Ethics – It’s not all black or white

Ethics underpins professionalism – there are many situations that require subjective judgement that could be considered ‘grey’.

The financial adviser Code of Ethics seeks to impose ethical duties that go above the requirements of the law. While those laws may be clear, anything open to subjective interpretation can be prone to ‘grey’ areas – unfortunately, not everything is black and white or clear cut. In this article, proudly sponsored by GSFM, those grey areas are explored in the context of ethics and financial advice.

It would be so neat if everything was clearly black and white, an evident right or wrong, a strong yes or no. Unfortunately, life is not always quite so straightforward.

The online Macmillan dictionary defines ‘grey area’ as:

‘…a situation in which the rules are not clear, or in which you are not sure what is right or wrong.’

That grey area is one that can’t be so readily categorised as the right or wrong way to act, sitting on a continuum between black and white. From an ethics perspective, the grey area is where right and wrong becomes blurred and generally requires some form of moral judgement. Grey areas become problematic when the process for dealing with them is flawed and can provide wiggle room when coping with ethical dilemmas in organisations[1].

Even in the law, which seeks to eradicate grey areas, there are situations that don’t exactly fall into a specific category; similarly, when examining ethics in a financial practice, it’s important to be aware that this grey area exists. Academic research suggests that all organisations have grey areas where the border between right and wrong behaviour may be blurred; however, this is where a major part of organisational decision-making takes place. While grey areas can be a source of problems for organisations, they can also have benefits[2].

Moral dilemmas

When a situation does not have a clear cut response, it falls on an individual’s morality – or moral compass – to provide guidance. This can be defined as:

‘…a term used in reference to a person’s ability to judge what is right and wrong and act accordingly.’

However, morality itself is full of grey areas and each individual’s ‘moral compass’ can be quite different.

According to Kohlberg’s six stages of moral development[3], this begins in childhood at a pre-conventional level where we don’t have a personal code of morality. Instead morality is shaped by the adults around us and the consequences of following or breaking their rules. As children get older, they begin recognising that the different people around them have different viewpoints and there’s not always one ‘correct’ perspective.

As individuals mature, they start to internalise the moral standards of valued adult role models – parents and relatives, teachers and coaches, and increasingly, celebrities and others with a strong media or social media profile. At this stage, reasoning is generally based on the norms of the group to which the person belongs, and individuals often make moral judgements or decisions based on how they perceive others will view them. Often, decisions are actively made to obey the law and avoid feelings of guilt at straying from one’s morality. According to Kohlberg, this level of moral reasoning is as far as most people get. Further, he believes most people take their moral views from those around them; only a minority think through ethical principles for themselves.

For advisers, their moral compass or moral reasoning needs to not simply determine what is right or wrong in a given situation, it must also enable them to decide a course of action that’s for the greater good – or in their best interests of their client. A strong sense of morality can help guide advisers to make good decisions, particularly in those situations that aren’t black or white.

Morals and the Code of Ethics

Ethics problems are not always clear cut. Detailed codes of conduct, such as the financial adviser Code of Ethics, target what is and isn’t acceptable in providing financial advice. It aims to bring clarity to decision making and is used to examine actions when it comes to enforcement.

Despite the existence of the Code of Ethics, you are likely to encounter ethics problems that aren’t definitively black or white, right or wrong, but fall into the grey zone and require professional and moral judgement to resolve.

A study[4] that investigated the effects of codes of ethics on perceptions of ethical behaviour found the presence of a code in businesses improved the organisational climate. It provided:

- support for ethical behaviour

- freedom to act ethically

- greater satisfaction with the outcome of ethical problems

- a positive impact on perceptions of ethical behaviour in organisations.

The financial adviser Code of Ethics was designed to increase public confidence by raising standards for financial advisers. It introduces ethical duties on advisers that go above the requirements in existing law and are designed to encourage and embed higher standards of behaviour and professionalism in the financial advice sector.

The Code of Ethics appropriately places personal responsibility on advisers to understand and apply their professional judgement to their ethical obligations in client engagements so that their professional conduct is focussed on providing advice that is in the best interests of the client[5].

