Inflation is a perennial concern, particularly among bond investors.

As the inflation debate continues, the economics team at fixed income specialists Payden & Rygel – one of GSFM’s investment partners – weighs in on what they think (almost) everyone is missing.

Inflation is once again a hot topic. This is not new; inflation is a perennial concern, particularly among bond investors. It’s understandable. When your coupon income is “fixed,” the last thing you want to do is erode the purchasing power of your stream of payments.

These fears extend beyond bond investors, as news of rising price pressures is dominating the headlines at present. A 2021 survey by Fortune magazine found that 87% of Americans are concerned about inflation, and 58% are “very concerned.”[1]

Lumber prices, car rental fees, new and used vehicle prices, medical care costs, tuition, and home prices have all skyrocketed. The experience in Australia is similar.

In the Wall Street Journal, James Mackintosh penned a piece whose title sums up the market consensus nicely: “Everything Screams Inflation.”[2]

Everything? We’re not so sure.

In what follows, we will review what inflation is, how it is measured (and some complications associated with its measurement), and why understanding inflation matters for investors in 2022 and beyond.

Purchasing power

We admit that prices are up—but is it “inflation”?

The first and perhaps most important thing to note is that price movements alone do not necessarily mean inflation. Instead, inflation is the thing that occurs when the purchasing power of money declines.

Yes, one main symptom of declining purchasing power is higher prices. However, the reasons for price increases are also important.

If the prices of goods and services are on the rise NOT because the money in your pocket is diminishing in value but because everyone wants to go to, say, Hawaii, that’s not inflation.

As economists, the why matters. The story behind each price increase (or decrease) matters.

Many things can cause prices to change. A lousy harvest ruins wheat crops. A cyclone destroys banana production. A sudden urge by a wide swath of the population to abandon urban apartment dwellings for single-family homes in suburbia or regional areas overwhelms the available supply. Homebuilders cannot produce homes quickly enough to cope with relative demand shifts.

However, important to our Hawaiian vacation example, adjustments can be made on the supply and demand sides of the equation. More rental cars will be sent to Hawaii eventually, and surging prices will force consumers to reconsider Hawaii as a summer vacation destination (at least this year), ultimately impacting prices.

A similar supply-and-demand story lurks behind many of the other price surges making headlines lately. For example, semiconductors are in short supply in 2021 because automakers cancelled chip orders in 2020, fearing a pandemic-induced demand slump would be slow to rebound. Instead, demand rebounded sharply. Unfortunately, supply chains will take more time to adjust.

These are not mere anecdotes about how dynamic the economy is—though they are that also! These anecdotes underlie our belief that recent price pressures will prove transitory, meaning price pressures could last several quarters, or in the case of chips, into next year. But producers will resolve them. Container ship crews stuck off the coast of Los Angeles will disembark and unload materials. And price pressures will abate.

Underlying our optimism are the stories behind the recent price changes that have to do with supply-demand mismatches and are not a reflection of the diminishing purchasing power of our money.

Did you know? The Fed’s inflation target

The Federal Reserve has a dual mandate of stable prices and maximum employment. The latter is a priority for the Fed, but most central banks aim only for stable prices. The former is the Fed’s most important role, made more famous by Chair Paul Volcker’s sharp increase in the Fed Funds rate to fight inflation in the 1970s. In 2012, the Fed adopted a 2% inflation target as measured by core PCE, its preferred inflation gauge. In 2020, after years of being below the target, the Fed amended its inflation goals. While keeping the 2% inflation target, the Fed amended its goals and objective to reflect “the view that this objective can best be met by seeking to achieve inflation that averages 2 percent over time.” Today, the Fed has faith in FAIT, flexible average inflation targeting.

If you can’t measure it, you can’t manage it

So, if price pressures alone don’t necessarily signal inflation, why does everyone seem to think they do? Well, directly measuring the purchasing power of money is difficult, so economists use a proxy instead: the cost of a basket of goods and services over time.

The idea is that temporary price pressures will fade, some prices (e.g., for Hawaiian hotel rooms) will rise, but others (food at home) will fall. Then, the average change in the price level over time will capture the underlying trend (inflation).

But it’s notoriously tricky to measure prices correctly. Who determines what’s in the basket and in what amount? How often should we change the basket? In the following example, each person’s experience of “inflation” could be drastically different from their neighbour’s; it’s entirely dependent on each person’s specific consumer baskets.

