Increasing exposure to riskier assets to chase yield is not the only course of action available.

Prior to 2008, a consistent factor in the personal investing landscape was the availability of low risk, meaningful returns generated from either cash deposits or government bonds. Apart from being a reliable source of income, such investments could be relied upon to provide a level of capital protection against declines in the riskier equities markets.

However, since the 2008 Global Financial Crisis (GFC), and more so since the arrival of the COVID-19 virus in 2020, investors are no longer afforded the luxury of generating meaningful low risk returns from these traditional fixed income assets. This has created significant challenges for investors relying on their portfolio income to meet their lifestyle needs.

There is no simple explanation as to how this situation arose; rather, it’s the culmination of multiple factors that commenced 70 years ago.

In that time the Australian economy and, in particular, interest rates have been buffeted by a number of forces, including:

- excessive inflation

- monumental structural changes to the economy and financial markets

- the arrival of black swan events.

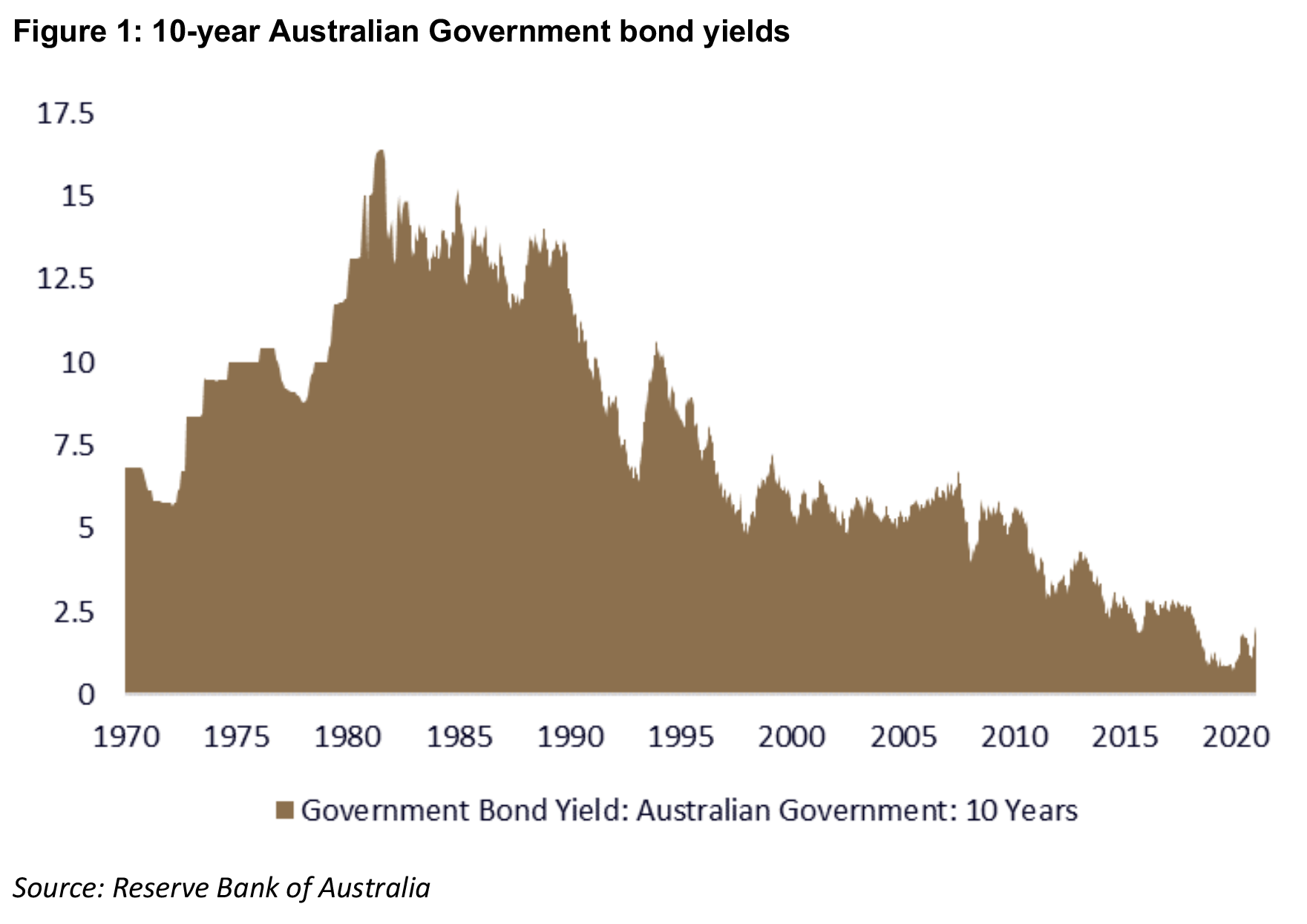

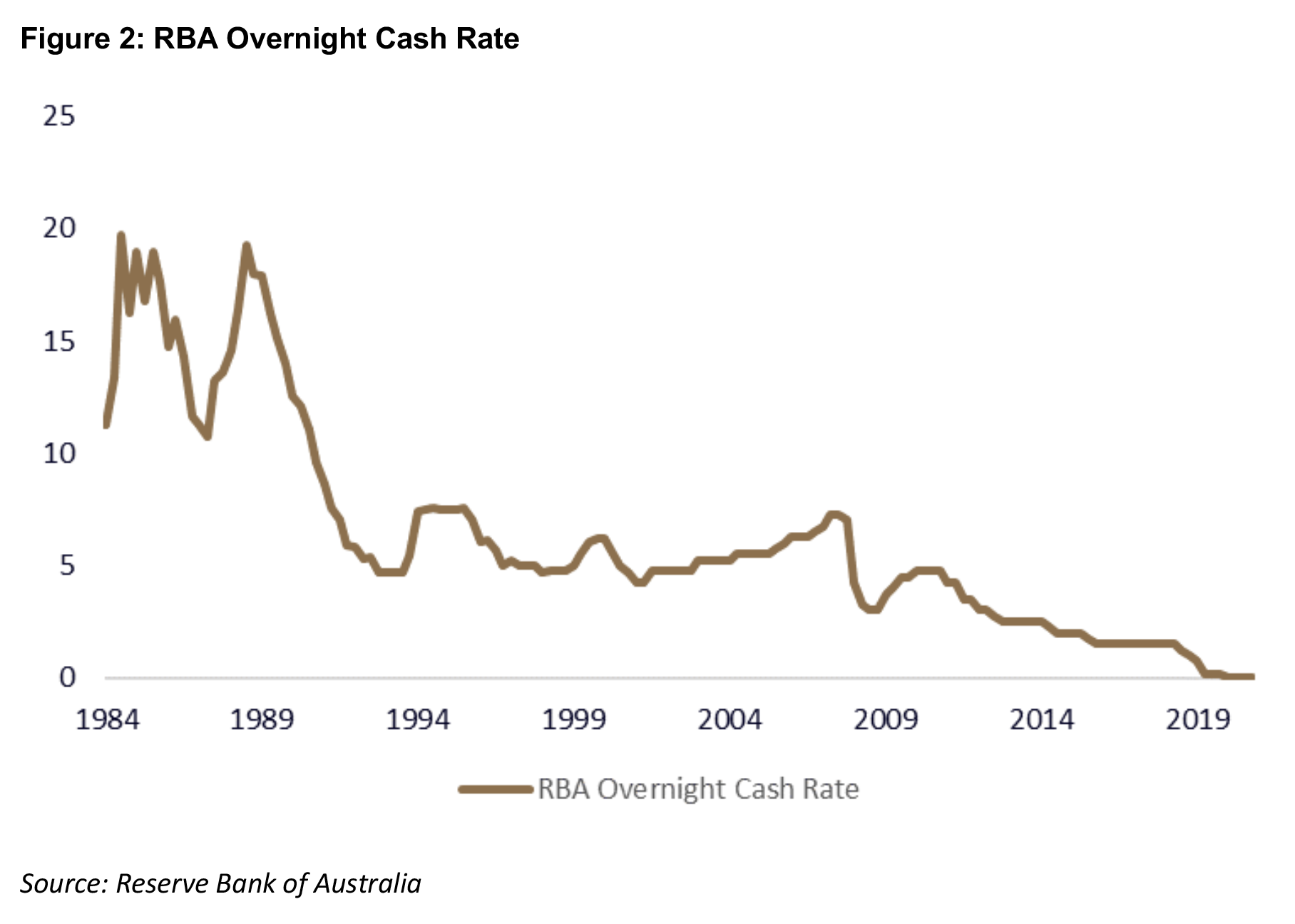

Dealing with these challenges has in turn required novel policy responses by governments and central banks across the globe, most of which have been designed to lower interest rates as highlighted in figures one and two.

The role of the RBA

An assessment of the Australian interest rate environment cannot be undertaken without considering the role of the Reserve Bank of Australia (RBA). The RBA was formed in 1960, with its original charter to assist in ensuring full employment, economic prosperity, and a stable currency within the Australian economy.