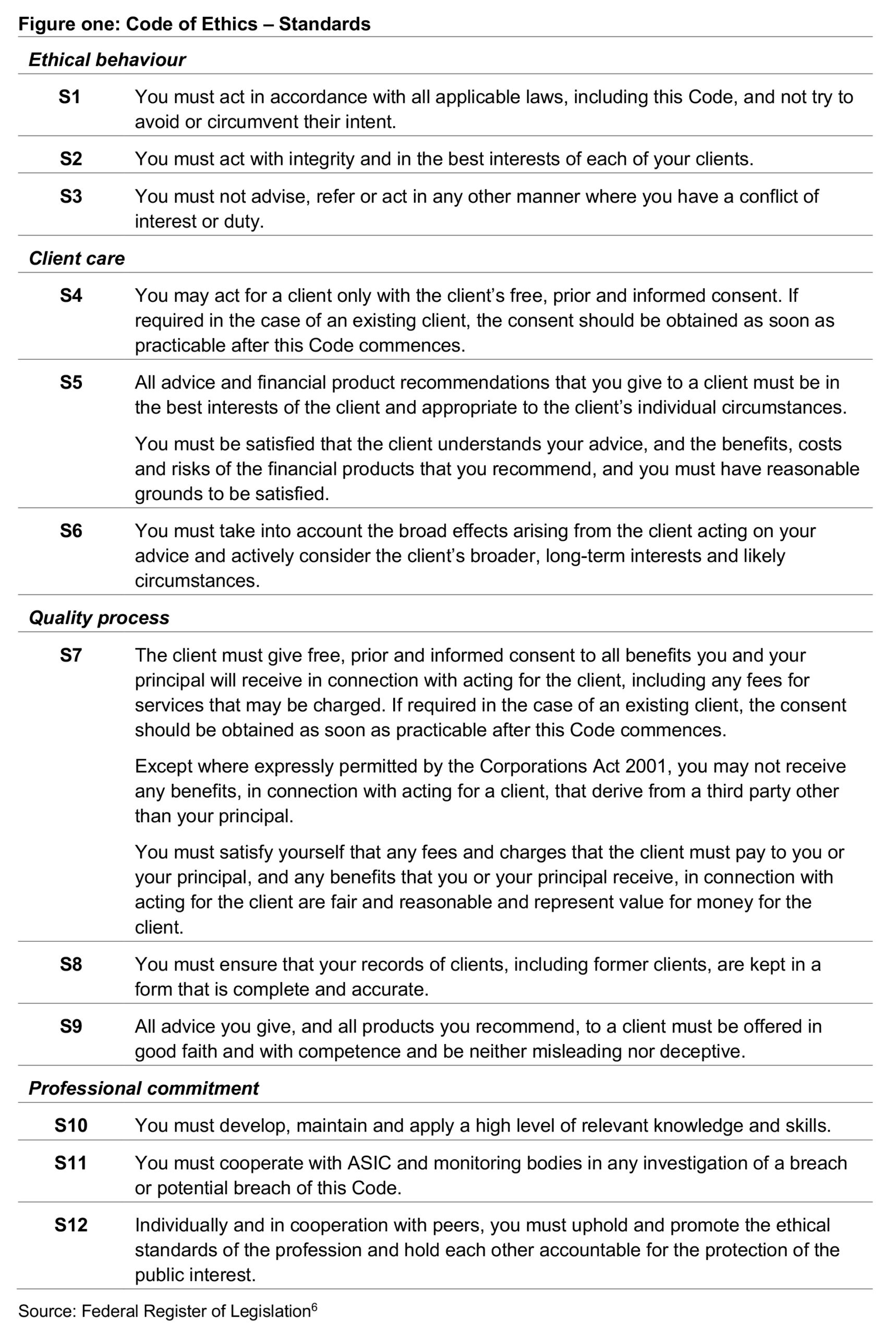

The Code of Ethics requires financial advisers to act in a manner demonstrably consistent with the twelve ethical standards summarised in figure one.

It is acknowledged by regulators that these standards are not intended to provide definitive guidance. Individual circumstances will differ in practice and there is allowance for differences of professional opinion on how the ethical rules of the profession should apply in a particular case. This is where you may encounter the grey zone.

