Retirement – Independent living

Understanding the in-home aged-care system can benefit your retiree clients.

As your clients get older, living independently in their own home may become more challenging. If a client needs assistance, there are many services to support a diverse range of needs. This article, proudly sponsored by Russell Investments, explores in-home care options, the government support that’s available and how it can benefit your clients.

Your client has retired, they live at home, but they need some support to remain there safely and comfortably. The level of support required will differ for each individual. It may mean assistance to shop, cook a meal or clean the home. For some clients, it may be personal care to bathe and dress. Others may need acute nursing care and a higher level of support to remain in their home.

Before we examine the in-home care system it’s important to note that it can be very challenging to navigate and nearly everyone will need some sort of help with it. It’s important that your client knows you are there to support them and answer questions about this complex process, should they require it. It’s also the time to ensure your client has established a Power of Attorney and Enduring Guardian.

In-home care

There are two government funded programs available to your clients; however, it’s important to note that these programs, despite government funding, are not without cost to the consumer.

The programs are designed to support older Australians live independently in their own homes for as long as possible. Independent living, in the person’s own home is important. It’s been found to improve quality of life and help retirees remain active and connected to their communities. Although it will vary from client to client, this may help the achievement of personal objectives that form part of a client’s financial plan.

Importantly, home can be many things; it can be a house, an apartment or a mobile home. It can be independent living in a retirement village.

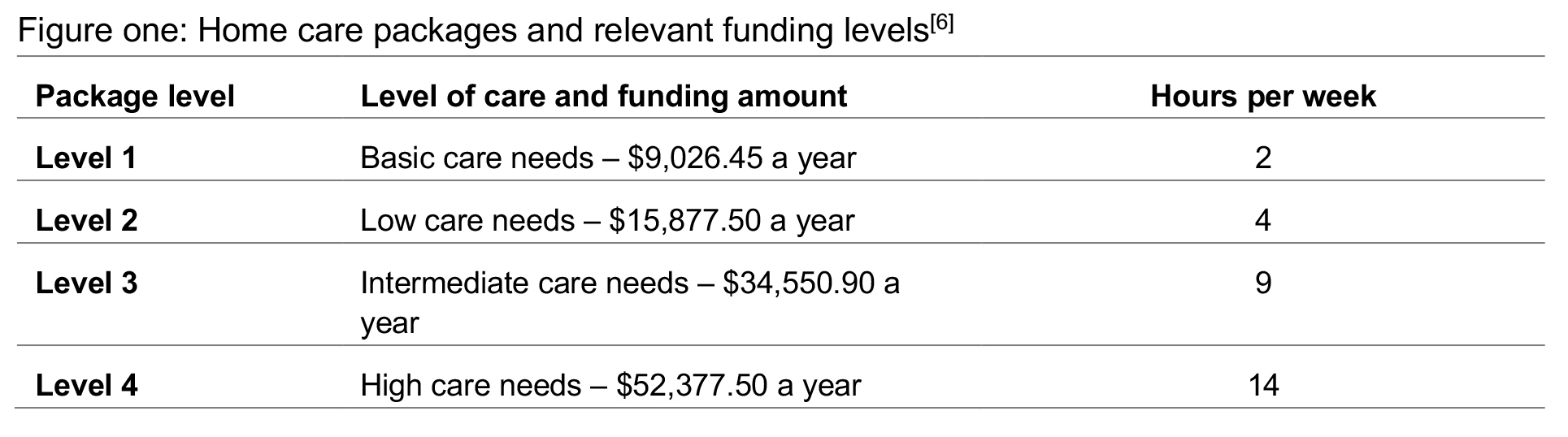

The first government funded program is the Commonwealth Home Support Programme (CHSP), described as an ‘entry level’ program designed for older people who need basic support in the home. For those clients with more complex needs, there’s the Home Care Package (HCP), designed to deal with higher care needs. There are four levels of HCP available.

While the two programs currently operate quite independently of one another and require separate application processes, a working group is currently focused on the transition to a single aged care model sometime in 2023.

At 31 December 2021, 217,724 people had access to an HCP, a 25.5 percent increase year on year. At the same time, there were 44,650 people who were seeking an HCP at their approved level, who had not yet been offered one. Of these people, 98.4 percent (43,942) had been approved for support through the Commonwealth Home Support Programme (CHSP)[1].

One of the issues a client may face when being allocated an HCP is receiving a plan that offers the appropriate level of care. At 31 December 2021, there were 23,779 people who were seeking a HCP at their approved level, who had already been offered a lower level HCP[2].

In 2015, Consumer Directed Care (CDC) became a legislated requirement for all CHSPs and HCPs, with a focus on flexibility and choice. This means the consumer has the power to make decisions about the aged care support they need, within the government’s rules for each program. It also gives consumers the power to choose their HCP provider and transfer to another approved provider if they are not satisfied with the services received.

