Client onboarding – the best kept secrets of leading advisers

Client onboarding processes are a pain point for both clients and advisers, being slow, error prone, and costly.

The introduction to a 2016 paper by global consulting firm KPMG, Transforming Client Onboarding[1], contained the following observation:

“Client onboarding is a largely manual, error prone, time -consuming, incomplete process. It often aggravates consumers and financial firms alike.”

Fast forward to financial advice in 2022 and this statement still holds true.

Which is problematic, on two fronts.

Firstly, the onboarding process is the first opportunity to deliver a seamless customer experience – consistent with contemporary consumer expectations – and demonstrate value before the benefits of your advice have started to flow through. As such, it can make or break the client relationship.

Secondly, client onboarding has traditionally been a costly and highly resource intensive process. Improving the efficiency of the onboarding process can therefore have a dramatic effect on the cost to serve, and in turn the overall sustainability of the practice.

Conversely, the risks of getting it wrong are substantial:

- unhappy clients, who may drop out of the process or switch advisers

- clients will be more reluctant to provide referrals

- clients may not appreciate your full value proposition and breadth of offering

- time is wasted with prospects not suited to your practice

- misalignment between service expectations on the client’s part and delivery on your part (resulting in under or over servicing)

- lower staff engagement.

For too long, onboarding has been dismissed as a back-office function, a compliance focussed ‘necessary evil’, tangential to a positive customer experience.

At a time when 100,000 advice clients have exited the sector in the last 12 months alone[2], the impact of onboarding on both client satisfaction and the cost of advice should arguably make it one of the top business priorities for advice practices around Australia.

Don’t take client loyalty for granted

There’s a long-standing narrative within advice that non advised consumers start off as ambivalent towards the value of advice, but are delighted once they get it. And it is certainly true that advice clients on the whole demonstrate high levels of satisfaction.

Three quarters of respondents to a recent study[3] of Australian advice clients said the advice had improved their financial wellbeing. 88.5% said the advice had given them greater peace of mind financially, and 86.2% said it had given them greater control over their financial situation.

But is it the adviser or the advice itself that customers are attributing the value to, and what does this mean for their loyalty to an individual adviser?

