Practical advice tips – the SMSF consumer protection challenge

From a consumer protection perspective, the increasing popularity of SMSFs represents a giant red flag for regulators.

Introduction

The growth of Australia’s Self-Managed Super Fund (SMSF) sector continues unabated, with ATO June 2021 statistics[1] revealing the sector now holds a record $822 billion in assets, an increase of $23 billion on the prior quarter, and around $80 billion higher than in June 2020.

These assets are held in around 598,000 funds on behalf of 1.14 million members, and now account for more than one quarter of Australia’s total superannuation savings pool[2].

But from a consumer protection perspective, the increasing popularity of SMSFs represents a giant red flag for regulators.

The combination of unsophisticated investors – attracted to SMSFs as a vehicle for property ownership – and specialist ‘advisers’ with thinly veiled conflicts makes for a perfect storm of ‘financial harm’.

Unsurprisingly, complaints made by self-managed super fund trustees about inappropriate financial advice for their retirement savings made up the majority of all advice grievances that went to arbitration at the Australian Financial Complaints Authority (AFCA) in 2020[3].

With SMSF members and trustees subject to many risks not shared by members of public superannuation funds, regulators have made the mitigation of these risks – and the protection of SMSF investors – the focus of several specific interventions.

In this article we will examine the consumer protection challenges inherent in the sector, exploring the profile and motivations of SMSF members, the risks and the problems they face, the specialist advice disconnect, and the mitigants being put in place to ensure the fidelity of SMSFs as a retirement savings vehicle remains uncompromised.

The characteristics of SMSF investors

While the stereotypical view of SMSF investors as being older – mainly retired – couples is largely borne out by ATO data[4] (86% of SMSF members are aged 45 and over, and 40% are aged 65 and over), the age profile of newly established funds tells a much different story.

For some time now, the most active age cohort in establishing new SMSFs has been the 35–44 group[5]. At the September 2020 quarter, that group set up 35.4 per cent of new SMSFs – almost twice the next-largest proportion, the 45-to-49s, who accounted for 17.8 per cent.

Perhaps even more surprisingly, the 25-to-34 age bracket established 10.6 per cent of new SMSFs, reflecting the same desire – to be hands on with their investing – that has driven them into the sharemarket in record numbers since the start of 2020.

Around 69% of all SMSFs are two member funds (generally husband and wife), with a further 24% of funds containing one-member only[6].

The gender split of members is reasonably even[7] (53%/47% m/f).

Whilst the average taxable income of SMSF members was found to be nearly double that of other superannuation fund members[8] ($109k versus $59k in 2016), this is skewed somewhat by those on higher incomes, and a detailed breakdown[9] from 2021 revealed that over half of existing members (likely those in retirement) were reporting an annual taxable income under $60,000.

Motivations to invest in SMSFs

Whilst at a high level, the desire to be more hands on in running their superannuation is the main driver of SMSF establishments, recent years have seen property ownership ambitions become a far more significant influence.

Figure 1 below details the main reasons for establishing SMSFs, and compares funds established 1999 – 2002 with those established 2015 – 2017.

As can be seen, the ability for SMSF members to have more control over investments, and the belief that they could achieve higher returns, at lower cost by adopting a ‘DIY’ approach, have remained strong influencing factors over the years. Most notably however, the proportion of members citing the purchase of property as a main reason for establishing an SMSF almost quadrupled, (from 6% in 1999 – 2002, to 22% in the 2015 – 2017 period), a trend which lies at the heart of many of the consumer protection challenges regulators are grappling with in this sector.

