Commercialising a therapeutic approach to financial advice

What are the practical implications for advisers wishing to formalise advice delivery based on coaching and financial therapy?

In an earlier article, Why are you so happy? Explaining the wellbeing effects of financial advice, we examined the ways financial advice – and the financial advice process itself – can improve the mental wellbeing of clients.

This wellbeing effect was found to be particularly strong when the client/adviser relationship extended beyond a purely financial and technical basis, into more of a coaching- style engagement.

In a follow up study exploring the commercialisation of such an approach, a majority of Australian financial advisers surveyed believed engaging their clients in this way increased the effectiveness of their advice and delivered commercial benefits for their practice[1].

In this article, we will explore the implications of such an approach across the advice value chain including business processes, skills and education, and remuneration.

The financial advice profession will only survive if it is based on deep relationships

Technological disruption continues to impact most industries, and financial services is no exception.

Consumers have access to more knowledge and more computing power than ever before, meaning that professions which rely on number crunching and/or rules-based processes are in danger of being automated (obvious examples include underwriting, credit assessments and tax returns).

As US Financial Adviser and industry observer Michael Kitces[2] put it:

“Computer algorithms can now perform accounting tasks quicker, better and cheaper than the financial planners who have traditionally done them. Rather than trying to compete with this, advisers need to alter their value proposition and transition from being knowledge workers to relationship workers, as being a gatekeeper to expert information is not good for business”.

Many elements of the financial advice value chain are open to automation, including fact finding, product comparisons, certain paraplanning processes, asset allocation and many others. Advisers that build their value proposition around these will soon find themselves threatened by the ‘rise of the machine’.

Whilst the current adoption of robo-advice sits at around 7%[3] and is largely driven by Millennials, Investment Trends research has found there is healthy appetite across all age groups. More than a third (36%) of online share investors aged 65 and above say they would consider using robo-advice, while 40% of those in the 55 to 64 age group are also keen[4].

What robo-advice platforms cannot provide – and where a sustainable future for financial advice lies – is deep, trusting, emotional connections that go beyond numbers.

Deep, trusting relationships deliver better outcomes for clients and advisers

The extent to which trust is important in the client/adviser relationship was quantified in the Zurich/AFA/Beddoes Trusted Adviser study[5], which found that increased client trust was associated with multiple commercial improvements including:

- higher referral rates

- more client sharing on information enabled more effective advice

- improved client satisfaction and retention

- a higher willingness to pay advice fees, on time and without question.

Deep trusting client relationships aren’t about the numbers

Advisers are increasingly called upon to provide non-financial counselling and support as their clients live out the human drama of day-to-day living.

In fact, research has found that, on average, almost half the time advisers spend with clients is discussing non-financial personal matters, including health, marital problems, legal issues, career, addictions, and even intra-family conflicts[6].

Most advisers surveyed believe their willingness to discuss personal matters allows them to perform their role more effectively and has been commercially positive.

Unsurprisingly, the same research found that most advisers expect their role as non-financial coaches and counsellors (in other words, financial therapists) to increase in importance in the future.

