue is to make it clear you intend to act on the feedback – which means the way you follow up is crucial.

Demonstrating you have made changes as a result of talking to your clients gives them a real sense of ownership and buy-in, taking your engagement to the next level.

Conclusion – the old ‘rules of engagement’ no longer apply

The importance of client engagement remains paramount to sustainable and profitable adviser/client relationships. But the old ‘rules of engagement’ no longer apply in a world disrupted by technology, social change and a global pandemic. By adapting to new digital habits and consumer preferences, advisers can open up a more genuine two-way dialogue with their clients, helping them design more personalised client experiences and enabling them to take their client engagement, and business, to new heights of success.

———-

References

[1] https://www.momentumintelligence.com.au/client-experience-survey

[2] https://www.futureofadvice.com.au/business-toolkit/latest-white-papers/client-engagement-guide/

[3] Brodie, R.J., Hollebeek, L.D., Ilic, A. & Juric, B. (2011), ‘Customer Engagement: Conceptual Domain, Fundamental Propositions & Implications for Research in Service Marketing’, Journal of Service Research, 14 (3).

[4] https://www.kitces.com/blog/reimagining-client-meetings-with-a-more-client-centric-financial-planning-process/

[5] https://www.cfainstitute.org/en/research/multimedia/2019/how-financial-advisers-can-deepen-client-engagement

[6] https://www.kaleidocreative.com/blogs/financial-advisor-client-journey-map

[7] Downloadable Toolkit: https://netwealth.com.au/web/insights/netwealth-innovation-toolkit/customer-journey-workshop/

[8] More downloadable Toolkits: https://www.kaleidocreative.com/blogs/financial-advisor-client-journey-map

[9] ‘Personal goals and psychological growth: Testing an intervention to enhance goal attainment and personality integration’, Sheldon, K.M., Kasser, T., Smith, K. & Share, T., Journal of Personality, vol.70, no.1, 2002.

[10] https://www.cnbc.com/2020/11/10/pandemic-forced-advisors-to-find-new-ways-to-engage-with-clients.html

[11] https://home.kpmg/au/en/home/media/press-releases/2020/07/four-fifths-consumers-prefer-digital-financial-services-covid-19-study-8-july-2020.html

[12] https://www.professionalplanner.com.au/2020/04/covid-19-the-second-biggest-challenge-for-advisers-in-2020/

[13] https://www.netwealth.com.au/web/insights/netwealth-2020-advicetech-report/2020-netwealth-advicetech-suppliers-guide/

[14] Ibid.

[15] https://www.bandt.com.au/aussies-spent-30-more-time-on-social-media-during-the-pandemic/

[16] https://www.theguardian.com/money/2021/jan/30/who-uses-social-media-for-financial-advice-lots-of-people-actually

[17] https://thewest.com.au/business/your-money/why-we-need-more-women-in-financial-planning-ng-b881303690z

[18] https://www.accc.gov.au/business/advertising-promoting-your-business/social-media

[19] https://www.netwealth.com.au/web/insights/netwealth-2020-advicetech-report/2020-netwealth-advicetech-report/

[20] Ibid

[21] https://www.theguardian.com/money/2021/jan/30/who-uses-social-media-for-financial-advice-lots-of-people-actually

[22] https://www.thinkadvisor.com/2012/09/25/4-ways-for-advisors-to-better-engage-clients/