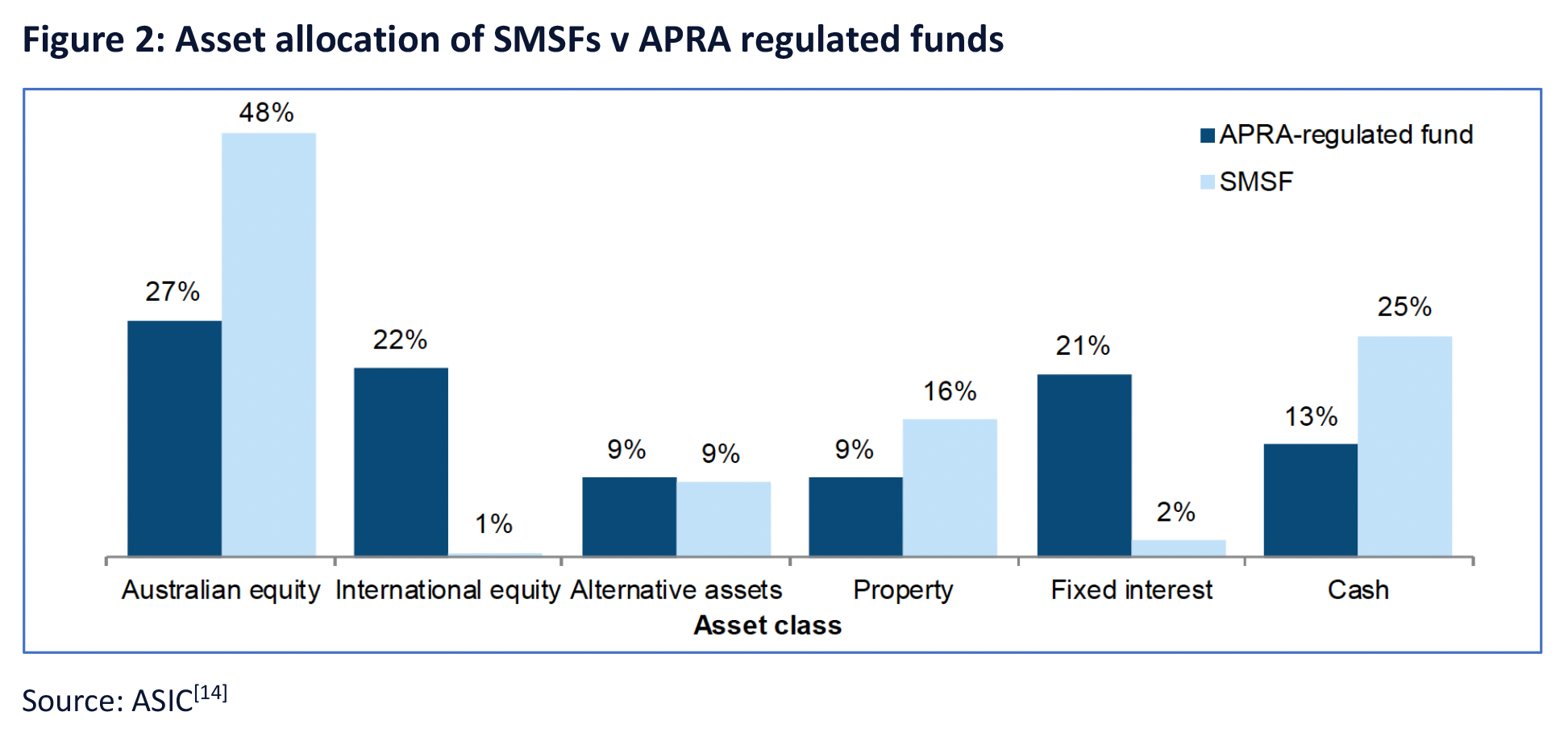

Concentration risk is rife

The increasing use of SMSFs as a property investment vehicle (albeit to fund retirement) is reflected in asset allocations which lack the diversity – and diversification – seen in professionally managed, APRA regulated funds.

Compared to APRA regulated funds, SMSFs are more heavily skewed towards cash, Australian shares, and property, likely reflecting the popularity of rental income and franking credits, as well as the more conservative approach you would expect from funds in the decumulation phase. Conversely, the relatively low levels of investment in fixed interest and overseas equities probably shows a lack of sophistication and lack of knowledge about how to access these investment classes.

ASIC research[11] from 2017 found the majority of SMSFs had more than 50% of their assets invested in a single asset class, exposing them to elevated levels of concentration risk.

(Even more alarming, 2019 figures suggest around 18,000 funds had 90% or more of their total assets exposed to a single asset class.)[12]

Whilst interest levels in cryptocurrency are growing, this class only accounts for around $200m in SMSF held assets, a tiny fraction of the overall pool.[13]

Other risks faced by SMSFs

In addition to the heightened levels of concentration risk borne by many SMSFs, trustees and members face a variety of other significant risks, including, but not limited to:

- Risks associated with the complexity of managing the administration and compliance obligations of SMSFs

- Underestimating the time and cost of managing an SMSF

- The costs of small balance funds

- Insurance cover risks (through inappropriate cancellation of existing cover or reduced access to group rates)

- Poor investment decisions made by unsophisticated investors

- Reduced access to dispute resolution bodies

- Lack of statutory compensation for theft or fraud

- Complexities and costs associated with fund structure, including

- Winding up the fund in the event of death or relationship breakdown

- Loss of capacity of a trustee

- Fund value falling below a financially viable level

- The treatment of death benefit nominations

SMSF reliance on advisers

The complexities of managing an SMSF make these risks significant, even for sophisticated investors with high levels of financial literacy, and it should come as no surprise that the vast majority of SMSFs call on a variety of ‘advisers’ to help run their funds.