Doing what is right will depend on the particular circumstances and requires you to exercise your professional judgement in the best interests of each of your clients.

Black, white and grey in practice

Ethics plays an important role in your financial practice – it’s not simply how you behave, but how your colleagues and referral partners behave. That’s why it’s important to educate and reaffirm, on a regular basis, the importance of ethical practices in your business.

While ‘grey’ issues often necessitate time and effort for a satisfactory resolution, problem solving around such matters can provide valuable information to your practice and help avoid complications in the future.

You can use these challenges to your benefit. Being aware of the grey zone and using examples and case studies that aren’t black and white provide an excellent opportunity for training and discussion. List the situations your team may encounter in their day-to-day work in staff training sessions, and work through possible options for the best resolution. Being proactive today might prevent development of a significant ethical problem tomorrow.

Importantly, the grey zone is why it’s important all employees of a financial planning business are aligned with its values and practices. You can’t assume everyone in your practice has a highly developed sense of ethics, which is why it is important to educate, restate and reinforce the importance of integrity, values and ethical behaviour as a regular part of your education practices.

If you are transparent about how to deal with ethical issues that aren’t clearly black or white, there’s a lower chance of breaching the Code of Ethics and, therefore, less likelihood of facing enforcement action.

Some unethical behaviours are obvious and (relatively) easy to deal with:

- abusive, coercive or intimidating behaviour toward clients, staff or third parties

- discrimination or harassment

- theft, fraud or receiving kickbacks

- failing to adequately deal with conflicts of interest

- failing to obey the relevant laws and codes that pertain to financial advice.

When you’re looking to set ethical standards in your practice, it’s important to remember that the law is the beginning, not the endpoint. That’s black and white. However, that doesn’t mean there aren’t potential grey areas in financial planning.

An example of this is having possession of inside information.

While everyone knows that insider trading is against the law, there’s a broad range of inside information that can come across an adviser’s path. Examples include:

- an acquaintance working at the local council who happens to mention the reclassification of an area of commercial property to residential zoning

- a client who discusses a significant new contract won or issued by their business

- a friend who bemoans a substantial revenue hit for the listed company they work for and the potential ramifications

- dinner party conversation in which you learn of a major merger between two listed companies

- an event at which a fellow attendee excitedly tells you how close his biotech firm is to a game-changing vaccine.

Having this information isn’t breaking the law. Acting on it for personal gain is. That’s black and white; section 1043A of the Corporations Act 2001 prohibits a person from trading in listed securities while in possession of non-public, price-sensitive information. The ASX regulatory guide explicitly states that Key Management Personnel, employees and family members are not permitted to trade when there is sensitive information not yet publicly disclosed.

Tipping off a property developer client about the pending reclassification of land is in the grey zone. It might not breach the law, but is it ethical?

In most instances, share trading activities based on information you’ve received will breach – or at least skirt very close to – insider trading. While there’s no shortage of people willing to share their stock tips, you need to examine the rationale underpinning the tip. When it arises from information not publicly available, it’s risky to recommend clients buy or sell based on that information.

Case studies

The following case studies are mostly based on real events; however, the names of people and organisations have been changed, and some details altered. The case studies have been drawn from ASIC and the Australian Financial Complaints Authority (AFCA) or its predecessor organisation. For each, potential breaches of the Code of Ethics are identified.

Case study one: SMSF advice

Self-managed superannuation funds (SMSFs) continue to be a popular retirement savings option for many Australians. At 31 December 2021, there were 601,906 funds with 1,129,321 members; in total, these SMSFs held net assets under management of $840,204 million[7].

The decision to establish an SMSF may be client driven or result from advice received from an accountant or other third party. It’s essential to understand the driver and rationale behind the decision, particularly if you are concerned about the appropriateness of an SMSF structure for the client.

Even if a third party has established an SMSF on their behalf and they come to you for investment advice, it’s important to ensure your clients understand their responsibilities as trustees of the SMSF, that they are personally liable for all decisions made by the fund. This includes following any advice you or other service providers give them.

