Products under the broad definition of ‘fixed income’ can differ markedly.

The concept of diversification has long underpinned modern portfolio theory and the widely adopted 60/40 approach to portfolio construction. At its most basic, this approach allocates 60 percent to growth investments and 40 percent to defensive assets; the latter is largely comprised of fixed income exposure. The allocation to growth and defensive assets is nuanced by the adviser according to each client’s objectives, needs and risk appetite.

Although fixed income is typically regarded as a defensive asset class, it is not always easy to distinguish the risks associated with the array of investments that fall under this umbrella term. As a result, advisers and investors can be unaware of the differences between credit risk and interest rate risk; understandable given that credit markets (credit risk) and bond markets (interest rate risk) both fall into the broader category of fixed income.

However, the exposure to credit or interest rate risk is important to understand. What might be an acceptable risk for one investor may not be appropriate for another. A risk that might seem relatively minor at one point of the market cycle may be exacerbated in another. An investment that appears defensive may, in fact, not provide those characteristics.

Fixed income securities issued by credit markets and bond markets may be viewed as comparable instruments for several reasons:

- both are defensive assets that produce low levels of volatility when other riskier asset classes, such as equities, sell off

- both are conservative asset classes and have provided stability to portfolio returns in periods of volatility

- over the past decade, the two asset classes have exhibited very similar outcomes; however, the extent to which they move in tandem is heavily dependent on the direction of interest rates.

Funds active in the Australian fixed income markets can be broadly divided into two categories:

- Those active in the credit markets, but don’t take on interest rate exposure.

- Those that combine interest rate risk and credit risk, but whose return profile is primarily dominated by movements in interest rates rather than credit. Such funds generally hold securities with an average credit rating of AA, implying minimal additional default risk.

The use of generic fund names – such as ‘bond fund’ or ‘fixed income fund’ – make it challenging to discern the underlying investment strategy. The simplest way to do this is via the Product Disclosure Statement or the fund’s benchmark.

Funds that only take credit risk tend to be benchmarked against the Ausbond Bank Bill Index or the RBA Cash Rate, sometimes with a spread attached. The Ausbond Composite Bond Index or Bloomberg Barclays Global Aggregate Total Return Index are common benchmarks for funds that primarily target interest rate risk.

However, even the benchmark can be misleading. Around 50 percent of fixed income funds in the Lonsec Fixed Income Sector Review 2019 were benchmarked against the Ausbond Bank Bill Index or the RBA Cash Rate, yet only 60 percent of these funds, according to their factsheets, don’t take interest rate risk. This can be determined by the fact that the fund takes little (less than a year) or no, interest rate duration, as evidenced by fund reporting.

Interest rate duration is the key measure of interest rate risk, while credit duration or spread duration signifies the fund is taking credit risk.

Return profiles

When selecting between interest rate and credit products, it would be easy to be oblivious of the different risk profiles of the two if examining returns over the past decade, when performance of credit markets and bond markets were broadly similar.

To illustrate this, we created a credit only, floating rate note index using credit spread movement in the ICE BofA BBB US Corporate Index 5-7 year (Credit Index) and compared it to the ICE BofA Treasury Index, a portfolio of US treasuries with no credit risk (Interest Rate Index). We use US markets as they provide a longer, richer data set.

Graph one illustrates the performance of these indices over the past decade, with a base of 1 set in August 2011.

The Credit Index and the Interest Rate Index (the Indices) achieved similar outcomes. In periods of extreme volatility, such as March 2020, the Interest Rate Index outperformed the Credit Index. At the same time, the Credit Index still exhibited conservative characteristics when you consider that the US S&P500 was down more than 30% peak to trough during March 2020.

The Credit Index generated a return of 35% over the past decade, at an average annual compounded rate of 3.05%. The Interest Rate Index generated 25% over the same period, at an annual compounded rate of 2.27%. These results occurred in an environment where interest rates marginally tightened but were mostly benign.

A world of falling rates

Over the past 40 years, interest rates have steadily declined. The world has been in the grip of secular stagnation causing yields on 10 year government bonds for each cycle peak to be lower than the prior cycle peak. Secular stagnation is a problem of planned savings exceeding investment, which is caused by a number of structural factors including:

- the ageing populations of Western countries

- rising global inequity

- the slowdown in productivity growth.

