The inflationary implications of deglobalisation, demographics and decarbonisation

The next decade is going to look quite different than the 2010s.

In a reflationary environment, GSFM’s investment partner Epoch expects investors to exhibit an increased focus on capital allocation, as well as quality and sustainable free cash flow. All is explained in this article from Epoch Investment Partners.

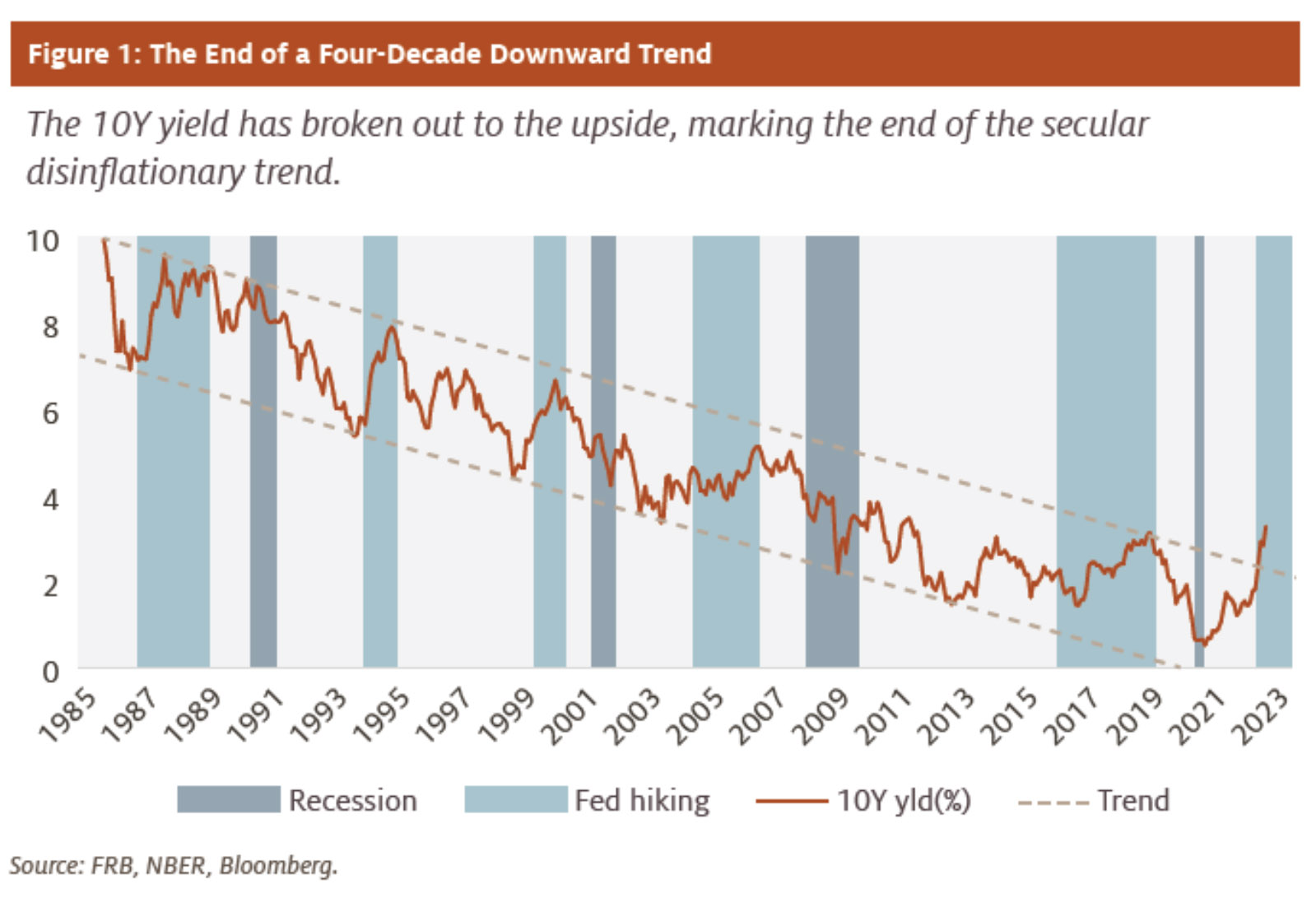

Until recently, we had been in a disinflationary environment since the 1980s, when Volcker helmed the US Federal Reserve (Figure 1). This secular trend reflected three forces:

- correcting the policy mistakes made in the ’60s and ’70s that stoked stagflation

- the increasingly globalised nature of trade, investment, and finance from the mid-1980s

- the deflationary impact of tech, which has been especially impactful during the last two decades.

