Bonds are back – What is driving the demand for Fixed Income ETFs?

What is driving the demand for Fixed Income ETFs?

The ASX Exchange Traded Fund (ETF) Market Cap hit a new record high surpassing $100bn earlier this year, exhibiting huge growth over the last 12 months of approximately 80%. Within this universe there have seen strong demand for Australian Fixed Income ETFs as investors look to position portfolios more defensively over the coming months.

Fixed income is often viewed as the ‘not so glamorous’ sibling in the family of asset classes. But fixed income is the cornerstone of a well-diversified portfolio which can play an important role in assisting with the preservation of capital and the generation of more stable distribution streams in an environment of volatile and potentially poor share market returns. So, it makes sense to understand how fixed income works.

The building blocks for defensive portfolios

Due to their simplicity and transparency, fixed income ETFs have been the tool of choice for portfolio rebalancing and risk management at the onset of COVID-19 assisting investors to navigate periods of low liquidity and high volatility.

Why consider fixed income ETFs and the choices for investors

There are a multitude of reasons why investors are increasing exposure to fixed income ETFs. Firstly, for strategic asset allocation purposes, fixed income ETFs can serve as a core component of a fixed income allocation providing attractive income and diversification benefits to investment portfolios. In addition, when it comes to tactical asset allocation, fixed income ETFs can play the role of a satellite exposure that can also be blended with traditional fixed interest strategies to produce a more balanced set of investment outcomes for investors.

An emerging trend is the use of fixed income ETFs being utilised as a liquidity management tool within a portfolio, complementing cash and therefore allowing an investor to vary the duration exposure, credit exposure and income levels in portfolios.

Access and examples of fixed income ETFs

Large denominations of up to $500,000 for some bonds create hurdles for retail investors seeking direct exposure to bond investments. Fixed income ETFs overcome these hurdles by allowing investors the opportunity to implement their ideas quickly and efficiently whilst also providing access to liquidity. Below are examples of 3 fixed income ETFs investing in 3 different asset classes, offering a range of different maturity time horizons and with that a differing running yield and yield to maturity.

