Geo-political tensions and volatility resulting from the more cyclical forces of inflation and tighter monetary conditions will likely keep equity markets volatile throughout 2022. Whilst companies are still generating improving earnings outlooks, we continue to see the de-acceleration in these rates of growth.

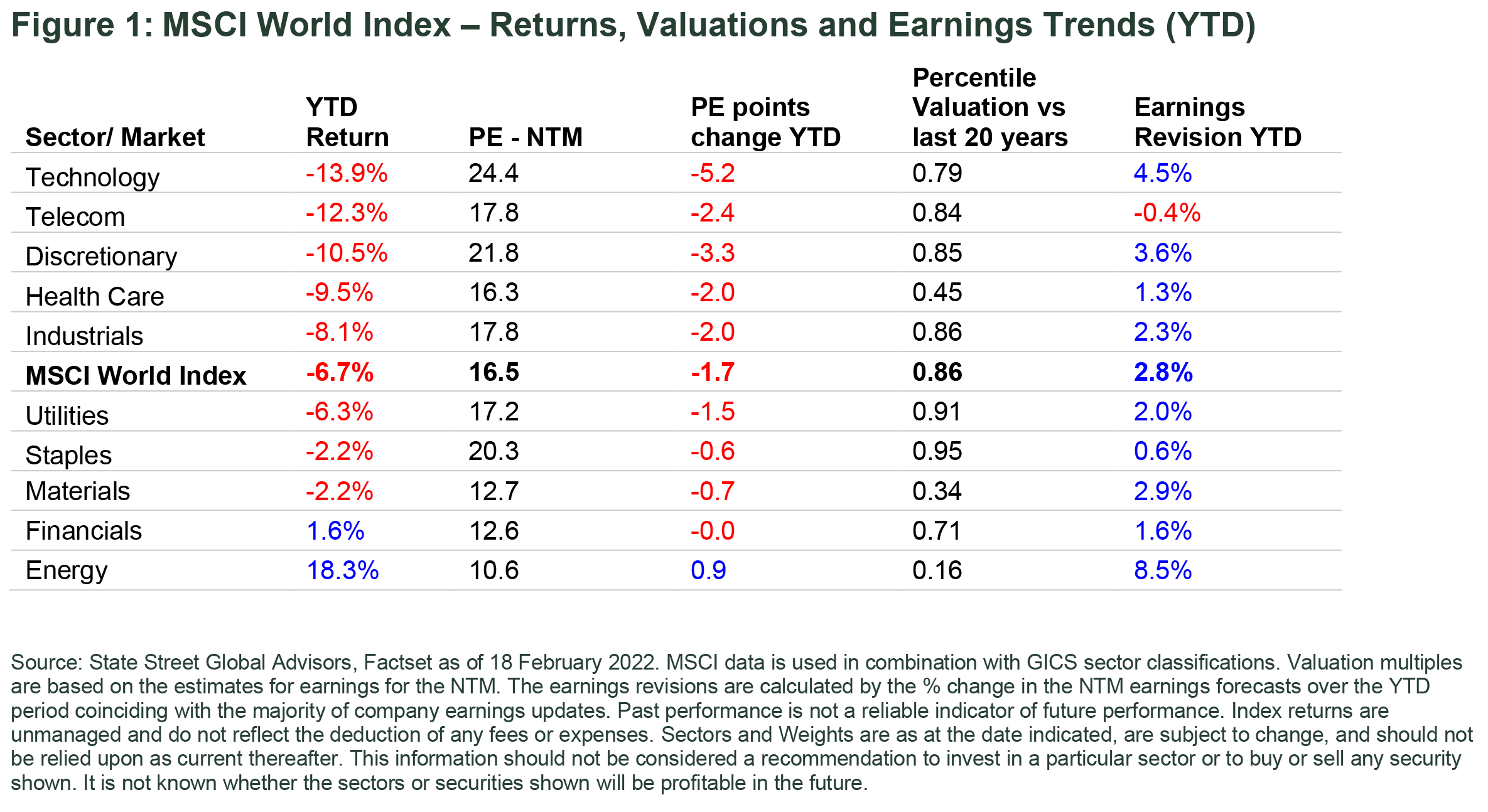

Equity market volatility is proving less transient in 2022. Recent geo-political issues are driving the headlines but beneath the surface the broader equity market has been facing a range of headwinds which are more cyclical in nature.1 As inflation has remained stubbornly high since early 2021, markets are factoring in higher short term rates which is negatively impacting expected growth, corporate profits, equity valuations and investor risk tolerance. Since the 31st December 2021 we have seen the MSCI World Index correct by -6.7% and the earnings multiple derate from 18.2x to 16.5x. At 16.5 times it still ranks at the 86th percentile verses the last 20 years. So still on the expensive side of history.

Within the MSCI World Index we are observing the least profitable parts of the market de-rate the most. Figure 1 below highlights the Technology and Consumer Discretionary sectors have de-rated the most year to date (YTD), yet still remain at historically high levels of valuation compared to the last 20 years. Energy has been the standout performing sector, directly benefiting from the geo-political situation and the rising oil price. The longer oil prices remain elevated the sooner we will see additional supply come online. Ultimately a supply side response would be expected to take the pressure off higher oil prices. Financials and materials have also faired reasonably well, benefitting from improving global growth and less demanding valuations. Healthcare, Materials and Energy rank as the cheapest sectors within the MSCI World Index when comparing their current earnings multiple to the last 20 years.

Figure 1 highlights the YTD earnings revision. Almost all sectors witnessed an increase in the expectations for earnings post the global company reports and guidance updates over January and February 2022. Whilst companies are still generating improving earnings outlooks, we continue to see the de-acceleration in these rates of growth. Back in August 2021 we pointed to the likely peak in earnings growth and indeed this appears to have come to pass. As at 26th June 2021 the 12 month % change in EPS for the next 12 months (NTM) was 40.4% and as at the 18th of February it was 24%. Rolling 12 month MSCI World returns have declined from 37% to 5.5% over the same period.

The Bottom Line Equity market volatility is likely to remain a feature of 2022. If geo-political tensions are resolved we will likely see a reversal of the YTD trends but the volatility resulting from the more cyclical forces of inflation and tighter monetary conditions are likely to remain. Earnings growth while positive is still deaccelerating and may not be enough to see the broader market re-rate.

By Bruce Apted, Head of Portfolio Management – Australia Active Quantitative Equities