The principles that guide the delivery of HCPs mean consumers[3]:

- are encouraged to identify their goals, which will be the basis of their care plan

- decide how much involvement they want to have in managing the package

- can choose the way services are delivered, and by whom

- have an individualised budget and a monthly statement of income and expenditure

- can expect regular contact with their provider

- can change the provider if their needs or preferences change.

Eligibility for either program is based on your client’s support needs and age; your client must be aged 65 years or older.

As well as meeting the age requirement, your client may be eligible if they:

- have noticed a change in what they can do or remember

- have been diagnosed with a medical condition or reduced mobility

- have experienced a change in family care arrangements

- have experienced a recent fall or hospital admission.

Commonwealth Home Support Programme

The CHSP provides entry-level support for older people who need some help to stay at home. If a client needs some home assistance, the service providers work with them to maintain their independence.

The program is designed to have someone work with your client, to help them maintain their independence, rather than simply doing things for them. This support can include help with daily tasks, transport and social support. It can also provide some basic home modifications and nursing care.

If your client uses the services of a carer, the CHSP can provide support for those times the carer needs to attend to matters away from the client’s home.

To access a CHSP, a home support assessment is conducted by the Regional Assessment Service (RAS). If they meet the requirements, your client can apply for an assessment online.[4]

A trained assessor then conducts a home visit to undertake an assessment. They will talk to your client about their individual circumstances and needs, and work with them to identify the services your clients may need to retain their independence in the home.

Services

CHSP services provided in the community may include[5]:

- social support – social activities in a community-based group setting

- transport – help to get out and about, for shopping, appointments or medical services

- services provided at home may include:

- domestic assistance – household jobs such as cleaning, washing and ironing

- personal care – help with bathing or showering, dressing and hair care

- home maintenance – minor general repairs and care of your client’s house or garden; this might include changing light bulbs, replacing tap washers or weeding and mowing

- home modification – minor installation of safety aids such as alarms, ramps or support rails

- nursing care – a qualified nurse makes a home visit for basic medical issues, such as the wound dressing.

Home Care Package

Home Care Packages (HCP) provide access to affordable care services to obtain help and support in the home. For your clients with more complex needs, an HCP may be an appropriate option. While it provides similar services to CHSP, the services are customised to meet the applicant’s individual needs.

There are four different tiers of HCP available, depending on the level of care required (figure one). As highlighted earlier in this article, it’s not uncommon to receive a funding for a package tier lower than that required, resulting in a funding (or service) shortfall.

While the same type of care and equivalent services are provided under each HCP level, the hours of care are increased at each level of care: i.e. a Level 3 package provides more hours of care than a Level 1 package.

Package supplements are also available. For example, there’s a Dementia Supplement for people with dementia. This and other supplements are available with any of the four levels of HCP.

Eligibility and assessment

To receive an HCP, the first step is an assessment by an Aged Care Assessment Team (ACAT). The role of the ACAT is to determine the level of care required and help your client – and their carers if relevant – establish the care services that will best meet their needs.

To qualify for an assessment, your client or a support person can use the online eligibility checker.[7]

