A new advice model to protect financial consumers – when Do-it-yourself becomes Do-it-together

Our love of DIY is also being channeled into investing.

Australian investors are having a Bunnings moment.

Lured not by a cheeky sausage sandwich between meals, but by a sharemarket that continues to defy gravity, our love of DIY is now being channelled into investing, as record numbers of Australians join the ‘Robinhood revolution’ and become investors for the first time.

Echoing overseas trends – and driven by a confluence of factors including low interest rates, Covid lockdowns, the proliferation of low cost and fractional investment platforms, and the ‘finfluencer’ phenomenon – investment markets have been transformed by an influx of investors who are younger, more active, and more prepared to take risks.

And while some of these new investors are entering the market with the help of experts – driving an increase in demand for financial advice – the majority are self-directed.

So, whilst innovation and the democratisation of investing should be celebrated, there is a feeling amongst many experts – and regulators – that this surge in amateur investing could represent a ticking time bomb, the detonation of which has hitherto been deferred by a continuing bull market.

From a financial consumer protection perspective, this new enthusiasm for DIY investing raises a number of important questions:

- Should regulators intervene?

- Should access to some investment types be limited?

- Will improved financial literacy help?

- How can we encourage such people to seek expert advice?

Ultimately, answering these questions may lead us to pose another:

- Is the time right for a new model of advice, where ‘self-directed’ investors and financial advisers work with each other?

The rise of the amateur

It is estimated that round 46 per cent of us now hold investments other than our primary residence or superannuation[1]. And whilst much of that money has been ploughed into bricks and mortar (our largest investment by far), many of us fancy ourselves as stock pickers too, with research suggesting 6.6m Australians own listed investments[2], and over 1.25m of those are described ‘active’ online investors[3].

Even when it comes to superannuation, the self-directed route has proven popular, with over 594,000 SMSFs currently registered with the ATO[4], a figure projected to grow further.

But whilst our love of DIY is hardly newsworthy, it is the recent meteoric, growth in retail investors, especially since the start of the pandemic, which has provided fertile fodder for market observers and regulators.

In Australia, the last year has seen over 400,000 investors made their first ever sharemarket trade[5], fuelling an increase in active traders of nearly 35%. Many of these investors have looked beyond our shores for opportunities, seeing participation in international equites double[6] over the 12 months to December 2020.

Much of this growth is being driven by younger investors. According to Canstar[7], around 40% of young Australians invested in the sharemarket in 2020, with 44% of millennials participating for the very first time.

And the way they participated was noteworthy too.

The majority (58 per cent) directly invested in shares, 30 per cent invested via a managed fund, 20 per cent via a fractional investing app (e.g., Sharesies, Spaceship, CommSec Pocket) and 17 per cent via an exchange-traded fund[8].

Outside the traditional sharemarket, it is estimated that around 1 in 6 Australians already hold some form of crypto or digital currency[9], with 4 million[10] expected to purchase some over the coming year. Perhaps unsurprisingly, Millennial and Gen Z investors are almost twice as likely to go down this path then their boomer and Gen X compatriots.

What’s driven the rush?

The transformational change in the face of investment markets, over the last 2 years in particular, has been seen around the world, and owes itself to a complex interplay between a number of powerful economic, societal, and technological forces.

Money is moving away from real estate and cash

From an economic perspective, interest rates which were already low pre-Covid have fallen further and will remain low for the foreseeable future. This has had a two-pronged impact for investors, making cash-based savings products even less attractive, and fuelling a red-hot real estate market.

Those who have been prompted to give up on their Great Aussie dream have looked for a new home for their investment dollars, whereas those who remain undeterred have had to look for ways to accelerate their savings as the required deposits continue to grow. (Post-Hayne tighter lending requirements probably deserve a mention here too). Regardless of which these two camps a person falls into, shares now look a lot more attractive.

Technology, finfluencers and social trading

Amongst the many disruptive forces shaping investment markets in recent times has been the proliferation of app-based trading platforms which through cheap pricing, gamification, and fractionalisation, are turbocharging this ‘democratisation’ of investing.

While global poster boy for these platforms – Robinhood – isn’t available to Australian investors, there is no shortage of local alternatives.

Australian born trading platform Stake, which allows zero brokerage access to US shares, has amassed well over 100,000 customers since launching just three years ago. New users jumped 129 per cent in the six months to June 2020, compared with the previous half-year[11].

Zip and Afterpay backed platform SuperHero, which only launched in September 2020, and offers a flat $5 per trade (and $100 minimum investment), took less than a month to reach 10,000 users and by the end of January 2021 had over 35,000[12].

