Carpe Diem – The time is right to start your own risk advice renaissance

Advisers that leverage opportunities can make life insurance advice a sustainable part of their practice.

The opportunity

One of the more notable aspects of the recent and substantial decline in adviser numbers has been the disproportionately large reduction in risk specialists. Investment Trends data[1] from the end of 2019 showed the proportion of advisers classed as risk specialists (for whom life insurance accounts for 50% or more of all revenues) had decreased from 34% to just 15%.

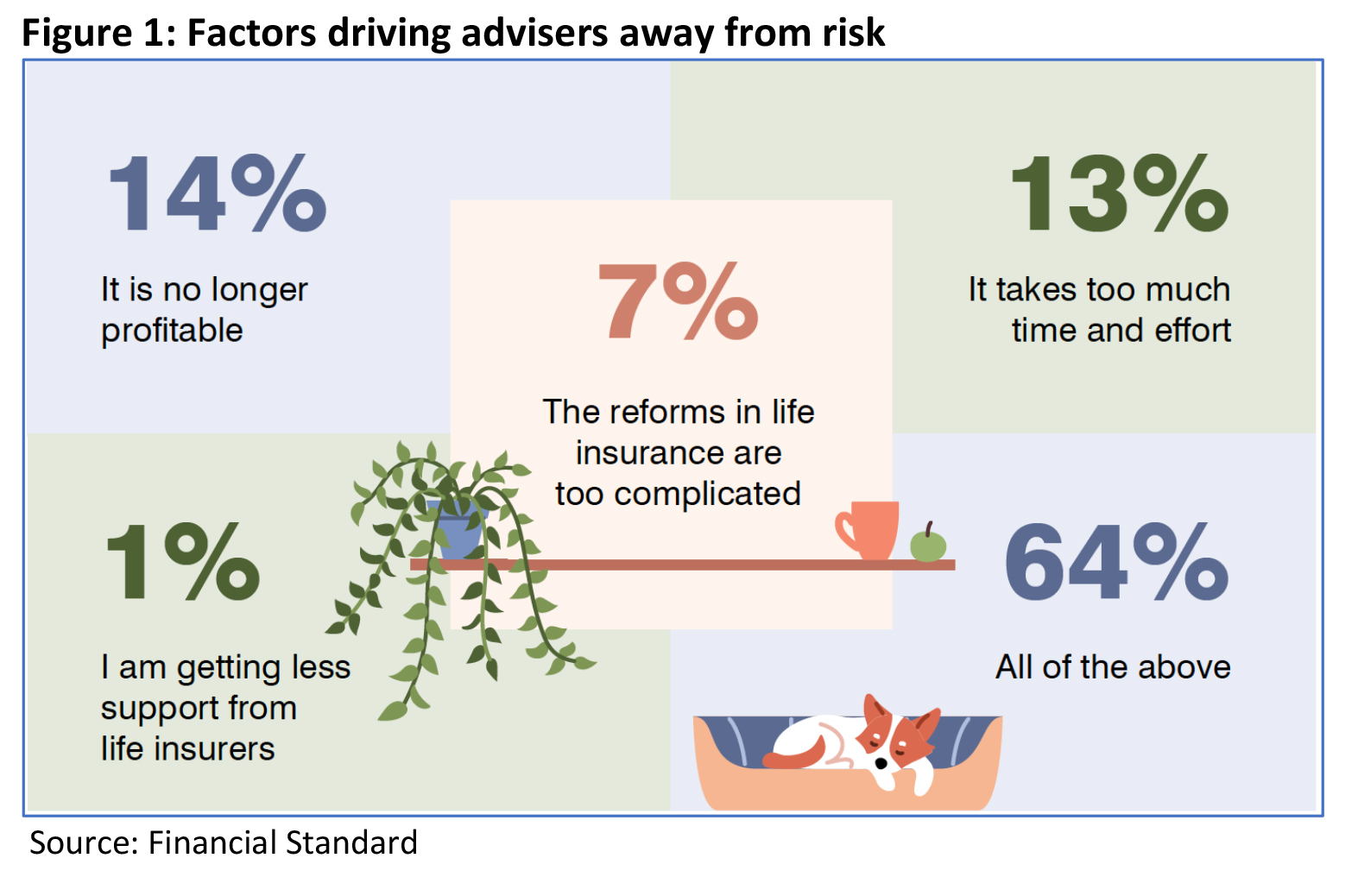

Recent research[2], shown in Figure 1 below, suggests a number of factors have driven this trend, chief amongst them the remuneration caps mandated under the LIF reforms, and the mounting compliance burden (including new professional development requirements).

But whilst these ‘grey clouds’ may be real, there are many silver linings to be found.

For starters, retail life insurance sales seem to have turned a corner, with Plan for Life data[3] released in March 2022 suggesting retail life insurance had started to experience modest growth after several years of contraction.

Furthermore, the large sales declines that have grabbed the headlines in recent times are – in all likelihood – mainly attributable to the introduction of the PYS and PMIF changes to group life cover, which saw under 25s move to an ‘opt-in’ system and low balance or ‘inactive’ super funds having their insurance ceased.

