Bringing growth and inflation together in asset allocation decisions

How does growth, inflation and real rates influence portfolio strategy in uncertain and changing times?

This is our final article of three aimed at providing advisers with a framework around asset allocation that will assist with client discussions and portfolio strategy in these uncertain and changing times.

In our first two articles (CPD: The importance of growth regimes to asset allocation decisions and CPD: The importance of inflation regimes to asset allocation decisions) we examined the influence of first growth, and then inflation and real rates on asset returns. In this article we explore the interaction between these factors and how this can be used to help deliver a better asset-allocation outcome. We also look beyond traditional assets and extend our framework to alternatives – opening new ways to seek both returns and portfolio diversification in a world where government bond yields remain at the lower end of their historical ranges.

Recapping our growth and inflation frameworks

When assessing growth dynamics, one of the best sets of timely indicators is the purchasing managers’ indices (PMIs), which reflect the health of an economies manufacturing and service sectors. A carefully selected group private sector companies are surveyed, providing valuable insights into the underlying trends being experienced in each sector. Data is then aggregated into a PMI index for the economy as a whole – a score above 50 indicating that activity is improving, and a score below 50 indicating contraction. For inflation, we look at both the current rate of inflation, as measured by a country’s consumer price index, and the expected future rate of inflation, as measured by breakeven inflation[1].