At the same time, we have seen rapid growth in largely unmoderated financial and investing ‘tips’ – the ‘finfluencer phenomenon’ – through social channels such as TikTok, YouTube, Facebook and Instagram.

On TikTok, the hashtag #FinTok has attracted more than 400 million views, while #stocktock has over 1.4 billion, #crypto over 4 billion, and #cryptocurrency over 1.7 billion views. Closer to home, Sydney based finfluencer Queenie Tan’s posts have gained her more[13] than 20,000 followers on Instagram on TikTok. Her videos explaining Australian tax rules for cryptocurrency capital gains and offering tips for first home buyers have each been viewed more than 300,000 times, and both last less than a minute.

The combination of more accessible markets and more accessible investment ‘knowledge’ has undoubtedly encouraged and empowered many new investors to enter the market.

Did Covid induced boredom drive the market?

The impact of Covid on investing has been undeniable, and in many respects may seem counterintuitive.

As businesses and sporting activity, and indeed most aspects of life, came to a grinding halt – especially at the beginning of the pandemic – tens of millions of people around the world found themselves at home, either unemployed, or working remotely. And many of them were bored.

For men in particular, that boredom was compounded by the almost complete absence of live sports, and therefore live sports betting.

This unprecedented scenario gave rise to several new types of investors.

- Those who started investing to replace the income they had lost after being laid off (we’ve read about plenty of these).

- Those who started investing as a substitute for gambling; and

- Those who started investing because they were bored.

Bloomberg commentator Matt Levine even coined the phrase ‘Boredom Market Hypothesis’ based on the idea that:

‘A lot of individual investors buy stocks mainly because it’s fun, and that the more fun stocks are, and the less fun everything else is, the more they’ll buy stocks. In a pandemic, when people can’t really leave their house and sports are cancelled, there is a lot less fun to be had elsewhere, so trading stocks seems relatively more fun, so people buy more stocks.’[14]

The willingness of retail investors to enter the market was so strong that they almost single handedly kept the market afloat during the initial heavy selloffs.

Research suggests during the March to May period in 2020, retail investors were net buyers of shares, to the tune of A$6.29 billion. Institutional investors were net sellers, shedding around $7.3 billion of equities over the same period[15].

The ticking time bomb

Whilst this surge in DIY market participation may well have several positive and long-lasting effects, such as increased national wealth, improved financial engagement, and an eventual increased demand for expert advice, there are likely to be several downsides too.

In the short term, many of these self-directed investors are likely to lose money.