A therapeutic perspective on advice

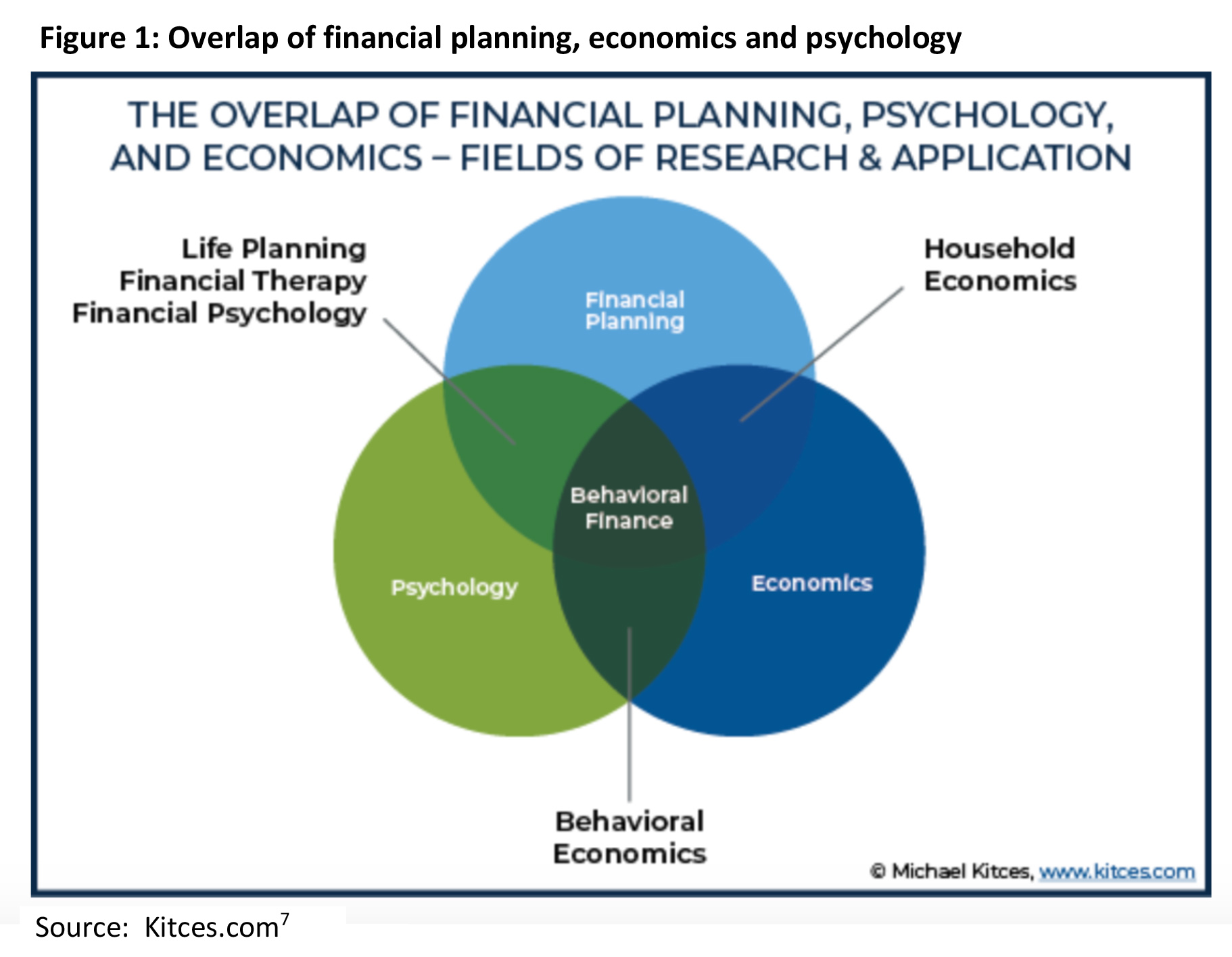

Sitting at the intersection of financial planning and psychology (Figure 1), the philosophy underpinning Financial Therapy rests on the idea that money has a deep, human meaning.

This meaning, often shaped in childhood, encompasses those entrenched behaviours, beliefs and attitudes towards money, many of which are unconscious, and some of which can become major obstacles to individuals mastering money and achieving their dreams in adulthood.

Overcoming these obstacles is therefore more likely to involve psychology than spreadsheets and embracing it to its full – commercially optimal – potential requires a rethink of the skills needed and the processes within which advice is delivered.

Some advisers may need to acquire new skills, or sharpen existing ones

Taking a more therapeutic approach to advice is not about becoming a trained psychologist, it is about recognising the therapeutic value in the advice you provide, the processes via which advice is provided, and the relationships you build. The requisite skills are therefore more based around relationship building, such as communication, and emotional intelligence, as well as understanding the cognitive biases inherent in client decision main processes.

Emotional intelligence

Daniel Goleman[8], the ‘father’ of emotional intelligence, identifies four components of EQ:

- self-awareness: An introspective understanding of personal strengths and weaknesses regarding interpersonal relationships;

- social awareness: An ability to appropriately adapt to the demands imposed across various social settings;

- self-management: An ability to control emotions that might otherwise negatively affect interpersonal relationships, that is, impulse control; and

- relationship management: The ability to create rapport, mutually rewarding emotional bonds, teamwork, and collaboration.

Successful advisers have elite communication skills

There is a strong relationship between trust and commitment, and communication is the glue that bonds the adviser-client relationship[9].

For providers of any professional service, a reasonable level of communications competency should be considered a hygiene factor. But there are unique aspects of the financial adviser/client relationship that require more refined communication skills. Money is a taboo topic for many[10], not easily discussed, even among family members. Moreover, money represents security, self-esteem, ego, and other significant psychological needs, often manifested in secrecy and denial, requiring a special communications approach.