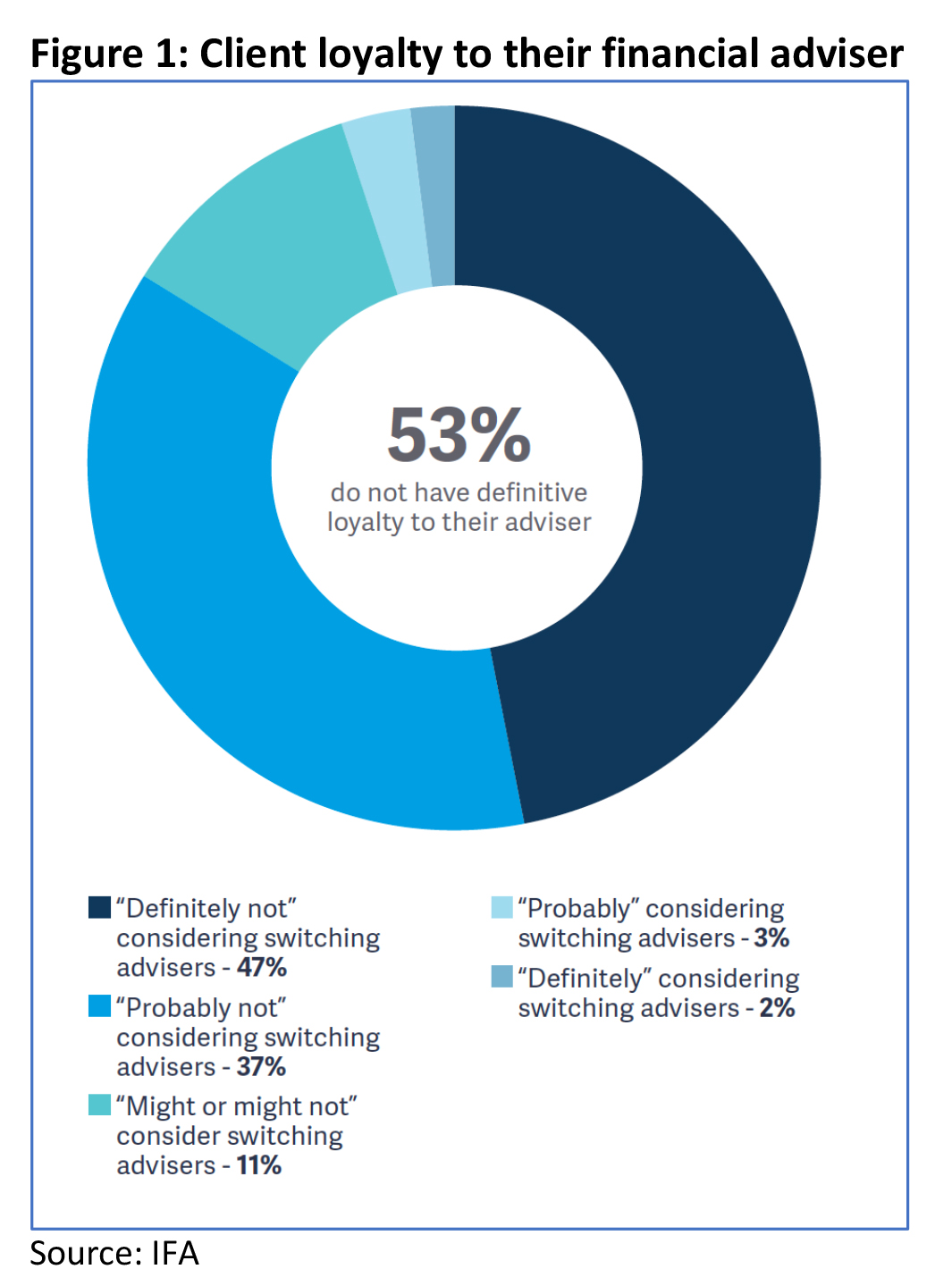

IFA research found that whilst client satisfaction levels with their advisers are high, loyalty isn’t widespread.

Ninety-four per cent of advice clients surveyed[4] said they were satisfied with their financial adviser. However, 53 per cent of advice clients said they don’t have a definitive loyalty to their adviser. There was also a weak link between greater rates of loyalty and longer relationships, with advice/client relationship greater than 10 years being surprisingly vulnerable.

The same study also found that around 50 per cent of advice clients don’t have total clarity on what their fees are paying for – hardly a recipe for a successful relationship.

Just as damaging can be drop-out rates – those clients who get part way through the onboarding process and just pull out in sheer frustration with the volume of touchpoints and paperwork. According to Adviser Ratings[5], around 50 per cent of potential clients drop out during the onboarding process if it’s a cold lead, and the average adviser loses 25 per cent if it’s a warm lead.

Even those who pay for comprehensive financial plans don’t necessarily go ahead with them. One US study found[6] that more than half the clients receiving a financial plan had only implemented 20% or less of the recommendations!