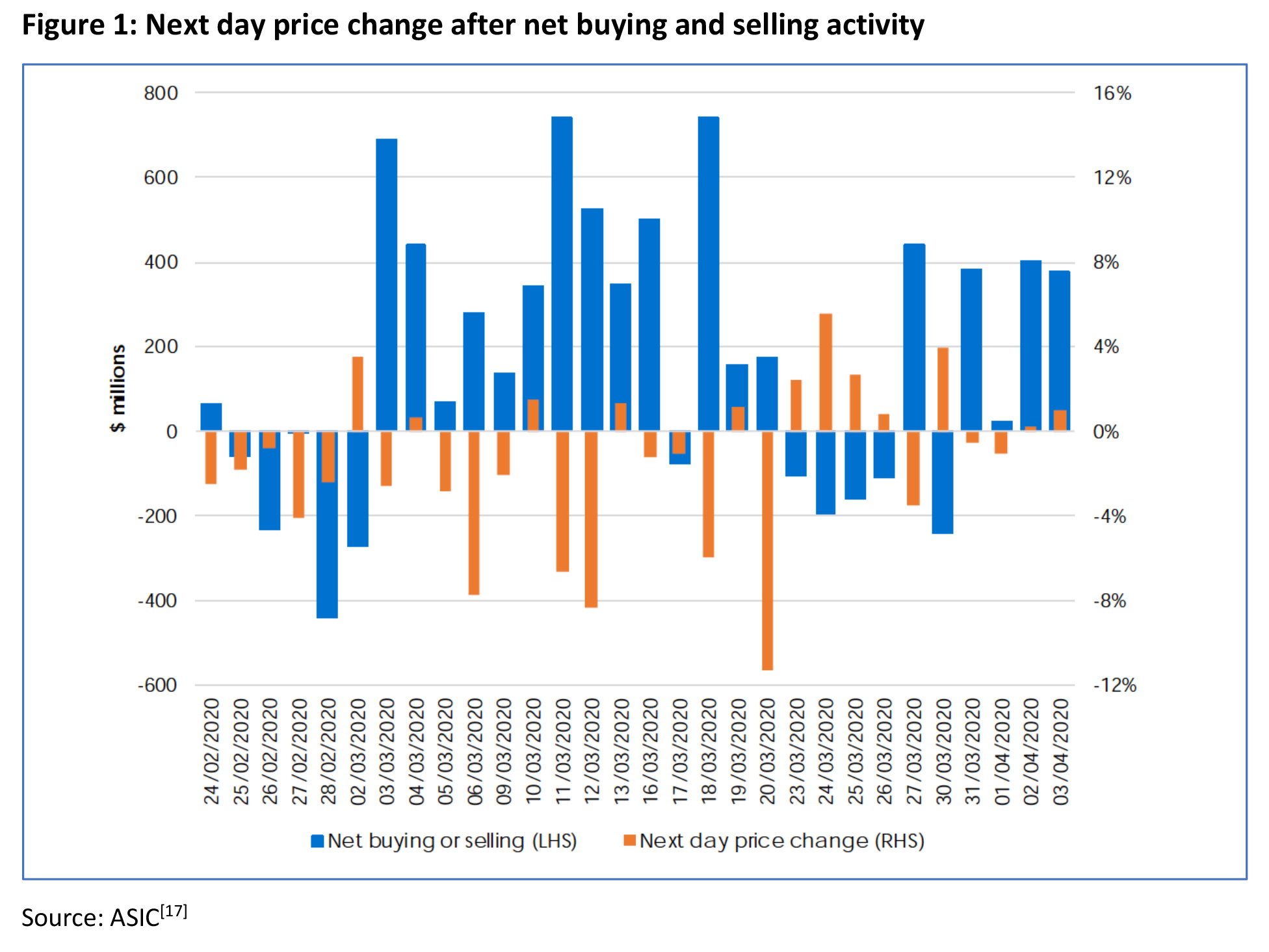

An ASIC analysis[16] of retail investor trading over the first few months of the pandemic made some alarming observations.

Terrible timing

The Pandemic saw a dramatic increase in the frequency of trading, with the average time period between trades of the same stock falling from 4.5 days pre-pandemic to just 1 day, whilst the time between trades of any stock fell from 2.5 days to 0.9 day.

Naturally this increased trade frequency amplifies the risk of getting the market timing wrong, which in many cases is exactly what played out. According to ASIC, for more than two thirds of the days on which retail investors were net buyers, their share prices declined over the next day. For more than half of the days on which retail investors were net sellers, their share prices increased over the next day.

Value investors or mug punters?

Whilst the tendency of investors to base stock purchase decisions on something other than rational financial analysis (they like the name, they use the products, the prospectus had a supermodel on the cover) is not new, the new cohort of ‘Robinhood’ stock pickers are still capable of throwing up a surprise or two, most notably in their predilection for cheap stocks (which offer more leverage and more ‘fun’). Whether it’s the Gamestop effect, or a genuine gambling mentality, the last year has given new meaning to the terms ‘buy the dip’ and ‘buy the trash’, with many investors attracted to stocks which are cheap, out of favour with institutional investors, or in some extreme cases, bankrupt[18]! Whilst in the short term many investors have ridden the wave of recovery and profited from their countercyclical buying – making them the ultimate value investors – one senses it will end in tears.

Trading in high risk and complex products

ASIC’s analysis also revealed an increased appetite amongst retail investors for high risk and more complex products, such as geared products, AREITs, and other ‘exotics’[19].

They made special mention of Contracts for Difference (CFDs), which in one week alone saw retail investors lose in over $400m in value, and more alarmingly, accrue negative balances (i.e., debts) of over $4 million.