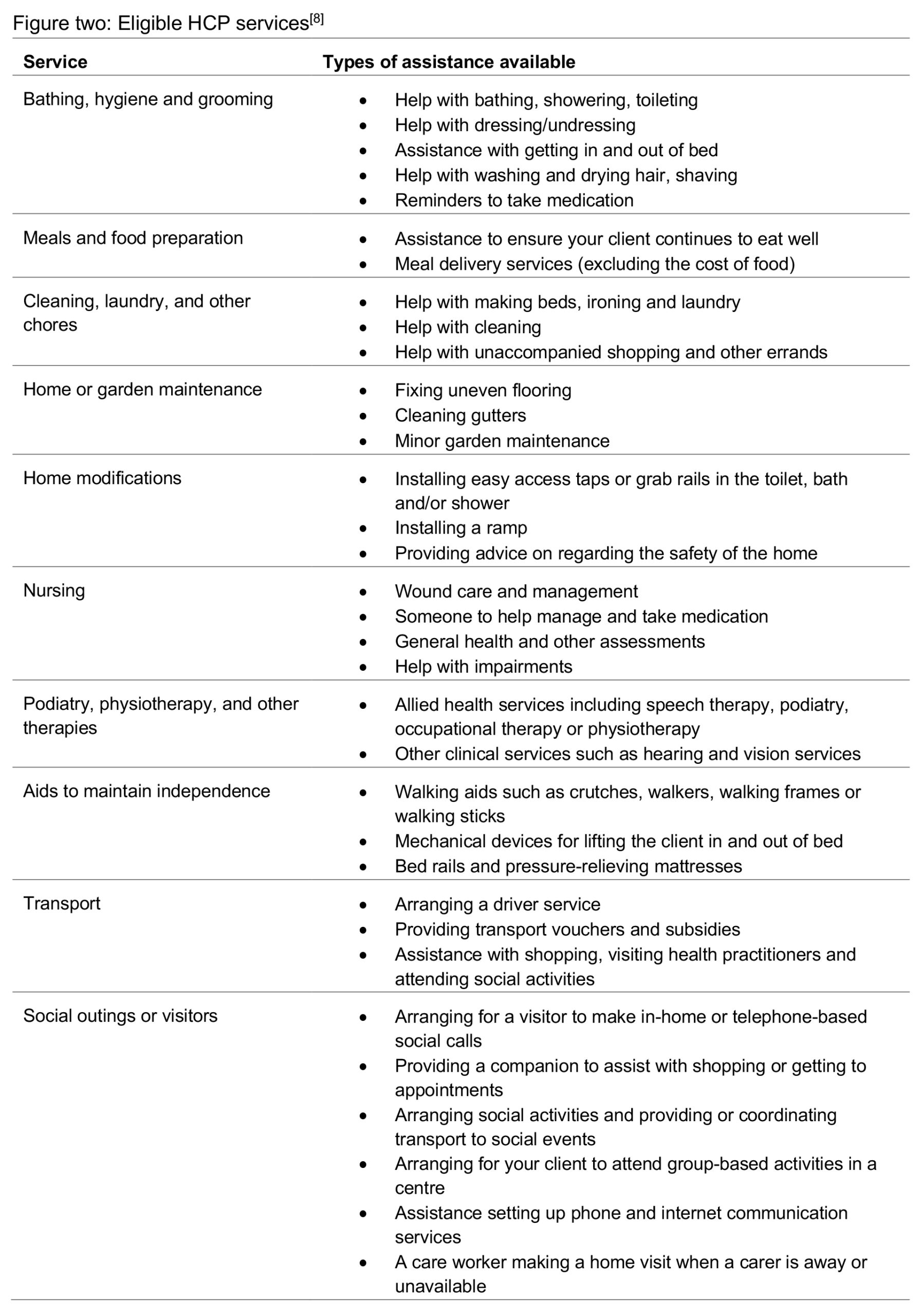

Once assessed and approved, your client will receive a letter outlining the subsidised services they have been approved for (figure two). The letter may also detail relevant organisations in your client’s area that can provide these services.

All services received by your client must be focused on providing them with care or assistance around the home. There are a number of things that your client can’t use package funds on, including:

- as a source of income

- groceries

- accommodation costs, including home purchase expenses, mortgage repayments or rent

- home modifications that don’t assist personal care needs

- holidays

- entertainment activities

- gambling.

Costs

Your clients will be expected to contribute to the cost of their care if they can afford to do so. How much they’re required to pay will vary and is dependent on the type and level of care and services provided. If your client needs a greater level of care than the HCP they’re allocated, their out of pocket expenses will be higher.

Each in-home care provider will likely have a different schedule of fees for their services. Your client needs to understand how the fees charged and government funding work together. This will help them to select the service provider that’s best placed to meet their budget and importantly, their care needs.

There are two different types of fee paid for by the consumer and that are set by the government.

