Why are you so happy? The wellbeing effects of financial advice and what they mean for Advisers

By mapping wellbeing outcomes to typical steps in the financial planning process, advisers will be better equipped to review their processes and opportunities.

Fact: People who have received financial advice are happier than those who haven’t.

You wouldn’t know it – given the media’s laser-like focus on the negative – but the financial advice profession is a veritable happiness machine.

That’s right, those people who have received financial advice are much happier than those who haven’t.

According to Fidelity’s value of advice survey[1], 50% of Australians receiving financial advice reported their mental health had improved as a result of advice, while 38% reported their family life was better. A similar study[2] by IOOF revealed those who receive ongoing financial planning advice experienced 13% greater levels of overall personal happiness, a 21% increase in peace of mind, and 19% less likelihood to have arguments with loved ones.

So why would that be? Is it simply because financial clients accumulate more money?

There are undoubted financial benefits of advice. Coredata/AFA research[3] proved beyond doubt that advised clients generally pay less tax, have less bad debt, generate greater lifetime income and earn greater return on their investments.

But, as tempting as it is to assume a linear relationship -financial advice equals improved material wealth equals increased happiness – the positive correlation between money and happiness – to the extent it indeed exists – is too simplistic to be of value.

To truly understand the relationship between financial advice and mental wellbeing requires us to look deeper into the psychological drivers of happiness. When we do this, it becomes clear that the value clients are deriving from advice are often quite different to the value the advisers believe they are delivering. And this discovery should lead us to reconsider – and redefine – the entire meaning of financial advice.

The link between money and happiness

The relationship between our finances and our happiness has long been, and remains, a topic of intense debate.

At one end of the scale, the link between financial stress – i.e., lack of money – and psychological problems – is well established. According to the Australian Psychological Society[4], personal financial issues are the number one most prevalent cause of stress throughout our community. International research[5] also shows that financial difficulties create psychological distress for individuals, primarily due to the way they diminish personal control and self-esteem. In a recent review, the prevalence of anxiety, depression and reduced psychological well-being was found to increase with increasing financial stress, and that living under financial strain is associated with feelings of inferiority, low worth, self-doubt, and deprivation.

Coredata, in research commissioned by Financial Mindfulness[6] also revealed how financial stress leads to anti-social behaviour, relationship conflict and breakdown, isolation, sleep loss and symptoms of depression.

Whilst such a linkage may seem self-evident, it is not in itself proof that the correlation between income and wealth and ‘happiness’ is always a positive, linear one.

Whilst economic growth[7] has indeed been proved to be associated with increasing subjective well-being, there is a substantial body of work[8][9] suggesting that wealth increases life satisfaction only so far (up to a base level of income) after which further increases in wealth have no impact.

Meaning that the value of advice is clearly about so much more than accumulating more money. But what exactly?

Perhaps the clue lies in earlier research[10] by Zurich and the AFA, which found the most important attribute clients were seeking in a financial adviser was interpersonal skills.

This suggests the benefits derived by clients from financial advice are more psychological than financial.

Advice outcomes makes us happy

According to Carol Ryff’s six factor model[11], psychological well-being consists of autonomy, environmental mastery, personal growth, positive relations with others, purpose in life, and self-acceptance.

Two of these drivers in particular – environmental mastery and positive relationships – have strong alignment with the process and outcomes of financial advice.

Financial advice increases environmental mastery

Environmental mastery describes a person’s ability to find or create a surrounding environment that suits their personal needs and capacities. High mastery individuals are adept at managing their environments and everyday affairs, controlling a complex array of external activities, and making effective use of surrounding opportunities. This sense of control or mastery over one’s life is linked to improved mental health[12][13], including reduced anxiety and depression, increase resilience and enhanced life satisfaction and well-being.

The extent to which advised clients feel more in control – of their finances and their lives – is a common finding across many financial advice research studies. Fidelity[14], for example reported that 86.2% of advice clients believe advice has given them greater control over their finances.

Similarly, a QUT survey[15] found, across multiple surveys, that the majority of clients viewed financial advice as making a positive contribution to a range of psychological well-being factors, including sense of security, peace of mind and a sense of control.

This wellbeing uplift – from mastery and control – applies to clients of all ages, although the scope of what needs to be controlled differs by generation. An ING/Rice Warner[16] study found that for millennials, their financial advice priority – what they needed help to achieve mastery of – was budgeting and cash flow management, whereas Baby Boomers prioritise the need to be in control of their retirement plans.

Financial advice builds positive relationships

The very bedrock of financial advice is trust-based relationships. As with many professional services relationships, most clients don’t have the same expertise as their adviser, nor do they have any easy way by which to judge or compare the quality of the advice they are receiving (although this becomes more possible over time).