Effective coaches/financial therapists are masters of:

- editing their verbal and nonverbal messages (so there is fidelity between the message intended and the message the client receives). Recapping and paraphrasing can be helpful here

- empathic listening – getting a sense of the feelings that the speaker is expressing and staying mindful of the emotional content being delivered as well as the literal meaning of the words. Staying patient and showing acceptance, not necessarily agreement, is important here

- speaking plainly and avoiding jargon. This doesn’t necessarily come naturally to experts in a particular field

- framing language and messages to be more effective (for example framing risk as a frequency – say 1 in 10 – has been shown to be more powerful than framing it as 10 percent[11]). Framing life insurance around the sum insured rather than the annual premium, is more likely to elicit the perception of it being an investment rather than a cost.

We all take shortcuts to avoid mental overload

Central to establishing a deep connection with clients is understanding the way they think and make decisions.

Scientists estimate the human body sends 11 million bits per second to the brain for processing, yet the conscious mind seems to be able to process only 50 bits per second[12].

The only way we can cope with this gap – and prevent our brains crashing like an overloaded website – is to use mental short cuts (heuristics) to make decisions amongst this deluge of data. These shortcuts look for patterns, make associations and quick inferences based on the limited information it can digest. In effect our brains ‘connect the dots’.

But, sometimes, in connecting the dots, we get it wrong, having a huge impact on the way we understand, interact with, and receive information and advice.

Called cognitive biases, these shortcuts can also lead us to make poor decisions, especially those that relate to finances.

The ‘availability’ bias[13] sees us place more importance on the most recent information we have received, which is why, for example, people seek life insurance after the death or illness of someone they know. The actual risk of them actually suffering that event hasn’t changed, it’s just that they are more aware of it.

In a situation where clients don’t have any ‘available’ experience or data to reinforce their need for life insurance, advisers can draw on news and examples (e.g. claims stories) that remind people of the risks and their consequences.

Loss aversion[14] is a bias which explains why our fear of losing is psychologically twice as powerful as the pleasure of gaining the same amount. Positioning life insurance as covering school fees is therefore less powerful than positioning it as preventing your client’s children losing their place at school.

Another shortcut at play in this example is overconfidence[15] about what the future will look like, including future income and the state of one’s health. Overconfidence about health has long been a barrier to consumers recognising the need for, and value of, life insurance, and data and tools which make it easier for people to understand the real risks can be useful in such circumstances.

Other biases for advisers to be aware of include:

- present bias

- projection bias

- anchoring

- regret

- over-extrapolation

- mental accounting and narrow framing

- the need for social proof

- maintenance of the status quo

- stereotyping.

