Sudden wealth is on the rise – how advisers can protect clients from its pitfalls

Sudden and unexpected wealth transfers are on the rise, but for many people this ‘’dream come true’ scenario can actually become a nightmare.

The challenges of sudden wealth

Most people, to a greater or lesser degree, dream of sudden wealth.

But whilst the pursuit of riches can be a powerful motivating force that helps people cope with their day-to-day struggles, and has energised a legion of entrepreneurs, athletes, entertainers, and business owners around the world, it can also drive a range of negative behaviours, from gambling and speculative investing, to fraud, theft, and even more serious criminality. Within families it can contribute to disputes and even financial abuse.

For many of those who achieve sudden wealth, the dream can quickly become a nightmare, as their inexperience in dealing with large amounts of wealth, and the accompanying change in lifestyle, can have a dramatic impact on their relationships, their mental health, and even their personal safety. It can also exacerbate any existing vulnerabilities an individual has.

As such, sudden wealth represents a major – and growing – consumer protection challenge.

Many people lose unexpected wealth within a few years, and ‘rags to riches to rags’ stories are sadly all too common. A US study of inheritances[1] found on average half of all money inherited is saved, while the rest is spent, lost, or donated within a few years.

The onset of the $3.5 trillion intergenerational wealth transfer[2] in Australia, the meteoric rise of crypto and stratospheric real estate prices will continue to drive significant increases in the number of Australians experiencing sudden wealth. This means the potential for clients to suffer financial or physical harm as a result of sudden wealth will also grow rapidly.

Financial advisers are ideally placed – more so than lawyers and accountants – to protect the suddenly wealthy, not just through the mechanics of structuring their financial affairs, but with a range of other resources and guidance that can help them avoid the many pitfalls of sudden wealth, including the dreaded ‘Sudden Wealth Syndrome’.

What is sudden wealth, and where is it coming from?

Whilst winning Powerball is the most headline worthy example of sudden wealth, a more practical – and broader – definition, such as that proposed by the UK’s Financial Vulnerability Taskforce[3] is of more practical value:

- a person receives a significant amount of money that they did not expect

- it occurred relatively quickly leaving little time to prepare

- that person has no experience or capability in making decisions around such large amounts of money.

Our definition therefore excludes business owners who are cashing in on their success, the children of wealthy parents, and others who are more financially savvy, or have had more time to prepare for the wealth transfer. (CTP payouts on behalf of children will also be excluded from this discussion, as legislation generally requires those payments to be held in trust, to ensure they are available to benefit the child for the rest of their lives).

And whilst a lottery win definitely fits this definition, statistically speaking advisers are far more likely to encounter clients who have experienced unexpected wealth through more orthodox channels, including an inheritance resulting from the untimely death of a family member, or from an unexpected source.