To assist the RBA in achieving the policy objectives embodied in its charter, it assumed control of setting interest rates, which was previously the responsibility of the Commonwealth Government. During its early years, the RBA influence was muted, especially when compared to the present, as countries remained under the post-World War II Bretton Woods exchange rate mechanism.

At the same time, the Australian economy was growing steadily in the post war years with little sign of inflation. Keynesian economics, which saw little need for interest rate policies, was the dominant policy tool for managing stable economic growth. During this period, an investor was able to earn interest rates of around 5% using bank term deposits, thereby offering investors a solid low risk fixed income.

The “Golden Age” of Western economic growth came to a grinding halt in the 1970s, with consumers facing punishing inflation, high unemployment, low to negative economic growth (a combination known as stagflation, a concept that will reappear post the GFC) and excessive interest rates.

In brief, the economic dramas of the 1970s evolved after the abandonment of the Bretton Woods system of fixed currency rates. This change saw disciplines around capital controls disappear, with the emergence of volatility in economic growth and price. Amplifying the instability was the prevalence of input cost pressures, including a notable spike in oil prices.

The Keynesian policy framework was discarded at this time as it was seen to be ineffective. It was replaced by the new Monetarist approach, which emphasised the role of money supply and interest rates in controlling inflation and maintaining economic stability. This policy shift marks the point in time when central bank actions moved to the forefront of investors’ minds, especially as interest rates rose to well over 15% by the end of the decade.