While the latter factor remains in place, we believe it is being overwhelmed by the 3Ds — deglobalisation, demographics and decarbonisation — meaning we have entered a secular reflationary environment.

Deglobalisation: Unwinding the law of comparative advantage

The two decades from 1985 will go down in history as an unprecedented period of hyper-globalisation. Trade barriers were reduced partially because of trade agreements (e.g., NAFTA, the European Single Market and the Uruguay Round), but the wave was led by developing countries in Latin America and Asia and formerly communist countries in Eastern Europe that undertook unilateral reforms[1].

However, globalisation has been in retreat for over a decade (Figure 2), a trend we attribute to four developments:

- China’s mercantilist, self-reliance policies (e.g., China 2025 and Common Prosperity)

- western populists, whose influence has soared since 2016 (partially in reaction to China’s policies)

- COVID-19, which demonstrated how vulnerable we are to extremely fragile global supply chains (e.g., for access to Active Pharmaceutical Ingredients (API) and Personal Protective Equipment (PPE) as well as semiconductors and lithium batteries

- Russia’s invasion of Ukraine, which has particularly impacted trade in oil, natural gas and wheat.

Of the four factors driving the trend toward deglobalisation, by far the most important is China’s mercantilist approach. This is best illustrated by their ‘dual circulation model’ which emphasises ‘international circulation’ (moving up the value chain in exports) and ‘internal circulation’ (expanding domestic demand). China’s aggressive form of state capitalism increasingly promotes self-reliance (in energy, food, semiconductors, AI, batteries, lithium, rare earth metals, and so on), so that industrial policies rather than comparative advantage are what drives trade and capital flows[2].

Adam Posen of the Peterson Institute emphasises the world is set to look a lot messier, as it is increasingly bifurcated into two economic blocs: one aligned with US and the other China. Even though the blocs won’t include every country, and some countries will engage with both the US and China, many countries will feel growing pressure to align with one or the other.

Dani Rodrik of Harvard stresses a paradox at the core of deglobalisation. China has been the greatest beneficiary of the hyper-globalisation game, but that is largely because it never had the intention of playing by the rules. Chinese policy makers put in place extensive industrial policies, provided huge subsidies to infant industries, tightly managed the RMB, restricted cross-border capital flows, and infringed on IP rights, all in violation of WTO rules. To Rodrik, China benefited so much from hyper-globalisation specifically because it manipulated the rules of the world economy to its advantage, essentially free riding on the openness of countries like the US.

One direct consequence is that China will likely be deglobalisation’s biggest loser. This reflects dwindling export opportunities as well as China’s waning access to advanced technologies, such as next-gen semiconductors. Moreover, decoupling will insulate Chinese companies, reducing competitive pressures and resulting in a less innovative and dynamic economy[3].

Deglobalisation has numerous implications, but here we’ll just emphasise three.