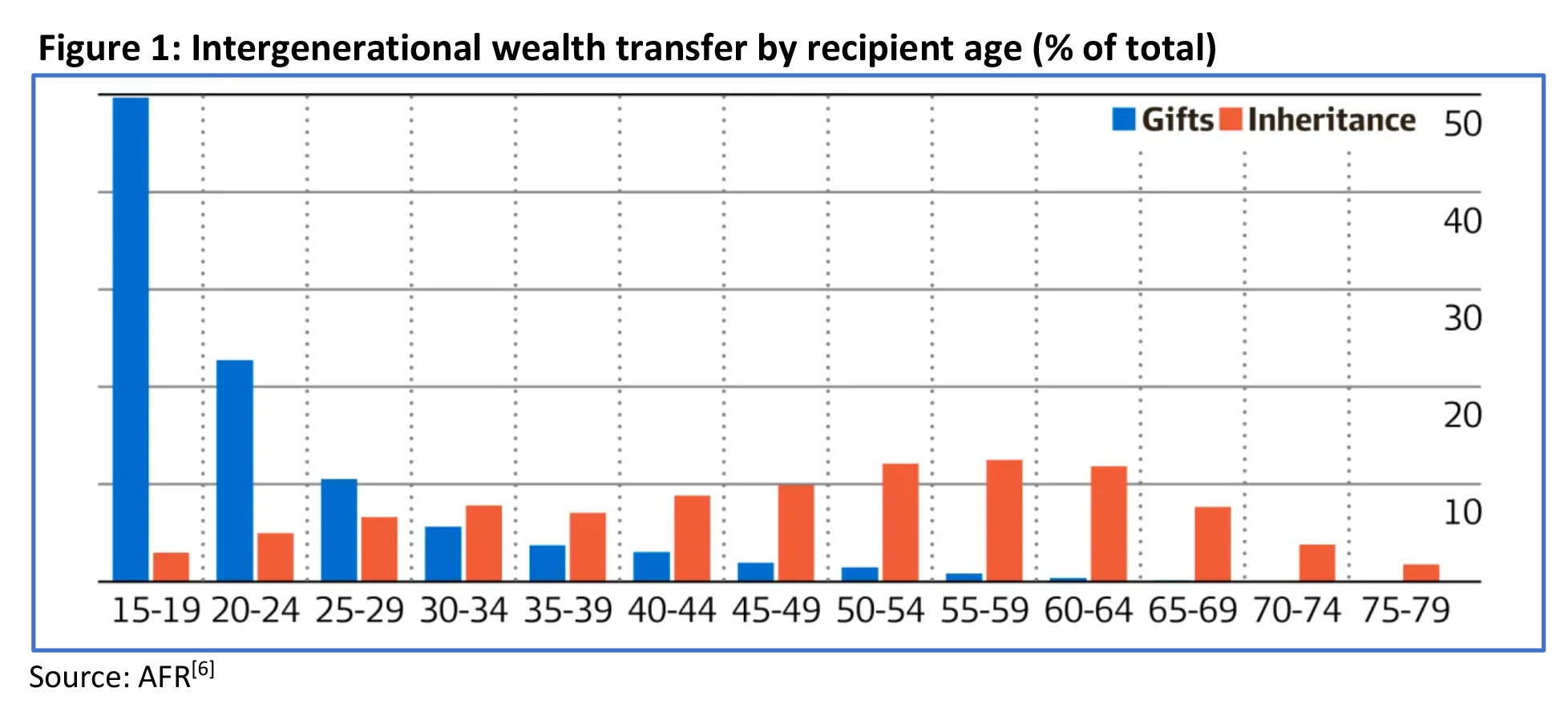

According to Productivity Commission research[4], Australians inherited over $120 billion in 2018, a figure expected to grow to over $224 billion per annum by 2050. And according to the Government’s Retirement Incomes review, by 2060, one in every three dollars paid out of the superannuation system will be an inheritance rather than retirement income[5].

But while Australians are most likely to receive an inheritance when they are in their fifties (Figure 1), billions are still being inherited or gifted to people much, much younger.

Other common sources of sudden and substantial can wealth include:

- the sale of a property

- a divorce settlement

- a large insurance payout, for example a CTP or TPD claim

- a redundancy payment.

Sudden wealth can make people vulnerable

Put yourself in the shoes of an individual who, along with their family, lives a modest lifestyle, with a steady job, a house, and a car. They have a mortgage, car loan and credit cards but all are under control. Their superannuation balance is small but growing. They have a circle of close friends and are generally happy with life.

Then one day, completely out of the blue, they find out they have come into several million dollars – perhaps from a lottery win or an inheritance from a relative they didn’t know they had.

Whilst it is accepted that some people remain calm, considered, and resourceful, they are in the minority. Once the initial shock has passed, many negative emotions commonly emerge, such as fear, anxiety, sadness, and guilt. This phenomenon is known as Sudden Wealth Syndrome, and it can have a devastating impact on its sufferers.

Sudden Wealth Syndrome

Sudden wealth syndrome (SWS) refers to the identity crisis, and subsequent behaviours and health impacts, suffered by individuals who have suddenly come into large sums of money[7]. SWS was first identified by American psychologist Dr Stephen Goldbart, in a study of the impacts of wealth on people. Symptoms can include feeling isolated from former friends, feeling guilty about their good fortune, and extreme fear of losing their money. Sufferers can become overwhelmed, grow suspicious of people around them, and make poor decisions such as overspending or lending money to family and friends causing strain on relationships.

Sometimes the negative feelings experienced upon an unexpected large wealth transfer are made far worse because of unwise actions taken by the individual, or their family members, in a knee-jerk reaction to their sudden change of circumstances. And of course, if the sudden wealth is the result of a life changing accident, or the unexpected death of a loved one, the feelings described above will be exacerbated by a range of additional emotions including grief and depression.

Regardless of how they got there, many suddenly wealthy individuals are therefore highly vulnerable to making hasty, ill-considered decisions which could have significant, negative consequences over both the short and long term. Which means they need protecting, from themselves, and from others.

Common mistakes made by those with sudden wealth

The complex, sometimes conflicting emotions experienced on receiving sudden wealth, and a lack of financial savvy, often combine to drive some common mistakes.