Perhaps most importantly though, the fundamental drivers of demand for life insurance are as strong as ever: people are still taking out mortgages and having children, and advisers remain their preferred source of information about life insurance products.

It is also worth noting that in the aftermath of the post- Hayne crackdown on anti-hawking, and the introduction of DDO regime in October 2021, many direct life insurers have either pruned their offerings right back, or withdrawn from the market altogether, further drying up options for consumers.

Whichever way you look at it, shrinking supply coupled with constant or growing demand creates a gap.

And a gap means opportunity.

Seizing the opportunity with confidence

There are of course many paths to seizing this opportunity. For some advisers this will look like strengthening risk credentials within an overall holistic advice practice, for others it may been bringing previously outsourced life insurance advice in house. Some may even choose to become a risk specialist themselves, as Melbourne Adviser Phil Thompson did when he transitioned his practice from the holistic Thompson Financial Services to 100% risk specialist Skye.com.au (For the record, Phil says he hasn’t looked back!).

But whilst the paths to capitalising on this opportunity may be varied, the success factors are the same. This is an opportunity that must be seized with confidence, and the foundations of that confidence can be found in 5 key areas:

- understanding the role of life insurance within financial advice

- operating efficiently – in engagement and process

- building Client relationship skills

- knowing your product, and

- taking advantage of communities and freebies.