Another consideration for investors during this period was the transition from academia to practice of Modern Portfolio Theory (MPT). As a consequence, investors became familiar with concepts such as 60/40 portfolios and risk appropriate asset allocation. MPT directed investors to allocate a given proportion of their portfolio to risky assets, such as equities, and the remainder in lower risk fixed income assets based on their risk tolerance. Importantly, with interest rates rocketing into the double digits and equity returns remaining subdued, investor confidence in new the approach grew.

While the 1980s marked the beginning and end of the trend of rising interest rates, the Australian public had to endure several years of punitive rates (for those borrowing money) before permanent relief finally arrived. Unfortunately, the reprieve arrived with what was to be Australia’s last recession for over 30 years, with the streak of positive economic growth only interrupted by the arrival of the COVID-19 virus.

The genesis of the volatile nature of interest rates in the 1980s was the Australian economy undergoing significant structural change that ultimately caused some unintended consequences. Crucial changes were the deregulation of financial markets and the floating of the Australian dollar. These changes presented new challenges to the RBA, including excessive investment speculation, an overly volatile currency, and the return of inflation. The RBA’s response was to increase interest rates again at the end of the decade, a response that contributed to the arrival of a deep recession.

The one upside of the 1990s recession was that inflation had truly been defeated. In addition, many of the structural contributors to the previous outbreak of inflation – for example institutional wage setting and the non-floating currency – were removed.