In 2017, 79% of SMSFs had used at least one ‘adviser’ in the previous 12 months. On average, SMSF members using an ‘adviser’ engaged with two types of ‘advisers’ The most commonly used advisers were accountants, the main source of advice for 31% of SMSFs. 17% used a financial adviser, 10% used an SMSF administrator and 6% used a stockbroker[15].

Of particular concern for ASIC is the proliferation of the property ‘one stop shop’ model[16], an inherently conflicted model which promotes the purchase of geared residential property through an SMSF, arranged by groups of related real estate agents, developers, mortgage brokers, accountants, and financial advisers. Aside from compliance concerns, such funds are more likely to be subject to concentration risk.

The SMSF advice disconnect

Reports by both ASIC and The Productivity Commission have shed a spotlight on the poor quality of financial advice related to SMSFs.

ASIC, for Report 575, reviewed 250 client files randomly selected based on ATO data and assessed compliance with the Corporations Act’s best interests’ duty and related obligations.

Their review found that in 10 per cent of the files reviewed, the client was likely to be significantly worse off in retirement due to the advice.

They called out a number of areas as being especially problematic:

- More than a third of the SOAs reviewed recommended the fund invest in a single asset class, and in 95% of cases this was property

- In more than half the cases, a related party was recommended for the provision of administration services

- The large number of files where gearing was recommended and associated debt to asset ratios

- Prevalence of funds with starting balances lower than accepted benchmarks

ASIC also found that

- In 91% of files, the advice provider did not demonstrate compliance with the requirement to provide appropriate advice under s961G;

- In 86% of files, the advice provider did not demonstrate that they had prioritised the client’s interests under s961J; and

- where advice was provided to replace a superannuation product, information on the product replacement was inadequate or absent in 68% of files.

Little surprise then those complaints made by SMSF trustees about inappropriate financial advice for their retirement savings may account for a majority of advice related complaints submitted to AFCA.

Research[17] of more than 1,000 complaints upheld by AFCA in 2020 found that around 65 per cent of all paid advice claims related to SMSFs. (Over 90% of paid super claims were also found to be related to SMSFs).

The same analysis also found complaints related to SMSF gearing, limited recourse borrowing arrangements and real estate investment had all increased over the previous year.

Case study – AFCA upheld complaint re ‘balanced’ asset allocation

The subject of one complaint[18] upheld by AFCA were SMSF trustees, who were assessed as “balanced” investors, and advised to hold 30 per cent of the fund’s assets in a balanced managed fund, 7.5 per cent in cash and 62.5 per cent in a single asset – property.

AFCA found that whilst a balanced investment strategy does not automatically cease to be balanced because a higher-risk element, such as property, is introduced into a portfolio, an SMSF with an asset value of $271,415 which borrows an additional $295,000 to invest in property is not following a balanced strategy, given the loan-to-valuation ratio involved.

AFCA was satisfied that the complainants were not provided with appropriate financial advice, and the provider was forced to pay $334,000 in compensation.

Consumer Protections for SMSF trustees and members

A range of interventions across the 4 pillars of financial consumer protection (financial literacy, product regulation, disclosure, and financial advice) have been introduced over the years to mitigate many of the risks unique to SMSFs.

Financial literacy

Running an SMSF is complex, and both ASIC and the ATO (who regulate SMSFs) continue to make improved financial literacy amongst SMSF trustees a key focus.

Along with the variety of information on SMSFs carried on ASIC’s MoneySmart website, the ATO has produced a number of educational resources for SMSF trustees, including free training courses, short videos, and newsletters.

The ATO also takes a more collaborative view when working with trustees that have breached their obligations, and in some instances will mandate training rather than applying financial penalties.

Suggested benchmarks around the minimum fund balances are another example of educational messages aimed at trustees and flowed from work by the Productivity Commission which identified $500k as the balance at which SMSFs become cost competitive with large funds[19].

Misleading Advertising

In recent years we have seen ASIC intervene in several cases of advertising they felt promoted SMSFs in a misleading way.

