Getting smarter about TPD – strategies to cut costs and avoid a claim time tax bomb

Strategic decisions made by advisers about client TPD cover can avoid potentially expensive tax traps that most claimants are unaware of.

TPD: truth, tips, and tax

Total and Permanent Disablement TPD cover is one of the most misunderstood types of life insurance cover, decried by many as being complicated, too costly, and too hard to claim on. But the reality is far from the truth, and against a backdrop of the 2021 IDII changes, smart advisers are rethinking the role of TPD within a life insurance portfolio. These same advisers are also across the complex tax and regulatory framework that is unique to TPD. As such, TPD is a product where advisers have a lot of value to add, in both the initial set up of cover, and at claim time, where numerous traps await the unwary.

In this article we will uncover the truth about TPD claims, examines the considerations when structuring cover inside and outside superannuation, and the claim time mistake which can literally cost the claimant tens of thousands of dollars in extra tax.

TPD claims statistics

One of the more pervasive labels thrown around since the Hayne Royal Commission is that of ‘junk insurance’, referring to insurance seen as having a low payout rate (and thus being of little value to the policyholder). Whilst the various people throwing this term around may well have a point in the context of some types of credit insurance, it’s a description that is misplaced when applied to TPD cover.

Let’s take a look at the APRA claim statistics to understand why.

Total claims paid

Table 1 below shows the total number of claims paid by cover type, for the year ended 30 June 2021. Of particular interest is the data in the Group Super section. The default nature of group cover means Death and TPD cover is usually issued in tandem, meaning that most fund members will have both (as distinct from retail cover where customers may choose not to take TPD). The fact that the number of Group Super TPD claims are substantially more than the number of Group Super Death claims – based on similar cover counts – reinforces the fact that TPD isn’t some unicorn event that hardly ever happens. Amongst the working population in group super funds, TPD is actually happening more frequently than death.

Claims acceptance rate

The second data point worth noting is that claims acceptance rates are relatively high – averaging around 90% for group claims and just over 80% for retail advised claims (the difference generally being explained by disclosure issues, which don’t apply to group cover as there is no underwriting).The individual non-advised (i.e., direct) channel has a markedly lower rate of admitted claims than any other channel, likely down to a combination of disclosure issues at application time, and the challenges in gathering the appropriate evidence to support a claim, both of which are areas where advisers add enormous value.

Claims ratios

Additional APRA data, shown in Table 2 below, shows that the claims ratios for TPD – the percentage of total premium collected that is paid out as claims – are not dissimilar to trauma and income protection. This suggests that – contrary to the view held by some – TPD is not overpriced relative to the claims risk. Indeed, by the time the acquisition and administration costs of retail policies are considered, TPD and Trauma premiums are probably hovering around the break-even mark.

Recapping the different definitions of TPD

There are several definitions of TPD available across the market, including:

- own occupation

- any occupation

- activities of daily living

- domestic duties

- permanent ‘loss’

- functional impairment.

Own occupation is the most generous in the sense that it is the easiest to claim against – permanent disablement is judged against the likelihood of ever been able to work again in your own occupation. This definition is especially valuable to professionals and those working in specialised roles where their skills may be less transferrable.

Claims assessed against an ‘any occupation’ definition look at the likelihood of the claimant ever being able to work again in any occupation for which they are suited by ‘education, training or experience’, which is obviously a harder definition to fulfil.

The Activities of Daily Living definition assesses claimants against their inability to perform a prescribed number of activities deemed critical to a normal quality of life, such as the ability to bathe, dress and feed oneself. This is the hardest of all definitions to satisfy and was introduced to allow cover to be available to people who weren’t performing paid work (e.g., homemakers), those is in very high-risk occupations, or those beyond a certain age (e.g., 65).

The Domestic Duties definition caters for non-working individuals, where a permanent inability to perform certain tasks around the home (such as cooking, cleaning, driving a car) can warrant the payment of a TPD benefit.

A TPD policy may also extend to include a ‘loss’ definition, one that may pay either a partial TPD benefit (i.e. the loss of, or loss of use of one limb or the sight in one eye) or a full TPD benefit (i.e. the loss of, or loss of use of two limbs or the sight in both eyes).

Selected policies may offer cover for functional impairments. This can include significant cognitive or mental impairment, and/or a permanent inability to perform certain tasks (e.g. writing, lifting etc.)