These changes allowed the RBA to rapidly reduce interest rates in the first half of the decade (the cash rate reduced from 17.5% in January 1990 to 4.75% by July 1993) and turn its focus to maintaining price stability, a change highlighted by the official adoption of a 2-3% inflation target in the early 1990s.

Rates did increase by 2.75% in the middle of the decade as the economic recovery picked up pace, but these increases were reversed some two years later as the RBA felt that the threat of returning inflation was over and the economy could continue on its current trajectory. By the late 1990s investors and consumers were well and truly in a new world where interest rates hovered around 5% with the occasional move higher or lower as the RBA attempted to fine tune the speed of the economy.

From the GFC to Covid-19

The period from ‘the easing of interest rates’ in the 80s until the commencement of the GFC in 2008 is considered the “Great Moderation”; a period when central bankers’ influence on the market became more profound due to their perceived ability to smooth economic volatility and ensure the public enjoyed solid income growth without the reappearance of inflation.

However, this illusion came crashing down in 2008 as firstly financial markets, closely followed by the global economy, collapsed as the contagion from reckless practices in the US housing market spread across the globe. Importantly, these practices were spurred by the desire to manufacture attractive fixed income products for investors in the new world of low interest rates.

To stave off a deep recession the RBA followed the lead of other central banks during this time and dramatically lowered interest rates — the cash rate fell from 7.0% in September 2008 to 3.0% in April 2009. Thereby, for the first time since World War, II investors were faced with generating little to no income from their bank deposits – but, after seeing equity markets fall by 40-50% from peak to trough, this issue was not an immediate concern.

Once the Australian economy stabilised from the effects of the GFC, the question of when interest rates would return to natural levels quickly consumed market observers. Those promoting a rapid return won the early debate as the RBA started lifting rates late in 2009 as the Australian economy picked up steam due to a huge amount of mining and energy capital expenditure and booming commodity prices.

However, that was not the end of the story. Larger economic forces started to take hold across the globe and the direct consequence of these forces was an extended period of secular stagflation as economies struggled to generate growth close to trend. For Australia, this saw the RBA consistently cut the cash rate from November 2011 to the point that it reached 0.75% prior to the arrival of the COVID-19 pandemic.