Commenting on one specific case[20], ASIC noted their determination “that all consumers including those considering a self-managed approach to their super get accurate information and are not misled by any form of advertising, including online and through social media”

“Any comparisons between SMSFs, and industry and retail funds, particularly regarding performance or fees, must be accurate and have a reasonable basis. Any qualification should be apparent to a consumer when they first see the information.”

Regulation

While SMSFs themselves are not classed as financial products, many use financial products as inputs (credit, managed funds etc), which themselves are subject to comprehensive guidelines around disclosures.

SMSFs are regulated by the ATO, they are required to comply with strict and comprehensive regulations in order to enjoy the various tax concessions available to superannuation funds.

Whilst many of these regulations are not explicitly based on consumer protection objectives, they do serve to minimise the risks of poor financial outcomes and ensure that funds are more likely fit for purposes as a retirement savings vehicle, and in this sense, they act as important protections for members.

Examples of these ‘protective elements’ include:

- the requirement to have well-documented, specific investment strategy that considers risk, return and the unique circumstances of members

- the requirement for trustees to consider life insurance for their members

- the mandatory inclusion of dispute resolution clauses in the Trust Deed

- Limited Recourse Borrowing Arrangements (LRBA) – protect members by limiting access of lenders to fund assets in the event of loan default

- other borrowing restrictions

- the forbidding of loans or financial help to members or relatives

- rules limiting early access (in line with rules applying to all super funds) help ensure the funds are there at retirement – when they are needed most

- reporting obligations which force trustees to keep abreast of the financial performance of their fund from year to year.

Advice tips

One of the best consumer protections is obviously quality financial advice, and following their work as part of REP 575, ASIC published a series of helpful adviser tips, based around areas of concern identified within that report. A selection of these tips is listed below, with the full list – and detailed explanations – found in ASIC Information Sheet 205[21] (Advice on Self-Managed Superannuation Funds, Disclosure of risks) and Information Sheet 20622 (Advice on Self-Managed Super Funds, Disclosure of Costs).

Compliance Tips – Areas of Focus For ASIC

1. Issues around best interests’ duty and related obligations will be looked at more closely if the starting balance of the SMSF is below $500,000, or if it does not adequately disclose (including in the form of a comparison) or clearly set out the costs of setting up, operating, and winding up an SMSF, noting which are unavoidable costs and which are optional costs. These costs should at least be described and, where possible, quantified.

2. ASIC will look at whether the adviser has considered the costs and benefits of the following options for the client, including:

- not fully closing down the client’s existing APRA-regulated superannuation fund to maintain their existing life and TPD insurance cover

- not holding any life and TPD insurance, or

- replacing existing cover with a new insurance policy taken out by the SMSF on behalf of some or all of the members of the SMSF.

ASIC is likely to be especially concerned if:

- the client had an existing life and TPD insurance policy, but the adviser did not consider the risk of losing this cover when recommending the establishment of an SMSF

- there was no consideration of the client’s life and TPD insurance needs when they are not yet a retiree and have not accumulated a superannuation balance to be sufficiently self-insured.

3. Consideration of whether clients have been adequately advised about the time, skills, and obligations necessary to operate and SMSF, and that, even if they outsource some aspects of managing the fund, they will remain ultimately responsible for complying with their responsibilities and obligations.

ASIC will consider assessments of the client’s literacy and whether they are able to appropriately develop their skills and knowledge to operate an SMSF.

4. The advice received by clients about their SMSF Investment Strategy and whether or not that advice was appropriate to the risk appetite and investment goals of the clients.

Conclusion

The growing popularity of SMSFs makes it more than likely that advisers will need to provide advice about both existing and potential new funds. Although the provision of quality, compliant advice should largely be taken as a given, arguably the biggest consumer protection challenge in this sector is protecting clients from themselves. Specifically, clients who have been sold on the SMSF ‘property dream’ – either by their friends or by marketing messages they have seen/ heard – may well be at heightened risk of taking on a responsibility far more complex, time consuming and costly than they are prepared to deal with.

While some degree of consumer protection is inherent in various regulations and education initiatives rolled out across the SMSF sector, financial advice is arguably the most important pillar of protection of all for SMSF trustees and members.

Many historical examples of poor advice in this space have prompted ASIC to focus more intently on advice provided in the SMSF space, and they have published detailed guidelines around their expectations. As well as familiarising themselves with these guidelines, Advisers should generally tread with extra caution when providing advice around SMSFs, given the consumer protection challenges inherent in the DIY approach.

———