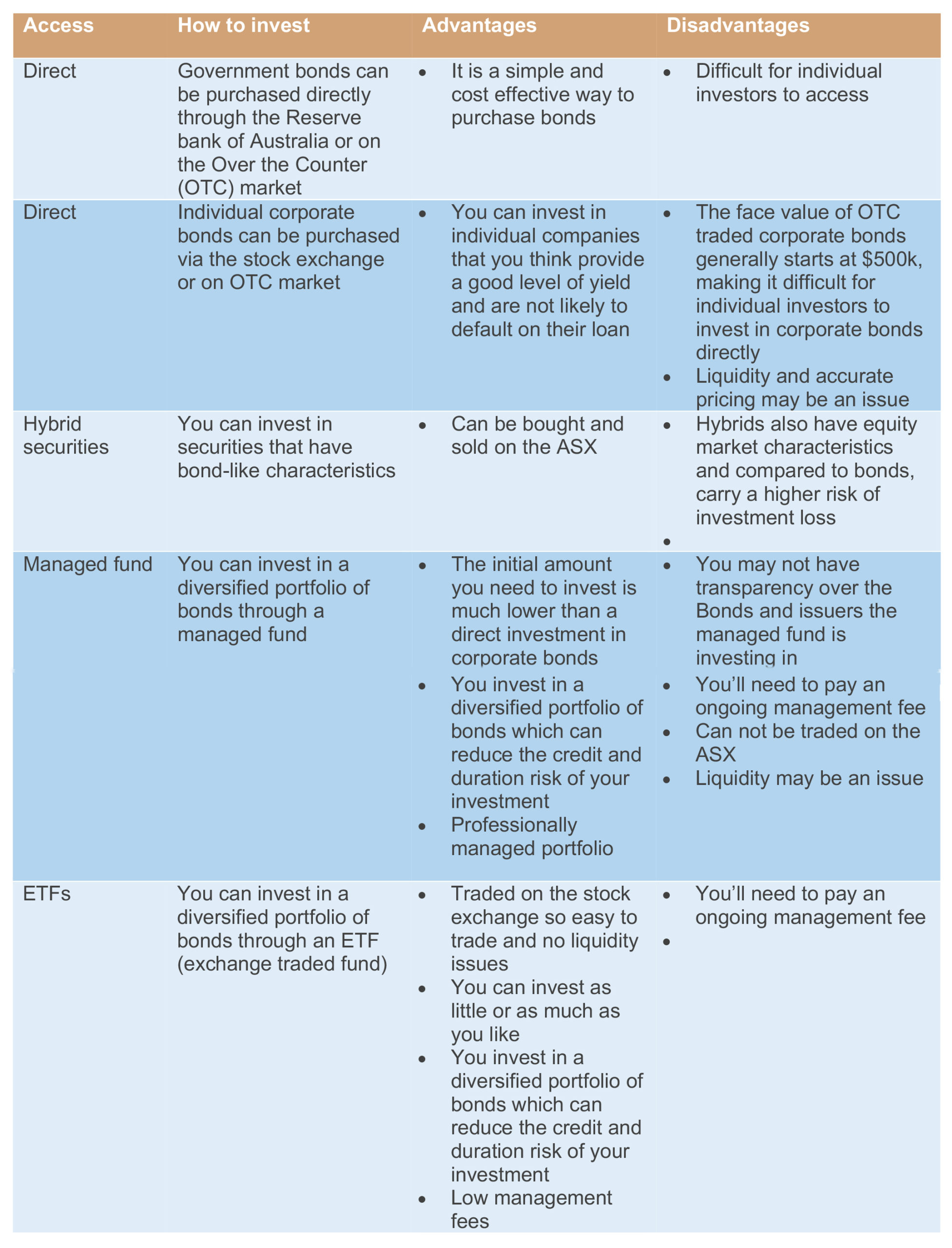

How can you invest in bonds?

There are a number of ways you can invest in bonds.

It’s important for investors to understand some of the main differences between fixed income ETFs in order to ensure the investment they are considering meets their unique financial goals, risk tolerance and investment horizon. Here are some examples we have mentioned in this article.

A Corporate Bond

This bond is a type of debt security and issued by a company in order to raise capital. This means the company gains the capital it needs, and the investor is paid a pre-established number of interest payments at a fixed or variable rate.

The bond relies on the ability of the company to repay and consideration of future revenues and profitability needs to be considered,

A Government Bond

This bond is a debt security issued by a government in order to help support government spending and obligations. Government bonds generally pay a periodic interest payment over the life of the bond. When the bond expires it usually repays the initial investment or principal.

These bonds are generally considered to lower risk but may offer a lower interest rate.

A Semi-Government Bond

This bond is similar to a government bond however they are issued by the various state and territory governments instead. These bonds pay different rates of regular interest and have different maturities. These bonds carry different credit ratings from the issuers.

5-point checklist when reviewing fixed income ETFs

- Investor time horizon: what is the investors time horizon and how can this be matched to the running yield and duration of the available fixed income ETFs

- Investor risk profile: what is the investors risk profile and what bond ETFs are available in the market to best align with the level of risk they are willing to take.

- Options available to the investors: what options available on both your approved product and services lists, have these options been rated by a rating house.

- Liquidity: what are the liquidity levels of the proposed solution? How often is the portfolio rebalanced and how regularly is income paid to meet the client’s cash flow requirements.

- Exposures: what are the underlying exposures within the portfolio, are they government, semi – government, corporate bonds, what are the ratings of the underlying exposures.

Risks to consider

As with any investment there are a number of risks to consider when investing in bonds. We’ve provided a summary of the key risks below.

Credit risk

This is the risk that the bond issuer defaults and can no longer make coupon payments or return capital at maturity.

You can minimise the credit risk of your bond portfolio by buying bonds from issuers with higher credit ratings. For example, Australian government bonds carry virtually no credit risk. You can also reduce credit risk by buying bonds from a range of different issuers, this diversifies your risk amongst several companies or institutions, and/or buying bonds with shorter maturity dates.

Interest rate risk

Coupon rates are based on underlying interest rates, the term of the bond and the credit risk of the issuer. When interest rates go up, bond prices go down as newer bonds are likely to be issued with higher coupons so are more attractive to investors. Conversely, when interest rates go down, existing bond prices go up. Interest rate risk is sometimes also referred to as ‘duration risk’.

You can manage the interest rate or duration risk in your bond portfolio by buying a range of bonds over time and with different time to maturities.