Discussing personal financial assets, personal life goals, and articulating plans for achieving those goals also relies on trust, candour, and a client’s willingness to be open and potentially vulnerable.

Clients who ordinarily wouldn’t dream of seeking out a counsellor or therapist will find themselves talking to their financial adviser about incredibly personal and emotionally charge topics such as a pending divorce, the aftermath of losing a loved one, caring for a special needs family member, or leaving a bequest. Thus, financial advisers, whether they planned for it or not, may become personal coaches and counsellors for their clients, providing therapeutic value, perhaps without even realising it.

The second relationship dimension of advice is the impact advice can have on the client’s relationships with others, especially their family.

Almost half (48.0%) of Australians say financial issues have affected how they get along with family and friends[17]. And yet, as already mentioned earlier, surveyed advice clients reported their family life was better, and they were less likely to have arguments with loved ones. Whether it be by reducing the anxiety related to financial issues, implementing behavioural change to reduce debt, or by simply opening lines of communication between client and spouse so they can talk about money, financial advice can make or break a relationship.

Advice processes also drive wellbeing

The advice outcomes, and client/adviser dynamic, are not the sole drivers of wellbeing in an advice relationship. Aspects of the financial planning process itself can also improve mental wellbeing.

Setting goals makes us happy

Goals are central to a sense of psychological well-being, and the setting and achieving of goals are at the heart of financial advice. Whether it be building a dream home, retiring early, leaving a bequest, or educating ones’ children, goals are an expression of our future, and help set the purpose for life’s journey as well as its direction. Without goals our lives lack structure and meaning.

Research[18] suggests that participating in activities aimed at developing goal setting and planning skills can increase subjective well-being and personal growth over time (in particular, life satisfaction), either by bringing about changes in self-perception and/or self-confidence, or by positive changes in one’s circumstances. Planning for goals is also associated with a greater sense of control, and fulfilling plans underpins competence and capability.

The psychological importance of the regular review

While successfully achieving goals has a distinctly positive psychological effect, a positive mood state is also associated with the mere anticipation of future outcomes. In other words, just the perception of progress towards goals can provide a positive psychological boost, ahead of those goals being reached[19]. This suggests the regular client review process has a vital psychological benefit. Financial advisers who remind clients of where they set off from, what they have achieved, and where they are headed on a regular basis are likely to reinforce their clients’ sense of environmental mastery.

Financial advice as therapy?

Several studies support the idea that the main benefits derived from financial advice are psychological, rather than financial.

The Trusted Adviser study[20] conducted by The Beddoes Institute for Zurich and the AFA found that interpersonal attributes, rather than technical knowledge and skills, were the most important criteria when choosing an adviser.