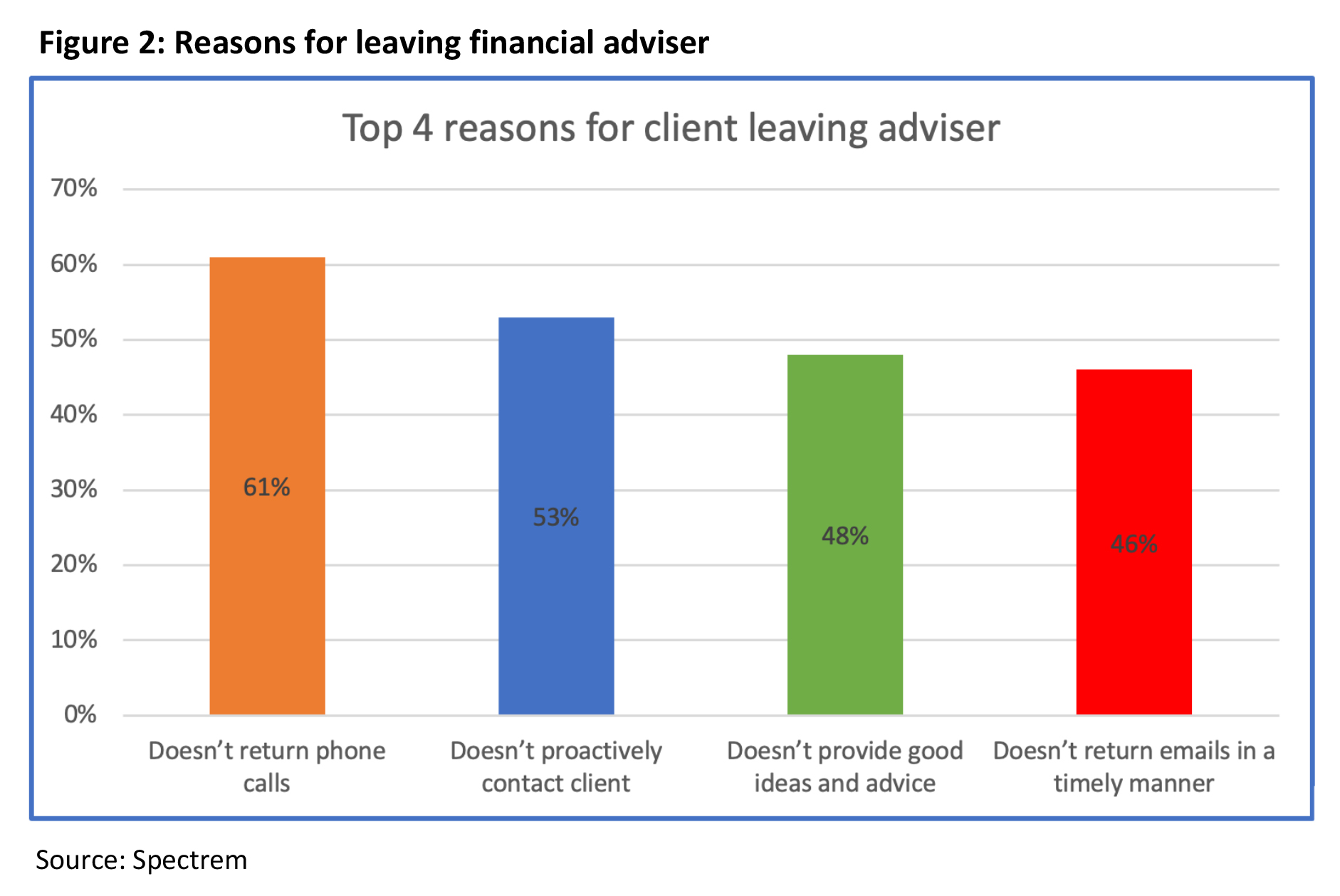

It’s poor service that drives them away

A Spectrem Group study[7] of financial advice clients with $1 – $5 million in assets found that three of the four most highly cited reasons for leaving their adviser were communication related:

Qualtrics research[8] also found that two of the top three reasons for client defections were service related, a finding consistent with studies into other sectors within financial services. The KPMG paper referenced above, for example, found that 89% of customers who switched financial providers did so because of a poor service experience.

All of this matters because the impact of client loyalty on the financial sustainability of a practice is substantial.

Just a 5% reduction in client attrition rates can boost profitability by up to 95%[9]. Ponder that!

The advice service experience is front loaded

Financial advice and financial planning client experiences are inherently front loaded. The bulk of the work is done upfront – fact finding, developing plans, implementing strategies. This is when a lot of client interactions take place and money changes hands. But the value derived from those plans and strategies doesn’t become apparent until well into the future – meaning in the short term, when your relationship is still in its formative stages, your onboarding experience is the only tangible way by which they can judge you. And that makes it super important.

Onboarding can be expensive

Onboarding can be one of the most resource intensive – and thus expensive – processes across an entire financial services business. Major banks literally spend hundreds of millions of dollars on it. Financial advice practices too spend serious time and money on onboarding – especially those who are largely still treating it as a manual, analogue process – scanning, printing, emailing, posting etc.

According to Coredata[10], it typically takes about three months from an adviser first meeting a prospect to them becoming a new client (the point when they are invoiced). Small firms tend to take a bit longer to onboard a new client – around a quarter of them take three months or longer, compared to about 15 per cent of medium firms and 13 per cent of large firms.

And costs are going up too, mostly as a result of increased regulatory requirements – some imposed by the actual law itself and some imposed by specific licensees. More than two-thirds of large practices say costs have increased “a lot” in the past three years, compared to about 56 per cent of medium firms and less than half of small firms.

By the time drop-out rates are factored in, the real costs of onboarding are skyrocketing, in many cases turning the initial provision of advice into a loss-making proposition. Research conducted by KPMG[11], and commissioned by the Financial Services Council, found the average cost of providing comprehensive financial planning advice is $5335 a client, vastly exceeding the average cost charged to consumers of $3660. The Coredata study[12] reinforces this, finding that no more than half of advice practices of any size charge a fee for initial advice that covers the cost of onboarding a new client. Fifty per cent of large firms say they cover the cost, along with 47.5 per cent of medium firms and 46.4 per cent of small firms.

So where does onboarding wrong?

There is no single, simple answer to this question, although it is fair to say that automation can make a quantum improvement in both client and financial metrics. Whilst some practices have nailed their onboarding strategy and processes, most probably have opportunities to improve in some, if not all, of the following areas.