Understand the role of life insurance within financial advice

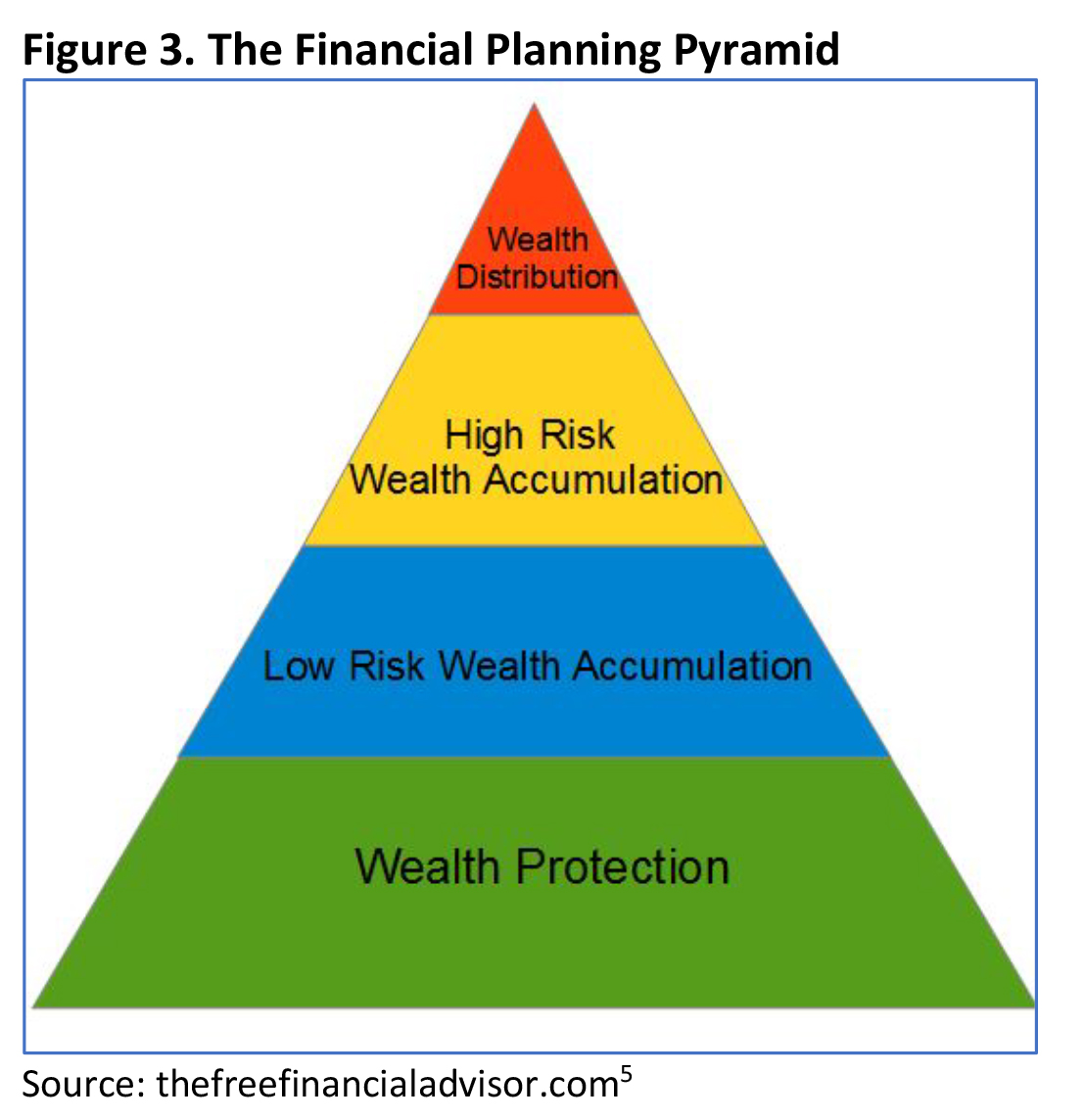

Most conceptual models of financial planning have protection, or life insurance, as one of the foundational elements – to be put in place before more advanced goals are tackled (as shown in Figure 3.) This is intuitively sensible, as the ability to earn an income is central to the ability to build wealth. Conversely the interruption of one’s ability to earn an income can bring even the best laid wealth accumulation plans unstuck.

Recognising this role is crucial in a number of respects.

Firstly, there is no question of life insurance advice being less important than advice relating to tax or investing. Quite the opposite. It is the advice without everything else can fall apart, and as such should be an advice priority for all clients.

Secondly, sharing an equally foundational role in the advice hierarchy is cash flow and budgeting, and there is no doubt that insurance and cash flow planning go hand in hand. It is this nexus which creates the opportunity for risk advice to be offered to a broader, younger, target audience. In a way, advice around cash flow and life insurance can be seen as an entry point to advice, helping build a pipeline of clients who will transition to more sophisticated advice needs as their income and asset base grows.

Nor is the demand for risk advice limited to tradies or young families with simple needs.

Strengthening your life insurance proposition can take you into a number of related markets, all of which come with the opportunity to deal with more sophisticated, challenging, revenue generating scenarios.

These related fields include:

- estate planning

- claims advocacy, and

- keyman, business succession, buy/sell and SME clients.

And of course, knowing that some advisers will always choose to outsource life insurance advice, building your own credentials may open up the opportunity to build referral partnerships with more practices.

