What are the challenges facing growth style investment in the current market environment?

Global markets have entered a difficult period as fundamentals turn and inflation has emerged, somewhat more strongly than expected. As global economies faced a myriad of difficulties over the past couple of years, governments responded by supporting their economies through these crises with large amounts of debt. That, in turn, has meant the equilibrium level of interest rates has continued to get lower and lower.

While higher inflation is now driving interest rates back up, it is unlikely they are headed back to where they were previously; ultimately, we are still living in a low-rate world. Highly indebted governments and consumers cannot afford rates to reach levels much above three percent.

If rates do get too high, the risk is that economies will be pushed into recession and, as we are starting to witness, inflationary (and rate) fears are having a negative impact on equity markets.

All of this means it is a tough time for growth managers; in fact, growth equities have been under pressure for some time, with many of the problems in global equity markets apparent as early as March last year.

Like any trend, investment styles come in and out of favour. While growth stocks are likely to fall out of favour in the current environment, it’s worth revisiting what sets them apart.

Growth investing is focused on capital appreciation, generally investing in companies with above average growth. Growth stocks also tend to exhibit high levels of profitability and earnings growth ahead of their peer group.

Growth managers tend to look to the future, and typically invest in companies that have a solid earnings outlook, even if the share price appears expensive in terms of metrics such as the company’s price-to-earnings (P/E) ratio or price to book (P/B) ratio – the investor is willing to pay more today for a company’s future cash flows.

The characteristics of a typical growth company are as follows:

- high P/E and P/B ratios

- low or no dividends – earnings are reinvested to grow the business

- high earnings growth.

A growth style investment tends to do best in buoyant market conditions; it would generally outperform the market when share prices are rising. Growth stocks also tend to do well when interest rates are low.

Conversely, growth investments tend to lose value in a bear market, often falling faster and harder. Growth funds are generally expected to offer the potential for higher returns; however, growth stocks and funds can be more volatile and may represent a greater risk when compared to other investment styles.

Investors need to remember that in any market environment, earnings growth drives stock prices. It’s not an equity market. It’s a market of stocks. So those companies producing great earnings growth can continue to do so through any cycle. It may not happen in a straight line, but it will happen.

Market outlook

According to our global growth investment partner Munro Partners, it’s not all doom and gloom, despite the headlines. Munro’s team believes the bigger picture is a low-rate world continuing to underpin high asset prices in the medium to long term.

In the short term however, inflation is causing interest rates to go up. Expectations around interest rates have changed rapidly in the last 12 months alone. In March 2021, the US Federal Reserve was forecasting no rate hikes for the next three years. By December, estimates had increased to three rate hikes, rising to seven by March, with latest estimates at close to 10.

A simple way to think about markets is that if you take the earnings yield of the S&P500 and subtract the US 10-year bond yield, you need to get a carry – or positive return – for taking the risk of owning equities.

That carry has remained roughly the same, at three percent, for a number of decades. Markets might have gone up a lot, but interest rates have gone down a lot too, which means the market has not become more expensive.

We’re now seeing that equity risk premium move below 300 basis points for the first time in many years and that is creating volatility in equity markets. Fortunately, as long as you assume that interest rates won’t get much above three percent in the long term, that equation will work itself out over time.

Figure one depicts different movements in S&P500 earnings per share (EPS) growth, price-to-earnings (P/E) multiples and index growth over the past three decades. There are varying periods of P/E multiple expansion/contraction, EPS positive or negative growth and market movements.

We believe the most likely scenario for the year ahead is P/E multiple contraction and EPS growth. That is slower EPS growth this year with P/E contraction, and potentially reduced growth next year with more P/E contraction.

However, the worst-case scenario outcome – of P/E contraction and negative EPS growth – would require a significant proportion of large US companies to simultaneously experience earnings contraction, something Munro believes to be highly unlikely.