Rethinking the advice process itself

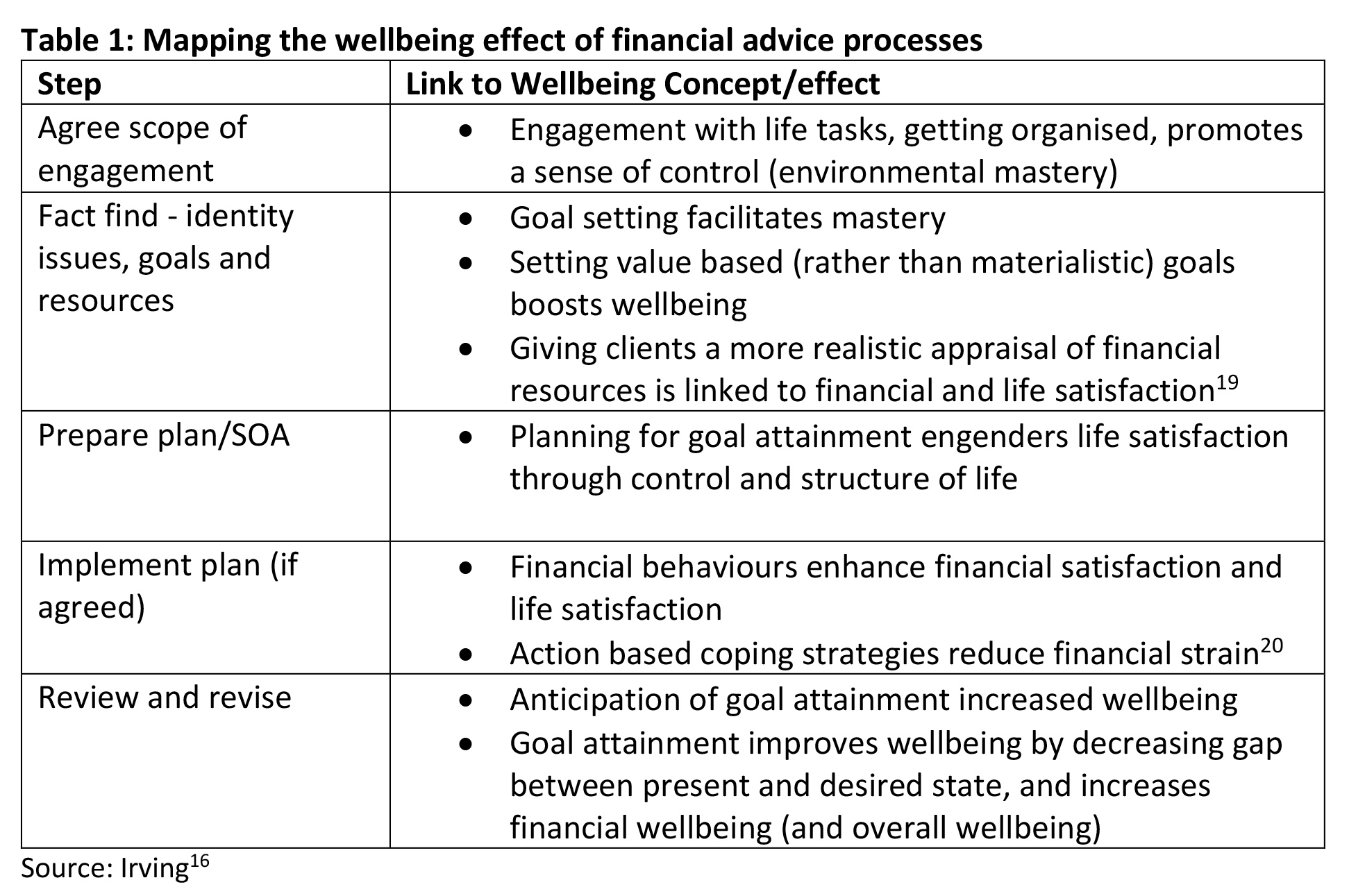

In our earlier article we explained how clients derived therapeutic value not just from the financial advice they received, but also from the advice process itself. Table 1 below identifies the wellbeing effect at each stage of the process.

With this in mind, advisers seeking to model their client relationships more holistically may wish to reflect on the importance of each stage, and whether their business processes are designed to optimise the value of each stage to the client (and in turn strengthening the client relationship).

Additional Considerations for advisers

- Asking more non-financial questions at the fact-finding stage, with a view to uncovering any underlying behaviours, habits or negative attitudes towards money, and the historical and familial context for such attitudes.

- Asking questions designed to uncover their life values and then designing financial goals accordingly

- For many clients, the first meetings will be cathartic, an opportunity for them to get things off their chest; rethink the length of your consultations, so clients have more time to talk about what they want to talk about.

- Having the client formally commit to goals and then building a contact schedule which allows for regular checking progress against those goals

- Research[17] has shown that clients who write down their goals are more committed to them and more likely to follow through on your advice. Rather than relying on pro-forma, pre-printed documentation, consider having your client write them in their own handwriting, including specific deadlines and measures of success

- Ensure the design and content of your Statement of Advice and supporting documentation maximises their potential wellbeing effect

- Ensure all your staff are aligned to the way you do business, to increase their buy-in and to ensure a consistent client experience

Rethinking adviser remuneration

Financial advice clients who have a more holistic, trusting, relationship with their adviser, are more willing to pay fees, a fact which is especially pertinent considering the ongoing negative media coverage of adviser remuneration.

As encouraging as this is, advisers seeking to more formally implement a therapeutic approach to advice still need to consider how to charge for their services.

The most equitable way for advisers to be rewarded is where there is a direct and transparent relationship between the work done and the fees charged. Services where there this relationship is obvious, and in which the client sees value, include:

- the initial stages of fact finding, advice preparation and execution

- the annual review process

- insurance claims, and

- any intra-review period advice

Advisers adopting a more holistic /therapeutic approach therefore need to consider:

- How much time they are now spending at each stage?

- How they improve the transparency around those stages?

- When is the appropriate time to charge for these services?

This could well see advisers seeing less clients, but charging more, thus generating more in overall fee revenue.

In a life insurance context this could also mean that advisers charge more for the initial advice and to manage claims, and less for those periods in between where work is much less.

Conclusion

There are well proven links between financial advice and mental wellbeing. And even though most advisers don’t formally acknowledge it or label it, it is clear that most advisers are already providing a form of therapeutic support to their clients that go beyond mere numbers.

Whilst for many advisers, implementing financial therapy/coaching approach simply means formalising and enhancing an approach they are already taking, there are several areas advisers need to address to ensure financial therapy is delivered to its full potential, including communication, business processes, education, and remuneration.

Successfully addressing these elements of the advice value chain in order to deliver therapeutic/coaching style advice will lead to proven commercial benefits and will help advisers quell the growing threat posed by robo-advice.

![]()

———-