Lack of clarity in target client

Leading advisers are selective in who they take on as clients, applying a range of criteria to determine if the relationship is likely to be sustainable. Ability to pay fees is not, in itself, an indicator of likely relationship strength. Not being clear and disciplined in the type of clients you want to take on, and not having robust processes to check this alignment before you even meet, can see a lot of costly effort wasted.

Inconsistent, undocumented onboarding experiences delivered by too many people

A study[13] of Australian advice practices revealed that only 40% of practices have a formal, documented onboarding process, whilst three quarters had multiple people involved in the onboarding process. That spells out a lot of opportunities for different people to deliver a different experience. This inconsistency can be frustrating for the client and cause staff members to feel anxious because they lack guidance.

Processes are not based on customer feedback

Advisers are not always good at seeking formal client feedback. Indeed, 2019 research[14] suggests less than one in three advisers seek such feedback with any formality or regularity. Without that feedback, advisers are flying blind on which aspects of the process clients actually like and derive value from, and which aspects represent pain points.

Believing onboarding begins once the client has agreed to go ahead

Nearly half of advisers[15] believe that onboarding begins once the client has committed to having an SOA prepared, or later. But from a client’s perspective, they are experiencing and judging your service offering much, much sooner. Certainly, from the very first appointment, possibly even from the first time they land at your website. Not allocating as much importance to the client experience in these areas will ultimately be costly.

Too slow, and not omnichannel

Consumer expectations are increasing all the time. Clients are comparing your experience not with other financial providers, but with technology, retail, and travel brands. They expect onboarding to be simple, paperless and fast. An omnichannel experience – where clients can engage with you and your process across different channels, including online and mobile, at different times – isn’t just a nice-to-have, it’s become a non-negotiable. 7 out of 10 ‘advisable Australians’ say a firm’s digital capabilities are critical to a positive client experience[16].

Too manual, not automated enough

Related to the above, the failure to automate is leading to practices compromising their client experience and compliance, whilst leaving efficiency opportunities on the table. In the US, a survey of 140 financial planning businesses employing 21,000 advisers revealed that advisers were spending 43 days a year on onboarding tasks that could be automated, representing an average of 13 hours per case.[17] (This study also found that 5% of onboarding steps account for a staggering 50% of time and cost). And yet despite this, only around one third of advisers are currently using an online fact find and risk profiling tool[18], and more than 40% don’t use digital signature tools[19].

Steps to getting it right

Getting onboarding right can do wonders for your client experience and practice economics. Here are a few steps you can take to make that a reality.

Take a step back

The experience demanded by millennials will differ to that optimised for high worth pre retirees. In order to align the onboarding process to your value proposition and ideal client, you first need to have clarity around what you want to stand for, and to whom.

Map out your current process

Take the time to write down every aspect of your onboarding process, including all steps, in order, the time taken to do them, and who is involved. Seeing this all mapped out will make it easy to work out the true cost of your process and identify opportunities for streamlining.

Seek feedback

Ask your clients which parts they love and which parts they don’t. You can do this via formal or informal means, but make sure they are honest about where they see value and where they see inconvenience and delay.

Co-create the new process with your team (and with clients)

As your client onboarding process should be a team effort that involves your client interacting with more than just the lead adviser, the process should be jointly defined by a cross-functional team of representatives from each of the client facing functions. The more your client has a relationship across your practice rather than just with you, the less ‘single point dependency’ you have, and the easier it becomes to offer clients first call resolution.

Furthermore, rather than just asking clients what they think about your old process, get them involved in designing the new one. If you have a client advisory board, then this is a perfect opportunity to put them to work!

Rigorously screen unsuitable clients out as early as possible

Minimise time wasted by you and them. Pre-screening is crucial and lends itself to a checklist or questionnaire, which can be online or offline.

Aim to make your process differentiated, engaging and memorable

If onboarding was renamed ‘brand launching’ you may approach it differently, and yet this is exactly what it is, your chance to shine and stand apart.

Put yourself in the clients’ shoes

Your client isn’t a financial expert; that’s why they need an adviser. The complexity of financial products can be overwhelming, as can the various documents, statements, and requests for information. Put yourself in their shoes and work on the basis that they have no knowledge of the content, chronology, or significance of each step of the product issue process.

Life insurance in particular can be fraught, especially if a client has been issued cover with exclusions or loadings. If they receive documents with lengthy exclusions which they don’t understand, it can undo all your hard work and assurances, so get on the front foot in explaining things to them.

When speaking with clients, avoid using industry jargon and acronyms without first providing an explanation of the meaning. And remember that as various PIN numbers and logins etc are generated and sent to clients, they may be a bit overwhelmed, so make sure you take the time to explain all this.