As you would expect the premiums for each tier of TPD reflect the likelihood of claim, with own occupation TPD being the most expensive.

Be strategic with the way you use TPD within a life insurance portfolio

Two major strategic considerations with TPD cover are:

- how TPD works in conjunction with other covers, and

- whether to structure cover inside super, outside super, or both.

How TPD works alongside other covers

At a high level, the four main categories of life insurance (Death, TPD, Trauma, & Income Protection) each cover different risks, and fulfil a different purpose. In an ideal world, a client would have all types of cover in a comprehensive risk portfolio. But budgetary constraints and other factors often mean the world is far from ideal, and role of an adviser is to help the client optimise their protection within those constraints. Often this means a degree of compromise is necessary.

One obvious way to extract more bang for the premium buck is to write TPD (and indeed other risks) as riders to a core cover (usually Death), rather than as a standalone cover. The rider approach, where a claim on a rider benefit (such as TPD) also reduces the sum insured for the core cover, represents less total risk to the insurer, and this is reflected in premium savings.

Another example is to consider the relationship between TPD and Income Protection. This has become particularly topical in the wake of the October 2021 IDII changes, and the subsequent repricing of Income Protection across the board.

Work by Zurich[3], showing the impact of different benefit and waiting periods on IP premiums, reveals that the balance between TPD and long-term IP can be a complex one to get right.

For example, an IP policy with a 6-year benefit period can be as much as 26% cheaper than a policy that pays all the way to age 65.

And research by KPMG[4] suggests the average income protection claim is 12 months (14 months for cancer and 18 months for mental health claims).

Zurich’s own data on the other hand, reveals a slightly different story. As of September 2021, 29% of Zurich and OnePath’s open and ongoing income protection claims were for periods of 5 years or more, 23% of which were for periods of 10 years or more.