1. Telling people and jeopardising their anonymity

Many people receiving sudden wealth, feel compelled to share the news with family members, friends, and colleagues. Sometimes, they do it immediately, because they happen to be with other people when they first hear the news.

This can lead to several difficulties and there are many examples where people have ended up either creating circumstances where they become vulnerable, or they have made an already difficult set of circumstances into an even more challenging situation than it was before they received the news.

Failing to keep sudden wealth private can also lead to the person becoming a victim of fraud, scams, and financial abuse at the hands of the family and friends and other unscrupulous parties.

2. Promising or making gifts without understanding the ramifications

Most sudden wealth recipients tend to overestimate how far that money can go, and in the haste to be generous to family and friends, it isn’t unusual to spend their money several times over. Promising to make gifts and then regretting that decision once they have had time to consider the ramifications can cause great anxiety on both sides. The individual must then decide between fulfilling that promise, with all the consequences, or reneging on it and risking their relationships.

Additionally, there can of course be taxation and Centrelink/pension implications down the line, for both the giver and receiver of any gifts of money or other assets.

3. Hasty decisions, irrational behaviour, and reckless spending

It is estimated[8] that 70% of lottery winners spend all their winnings within a few years, and it certainly seems to make sense that those unused to dealing with large sums of money are more likely to lose it. (In the US, lottery winners are more likely than the average American to declare bankruptcy[9]). Often this can be the result of spending based on impulse rather than need or practicality. A fleet of luxury cars that sits in the garage, or a house too large for the family who lives there are probably at the milder end of the scale (at least the house is likely to appreciate in value).

But even putting aside the more extreme, and rarer, examples of those winning big on the lottery, the risk of hasty decisions and reckless spending is equally problematic for those who have come into sudden wealth through less fortuitous circumstances. This can often be because they overestimate how much money they have and underestimate how much things will cost.

As Anne Graham, award winning Financial Adviser and CEO of Story Wealth, put it “What they tend to do is spend it ten times over. There’s a lot of zeroes on this money but they think it can go further than it actually can”.[10]

The long-term consequences of getting this wrong can be stark:

- a young adult receiving an inheritance could blow their chances of getting into the property market later in life by frittering away those funds

- a person made redundant in their fifties may find it more challenging to re-enter the workforce, meaning their pay-out needs to sustain their lifestyle rather than fund luxuries and dreams

- a TPD benefit is effectively an advance on a lifetime of earnings foregone because of a serious, permanent, disability, one which may require specialised and expensive care on an ongoing basis. Frittering it away could dramatically undermine quality of life and impact both the sufferer and their caregivers.

4. Making poor investment decisions

Even those attempting to do the right thing and invest – rather than spend – their sudden wealth can see it disappear if they are making emotional, uninformed, mistimed, or poorly researched investment decisions.

There are, after all, many ways to lose money by investing poorly:

- a pre retiree investing in more aggressive portfolio at the market peak

- investing in highly speculative stocks which lose value

- conversely, investing in low yield cash investments which lose real value over the longer term

- a lack of diversification

- investing in exotic financial instruments and cryptocurrencies

- buying a franchise or a small business in a dying industry or a poor location

- investing in a business venture or unregulated fund which fails.

It goes without saying that these are the types of mistake financial advisers help clients avoid all the time.

5. A general lack of financial awareness and planning ahead

A minefield awaits the suddenly wealthy, who don’t know what they don’t know (because they have never needed to know it). That lack of knowledge applies to both the challenges – such as taxation implications – and the opportunities associated with sudden wealth. Those who don’t already have a financial adviser may also be unclear about how expert financial advice can help them, or even what sort of advice they need (Investment? Taxation? Legal).

Estate planning can also be problematic – either because of the complete lack of a will, or because existing wills are left unchanged even though an individual’s new circumstances make them inappropriate and not fit for purpose.

The subsequent decision paralysis across a range of issues – stemming from not knowing who to turn to for help – can have disastrous financial consequences.

How a financial adviser can help suddenly wealthy clients

Financial advisers are clearly the best equipped to help those with sudden wealth navigate complex financial issues, from understanding risk tolerances, to planning the strategies that will underpin a dream, and possibly early, retirement.

But there’s much more to it than the tax strategies and portfolio decisions aimed at helping clients preserve and pass on their wealth. There’s the part where you help them cope with a very different set of challenges as they start to live very different lives:

- how to emotionally accept that they now have wealth

- how to deal with friends and family who want financial help, and

- how to avoid being taken advantage of.