Liquidity risk

Your ability to buy and sell your bonds will depend on how liquid they are. Government bonds are very liquid whereas bonds with lower credit ratings and small issuances are likely to be less liquid.

Pricing risk

There is no central pricing source for bonds, which can make it difficult to know the ‘true value’ of your bond.

Inflation risk

Inflation impacts the purchasing power of your investment. If inflation is running higher than the coupon rate, the value of your investment will be worth less in terms of purchasing power at the end of the term.

Investor strategy case study – Reduce portfolio volatility

Situation: Josh and Ella Simpson have a self-managed super fund and are concerned about equity market volatility over the next 12 months.

Solution: The Simpsons diversify their portfolio into bonds by purchasing an equal amount of each of the Russell Investments Australian Bond ETFs. This was an alternative to cash given their desire to maintain an element of capital growth and diversification.

Investor strategy case study – Simple access

Situation: Louise Smith is a client of a private wealth firm which has been able to get her access to hybrids and bonds by single issuers at relatively high minimum investments. She’d like to diversify into further securities with bond characteristics but does not know how to access them. Louise does not want to purchase a bond managed fund.

Solution: Louise allocates some of her investment to the Russell Investments Australian Select Corporate Bond ETF as a core holding. This gives her access to the 4 major banks through a single trade on the ASX at a low minimum investment. She maintains her hybrid investments as satellites

Examples are for illustrative purposes only and should not be relied upon for the purposes of making an investment decision.

Market outlook for rates and inflation

The key thematic that has played through markets over the last few months has been inflation, and the argument over whether the recent rise is temporary or not.

One of the other questions that many market participants are grappling with is the rise in government debt over the last twelve months and looking to understand if this is sustainable over the medium-term, and what might be the implications for fixed income investors?

Inflation

Starting with the outlook for inflation and future Reserve Bank of Australia (RBA) policy. It is expected that the global spike in inflation is transitory, driven by base effects (i.e. very weak inflation last year leading to higher inflation this year) and some supply chain bottlenecks.

We are starting to see some of the products that saw significant price rises earlier in the year now reducing. An example of where there has been this pull back in prices is the price of lumber and wood chip prices.

In Australia, we are due to get the inflation reading for Q2 2021 in the coming weeks which will show a significant jump for the reasons mentioned above.

There have been a growing number of anecdotes about wage increases, both domestically and internationally. However, it’s not expected that this will lead to broad-based wage pressures over the next twelve months.

Despite the very strong improvement in the labour market in Australia, there is still some spare capacity to be absorbed. Without getting into too much economic jargon, for broad-based wage pressures it could be expected that the unemployment rate has to be in the low 4% range. The current estimate of the natural rate of unemployment.

Given the unemployment rate is currently at 5.1%, there is still some way to go before reaching that level. There is also the re-opening of the borders sometime next year, which will add to the capacity of the domestic labour market as foreign workers return to Australia.

Impact on rates

What does all this mean for the RBA? The RBA are possibly unlikely to raise the cash rates until the second half of 2023. The RBA are very focused on providing support to the labour market and would like to see wage growth sustainably above 3% – which would be consistent with inflation sustainably within their target range of 2-3%.

This hurdle is going to be difficult to achieve before the end of 2022. However, expect that the RBA will continue to taper their bond purchase program through next year.