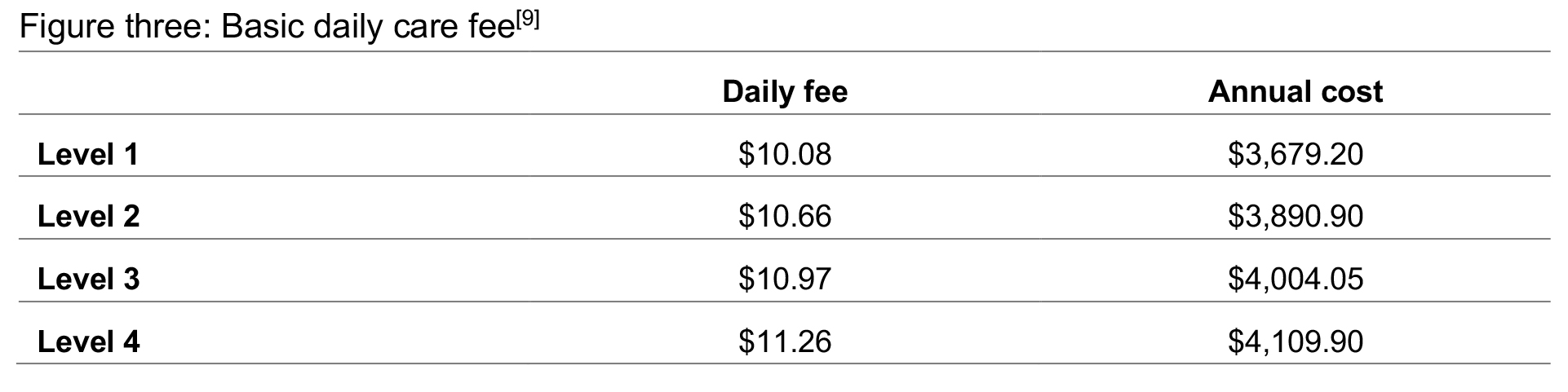

Basic daily care fee

This is a co-contribution towards your client’s HCP and is to the government funding and spent on your client’s care. It is calculated daily and paid monthly and is charged seven days per week. This fee increases on 20 March and 20 September each year. It’s shown as a daily or annual cost in figure three.

Income Tested Care Fee

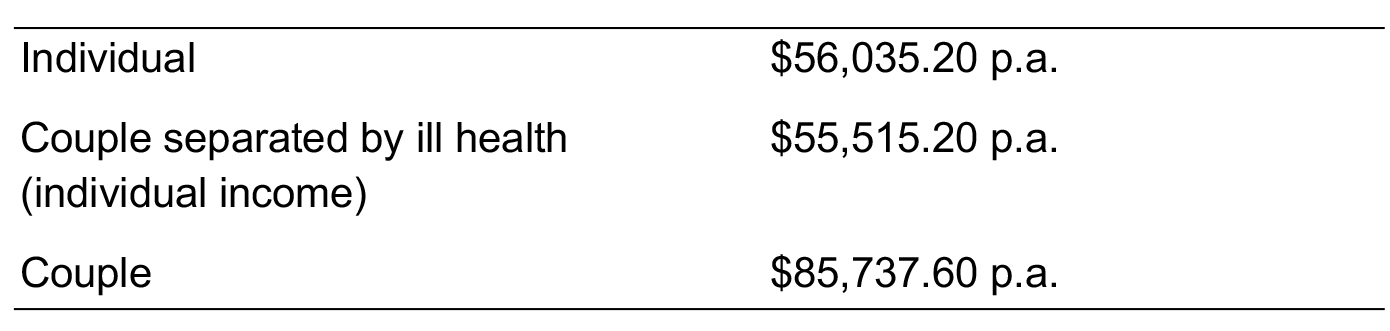

If your client is a partially or fully self-funded retiree, then they will most likely incur a means tested income tested care fee.

For the purposes of assessing your client for the income tested care fee, a retiree is considered self-funded if they meet the following annual income thresholds.

If an individual or couple meets or exceeds these income thresholds, they are deemed to be fully self- funded and need to pay the maximum income tested care fee.

For a fully self-funded retiree, the income tested care fee is $11,759.74 p.a. For those on a part pension, it’s a maximum of $5,879.85. Although it’s an income test, some assets like shares and bank accounts are deemed to earn a certain income for this assessment.

Unlike the basic daily care fee that is added to the HCP, if your client has to pay an income tested care fee then the government reduces the funding they pay by the same amount.

The maximum income tested care fee per year is $11,759.74 and there’s a lifetime threshold of $70,558.66.

There are also fees paid directly from the Home Care Package itself, so the consumer isn’t out of pocket, although they do erode the value of the package and what it can cover. These fees are:

- Case Management fee

- Home Care Package Management fee.

Private in-home care services

There has been an increase in the number of private services – a small number of higher profile services are provided below:

These organisations offer assistance with access to and the administration of in-home care services. Generally these providers will hold and administer an individual’s funding. However, this is conditional on the organisation meeting the CDC requirements and supports and facilitates individual consumer choice in relation to both the services received and the provider of those services.

Private providers can make it easier to compare service providers and costs and provide information and support to consumers. However, it’s important to note that there is no avoiding the necessary government assessments to access either in-home care program, irrespective of whether your client chooses to use one of these services.

In most cases, your client can either pay privately for the support services received through a private in-home care provider or use their HCP to pay for it. Depending on the level of care required and the client’s HCP, it may be a mix of government and private funding.

While accessing government funded in-home care packages is time consuming and often-times challenging, it’s a good way to enable your clients to live at home safely and comfortably. The statistics show that most older Australians want to avoid residential aged care for as long as possible, a desire likely heightened by the recent Royal Commission into the sector and the poor health outcomes highlighted by the Covid pandemic.

As noted earlier in the article, navigating the system is not for the faint hearted. Most people will need some assistance. Being available to your client to support them through this complex process will reaffirm the importance of your role as a trusted adviser and stand you in good stead with them – and in many cases – with the next generation of the family.

It’s likely that most of your clients will need to at least contribute to their in-home care and, in some cases, pay substantially above the available government funding. Planning to live at home is an important part of retirement planning. As your clients age, the cost of care will become an increasing proportion of their expenditure.

———-