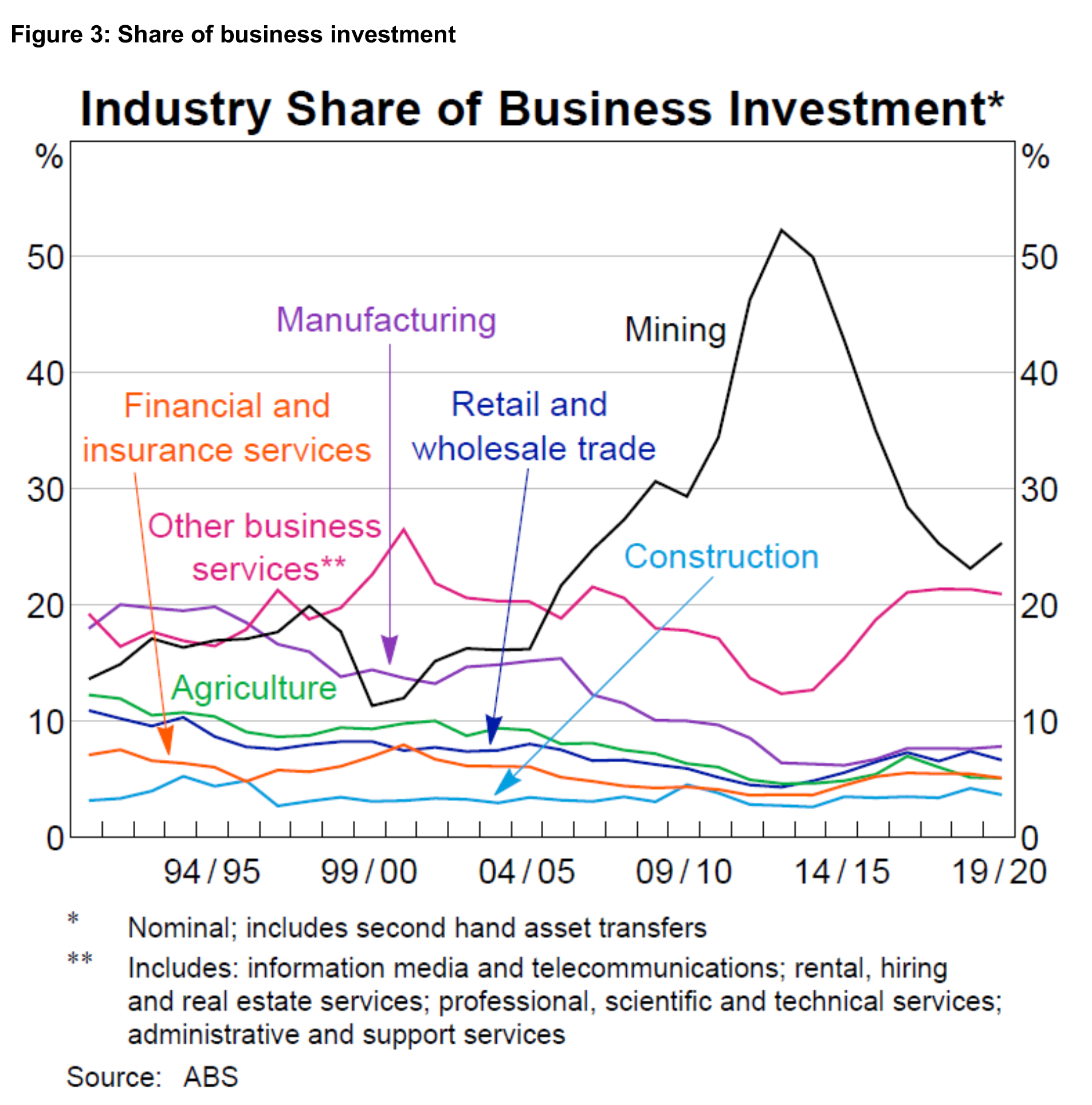

While the lower for longer interest rate mantra took some time to assert itself, the driving forces behind it had been building for some time. These forces included stagnant business investment across many sectors (figure three), leading to minimal productivity gains, fiscal austerity by Western governments, increasing income inequality, and reduced gains from globalisation.

The upshot for the Australian economy, and the RBA, was that wage pressures, and therefore inflation expectations, were non-existent. This situation left the RBA with no choice but to keep interest rates lower for longer in the hope of spurring some inflation. A significant side-effect from the RBA policy is that people relying on a stable fixed income generated from bank deposits have found themselves in need of other income sources, including an inappropriate increased exposure to risky assets.

The impact on investors

The most recent downward leg in interest rates saw the Australian cash rate hit 0.10% in June 2020, a move in response to the massive economic downturn caused by the COVID-19 pandemic. Central banks had little option but to slash rates in an attempt to stave off a more severe downturn. In addition, for the first time in its history, the RBA undertook practices to ensure that medium term rates remained as low as possible after the cash rate hit its lower bound.

Despite these historically low rates, at the end of September 2021, Australian investors had more than $400 billion on deposit with financial institutions[1], earning less than one percent per annum, a level lower than the inflation rate on an after-tax basis for most investors.

While government fiscal stimulus has supported the public through the pandemic, as the world returns to a level of normality those dependent on returns from traditional fixed income assets are facing an unkind outlook. The RBA has committed to not raising rates until inflation is persistently above its 2-3% range, which they’re currently predicting to be in 2024.

With inflation rising in other developed economies, notably the United States, it’s possible this could change. Given rates are already at their lower bound, any lift in rates will be detrimental to the capital performance of portfolios with their defensive asset allocation held mostly in government bonds, as is common across 60/40 portfolios and for those investors with a lower level of risk tolerance.

Increasing exposure to riskier assets to chase yield is not the only course of action available and, more so than ever, individuals must consider their income requirements and the level of risk they’re willing to take to achieve them going forward. Floating rate fixed income investments and credit funds may provide an enhanced return outlook without significantly increasing risk.

———