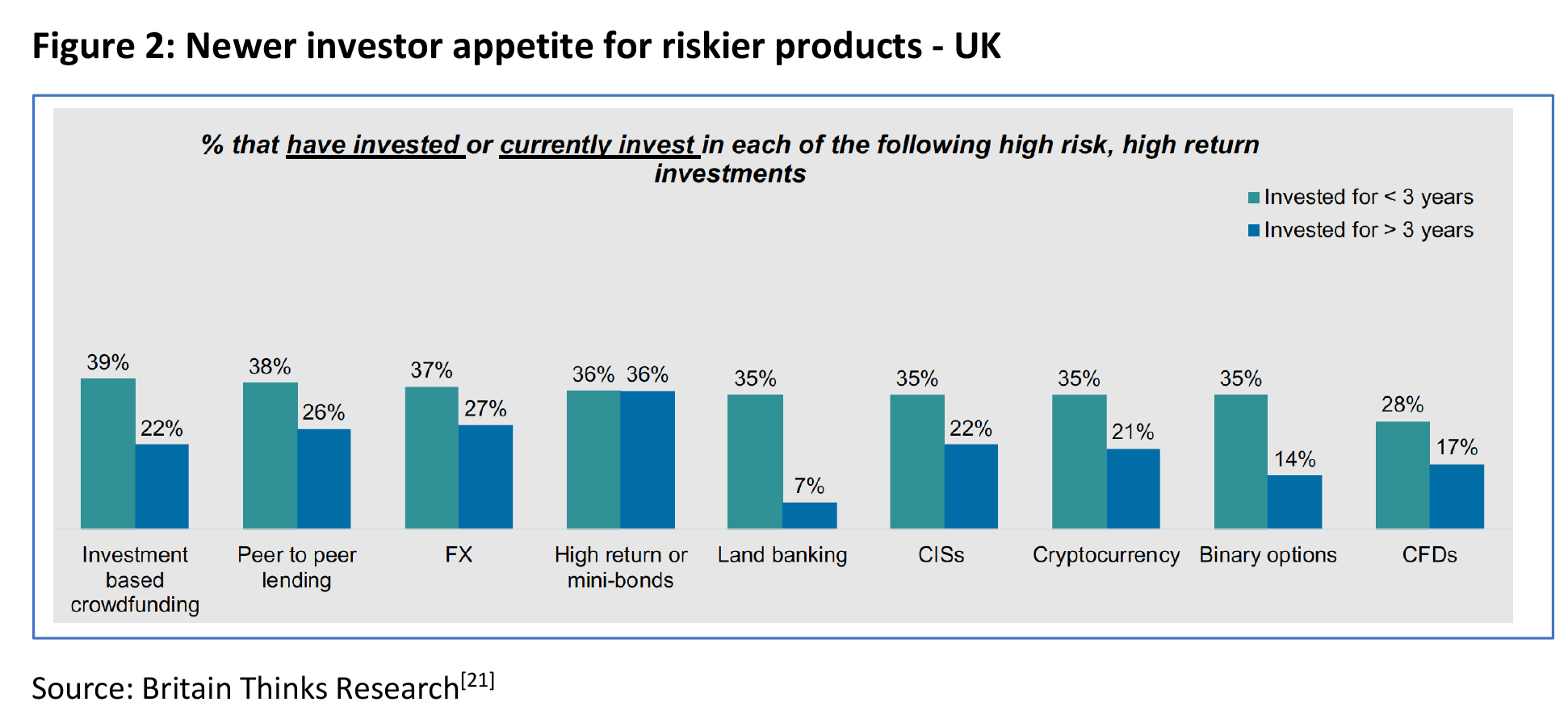

It is likely that the Australian experience mirrors that identified in UK research[20] published earlier this year, which showed self-directed investors with less than 3 years’ experience had a markedly higher risk appetite than those with over 3 years’ experience.

Not understanding tax rules

Another trap for newer investors in particular is the ATO wash through rules, designed to prevent tax loss harvesting. Investors who more actively trade – and who don’t have the benefit of expert tax advice – are potentially more likely to fall foul of this rule, potentially with significant financial implications.

Protecting consumers from themselves

The question of whether investors deserve protecting from themselves is a complex one. And notwithstanding Senator Jane Hume’s observation that “The fact that some people make poor decisions does not justify restricting the ability for ordinary Australians to participate in investment”[21], the inclination of most regulators, around the world, is to introduce new mechanisms to protect the newly empowered individual away.

The challenge faced by regulators is, of course, how?

In previous articles on this topic, we have identified the four main pillars of financial consumer protection as:

- Financial literacy

- Product Disclosure

- Product Regulation; and

- Financial Advice

With the tendency of increased disclosure to lead to information overload and confusion becoming increasingly apparent, the effectiveness of disclosure as a consumer protection mechanism is now largely discounted, leaving regulators 3 levers to pull.

Improving financial literacy seems obvious – and the benefits would be significant – but the way to achieve this successfully has eluded many experts for a long time. From online courses to ASIC sponsored MoneySmart programs in schools, nothing has shifted the dial, and overall Australian financial literacy continues to be poor. (A 2019 HILDA survey found only 25 per cent of those aged under 25 could correctly answer questions on compounding interest, diversified investing and inflation.)[22]

Perhaps the answer lies with the much-maligned finfluencers?