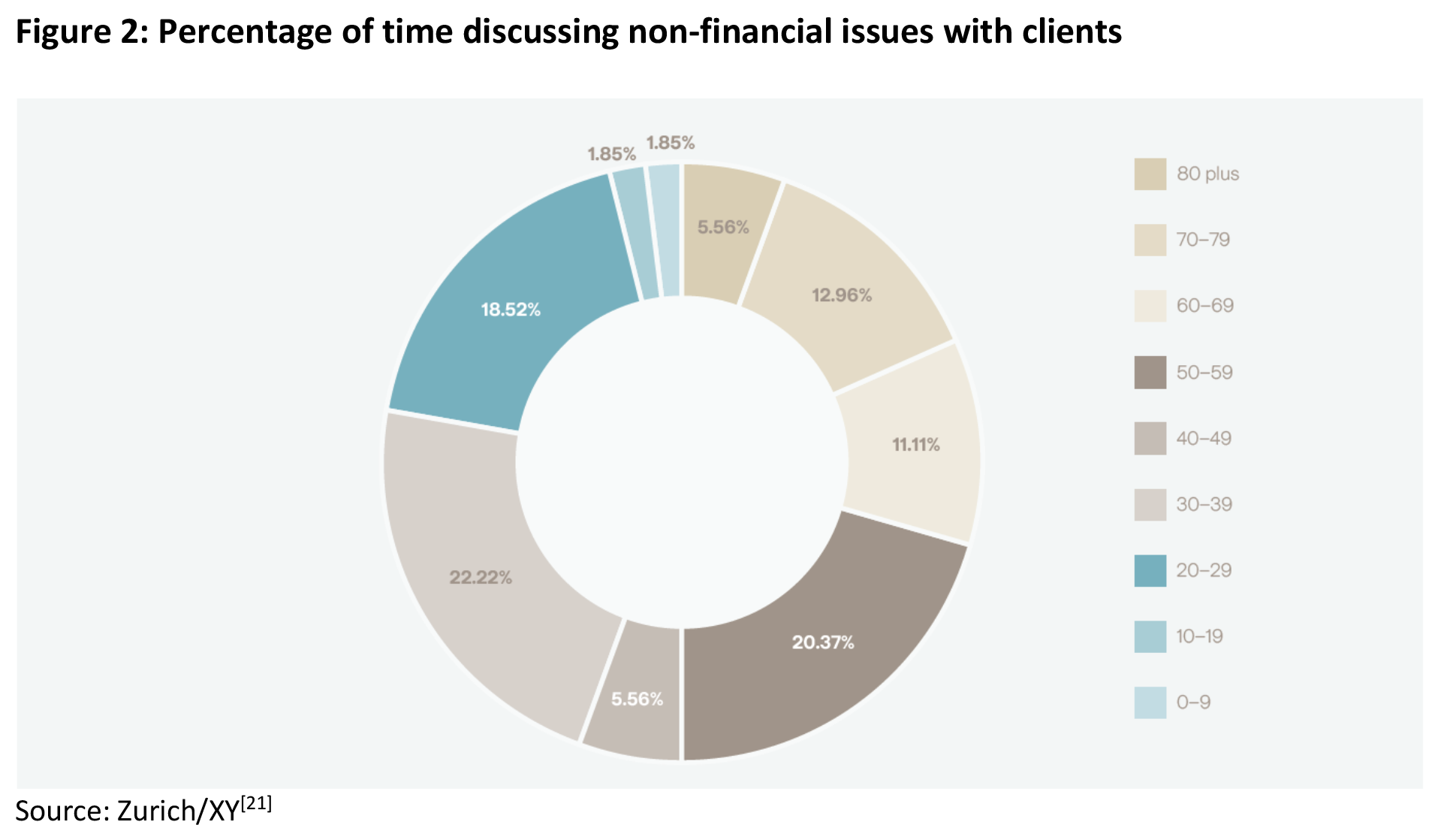

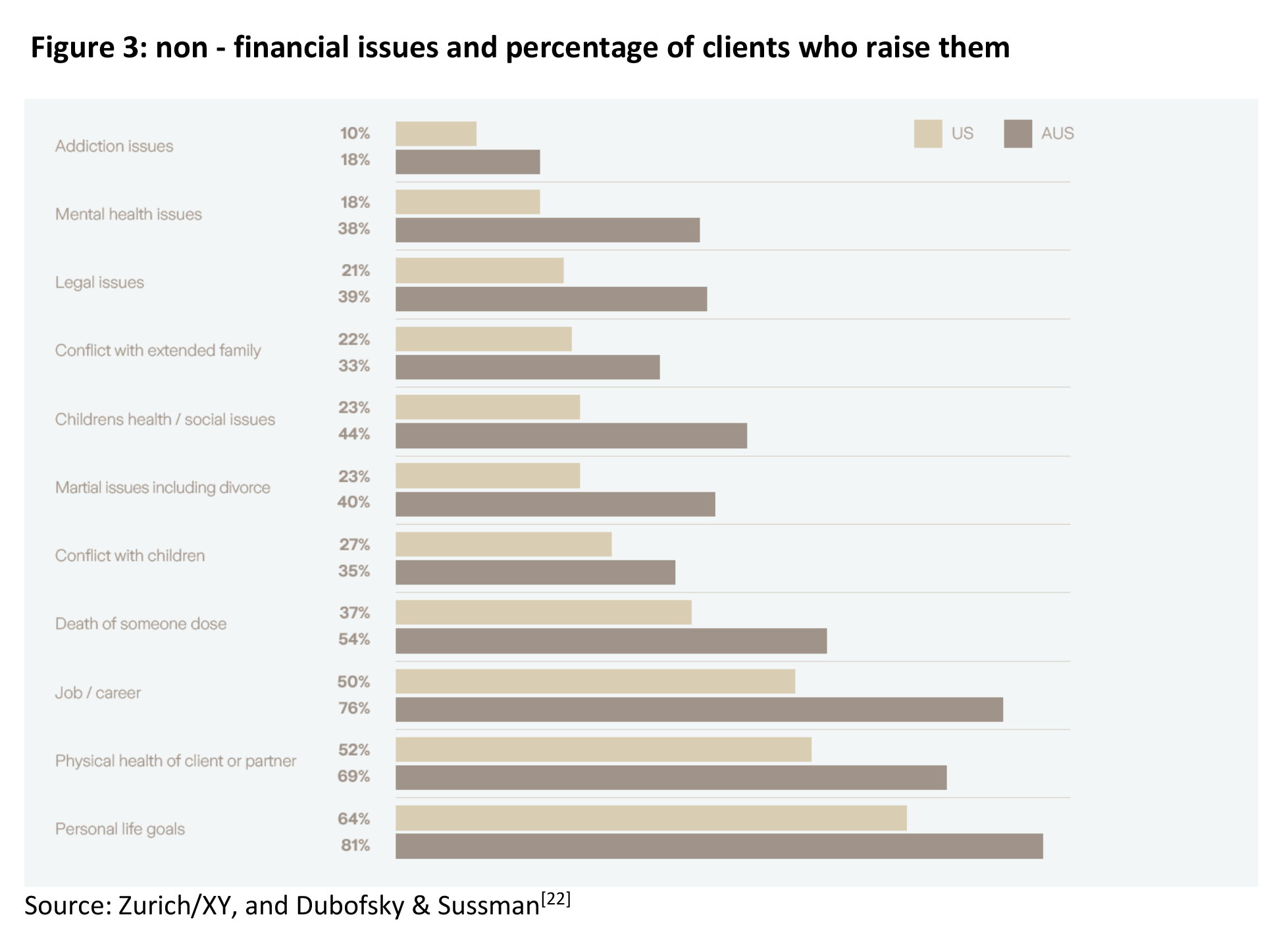

More telling though, were the findings of an XY Adviser/Zurich[21] study of the conversations advisers were having with their clients, and adviser perceptions of the non-financial impact they have made on their clients’ lives.

The headline finding of this study was that on average, Australian advisers spend 45% of their time with their clients talking about non-financial personal issues.

Advisers as counsellors and mentors

The survey also revealed adviser/client engagement to be deeply and emotionally impactful:

- 83% said a client had become very emotional during a planning session

- 72% said their client had confided a secret in them, and them alone

- 50% had served as a mediator between their client and other family members.

These personal, non-financial conversations have a positive impact on clients

Advisers were asked about the impact these personal, non-financial, conversations had on their clients and their business.

- Almost half (47%) agreed there was more effective communication between husband and wife, parents and children, or others who may be significant in the clients’ lives

- 47% felt their client was living a life closer to their core values, and enjoying what is most important to them

They are good for business too

- 52% felt their ability to do a good job at financial planning was enhanced or improved; and

- 39% agreed their business had increased as a result

Unsurprisingly, 94% of advisers surveyed said their role as coach and counsellor was increasing in importance. Leading us to pose the question:

Is financial advice therapy, and are advisers therapists?

Advice as therapy

It is clear that financial advisers provide more than just financial expertise.

Whilst financial advisers are not expected to be fully trained mental health experts, or psychological therapists, evidence shows both the advice relationship, and the advice process itself, provide many therapeutic benefits. For most clients, the adviser is a mentor, counsellor, and mediator, supporting them as they live out the human drama of day-to-day life.

Furthermore, most Australian advisers themselves recognise the importance of their role as counsellors and mentors, expect it to increase in importance, and believe it has commercial benefits.