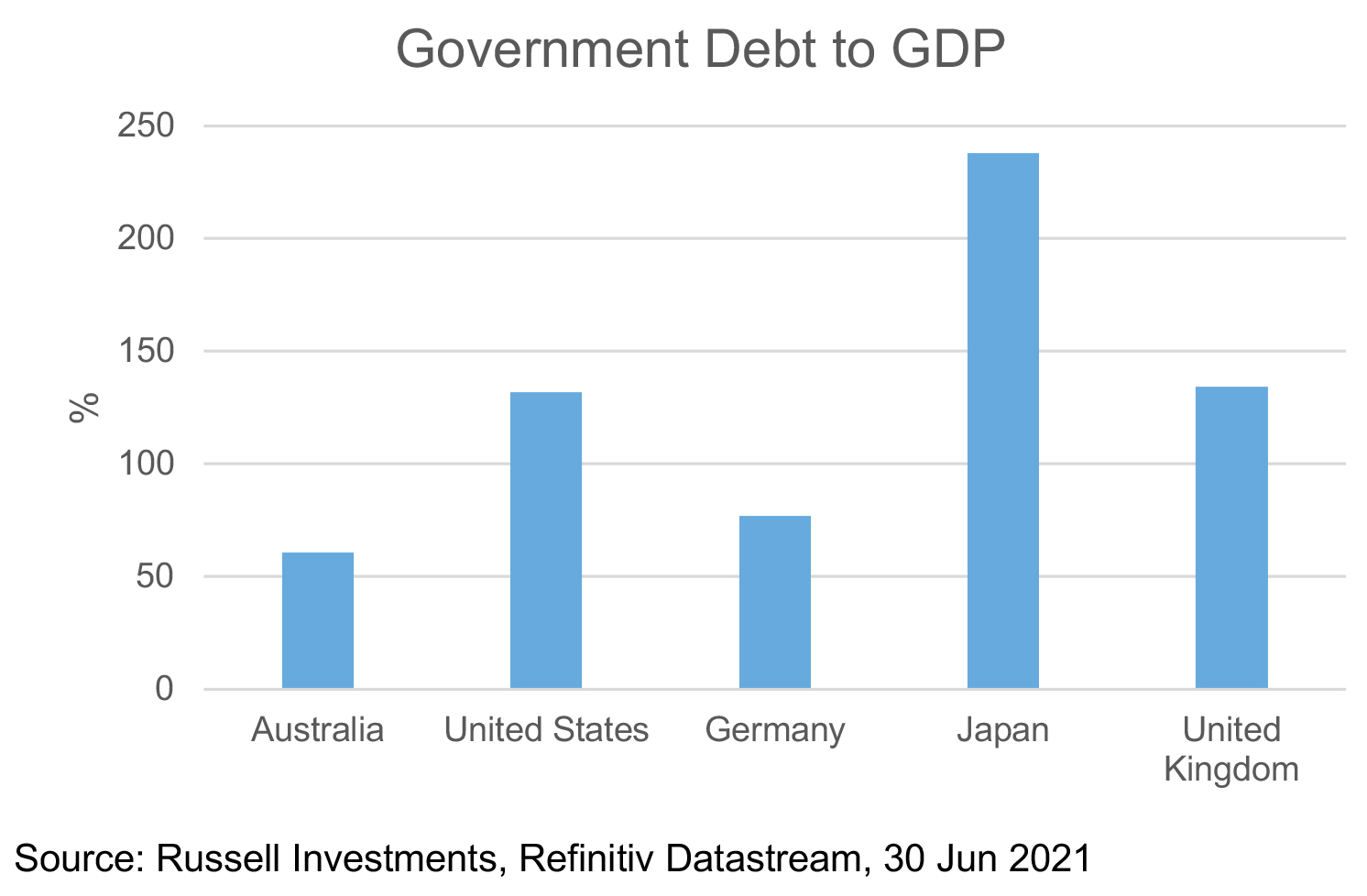

Government debt

The increase in government debt. Federal net debt is expected to peak at 40.9% of GDP[1] in a couple of years, this is viewed as quite low compared to other developed economies.

The recent State government budgets have shown similar increases, while corporates have also seen an increase in their debt loads over the past year. As noted above, both State government and corporate debt have a lower duration than Federal debt, and so are relatively less sensitive to increases in interest rates compared to Federal debt.

It is not expected that this increase in debt should concern investors in the nearer term, given how low interest rates are and the strong outlook for economic growth over the next 1-2 years. On a related note, it’s also not expected that the Federal or State governments will become overly concerned with the increase in government debt and implement forms of budget repair, given their focus on ensuring the economy was supported through COVID and the Federal governments focus on getting the unemployment rate below 4.5%.

ETF Innovation to meet client needs

Investors are starting to demand more specific exposures through ETFs such as different maturity buckets across the yield curve or different types of credit. This desire for more precise exposures has led to an increase in Bond ETF launches.

This ability to reflect an investment view by taking a position on credit or duration is an interesting dynamic and it is becoming more apparent that one ETF cannot provide everything an investor needs. As investors become more focused on fixed income buckets more specific solutions and products can help.

In the future, there is scope for significant further innovation in the Fixed Income ETF landscape particularly in areas like Environmental Social and Governance (ESG) and factor investing.

By Alistair Martyres

———