Debbie and Geoff sought financial advice after their accountant recommended the couple establish an SMSF. Debbie has run a successful restaurant for many years, which she plans to sell in 2-3 years, and Geoff holds a senior executive position with an ASX-listed company. He plans to retire around the time the restaurant is sold. Geoff has sizable super savings in a corporate account, whereas Debbie’s retirement savings will result from the sale of her business. The accountant believes they should establish an SMSF now and transfer Geoff’s super balance, followed by the proceeds of the business sale once complete.

The couple meets with financial adviser Helen to get an investment strategy for the SMSF, as well as assistance with the strategy’s implementation. This is Helen’s first meeting with Debbie and Geoff. When she probes them about the SMSF and their roles and responsibilities, she realises they do not understand what’s involved with the ongoing management of an SMSF.

Helen explained their responsibilities as trustees of the SMSF and that they could be penalised for non-compliance in several ways:

- their fund losing its concessional tax treatment

- being disqualified from their role as trustee – this means they can no longer be members of the SMSF, and they are unable to start a new one

- fines or imprisonment, depending on the seriousness of the breach.

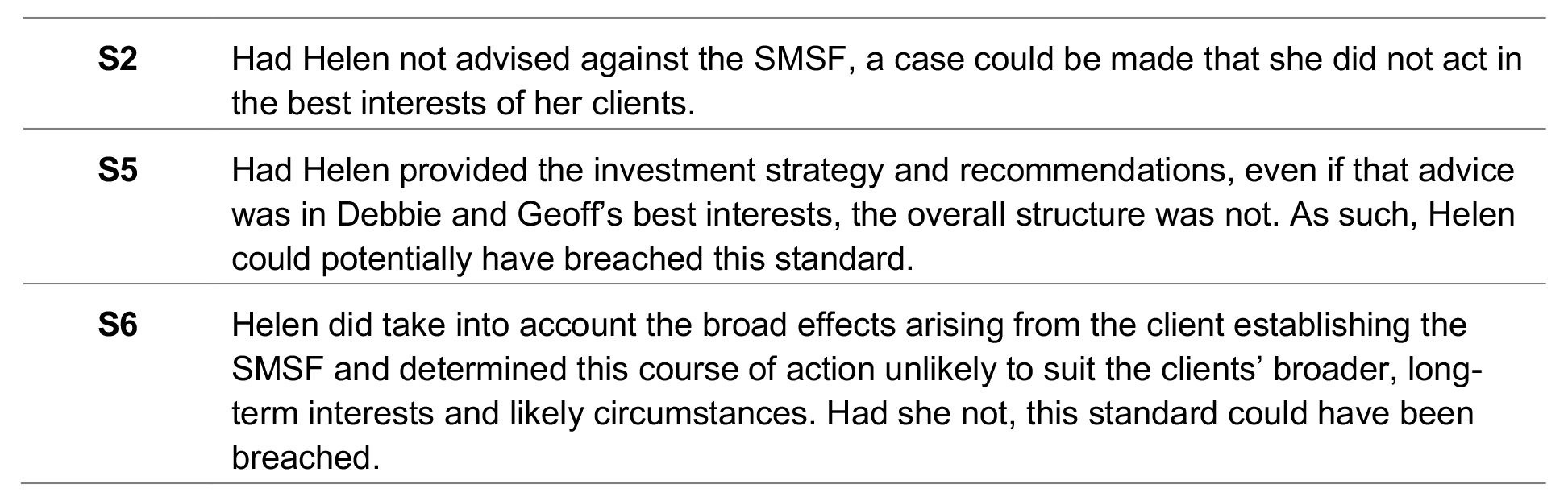

After lengthy discussions, Helen concluded that Debbie and Geoff were unlikely to have the requisite knowledge or time required to make an SMSF viable. As a result, she advised against this course of action.

Had Helen simply accepted the accountant’s advice to establish the SMSF and created an investment strategy and implementation plan as requested, she could make the case she was acting on her clients’ wishes and their accountant’s recommendation. The situation is not black and white. However, by engaging with Debbie and Geoff and understanding their capacity, Helen has acted in their best interests by recommending against the course of action.

Helen acted in the client’s best interests. Had she not taken that course of action and the clients were adversely impacted, the case could be made that she had breached the following standards in the Code of Ethics.