Perhaps unsurprisingly, economists couldn’t agree on just one basket, so there are many.

For example, there’s the popular Consumer Price Index (CPI) and the Fed’s preferred inflation gauge, the Personal Consumption Expenditures (PCE) deflator. There are also headline (overall) and core (excluding volatile food and energy categories) measures.

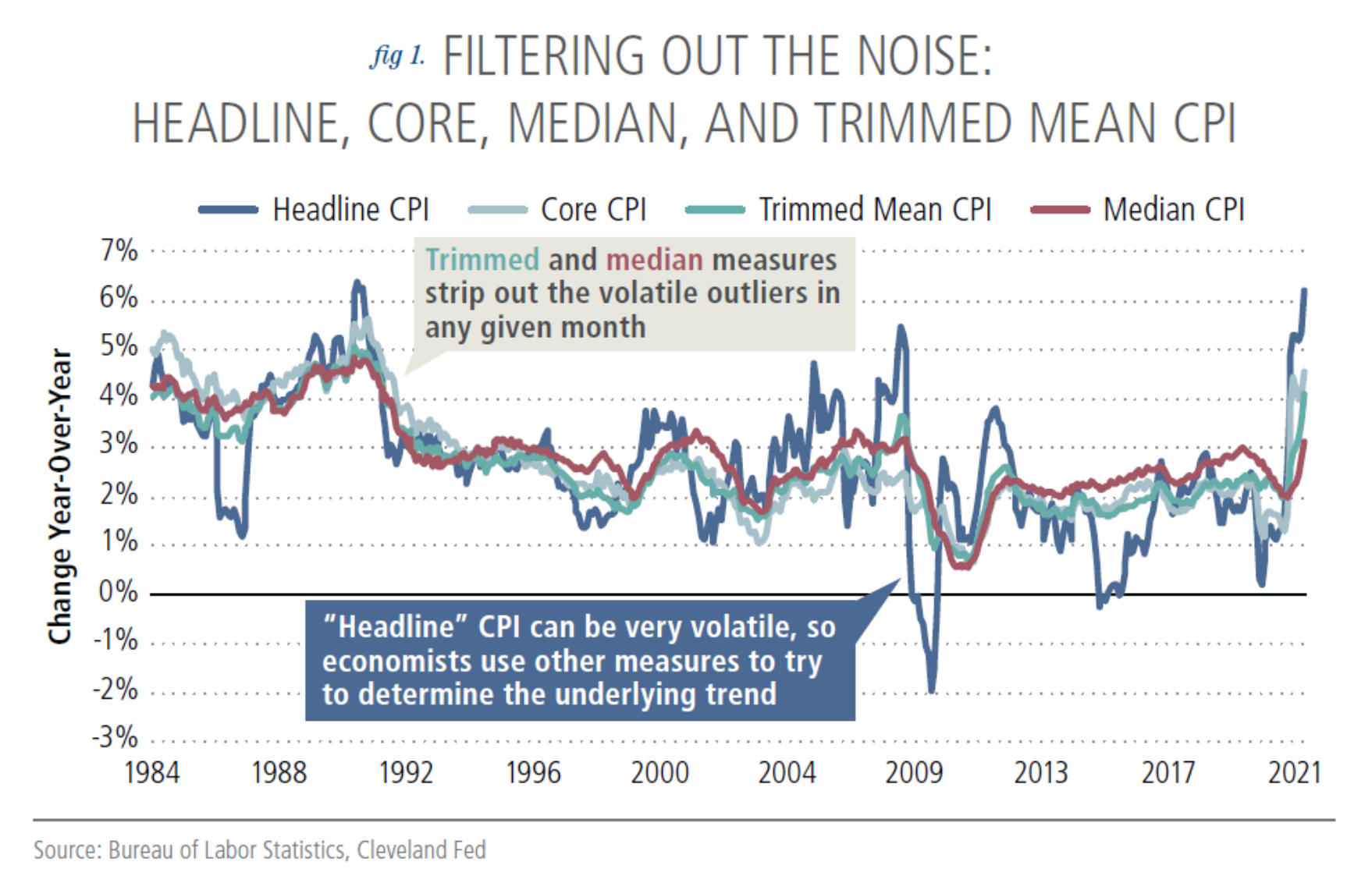

We (the Payden Economics Team) prefer the trimmed mean and median estimates produced by the Federal Reserve Bank of Cleveland and the Federal Reserve Bank of Dallas, respectively. We prefer these two measures because they strip out the volatile outliers in any given month regardless of whether the culprits are food and energy or something else altogether (see Figure 1).