Emotional acceptance

Transitions can be stressful – even good ones! Getting your head around a quantum change in personal circumstances can be truly daunting. As an adviser, you need to recognise the heightened emotional state your client will be in, especially at first. Your job is to reassure them, and ensure they take time to process what has happened, and not make any hasty decisions.

Dealing with family and friends

Birds of a feather flock together. A person of moderate means likely does not have a group of multimillionaire friends. In terms of current relationships, there will be tension—one sided if the client keeps their newfound wealth private; two-sided if both parties are aware of the changed financial circumstances. It can be a complicated situation to handle.

Whilst keeping the news of sudden wealth private is recommended, in the context of close family and friends, it can be nearly impossible.

A temptation to give money away to family and friends must be avoided, as too much generosity can backfire and set a dangerous precedent.

As an adviser, you should take on the role of ‘bad cop’, buying your client time and being a sounding board for them to discuss what is happening around them. You should even suggest they respond to all requests by saying ‘my hands are tied until my financial adviser resolves a few important issues’.

Unfortunately, some of your client’s relationships will inevitably sour or end. This is unavoidable in many cases since some people have a hard time accepting a friend or family member’s extreme wealth. Be sure to prepare your client and let them know that this is a typical by-product of financial windfalls.

Avoid the wolves

As well as being beset by family and friends asking for handouts, suddenly wealthy clients are also vulnerable to unscrupulous people pitching them risky and unregulated business and investment opportunities.

Again, your role is to be your client’s trusted adviser, confidante, and gate keeper. Encourage them to discuss all such ‘opportunities’ with you before signing and committing to anything.

Depending on the nature of what is being discussed, these are circumstances where should work collaboratively with your client’s lawyer and accountant (if they have one).

Estate planning

Notwithstanding the importance of your client ‘taking time to catch their breath’ before committing to any major spending or planning, sorting out their estate plan may require a little more haste. That’s because clients without a will suddenly have a lot more at stake, while those with a will already in place are likely to find it is no longer appropriate to their dramatically changed circumstances.

Whilst the underlying shape of your client’s assets may change once you have put a comprehensive plan in place for them, this doesn’t prevent them setting up estate plans now (and fine tuning them if necessary once they start to implement your detailed financial strategies).

Philanthropy and social causes

It is not unusual for recipients of sudden wealth to donate to charities, and this can be for a variety of reasons. It could be that they feel undeserving or guilty about having received that money, it could be that they are fearful that wealth will disrupt their hitherto happy life, or it could simply be that they are now in a position to donate more to a charity they have supported through their lives.

Whilst understanding your client’s values and causes is a standard part of the client fact find process – forming the basis of any ESG investing strategies – the receipt of sudden wealth is the ideal time to revisit these conversations with your client. Whilst your role isn’t to influence your client’s choice of charity, you can still play a gatekeeper role, including confirming that a charity is legitimate, and ensuring they understand the financial impact of their proposed donation on their remaining wealth.

Ongoing monitoring for signs of financial abuse

One key advantage that a financial planner or adviser has over the other professions is the regular contact and the nature of the relationship that is developed over a lifetime with a client. As such, they are generally better positioned to have an awareness of any financial abuse that may be occurring. Sudden wealth can increase the risk of such abuse.

A variety of red flags can present themselves when financial abuse is occurring, and financial advisers should remain vigilant in monitoring and acting on these signs where required (including discussing them with your client and reporting the issues where appropriate).

These signs include:

- unexplained or unusual activity on bank and investment accounts

- the sudden presence of a ‘gatekeeper’ who accompanies clients to meetings

- changes of address and/or email for statements and financial documents

- suspicious signatures

- sudden and/or frequent financial activity

- ATM withdrawals by housebound person

- online transactions by a person with no internet connection or enabled device

- changes in their property, wills, or other documents which are unexpected, sudden or in favour of new acquaintances

- the sudden appearance of previously uninvolved relatives claiming rights to the victim’s affairs and possessions

- an unexpected change in legal advisers.

In summary

Sudden and unexpected wealth transfers are on the rise, but for many people unused to dealing with large sums of money, this ‘’dream come true’ scenario can actually become a nightmare, characterised by anxiety, relationship breakdowns and even financial abuse. As such, sudden wealth represents a major consumer protection challenge. Financial advisers are uniquely qualified and positioned to help their clients emotionally adjust to sudden wealth, develop new money behaviours, and design and execute strategies to optimise and protect that wealth in a way that is consistent with their values, and which improves, rather than threatens, their overall wellbeing.

——–