Case study two: A poor decision outside the workplace

A financial planner gained notoriety in 2021 when he breached travel bans to attend the AFL grand final in Perth. At that time, much of the country was in lockdown because of Covid-19 and Western Australia had strict border regulations and quarantine requirements.

The adviser deliberately circumvented those requirements to attend the sporting event. As a result, he faced penalties in Western Australia. In March 2022, ASIC banned the Melbourne-based adviser from providing financial services or engaging in credit activities for ten years. This includes being prohibited from controlling an entity that engages in credit activities or carries on a financial services business.

This is an interesting case. The adviser’s actions did not adversely impact clients; he did not breach laws pertaining to financial advice, nor contravene the Code of Ethics. This is a decidedly grey area as it relates to the provision of financial advice; black and white as to the breach of the WA Emergency Management Act 2005.

In its media release, ASIC stated that it is “satisfied that the adviser lacks the honesty and integrity to participate in the financial services and credit industries”.

Honesty and integrity are two of the key values that underpin the Code of Ethics. Integrity features explicitly in standard two: “You must act with integrity and in the best interests of each of your clients”.

Given the national media attention the adviser received, one could make the case that he breached standard 12: “Individually and in cooperation with peers, you must uphold and promote the ethical standards of the profession and hold each other accountable for the protection of the public interest.”

Case study three: Falsified documents

While falsified documents would not generally fall into the ‘grey’ zone, consider the case where an adviser falsifies documentation to get clients access to an investment opportunity that is in their interests. Still wrong…but, some might argue, with good intentions.