In short, don’t confuse the measure for the subject. Since prices are inputs into price indexes, it’s easy to conclude that inflation is prices. Price baskets are mere attempts to gauge inflation, not inflation itself. Prices can change for all sorts of reasons. But if you have to pick one (or two), we recommend using a median or trimmed mean measure to guide your inflation views.

The supply of and demand for money

So, if inflation is about the purchasing power of money, what changes purchasing power? We have to go back to basics: supply and demand.

Fed-haters will immediately pounce on the supply concept and chime in here: “The Fed prints money, and that’s devaluing the currency! The money supply has exploded!”

Not so fast.

The Federal Reserve is part of the equation in a modern economy albeit a relatively small player in expanding the broader money supply. So yes, they do “print” high-powered bank reserves, but they don’t print money. The Treasury does that.

Money supply is a broad measure that includes the reserves at the Fed, coins in your pocket, cash in the ATM, deposits in the bank, savings in your money market fund, liquid assets in your enhanced cash portfolio, lending provided by banks and other financial institutions, etc. There is ample “supply,” and its composition is determined less by the Fed and more by a vast array of institutions who are willing to grant you credit.

In other words, the supply of money is complicated. Strictly speaking, a growing supply puts downward pressure on purchasing power and upward pressure on prices, all else being equal.

While the money supply has increased, it does not reflect “money printing” (see Figure 2). It reflects savings due to a change in the Fed’s methodology for calculating the money supply that aggregates checking and savings accounts. Conveniently for the conspiracy theorists, the difference went into effect just as the Covid-19 pandemic took hold![3]

Some households also amassed savings during the pandemic, boosting the measure.

The other part of the money equation, demand, is also important. If consumers maintain confidence in and hold the currency, price pressures remain subdued.

Suppose currency holders have dim expectations for their currency’s future. They might seek to rid themselves of it and hold something else that will better maintain purchasing power.

History shows us repeated examples of the phenomenon described above: Turkey, Argentina, and Brazil. Even the United States and much of the developed world in the 1970s saw the demand for their currencies drop precipitously after the Bretton Woods currency system collapsed.

In short, the confidence consumers have in a currency is much more likely to determine the long-term purchasing power of said currency (and, therefore, inflation) than the movements in the cost of a basket of goods and services. Unfortunately for economists, consumer confidence in a currency is harder to measure reliably than tabulating the cost of a sample basket.

Putting inflation fears to rest

Now that we understand what drives the purchasing power of money and what distinguishes price pressures from inflation, we can address the widespread fears about inflation.

What about a return to the 1970s? As we learned, in the 1970s, a flight from dollars to goods holding more value can be sudden—and violent. Understanding the confluence of events precipitating the rise of inflation in the 1970s may allay fears of “repeating the 1970s,” which cast a long shadow over today’s arguments about inflation.

Is the dollar perched on the precipice of a massive decline? We don’t think so.

We can hear you saying, “What about the Federal budget deficit? The stimulus rounds surely count as inflation.”

But do they? Since the federal government had insufficient funds available to pay the bills, it borrowed in the markets. Thus, the Treasury borrowed money from someone and transferred it to someone else. Does that change the purchasing power? Not necessarily.

We can’t find an empirical relationship between debt and inflation in the developed world.

However, if we use Japan and the US as examples, debt growth appears to dampen inflation!