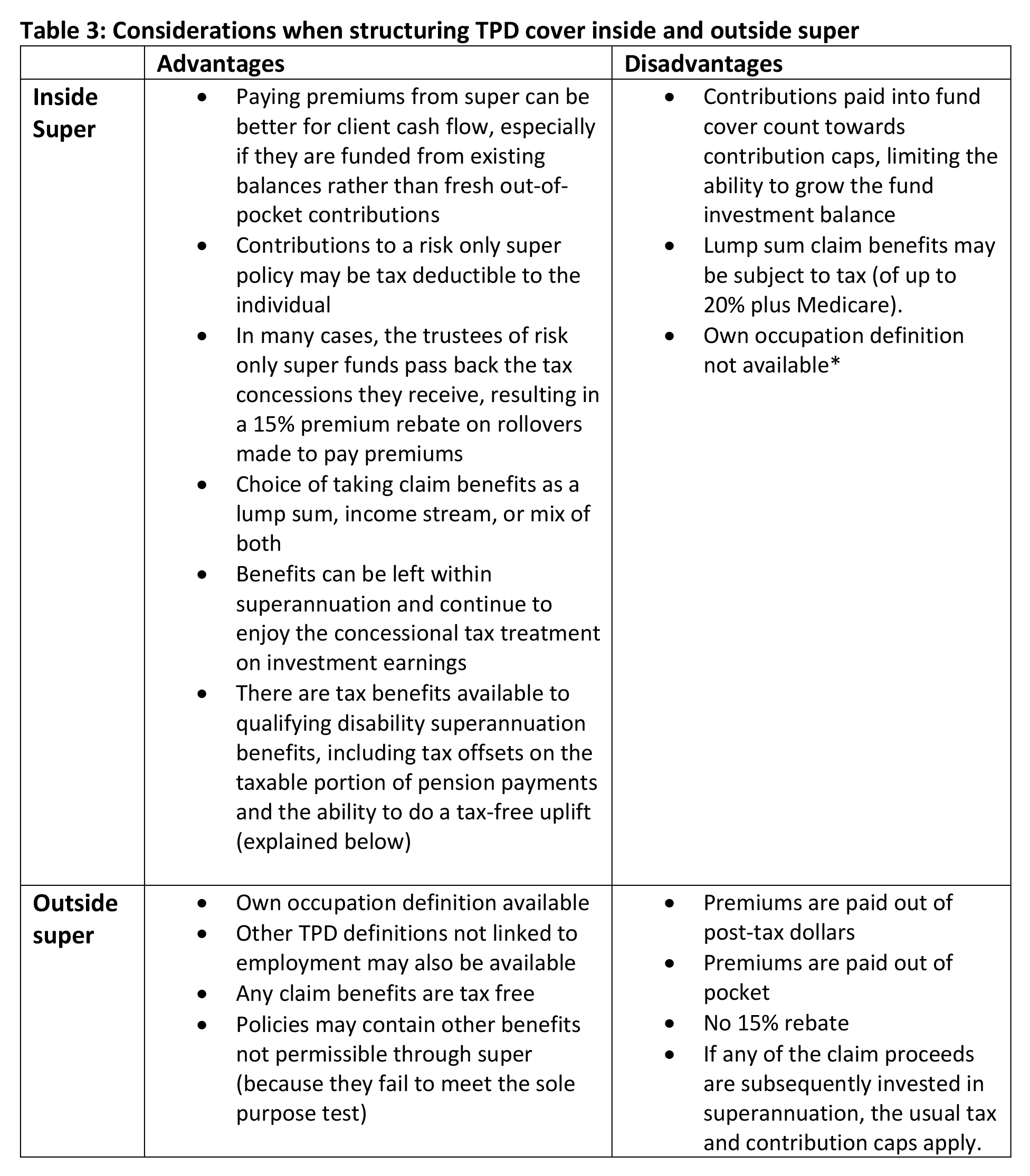

Inside or outside super?

The question of whether to hold TPD cover inside, or outside superannuation is also complex, and again the right approach will depend on many factors, including the client’s occupation, income, and cash flow position.

One major consideration is that several definitions of TPD (e.g., Own Occupation, Domestic Duties, Functional impairment and ‘Loss’ definitions) don’t meet the definition of incapacity contained in the Superannuation Industry Supervision (SIS) Act which governs superannuation. As such, only those which align to the ‘any occupation’ TPD will satisfy the condition of release which allows claims to be paid from superannuation. The desire of clients to have the more comprehensive coverage of own occupation, but in a financially optimal way, has seen linking strategies – explained below – become popular.

Table 3 provides a high-level summary of the pros and cons of structuring TPD cover inside and outside super.

* Some pre 2014 policies may still offer own occupation definition under grandfathered arrangements, so check before cancelling/upgrading such cover.

Linking coverage inside and outside super

A popular strategy to optimise the tax and cash flow benefits of taking cover through super and still have the peace of mind of an own occupation TPD definition is to link cover inside and out.

Whilst the actual mechanics and language vary across insurers, the core concept is the same as that offered by Zurich[5] under their ‘Superannuation Optimiser’ feature:

A policy with own occupation TPD outside super is linked to TPD on a policy owned inside super. Any TPD claim must first be assessed under the any occupation definition applying to the policy held through super. If the definition is met, the trustees will authorise a claim to be paid out, as a disability superannuation benefit. If the definition is not met, the claim will then be assessed under the own occupation benefit, and, if it meets that definition, paid out as a non-super tax-free lump sum.

Note that in this scenario, the TPD sum insured would become zero, and the sum insured under other linked coverages would also be reduced. At this point, a cover buy-back – which allows the core death coverage to be returned to the pre claim level – can become worthwhile.

Because the cover is linked, rather than duplicated, cover isn’t being paid for twice. The total cost is no more than if you were paying for own occupation outside TPD and, the advantages described in Table 3 will apply to the portion of the premium that is paid through superannuation.

TPD claims within super – the hidden trap

Assuming a claimant satisfies the conditions of release for a TPD benefit to be paid, that benefit will be added to the client’s superannuation balance. At this point the taxation considerations become quite complicated, and the consequences of making the wrong decision can literally increase the claimant’s tax burden by tens of thousands of dollars. As will be explained below, the likelihood of falling into this tax trap has increased dramatically since the introduction of the Protecting Your Super and Putting Members’ Interests First legislations, meaning strategic risk advice has become more valuable than ever before.

Tax treatment of disability superannuation benefits

Upon payment, TPD insurance proceeds are paid into the claimant’s superannuation fund, initially forming part of the fund’s taxable component. Herein lies the first major advice opportunity.

Tax free uplift

Claimants can benefit from an increased tax -free component – a so called ‘tax free uplift’ – if they take the benefit as a lump sum or roll it over to another fund.