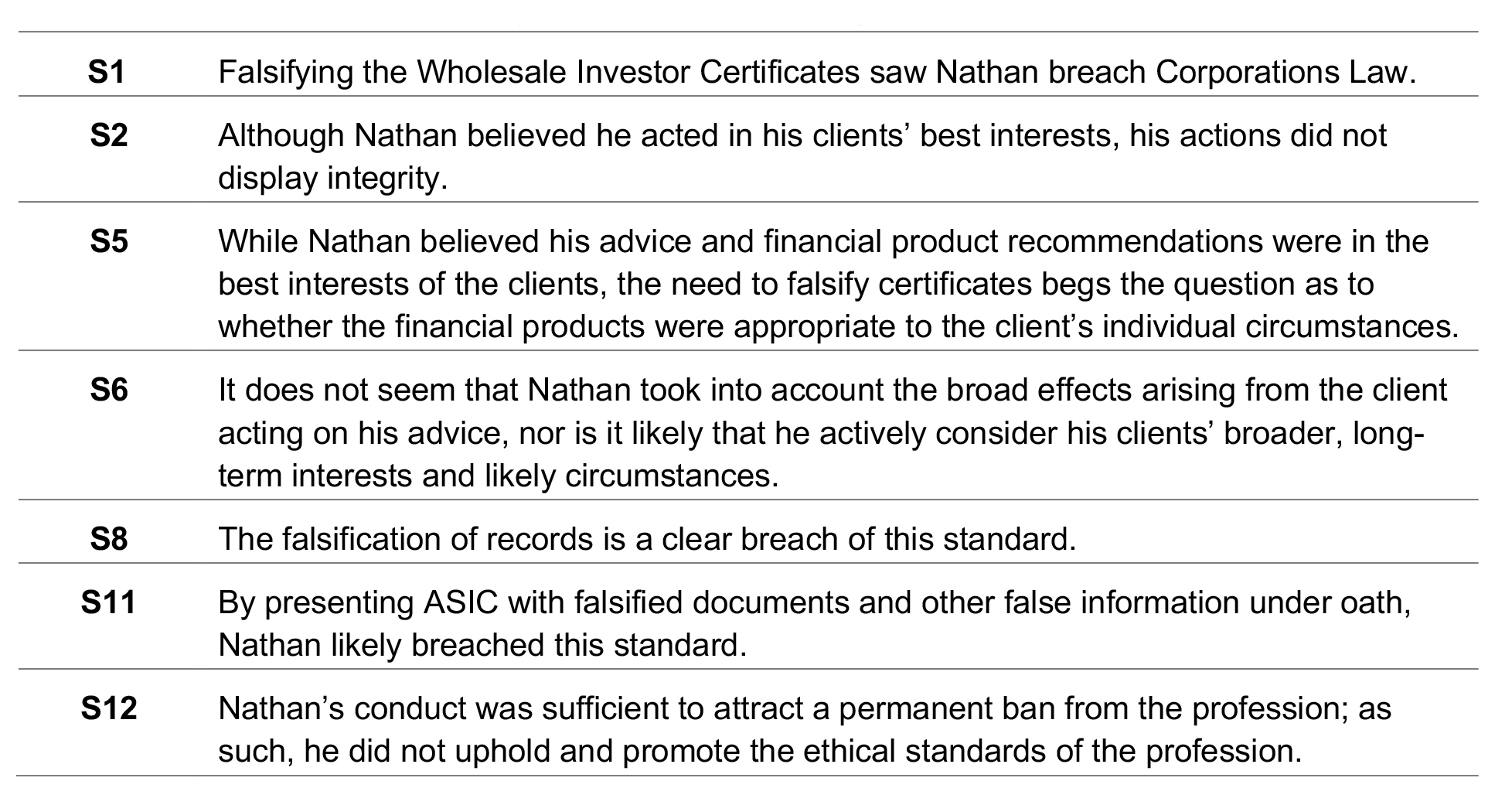

Sydney Adviser Nathan provided a number of his clients with falsified wholesale client certificates to enable them to access a range of financial products designed solely for ‘sophisticated investors’ as defined by Chapter 6D of the Corporations Act 2001. The certificate should be issued by a qualified accountant certifying the client has prescribed net assets or gross income level.

Nathan did this because he believed the financial products were in the clients’ best interests; they provided exposure to asset classes otherwise difficult for retail investors to access and the fee load was lower.

When ASIC audited Nathan’s practice, he presented falsified documents and was accused of being found to have ‘repeatedly attempted to deceive the corporate regulator with falsified documents’.

As a result, Nathan received a permanent ban from ASIC for misleading or deceptive conduct regarding the fabricated evidence. He also knowingly provided false answers and information related to the fake documents when questioned, both under oath and by way of statutory notice.

Nathan also fabricated other evidence, including emails and witness statements, both of which were used during an ASIC hearing. These actions took Nathan’s intent, potentially in the grey zone, to well and truly wrong.

Nathan’s actions see him potentially breaching the following standards in the Code of Ethics.