Graph two illustrates the movement in 10 year treasury bonds over this period.

So, how did the two Indices perform in such an environment?

To make the comparison, we had to recreate both Indices as the underlying data series did not extend far enough into the past; the key component of the Credit Index, the ICE BofA BBB US Corporate Index 5-7 year, dates back to 1996, while the ICE BofA Treasury Index commenced in 1977.

The recreation of the Credit Index involved regressing movements in the ICE BofA BBB US Corporate Index 5-7 against the S&P 500 Index to determine likely historical spread movements. This was then combined with Moody’s and S&P default data, as well as Libor levels, to form the performance of the Credit Index. The Moody’s and S&P default data for BBB credit is very low and so doesn’t have a significant impact on the returns of the Credit Index. Over the period 1981 to 2021, on average BBB credits defaulted at a rate of 0.14%, so the main contributor to the returns of the Credit Index in any period was the movement in spreads and the issue’s coupon.

The recreation of the Interest Rate Index was quite simple. The ICE BofA Treasury Index has an extremely high correlation with moves in 5 year and 10 year treasuries, which have history going back to the start of the last century. Graph three shows the output of the two Indices.

The Credit Index increased 10-fold at an annualised compounded rate of 5.95%, benefiting from high coupon rates and a low level of defaults. As a floating rate that doesn’t experience capital appreciation when interest rates fall, 5.84% of the Credit Index’s 5.95% return was due to coupon payments.

By comparison, the Interest Rate Index nearly doubled that, with a 17-fold increase or an annualised compounded rate of 7.39%. Of this, 5.48% was attributable to coupons and 1.91% was gained through capital appreciation of the underlying assets.