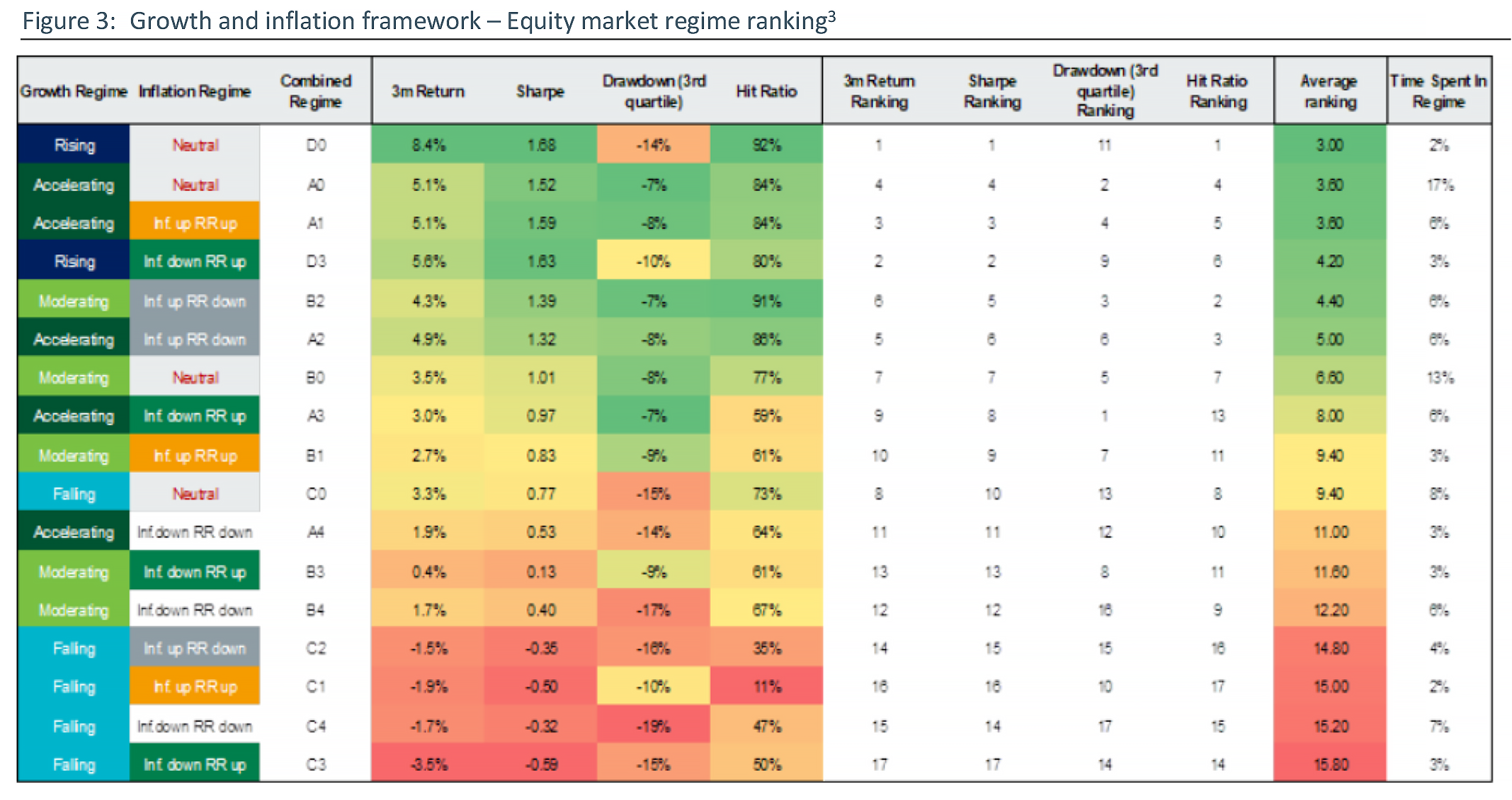

From a growth perspective, the sweet spot for risk assets has historically been an Accelerating growth regime (A). During these times, the correct asset-allocation strategy has been to skew towards pro-cyclical exposures such as equity markets. The Falling growth regime (C) is the only one in which average equity market returns have historically been negative. Volatility tends to be much higher when PMIs are sub-50 (regimes C and D) and the historic range of drawdowns seen in regime C are more extreme than in any other growth regime.

When we extend our framework to assess the impact of inflation, one finding that seems somewhat counterintuitive is the extent to which higher CPI, breakevens and real rates appear to be the most constructive environment for risk assets, such as equities. Regime E, where both inflation and real rates are rising, has historically been the best environment for equity markets while regime H, a combination of sharply falling rates and inflation has historically been the worst environment for risk assets. In regime E, returns are often negative; equity drawdowns are worse than in any other environment and equity volatility is highest. With this backdrop it is unsurprising that regime E is also historically the best regime for government bonds and investment grade credit.

When we combine regimes, it allows more nuanced analysis

Combining the growth and inflation view helps to clarify not only what the prevailing environment means for an asset’s performance but also how those prospects may change as economic conditions evolve.

For example, for equities, a shift from an Accelerating growth environment to a Moderating one clearly implies a move to a less impressive (though solid) backdrop for equity returns. However, if growth is still robust enough to keep inflation rising then the risk-adjusted returns potentially on offer remain favourable – especially if the cost of capital (real rates) is falling at the same time (see Figure 2, combined regime B2).

On the other hand, if a shift from Accelerating growth to Moderating occurs against a backdrop where inflation and real rates are also declining sharply, there is a risk that the environment is sufficiently weak that this is simply a step in a transition to a Falling growth regime. Falling growth regimes are the worst environments from an equity perspective (combined regimes C1 to C4) – historical returns and drawdowns have been particularly unappealing regardless of the direction of inflation and real rates.

We can also see from Figure 2 that rising growth environments (generally where economies are recovering from recession) tend to be associated with the most spectacular equity returns – but the amount of time spent in these regimes is fleeting. Indeed, identifying such periods is akin to ‘buying stocks at the bottom’ – an easy concept to grasp but somewhat harder to execute in practice.

Extending our framework to other asset classes

As the most volatile of the mainstream assets within a multi-asset portfolio, understanding the likely performance characteristics of equity markets is at the forefront of our thoughts. However, we can use our framework to assess a range of both traditional and alternative assets.