Note that this doesn’t automatically occur when the insurance benefit is paid into the superannuation account. Evidence is required, in the form of certification from 2 legally qualified medical practitioners, that the person because of ill health, is unlikely to ever be gainfully employed in a capacity for which they are reasonably qualified because of education, training or experience (i.e., they meet the any occupation definition).

(You can’t always rely on the TPD claim process as a substitute for this evidence. Specifically write to the fund to request them to apply the tax-free uplift and, if required by the trustees, supply fresh medical practitioner certification.)

The increase in the tax-free portion of the disability benefit is calculated according to the formula below[7]:

Days to retirement = number of days from when person stopped being gainfully employed to their last retirement date (usually 65).

Service days = Number of days from the start of the eligible service period in the fund to the date the disability super lump sum benefit is paid.

The eligible service period tax trap

The eligible service date (the start of the eligible service period) is the earlier of the following dates:

- the date the superannuation account was set up

- if the super account was set up by an employer, the eligible service date (ESD) is the date employment with that employer commenced

- if multiple superannuation accounts are consolidated, the earliest ESD is always retained.

The trap lies within the consolidation of superannuation accounts beyond this point, either deliberately or inadvertently. If super accounts are consolidated after a claim has been paid, any earlier service date will take precedent. An earlier service date causes the number of service days to increase, increasing the denominator in the formula above, and therefore reducing the tax-free uplift. This is explained in the case study below:

Case study – super consolidation increases tax burden on TPD claim benefit

Jane becomes eligible for a permanent incapacity (TPD) benefit of $500,000 through her fund. In addition to any existing tax-free amount already in her fund, she is eligible for a tax-free uplift.

For illustrative purposes, after considering her age and eligible service date let’s say the tax-free uplift was calculated as:

Now, let’s imagine Jane has an old, inactive, low balance superannuation account that was started several years earlier, and consolidated that account into the account holding her TPD benefit. Her eligible service date would become the later date (from the old, inactive fund), thereby increasing the number of service days. If, for example, those days were increased by 2,000, to 5,000, then the above calculation becomes:

Result = Jane’s tax-free amount has decreased by $63,158 ($300,000 – $236,842), an amount which could now be subject to as much as 22% tax, depending on Jane’s preservation age and how she accessed the benefit. That’s as much as $13,895 in extra tax, all because of something which everyone tells us is sensible (consolidating superannuation accounts)!

The Protecting Your Super Legislation, and the way the changes automatically sweeps inactive low balance accounts and allocates them to active accounts, means this consolidation can happen against the will of the individual, with potentially expensive consequences.

Strategies to avoid this

- Firstly, it goes without saying that in the event of a claim, any plans to consolidate super accounts should be put on hold.

- Secondly, they should immediately lodge with their fund the appropriate ATO form to prevent such automatic consolidation.

- And thirdly, they should consider locking away the more recent eligible service date by rolling over their superannuation benefit to another account. As well as locking in the tax-free component, this also locks in the status of that amount as a ‘disability payment’, meaning they won’t be required to provide any fresh evidence to meet a condition of release (as would potentially be the case if the payment was left in the existing fund and withdrawn later).

‘Washing out’ more of the taxable component

If the client makes a non-concessional contribution to the account containing the claim benefit, before that account is rolled over into a new fund (to lock in the tax-free amount), the effect of the tax-free uplift is amplified.

Account based pensions, Centrelink, and other considerations

Of course, withdrawing their TPD benefit as a lump sum is not the only option available to claimants. Members meeting the permanent incapacity condition of release are also able to commence an income stream from their superannuation account (via an Account Based Pension). Such payments are taxed at the recipient’s marginal rate less a 15% tax offset on any taxable component. Given the claimant is no longer gainfully employed, their marginal rate is likely to be low, meaning even under preservation age they may be able to draw out significant amounts with minimal or no tax.

From a Centrelink perspective, any amount held in the accumulation phase is not assessed under the assets or income test while the client is under the Age Pension age, meaning they could still be eligible for a disability support pension.

Amounts held in Account Based Pensions are fully assessed under the assets test.

Summary

Decisions around the structuring of TPD cover, its role within a risk portfolio, and the best ways to access any claim benefits paid are complex, with many costly pitfalls awaiting the unwary. These complexities present both challenges and opportunities to optimise the claimant’s financial position. Financial advisers are uniquely placed to ensure their clients make the most optimal decisions, meet these challenges, and fully capitalise on these opportunities.

![]()