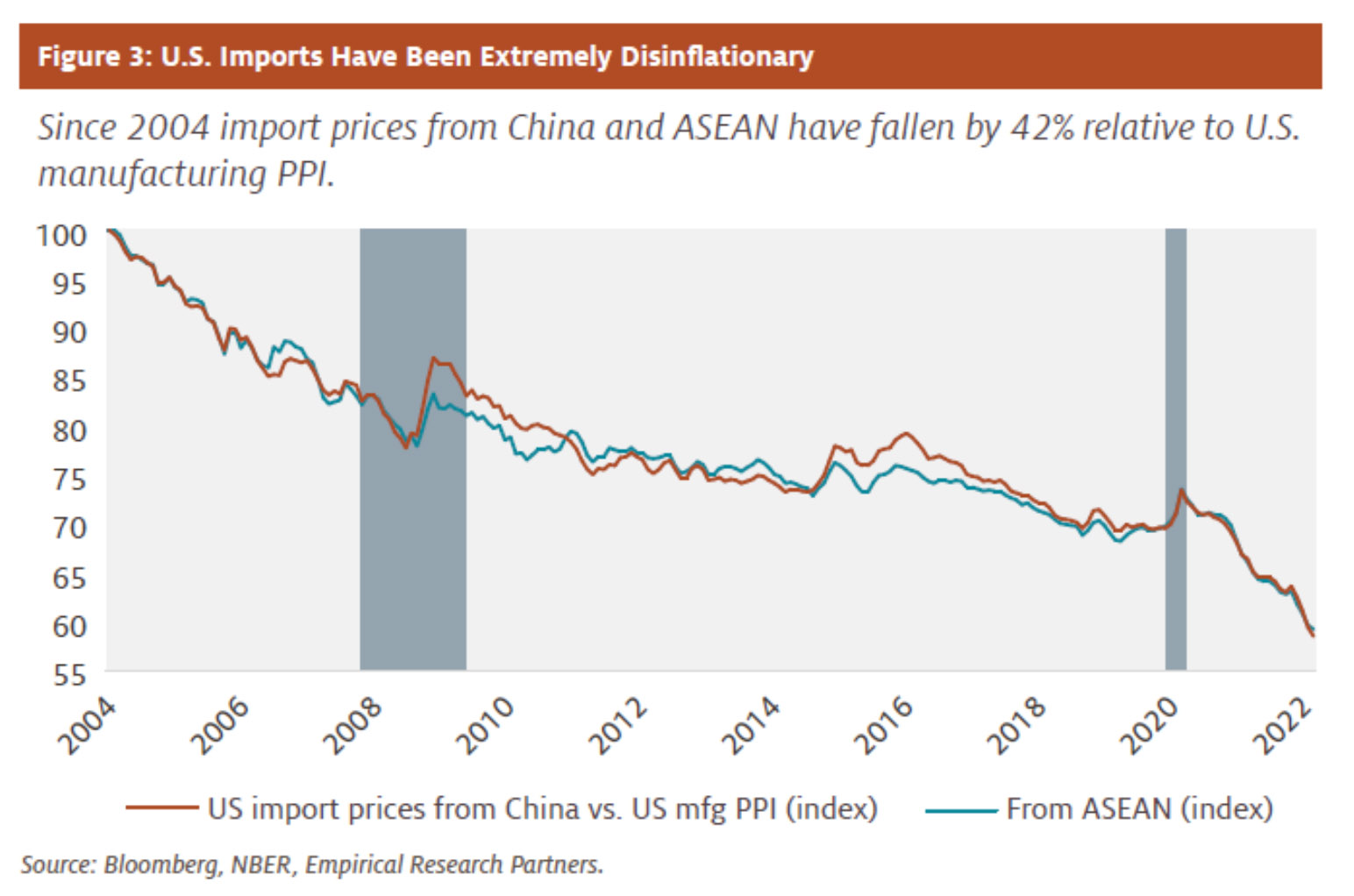

First, hyper- globalisation has been deflationary (Figure 3), but we expect this effect to wane over coming years. Second, the China Shock reduced US manufacturing employment and dampened domestic wage gains[4].

Although these trends have been important since at least 2001 when China entered the WTO, they are likely to be at least partially reversed as America brings some jobs back via on-shoring and friend-shoring. For example, Goldman Sachs forecasts ‘Slowbalisation’ will boost annual core PCE inflation by 0.4 ppt, which strikes us as a reasonable estimate.