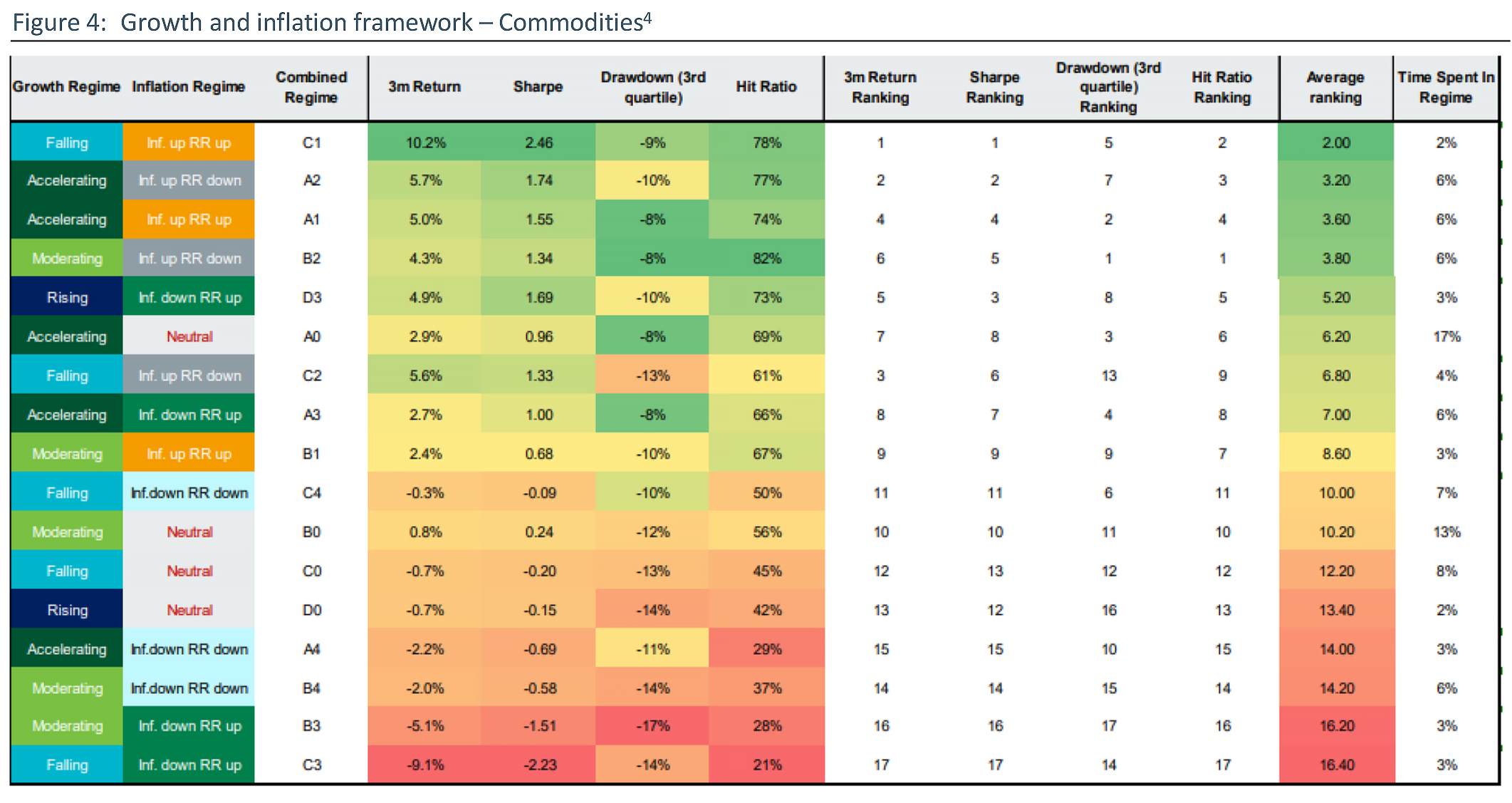

While growth is the most important for equity market returns, for commodities it is the direction of inflation that matters most (see Figure 4). The top four regimes for commodities are those where inflation is rising, while the four worst regimes are when inflation is falling. This is intuitive given the intrinsic linkage between commodity prices and inflation, but it serves to reaffirm the usefulness of viewing assets within an economic regime framework.

Similarly, for the trade-weighted dollar (Figure 5) the most dominant driver is the direction of real rates. This is once again an intuitive result as high real interest rates act as a natural draw for international capital seeking the most attractive returns.

Looking beyond traditional asset classes

To access a truly broad opportunity set, we believe that a multi-asset strategy must take a flexible approach that gives access to both traditional, directional assets and alternative, less directional assets. With government bond yields towards the lower end of their historical ranges, alternative strategies can offer opportunities from both a risk mitigation and return generation perspective – offering a different way to add diversification at a time when traditional sources of diversification may prove less reliable than in the past. The asset allocation framework described in this article can be just as applicable to these alternative strategies.

To illustrate, in Figure 6 we compare a range of alternative diversifiers across two of the regimes in our growth framework. These include equity factor-based strategies (momentum, volatility, quality buybacks vs dividends as well as value/growth), traditional relative value trades (developed markets versus emerging markets, credit spread compression and equities versus bonds) as well as traditional hedges (option strategies, defensive currency strategies and government bond and yield curve trades). All factor-based strategies are based on US equities and use the broader US market as their funding leg.

Looking at their historical performance, the classic factor-based strategies such as ‘value versus growth’ appear to offer little from a regime perspective although cyclicals versus defensives behave in a logical manner. Hedging strategies tend to be a drag on performance in accelerating regimes (which is when risk asset returns are greatest) but perform well in a moderating regime.

In the current environment, with government bond yields still at low levels and with inflation uncertainty high, alternative strategies such as developed versus emerging market equities or defensive currency trades, can offer different ways to diversify a portfolio rather than relying on traditional assets such as government bonds.

Conclusion

Across the three articles, we have shown the importance of growth, inflation and real rates within an asset allocation framework and the importance of the interaction between them. The dominant influence within the growth and inflation mix differs significantly across asset classes. While growth is the most important for equity returns, the direction of inflation matters most for commodities and real rates for the US dollar. Regimes that are highly positive for certain asset types, can be the worst regimes for others.

Although the pandemic was brutal in terms of the size of economic drawdown and the rapidity in which it took place, the recovery has, so far, followed the same trajectory as historical precedent. This has reaffirming our belief in the clarity of our framework as we look to the new growth and inflation challenges we expect in the post-pandemic world.