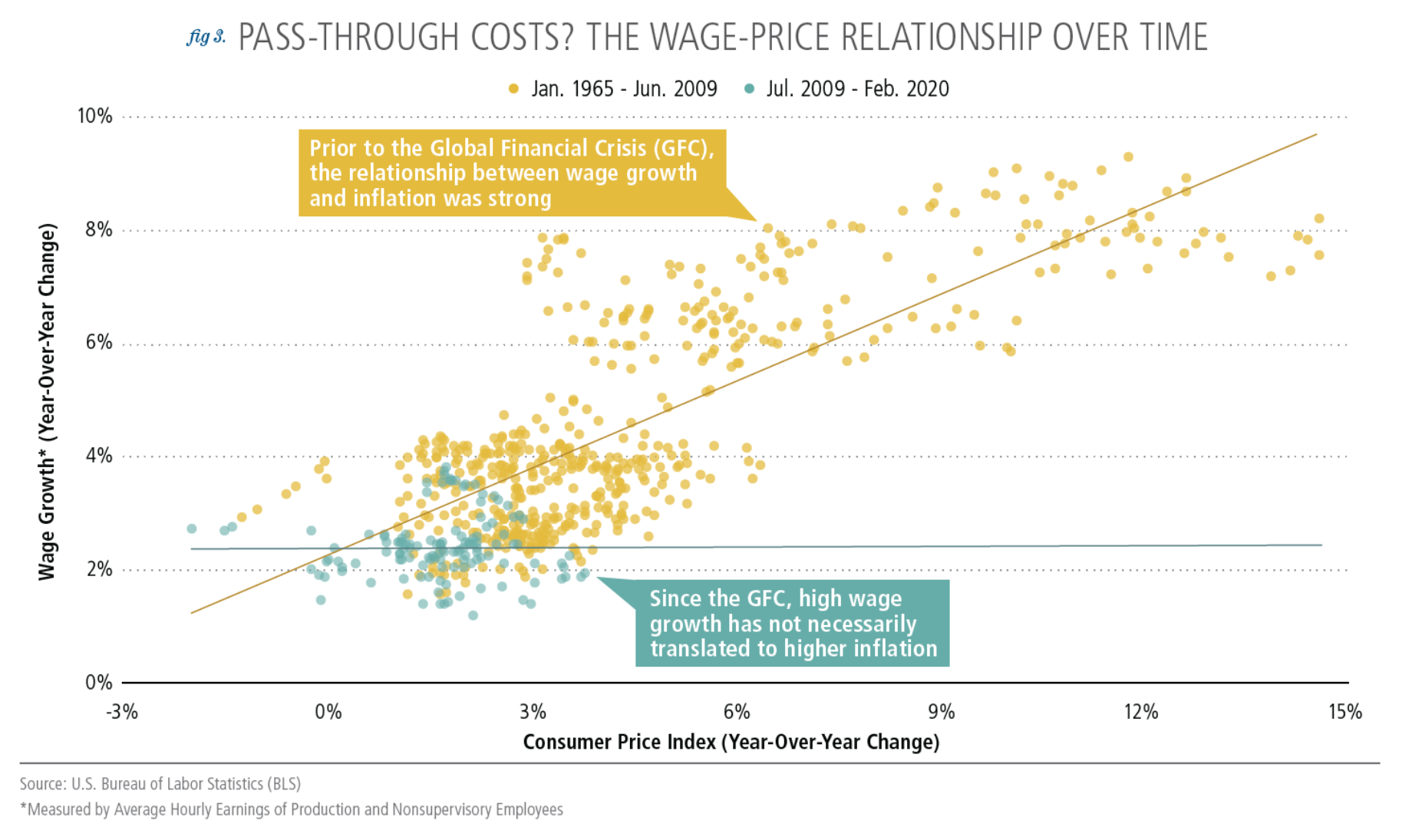

Others may ask, “What about a wage-price spiral due to a shortage of skilled workers?”

First, we doubt there truly is a “labour shortage.”

Despite the headlines about how specific industries are having difficulty finding enough workers, there were roughly 6.9 million unemployed people as of November 2021. Many of the hiccups in hiring are, in fact, more likely due to the unprecedented closing and reopening of the US economy and lingering fears about Covid-19 than they are to a chronic labour supply issue.

Second, wages do not appear to cause inflation (see Figure 3). Why would that be? Well, wages are not an input in the most common measure of inflation, CPI, because they are not a consumer good. Instead, wages are an issue for producers.

Unfortunately for producers, while they might face higher wage pressures, they can’t always pass on the cost of higher wages to customers in the form of higher prices. Higher input costs do have an impact, however, because they might eat away at profits in the short run and force firms to find ways to be more productive without adding labour in the long run.

Ultimately, inflation is a tricky concept and a lot more complicated than you might think at first glance. So, before your passions spill over into heated debate, take a step back and realise that when some people use the word “inflation,” they mean “higher prices.”

When prices are on the rise due to a shift in the supply and demand for money, that’s inflation.

When prices rise due to supply-side bottlenecks or a sudden change in consumer behaviour, that’s not inflation. The way we tell the difference, at least in real time, is to consult inflation gauges that sift through the short-term noise (we prefer the Trimmed Mean).

Even though the topic of inflation can be somewhat esoteric, don’t let the oversimplified fear-mongering headlines keep you up at night.

——–