Efficiency – in engagement and process – is critical

Against a backdrop of rising compliance costs, a mantra of efficiency has understandably permeated many advice narratives. And risk advice is no different. But of course, driving efficiencies without compromising the client experience isn’t purely a technological play. (although there is no doubt that RegTech has an increasingly important role to play here).

Field underwriting and pre-assessments

In the context of life insurance advice, efficiency can be driven by investing in pre-work, in the form of field underwriting and pre-assessments, which can minimise surprises and thus minimise the rework that often accompanies unexpected underwriting outcomes.

In simple terms, field underwriting is gathering enough information about the life insured to be able to determine their insurability before they actually apply for cover.

This generally means understanding whether there are elements of their health, occupation, family history, or other circumstances which could impact the willingness of an insurer to offer cover on standard terms.

Successful field underwriting therefore relies on an understanding of the client’s circumstances and the underwriting approach of the insurer, bridged by a base level of understanding of medical terminology and medical conditions.

Having this understanding enables you to make a judgement of your client’s insurability before they even apply, which can help you narrow down your selection of suitable insurers.

Knowing which health conditions are likely to attract a loading or exclusion is also important, as it will help you set client expectations from the outset. Understanding how loadings and exclusions work, and in the circumstances in which their removal can be requested, it also important.

Pre-assessments go hand in hand with field underwriting and involve getting an indicative sense of how a client is likely to be underwritten by an insurer. This can allow you to narrow down your choice of insurers as well as indicate those aspects of your client’s situation which may require more clarification and information gathering. Pre-assessments can therefore improve your efficiency as well as manage your client expectations.

Essential to a smooth process is honesty and openness on the part of your client, and this means your pre-assessment information gathering needs to be rigorous. In this sense the level of detail sought by insurers in their personal statements and – where applicable – their supplementary questionnaires, is a good benchmark.

RegTech as an efficiency driver

The remuneration caps in life insurance elevate the importance of efficiency in this space, and compliance processes – and their associated costs – are an obvious area of focus.

RegTech (regulatory technology) is a rapidly developing area, and the scale of customer data and regulatory complexity of financial services has seen the sector become one of the earliest adopters of RegTech solutions. RegTech can be both high tech (Artificial Intelligence, Machine learning, voice recognition) and low tech (digitised data, forms, and transactions).

But while many advisers have acknowledged the opportunity for technology to improve both the accuracy and efficiency of compliance processes, there is still a gap between words and action, with a relatively recent study finding only a third of advisers were using an online fact find and risk profiling tool[6].

Putting aside the debate in some quarters about whether scaled advice is feasible under FASEA, Life insurance advice does lend itself more easily to advice of a more limited scope, which can have clear efficiency benefits. RegTech could well be the tool that gives more advisers the confidence to unlock those benefits.

Building client relationship skills

The extent to which advice clients place more importance on soft skills over technical knowledge is well documented. Arguably this is more important in life insurance advice, where deeply personal discussions about health, income, lifestyle, and family relationships are central to the advice process.

As well as paying attention to your communication and interpersonal skills, an understanding of the way humans think – their reliance on mental short cuts or heuristics – can be especially important, particularly in the context of an intangible product such as insurance (a product nobody hopes to claim on).

Humans rely on these mental shortcuts, identified through the study of behavioural science, to help us make decisions amongst the deluge of data our brains process each day. Understanding how biases work can help advisers tap into the clients thought processes more quickly and tailor their approach to drive more clarity and more informed choices.

Anchoring, loss aversion, overconfidence, and overvaluing the present and discounting the future are all common biases that advisers should understand and adjust for.

Perhaps one of the most relevant heuristics in an insurance context however is ‘availability’. The availability heuristic is a mental shortcut that relies on immediate examples that come to mind when evaluating a specific topic or decision. Under this short cut people tend to place more importance on the most recent – available – information they have received.