Notwithstanding questions about their qualifications and the quality of their ‘wisdom’, their popularity has proved beyond doubt that younger Australians are actually interested in financial topics, and willing to invest their time (and money) in improving their financial knowledge.

The difference then is ‘who’ is delivering the information (younger, relatable people), and ‘how’ they are delivering it (jargon free, short, entertaining videos and podcasts through social media).

What’s more, some of these investors even charge a subscription fee, which their followers seem more than happy to pay!

Many financial advisers have already started to realise this and are now making a welcome entry into the finfluencer world themselves.

Case Study – Financial Adviser as Influencer

Australian financial adviser Victoria Devine of Zella Wealth is the producer of the ‘She’s on the Money’ podcast, which rocketed from 17,000 members on Facebook, and less than 500 Instagram followers, to 130,000 and 70,000 respectively by the end of 2020. Her podcast offers general advice and information to a highly engaged community who actively share stories about money wins and losses and ask questions about everything from the best gas providers to building up super funds. Victoria is constantly expanding her paid offering as well, which now includes an online budgeting and cash flow masterclass[23] for $395 and other subscription-based services.

Regulatory intervention

We have seen a number of regulatory interventions designed to protect consumers from the risks associated with more complex financial products.

The new DDO regime seeks to make financial products more fit for purpose by ensuring they are designed around a well-defined and well-articulated target market. This regime doesn’t capture ordinary shares or derivatives but does capture managed funds and many other popular product categories.

Another option is to restrict access to riskier products, as Australia has done via its ‘sophisticated’ and ‘wholesale’ investor rules. These rules preclude anyone who doesn’t meet the ‘sophisticated investor’ definition (earning more than $250k per annum or holding more than $2.5m in net assets) from investing in certain types of products.

This rule was in the spotlight earlier this year when ASIC banned retail investors from accessing ‘binary options’, and media coverage suggests they have other ‘over the counter’ derivatives on their radar too[24].

The major flaw in this approach is of course that the income and asset levels are intended as a proxy for heightened financial literacy and better financial decision making, and in many cases, this is simply a false assumption.

Mandating knowledge – or advice

An approach based on actual financial knowledge was introduced in Singapore in 2012.

The Customer Knowledge Assessment (CKA)[25] attempts to judge whether an investor has the knowledge or experience to understand the risks and features of investment products such as managed funds. Knowledge or experience in this case means qualities such having a finance qualification, having sufficient work experience in a finance-related job, or having bought a similar type of product before. Individuals passing the test have largely unrestricted access to retail investments. Those that “fail” the CKA, that is, are deemed lacking suitable experience or knowledge, are required to receive financial advice before investing, and could also be subject to extra safeguards, such as lower trading limits.

Time for a new ‘Do It Together’ (DIT) advice model?

To this point the world of DIY investing has been largely dichotomous; investors have tended to be entirely independent, or entirely dependent on an expert adviser. Forces in both directions have kept it this way: the psychology of many DIY investors is that they enjoy the control, and they think they can do a better job, cheaper, than an adviser. (The negative media coverage of advisers simply reinforces their beliefs). Advisers on the other hand struggle to work with investors who want to be more ‘hands on’ into their business model, for fears they may be exposed to increased compliance risks, or simply because such clients don’t fit their business/charging model.

This is a shame as there is undoubtedly an appetite, especially amongst younger investors, for that second opinion, that mentor and sounding board. And working with an adviser will protect DIY investors from their own flawed decision-making processes.

Rather than being driven to robo-advice platforms for this more limited guidance (or accountants if they want more human intervention), perhaps DIY investors are looking for Do-It-Together (DIT) models, where financial advisers help DIY investors strike a better balance between time commitments, research and other back-office functions while allowing DIY investors to maintain control of their assets?

For many advisers this will require a rethink of their attitudes to providing scaled advice, even general advice, and how they charge for their time.

Countless studies have shown the biggest barrier to people seeking financial advice is not the lack of trust, it is the cost, and the belief that their circumstances don’t warrant the sizeable investment (time and financial) in a full financial plan.

Charging for advice on an hourly basis (ensuring the hourly rate was set at a level that was sustainable for the practice) will not only be reflecting a need in the market, but it will also make advice more affordable and transparent, which in turn will help enhance its reputation.

And after all, getting expert advice is ultimately the best consumer protection available, even for those who like a bit of DIY.

———-