We trust that this series of three articles has been a helpful reference point for discussions with clients on portfolio strategy. We are working on a research piece on the importance of assessing financial conditions and look forward to sharing that in due course.

By Matthew Merritt, Head of Multi-Asset Strategy Group

Read part 1: CPD: The importance of growth regimes to asset allocation decisions

Read part 2: CPD: The importance of inflation regimes to asset allocation decisions

———

Notes:

[1] Source: For illustrative purposes only

[2] A consumer price index measures the rate of change in prices for a basket of goods and services that are typically purchased by households, breakeven inflation is the rate of inflation at which a country’s nominal government bonds would generate the same return as inflation-linked government bonds. This gives us the level of future inflation that markets are currently pricing in.

[3] Ibid.

[4] Ibid.

[5] Ibid.

[6] Ibid.

———

IMPORTANT INFORMATION

RISK DISCLOSURES

Past performance is not indicative of future results. Investment in any strategy involves a risk of loss which may partly be due to exchange rate fluctuations.

The performance results shown, whether net or gross of investment management fees, reflect the reinvestment of dividends and/or income and other earnings. Any gross of fees performance does not include fees, taxes and charges and these can have a material detrimental effect on the performance of an investment. Taxes and certain charges, such as currency conversion charges may depend on the individual situation of each investor and are subject to change in future.

Any target performance aims are not a guarantee, may not be achieved and a capital loss may occur. The scenarios presented are an estimate of future performance based on evidence from the past on how the value of this investment varies over time, and/or prevailing market conditions and are not an exact indicator. They are speculative in nature and are only an estimate. What you will get will vary depending on how the market performs and how long you keep the investment/product. Strategies which have a higher performance aim generally take more risk to achieve this and so have a greater potential for the returns to be significantly different than expected.

Any projections or forecasts contained herein are based upon certain assumptions considered reasonable. Projections are speculative in nature and some or all of the assumptions underlying the projections may not materialize or vary significantly from the actual results. Accordingly, the projections are only an estimate.

Portfolio holdings are subject to change, for information only and are not investment recommendations.

ASSOCIATED INVESTMENT RISKS

Multi-asset

-

Derivatives may be used to generate returns as well as to reduce costs and/or the overall risk of the portfolio. Using derivatives can involve a higher level of risk. A small movement in the price of an underlying investment may result in a disproportionately large movement in the price of the derivative investment.

-

Investments in bonds are affected by interest rates and inflation trends which may affect the value of the portfolio.

-

The investment manager may invest in instruments which can be difficult to sell when markets are stressed.

-

Property assets are inherently less liquid and more difficult to sell than other assets. The valuation of physical property is a matter of the valuer’s judgement rather than fact.

-

While efforts will be made to eliminate potential inequalities between shareholders in a pooled fund through the performance fee calculation methodology, there may be occasions where a shareholder may pay a performance fee for which they have not received a commensurate benefit.

ESG

-

Investment type: The application and overall influence of ESG approaches may differ, potentially materially, across asset classes, geographies, sectors, specific investments or portfolios due to the nature of the specific securities and instruments available, the wide range of ESG factors which may be applied and ESG industry practices applicable in a particular investable universe.

-

Integration: The integration of ESG factors refers to the inclusion of ESG risk factors alongside financial risk factors in investment analysis and research to judge the fair value of a particular investment and may also include the monitoring and reporting of such risks within a portfolio. Integrating ESG factors in this way will not typically restrict the potential investable universe, but rather aims to ensure that relevant and material ESG risks are taken into account by analysts and/or portfolio managers in their decision-making, alongside other relevant and material financial risks.

-

Ratings: The use and influence of our ESG ratings in specific investment strategies will vary, potentially significantly, depending on a number of factors including the nature of the asset class and the structure of the investment mandate involved. For an investment portfolio with a financial objective, and without specific ESG or sustainability objectives, a high or low ESG rating may not automatically lead to a buy or sell decision: the rating will be one factor among others that may help a portfolio manager in evaluating potential investments consistently.

-

Engagement activity: The applicability of Insight firm level ESG engagement activity and the outcomes of this activity relating to buy, hold and sell decisions made within specific investment strategies will vary, potentially significantly, depending on the nature of the asset class and the structure of the investment mandate involved.

-

Reporting: The ESG approach shown is indicative and there is no guarantee that the specific approach will be applied across the whole portfolio.

-

Performance/quality: The influence of ESG criteria on the overall risk and return characteristics of a portfolio is likely to vary over time depending on the investment universe, investment strategy and objective and the influence of ESG factors directly applicable on valuations which will vary over time.

-

Costs: The costs described will have an impact on the amount of the investment and expected returns.