It is easy to see how this may impact decisions we make around financial matters, such as insurance. Rather than your client rationally assessing risks and probabilities, they are more likely to be influenced by an event that they have become aware of, through the news, or because a friend or family member has been affected. This is why we see sales of home insurance increase after a flood, and people seek life insurance after the death or illness of someone they know. The actual risk of them actually suffering that event hasn’t changed, it’s just that they are more aware of it[7].

In this context, one of the most powerful ways to frame the importance of insurance is to ask the client whether they know any loved ones, relatives, friends, or colleagues who have suffered a serious illness or accident, or worse. (Unfortunately, the odds are extremely high that the answer to this is yes). Tapping into these memories can be far more powerful in making the risks real than pages and pages of statistics around the odds of death or disablement.

Of course, the downside of this effect is that, as their memory of the event fades, the value placed on that insurance is diminished[8] in their minds. After a few claim-free years, people may start to question the value of that cover. In such a situation, advisers should seek to increase the ‘availability’ of the risk, by drawing on news and examples (e.g., real life claims stories) that remind people of the risks and their consequences.

Whilst soft skills are typically developed ‘on the job’ and are honed with experience, many advisers highlight the value of mentors and peer communities, as well as the dedicated courses training programs available.

Know your product

Notwithstanding the overwhelming importance of soft skills – a point applicable to all types of advice – life insurance is technically demanding, with complexity to be found in areas such as underwriting, product features and definitions, and structuring.

Regardless of whether you aim to specialise in risk, or it is just one component of your overall advice offering, building technical strength is therefore crucial.

This includes becoming familiar with the nuances of different products, the way different insurers view certain health conditions and occupations, and the design of legacy offerings (increasingly important since the IDII intervention).

Fortunately, many life insurance providers, including Zurich, offer resources through various channels to help advisers to build this strength, including BDM support, comprehensive face to face and virtual educational programs and PD Day presentations.

Zurich’s _ZONE includes over 70 hours of CPD content across 5 ‘zones’, covering topics such as client engagement, retention, marketing, innovation, soft skills, and leadership.

Other resources leading risk specialists rely on include the claims data published by ASIC, which shows differences between insurers and products, and the more detailed breakdowns published by many insurers.

It should also go without saying that risk researcher software, available for a relatively modest cost, is a must have.

Put simply, the sheer volume and complexity of life insurance products makes the modest cost of a subscription to risk research software an investment that will pay immediate dividends. As well as the obvious efficiency savings in product comparisons across multiple criteria (including premium rates), there are often other useful resources to be found within them, including data on claims rates and statistics around the likelihood of suffering various health conditions.

Communities and Freebies

Whether you are looking for tips on developing your bedside manner, you’ve got an unusually complicated client scenario to deal with, or you just need a second opinion on your approach to a particular topic, peer networks and communities can be invaluable. This is especially so for those advisers in smaller practices, and those who don’t yet have a wide range of experiences to draw on – perhaps because they are new to the profession, or the risk aspect of their practice is still small or in its infancy.

No matter what your issue, chances are someone has been there, done that, and got the t-shirt.

There are a number of communities advisers can become a part of, including communities within their own licensee, region, or professional association, broader communities such as XY Adviser, or dedicated life insurance communities such as MDRT or online groups like My Risk Adviser (a members only Facebook community with 1400 members), or the Australian Risk Advisers Group on LinkedIn (3500 members).

Everyone also loves a ‘freebie’ and advisers should avail themselves of the mountain of free, risk specific resources available, including the training, marketing and technical support offered by many insurers, invitations to professional development sessions and industry events (become friendly with a few BDMs!), and online content – including that with CPD attached – offered by many publications (including this one).

Summary

Shifting industry dynamics have seen the opportunity to make risk advice a viable part of your offering bigger than ever before. With the right focus, and by leveraging the resources available, advisers can confidently deliver life insurance advice in a way that is highly sustainable, enabling them to create ‘advice readiness’ amongst a much broader range of client segments.

![]()