Ensure the process can be tailored where appropriate

It’s hard to make one process satisfy every single customer, so build in the ability to tailor some aspects. For example, communication is not a one-size-fits all proposition. No matter how closely your clients all fit into your picture of the ideal client for your business, their communication preferences may differ greatly. What works for one client may not be even remotely suitable for another. Some clients may like to hear from you more often than others, some as little as possible. For some, emails, texts, or even direct messaging through social media, might be preferred, while others may prefer a quick (or long) phone call or meeting to review the details and ask questions. Remembering this, your onboarding process must be flexible enough to treat each client as the individual they are. Establish and make a record of your client’s preferences early in the process. And make sure you ask rather than assume (there are plenty of retirees who prefer digital communication and Gen Y’ers who want face-to-face meetings).

Establish accountability and responsibility across your team

Allocate ownership of (and accountability for) the various steps in the process to the most appropriate individuals within your business. Certainly, it is unlikely that having the lead adviser steer the client through the entire process is a sensible use of their time, as good as it may seem for the client.

Appropriateness can be based on many criteria, such as special expertise, client value, existing relationships etc. The onboarding process is actually the perfect time to showcase the breadth of your offering and to build confidence in the abilities of your wider team – think of it as business continuity (or “if I get hit by a bus”) insurance that you’ve actively created a positive relationship and level of trust between your clients and your wider business.

Digitise and automate

Arguably the biggest single step an adviser can take is to automate and digitise their onboarding approach. In one fell swoop, it is possible to improve client satisfaction, make onboarding quicker and cheaper, and reduce duplication and errors.

Australian research has shown that advisers using digital tools – including e-signatures, online fact finds, and video meetings – are achieving higher growth, better client engagement, and more scalability than those who don’t. (The efficiency saving from online fact finds alone is estimated at 65%[20]).

Don’t be tempted to revert to face-to-face meetings as things start to ‘normalise’ after COVID. From a client’s perspective, online meetings are more convenient and less stressful, even for older clients. Having to get dressed up, remember to bring the right documents, and factor in travel and parking time can make clients quite anxious ahead of a face-to-face adviser meeting, which can contribute to meetings being cancelled or not as productive as they could be.

And nor do virtual meetings create a barrier to emotional connection. A US study[21] found that the lower barriers to entry of virtual meetings (both emotional and logistical) can actually make them more effective than physical meetings in addressing the client’s emotional needs.

From an adviser perspective, there is now the flexibility to hold meetings from non-office locations, outside traditional hours, and without the normal support staff that may be needed in an offline world.

To the extent that people expect – and even prefer – virtual meetings to be shorter and more focused, advisers can engage with more clients on any given day, and increase the frequency of contact: for example, exchanging a 60-minute quarterly meeting to monthly meetings of 20 minutes each (which may be more useful at keeping the client on track).

Shorter virtual meetings will also reduce frequency of clients cancelling meetings at short notice due to sick children, inclement weather, or transport woes. If the meeting involves them staying at home, those excuses disappear!

Don’t forget the training

Having taken the time to reinvent your onboarding process, make sure that everyone in the business is up to speed on the new protocols and processes, and has the necessary skills to perform their part.

This may involve specific training or e-training of some staff with regard to putting the processes into practice, training around better ways to converse/interact with clients (especially for staff new to client facing aspects who would have traditionally been considered back-office staff), or the use of new technology.

Track and measure the process

Just as with your business, your onboarding process should be constantly evolving – ensuring it remains a point of competitive differentiation. Your process will never evolve

at the rate required if it is not actively tracked, measured, and adjusted accordingly.

Process measurement is an important part of keeping your onboarding process a relevant and distinctive point of differentiation. In addition to surveying the new clients you

bring on board for their personal views, as you build your new onboarding processes, put monitoring systems and measurable KPIs in place that help to identify parts of the process that may not be functioning to the greatest effect.

Metrics to track can include:

- client satisfaction

- timeliness of processes

- Error rates

- compliance metrics

- complaints

- outsourced v insourced turnaround times

- conversion rates and attrition rates

- cost per customer

- adherence to service standards.

Summary

The capacity for the onboarding process to significantly impact client satisfaction, practice profitability and advice compliance makes it arguably the single most important process for an advice practice to focus on. By taking a more client centric approach to designing their onboarding process, and by investing in technology which can automate many aspects of the process, advisers can effectively offer a better onboarding experience, faster, and at lower cost. The resultant impact on practice sustainability can thus be substantial.

——–