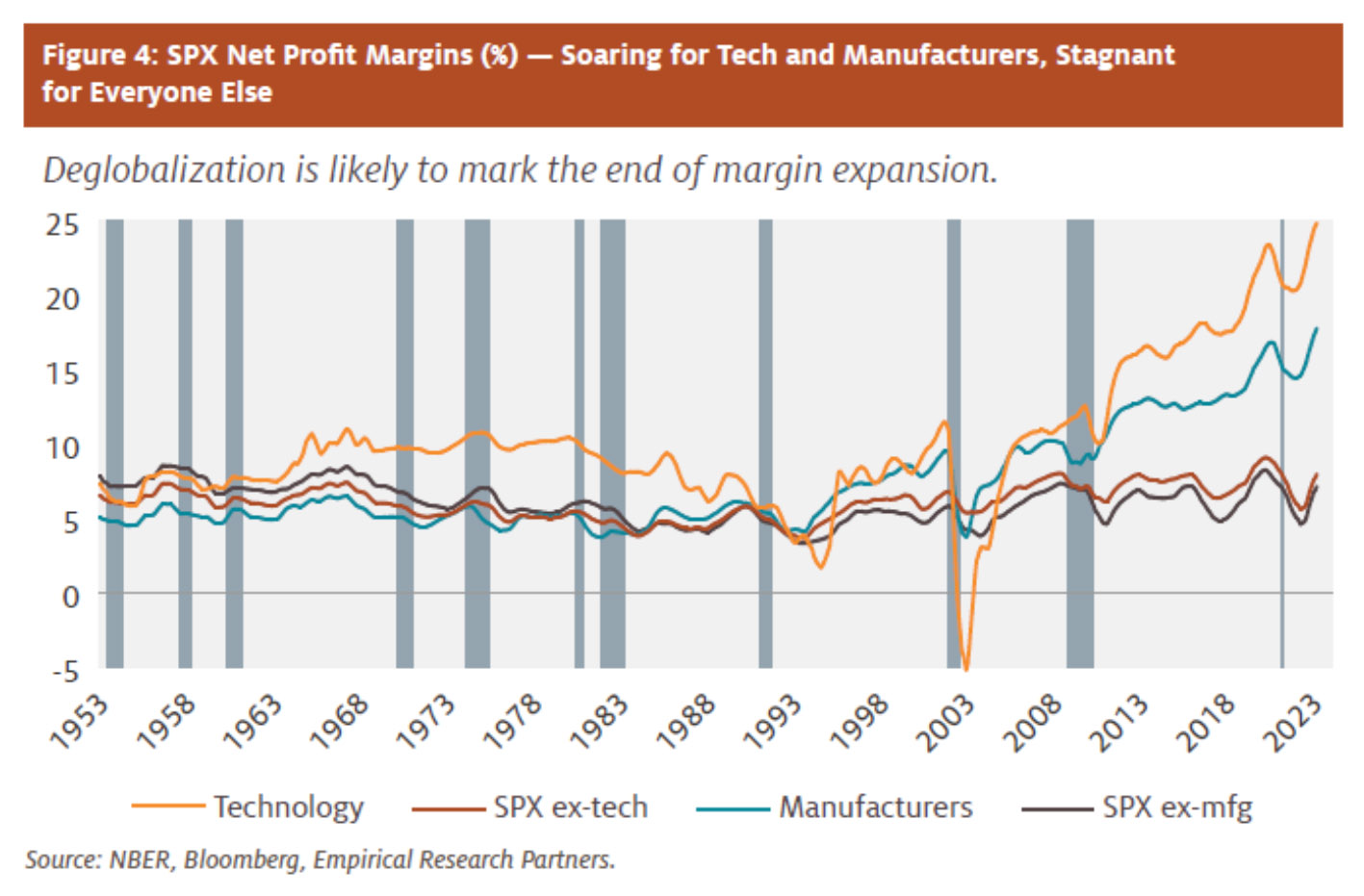

Third, corporate margins, especially for tech and manufacturers have been turbo-charged by four features of hyper-globalisation: highly efficient supply chains, wage savings, lower interest rates and reduced tax rates (Figure 4). With globalisation in retreat, we expect margins to compress, especially for tech and manufacturing.