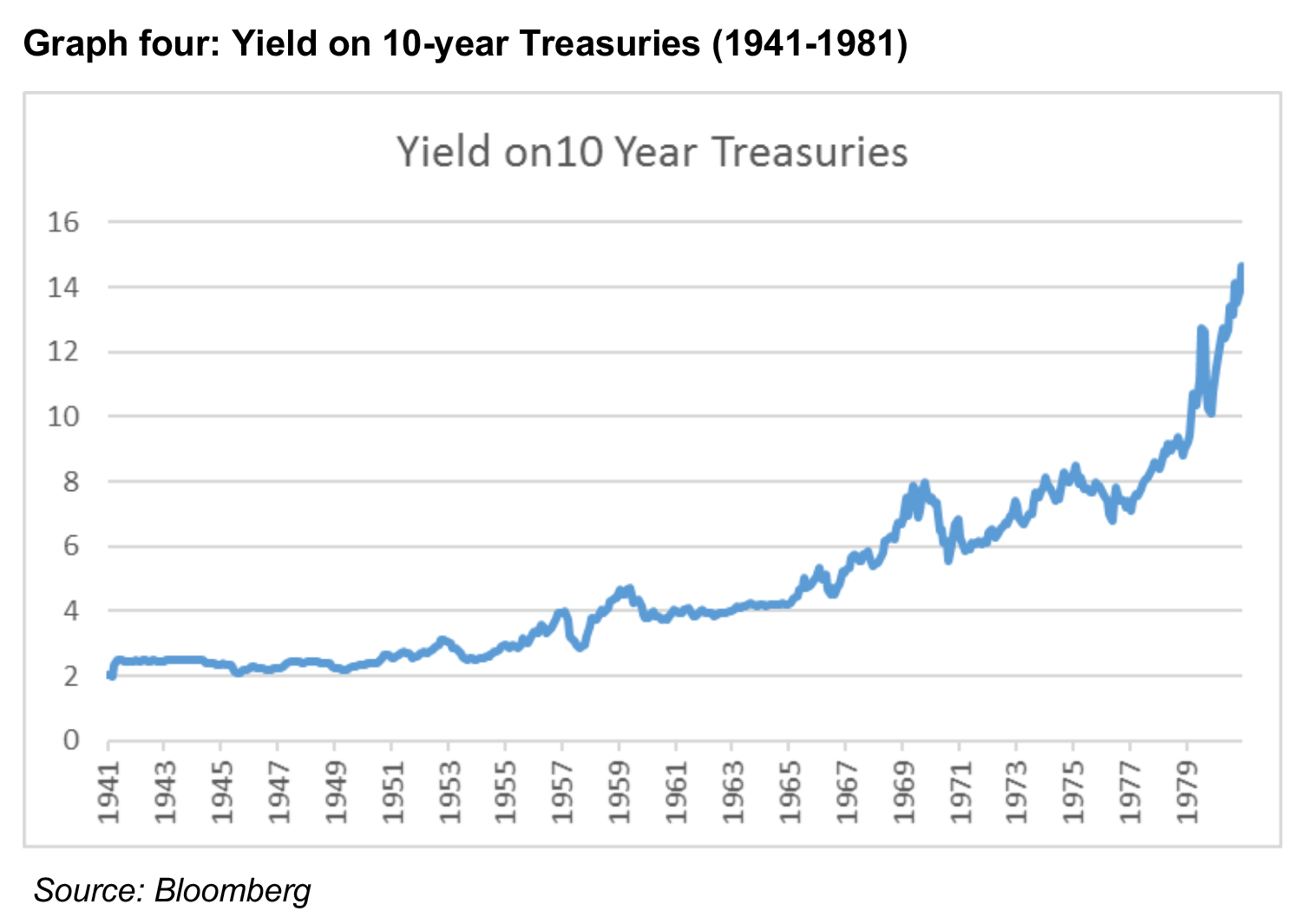

While interest rates fell over the past 40 years, benefiting the Interest Rate Index over the Credit Index, the story over the 40 years prior was starkly different. Between 1941 and 1981 interest rates constantly climbed and accelerated towards the end of that period, as shown in graph four.

Inflation in the mid-sixties was benign, running at around 1% per annum. This changed, however, with the collapse of the Bretton Woods system of backing the US dollar with gold and the subsequent mismanagement of monetary policy.

Demand-pull inflation appeared as a result of significant fiscal stimulus caused by a combination of spending programs and the cost of the Vietnam war. The US Federal Reserve refused to raise rates believing that a higher but sustainable level of inflation would help achieve full employment in the US.

However, cost push inflation also appeared, caused by a number of energy crises that fed into higher retail prices of core goods. This ultimately culminated in inflation reaching more than 13% in 1980.

In that environment, the Interest Rate Index clearly underperformed the Credit Index (as shown in graph five).

From 1941 to 1981, the Credit Index rose by more than nine times, at an annualised rate of 5.8%. Over the same period, the Fixed Interest Index increased just 3.4 times, an annual rate of 3.07%. As interest rates rise, the price of instruments with a fixed coupon fall, resulting in a capital loss on disposal of that asset.

The Interest Rate Index experienced continued capital losses during this period; it generated a return from coupons of 4.71% but lost 1.68% from negative price movements. The Credit Index benefitted 5.88% from coupons, with just a 0.08% loss due to capital movements.

The acceleration of performance of the credit index in graph five is consistent with the acceleration of 10 year US government bond rates shown in graph four. As interest rates move higher, the coupon on the Credit Index becomes greater, which in turn generates a stronger performance. The capital loss component of the Credit Index is immaterial.

While the possibility of the world again experiencing the type of hyperinflation seen in the 1970s seems remote, we now appear to be at a crossroads, one where the inflation story is turning around. The structural problems that have caused inflation and interest rates to fall over the past 40 years still remain; the average age of the world’s western populations will continue to rise over the next couple of decades.

However, an aggressive approach to fiscal stimulus has become a more acceptable policy response to lagging economic conditions, which looks to offset these structural disinflationary factors. Wage inflation has continued to rise, being supported by sluggish labour participation rates and this looks to sustain the current high levels of inflation, and in turn lead to higher interest rates.

The principles of diversification and asset allocation equally apply within the defensive component of a diversified investment portfolio. This is why it is important for advisers and investors understand the difference between credit risk and interest rate risk, and the part exposure to each should play in portfolio construction.

It is important that advisers investigate which risks the fixed income funds they recommend are exposed to; a fund’s portfolio is likely to contain a number of different investments dependent on the fund’s to investment objectives and, in some cases, market conditions. The benchmark adopted for a specific fixed income fund can provide a good indication as to whether its primary risk is interest rates or credit; however, the best way to determine this is by scrutinising each fund’s product disclosure statement and relevant fund factsheets.