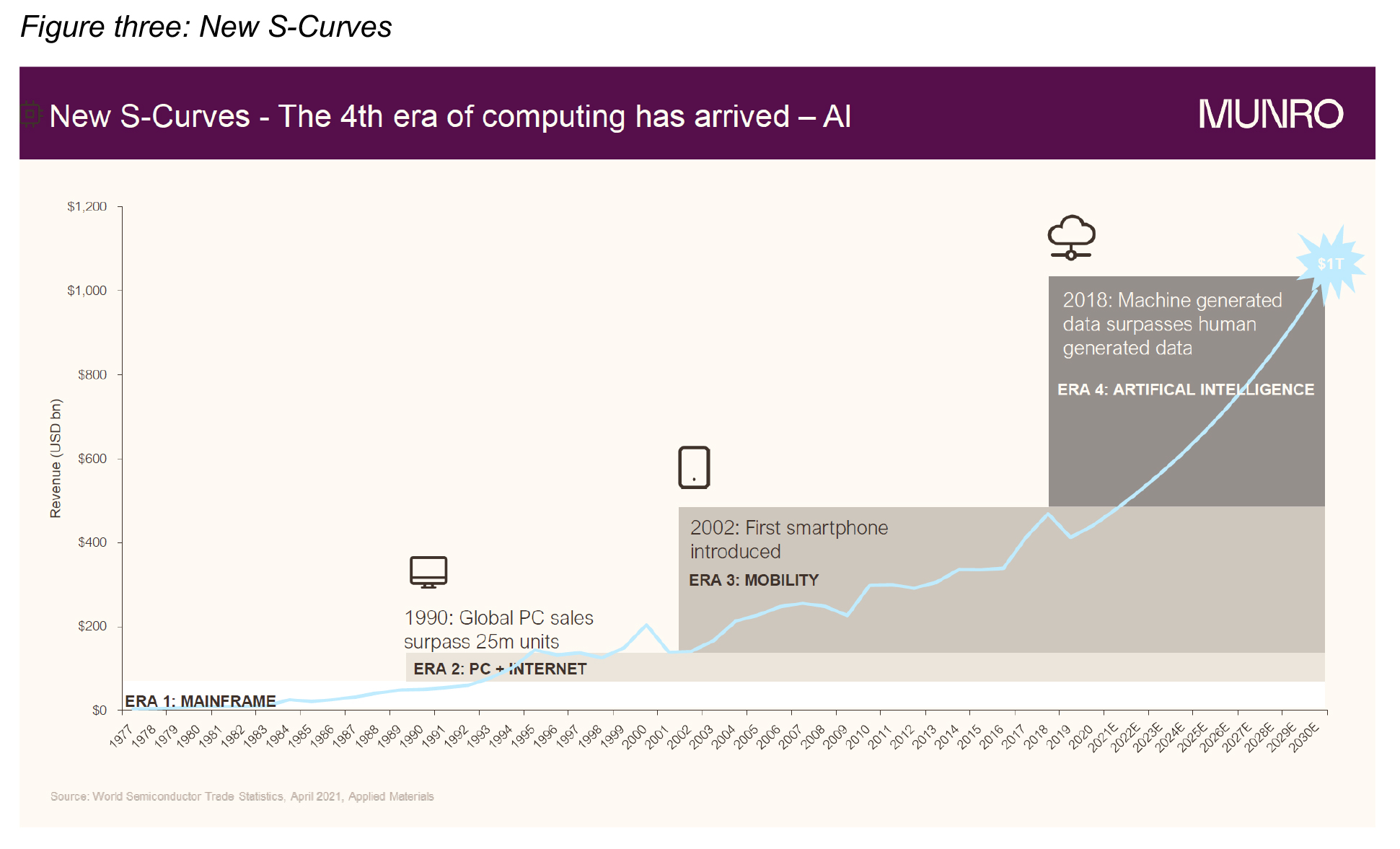

It’s important to note that growth equities have been under pressure for a while (figure two). The important thing is to focus on the identification of big technological and structural changes in society, which are a key component in recognising good companies – and invest accordingly.

The power of the S-curve

The S-curve tracks how a company or industry grows over its lifecycle. There comes a point in a lifecycle when growth inflects, driven by a structural change. It is the tailwind created by the structural change that allows a company to deliver and create wealth.

Facebook, Amazon and Apple have ridden the wave of demand for technology products and services that did not exist 15 or 20 years ago, but which are now considered indispensable in our daily lives.

To recognise the winners, investors need to identify both the next round of structural changes and the companies that will benefit from them. Importantly, this needs to be as close to the start of the S-curve as possible, and not at the end.

Areas of interest

As a growth investor, Munro identifies sustainable growth trends that are under-appreciated, not well understood and mispriced by the market, and in its view, the resulting winning and losing stocks. Investors invest in equities – not economies – and equities are driven by structural earnings growth, and this is why Munro focuses on identifying key areas of interest and structural change.