Demographics: Following the path of Europe and Japan

Turning to the second ‘D,’ US population growth is expected to average 0.6% annually this decade, half the rate experienced from 1950–1999. Moreover, the US Census Bureau expects population growth to continue slowing during the following three decades. This partly reflects dwindling immigration growth, which has declined from 4.6% annually in the 1990s to less than 1% in recent years.

A key consequence of these two trends is a rising dependency ratio (DR, the ratio of older dependents, over 64 years, to the working-age population, 15–64). The DR ratio is rising in all major economies, but its acceleration is especially notable in China and Europe.

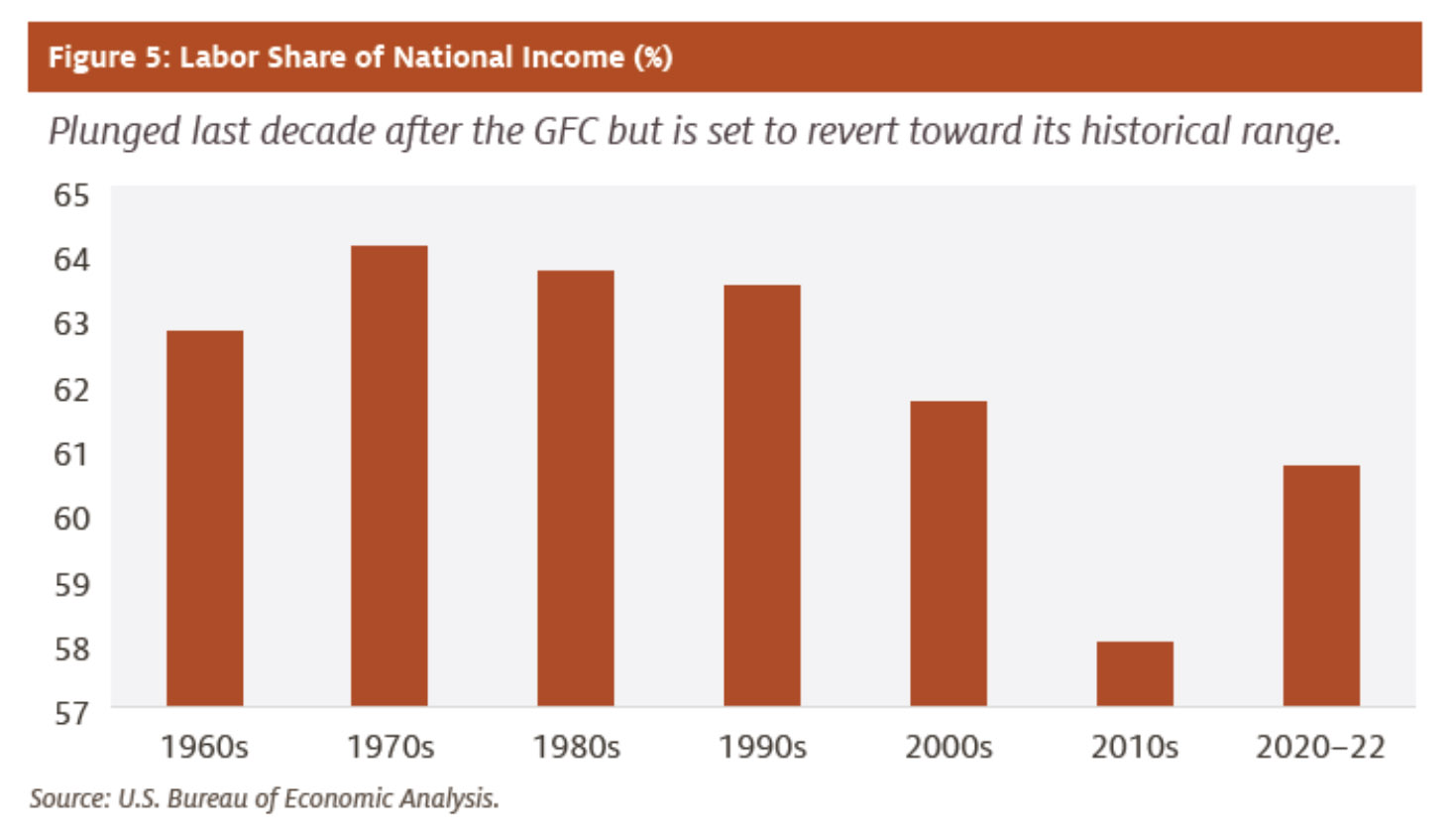

Slowing population growth and a higher DR has a number of implications, including: rising public debt and deficits, lower top-line growth for corporates, and tighter labour markets which means stronger wage growth. The latter, which is also a feature of deglobalisation, implies a higher labour share than was experienced last decade (Figure 5).

This share plummeted during the 2010s, falling to 58%, but is now moving up toward the historical range of 62–64%. We also expect a higher DR to induce a reduction in the savings glut, which will tend to raise interest rates across the board.

Decarbonisation: The energy transition will prove inflationary

The third ‘D’ is decarbonisation. There are four reasons why we expect ‘greenflation’ to become a major economic force[5] in the transition to Net Zero Emissions (NZE).

First, global capital investment in energy is expected to more than double by 2030. The energy industry has been under-investing since 2014, and the investments required in electricity generation and infrastructure are emphatically massive. Further, the average capex intensity of low carbon energy is roughly twice that of hydrocarbons.

Second, the transition involves tremendous increases in demand for ‘green metals’ (lithium, cobalt, nickel). The transition has only just started, but already the prices of most green metals have already more than tripled.

The third is ‘green premiums’, which represent the additional cost of choosing a clean technology over a traditional one. To achieve NZE it is critical to eliminate Green Premiums, which can be done by either making green technologies cheaper (through innovation and scale) or fossil fuels more expensive (through carbon taxes or regulations). While renewable electricity is getting cheaper, this will take time and until then, the transition involves higher costs and is inflationary.