Case study four: Crypto investment group

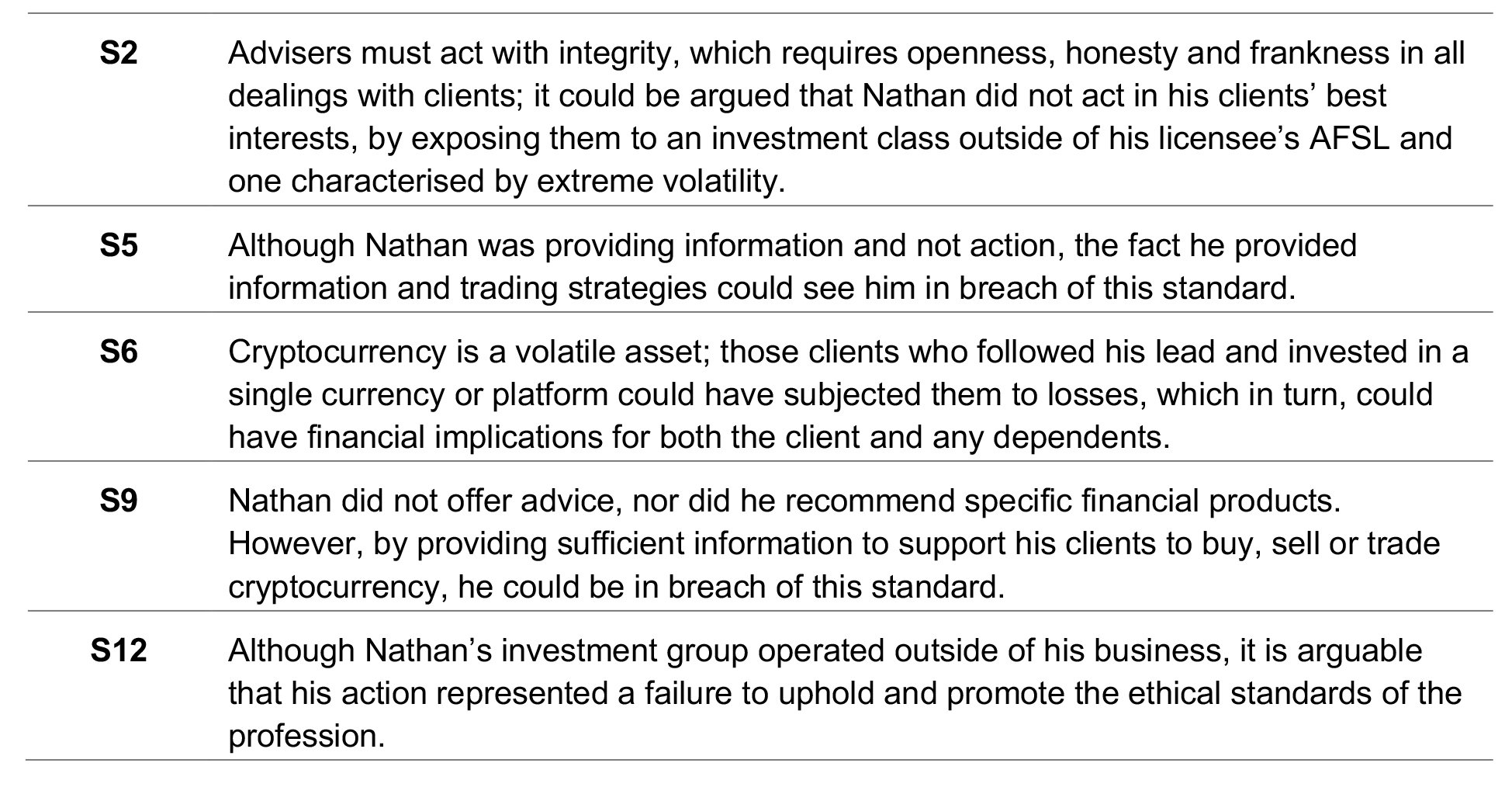

Clifton is a young financial adviser building a base of Millennial and Gen Z clients. He’s always been interested in cryptocurrency and while at university, spent time mining Bitcoin. As an early adopter of Bitcoin and other cryptocurrency, he has made some spectacular profits (and quite a few losses).

He’s chatted to some of his clients about his interest in cryptocurrency and several of them expressed interest in learning more. As something outside of the scope of his licensee’s AFSL, he put together a small investment group that met outside of business hours. The group discussed different cryptocurrencies, crypto trading platforms and strategies to buy and sell. Importantly, Clifton did not trade on behalf of any client or provide advice. It was, in his mind, purely educational.

Although Clifton did not trade or in any way act for his clients, quite a number of these clients invested in different cryptocurrencies or cryptocurrency platforms, with varied financial outcomes. By providing detailed information about this asset class, a case could be made that he strayed into the grey zone and potentially breached the following FASEA standards:

The best interest duty underpins both the operations and provision of advice by financial planning practices and enshrines it in law. Similarly, the Code of Ethics makes ethical practice a binding requirement for financial advisers – whether the situation is black and white, or not.

Financial advisers are required to act ethically and in the best interests of their clients at all times. While that might seem an obvious requirement to many readers, the almost daily media announcements detailing an adviser’s wrong doings and the consequences demonstrate these requirements are overlooked by some practitioners and businesses.

An ethical and professional partnership between adviser and client occurs when a client understands the adviser’s recommendations and trusts that the advice is in their best interest. If unsure about any element of advice you provide, if it’s not clearly black or white, consider the client outcome. Will your client be better off if that advice is implemented? Does the advice breach any standard in the Code of Ethics? Does it breach your moral code? If you’re still unclear, discuss with your colleagues and licensee.

It’s important to remember that at its simplest, ethics can be viewed as knowing what the right thing to do is, and then doing it – always in the best interests of each and every client.

———-