The team believes that the investment success stories of the future will emerge from within the big technological and structural changes affecting global society and focuses on identifying and understanding these trends, which it calls its Areas of Interest (AoIs).

With the advent of artificial intelligence and machine learning, the fourth era of computing has arrived (figure three) and with it, an S-Curve leading to a trillion dollar industry.

A key component for this technology is semiconductors, which have gone from a zero percent market nearly four decades ago, to half a trillion US dollars today. Semiconductors now are on their way to becoming a $US1 trillion business as we head into the fourth era of computing, or the artificial intelligence (AI) era of computing.

As every single device in the world becomes connected to the internet – from fridges to security systems, parking garages to electric vehicles – a multitude of data is going up into the cloud. Once there, it needs to be processed at incredibly fast speeds with AI to create predictive outcomes. This is already happening to some extent with, for example, streaming service, music and reading recommendations.

This high-speed data processing is going to require more GPUs or graphic processing units to create accelerated computing. Munro is forecasting that the server market has the potential to grow from roughly $US25 billion per annum today to nearly $US250 billion, or by a multiple of 10, by 2035.

There are just three or four companies worldwide in this highly focused business of high-performance computer architecture.

Case study: AMD

Advanced Micro Devices, Inc. (AMD) is an American multinational semiconductor company based in that develops computer processors and related technologies for business and consumer markets.

As shown in figure four, AMD’s earnings growth has grown structurally over time and will continue to grow as an increasing number of companies invest in this product. Not so long ago, investors had to pay 30 times earnings for AMD, but it is now available at 18 times earnings, even though it’s growing its earnings at 35 percent this year and is forecast to grow its earnings at 30 percent next year.

Decarbonisation and the climate opportunity

When it comes to climate, it’s at the beginning of its S-Curve. In 2020, global investment in the transition to low-carbon energy broke the $500 billion barrier for the first time[1]. This was spent on renewable power, electric vehicles and other technologies to cut the global energy system’s dependence on fossil fuels. The investments in the transition to a low-carbon economy showed a 9 percent increase over 2019 expenditure and came despite the Covid-19 pandemic.

Munro Partners likens the climate opportunity to the early stages of the technology boom, with many climate change companies set to get dramatically bigger.

However, funding this climate epidemic is going to be extremely costly. Given the ambitious carbon goals now being announced, Munro expects it to cost over $30 trillion US dollars between now and 2050. Figure five shows the estimated breakdown of where this huge investment will need to be made, and thus where the sectors of opportunity exist.

It’s important to note that the “zero carbon” 2050 target does not mean emitting any more carbon; it means emitting no carbon.

These ambitious political commitments are being mirrored in the corporate world, which rather than taking a ‘wait and see’ approach, is transitioning to a low carbon future independently of government mandates. Many corporations are changing their behaviour – or promising to – in the face of overwhelming demand for ESG and other socially responsible initiatives from customers, employees and shareholders.

Case study: Electric vehicles

At 2 percent of all passenger vehicles sold in 2021, electric vehicles may account for just a small percentage of total vehicle sales in Australia…but that has tripled over the past 12 months, according to the Electric Vehicle Council of Australia.

This trend will continue, as Australia catches up with the rest of the world. Of the $US50 trillion we forecast climate transition to cost globally, we expect that around 18% will be in passenger electric vehicles and clean transport.

The overall number of total vehicles sold may not increase dramatically over the next 25 to 30 years, but electric vehicle penetration of the total market definitely will and is forecast to grow from less than 10% now, to as much as 50% by 2050, as figure six shows.

The obvious investment for this sector is Tesla but it trades at a price earnings multiple of around 50 times. In Munro’s opinion, there are other cheaper companies in the supply chain.

An example of this is the semiconductor industry. Most modern vehicles need semiconductors, but electric vehicles need twice as much semiconductor content as your average internal combustion engine vehicle. An autonomous electric vehicle needs twice as much semi-conductor content again.

Companies involved in battery production and charging, as well as lithium mining and production, are also all set to likely benefit from increasing market penetration of electric vehicles.

There is no doubt it’s a tough time to be investing in growth stocks but by continuing to identify the structural areas of interest, such as accelerated computing and electric vehicles, growth fund managers and investors can take advantage of lower prices and be well positioned when the market and interest rates do return to some level of normality.

———–