The US financial planning industry is more advanced in acknowledging, and formally recognising, this intersection between financial planning and life coaching. Variously described as Life Planning, Financial Therapy and Financial Psychology,

Financial therapy is a new and growing field, defined by the eight-year-old Financial Therapy Association[23] as combining finance management techniques with attention to the cognitive and emotional challenges associated with money. Practitioners typically come in with a primary background in either psychology or finance and learn the other specialty to help their clients address their money issues from both the practical and emotional sides of things.

In the US, both Financial Therapy and Life Planning have a degree of formal recognition, by way of member collectives and the availability of formal training and accreditation. Whilst no equivalents currently exist in Australia, the evidence suggests that many local advisers are already providing the type of support covered by these new labels.

However, the lack of dedicated educational offerings in these areas means Australian advisers are largely ‘winging it’, doing an admirable job of dealing with emotionally complex clients without necessarily being fully equipped.

It’s time to redefine and reposition financial advice

Considering the above, perhaps now is the time to consider both formally recognising the therapeutic nature of financial advice and making available appropriate training and tools to ensure a degree of consistency in skill levels throughout the advice profession. This in turn will give advisers more confidence in, and appreciation of, the true nature of their advice.

Of course, such a re-evaluation of the role of advice – and advisers – would not be without significant implications across many elements of the advice value chain.

Some of the areas impacted would include:

- education and training

- ethical considerations

- the scope of the advice process including fact finding and SOA’s

- ongoing professional development

- client success metrics

- the marketing of advice

- service packages

- job design and role descriptions

- remuneration structures

- fee schedules.

Whilst these implications are undoubtedly significant, they do not represent insurmountable barriers to the repositioning of advice. And reposition we should, given it is the clients, not advisers, who determine the true impact advice, and the advice process, makes on their lives.

![]()

———-