Finally, most green technologies remain significantly more expensive than their fossil-fuel counterparts. While ‘green premiums’ will decline with innovation and scale, in many cases this will take decades and until then, the transition involves higher costs and is inflationary.

The transition from brown to green energy will likely be messy. Energy transitions always take a very long time, especially when green energy investment is not ramping up nearly quickly enough, half the technologies needed to achieve NZE by 2050 don’t yet exist on a commercial basis, and enormously outdated laws and regulations stymie innovation. A disorderly handover implies periodic supply shortages and even more volatile energy prices.

While inherently imprecise, we estimate these factors will increase trend inflation by 25 to 50 basis points over the next decade. The confluence of greenflation plus the reflationary effect of deglobalisation is likely to more than counterbalance the deflationary impact of tech. Consequently, inflation and nominal interest rates will be higher and more volatile, especially relative to the levels of the last two decades.

Implications for investors

We believe reflation and greater macro volatility implies an increased focus on capital allocation, quality and sustainable free cash flow (FCF). A good record of capital allocation includes making sound investments that grow earnings.

The next decade is going to look quite different than the 2010s when the 10-year yield averaged 2.4% and inflation trended well below the 2.0% target. We are saying farewell to the ‘Great Moderation’ and opening the door to higher macro and inflation volatility. This includes more robust wage growth and a labour share that is elevated relative to the experience of the last two decades. For policy makers, this means less room for stimulus, both monetary and fiscal. Modern Monetary Theory (MMT) has been tossed in the dustbin, although the legacy of high fiscal debts and deficits is inescapable.

Investors should be prepared for lower top-line growth, as implied by each of the 3 Ds. Moreover, margins have been turbo-charged by globalisation and lower interest rates, trends which are now well behind us. This implies tighter margins for many sectors, especially tech hardware and manufacturing.

Further, higher inflation and bond yields compared to the 2010s comprise a headwind for long-duration assets, including speculative tech, biotech, and venture capital. In addition to greater volatility and a forceful rotation in sector leadership, expect equity markets to deliver lower prospective returns relative to that experienced since the GFC. With a ‘fatter and flatter’ return profile, investors are likely to require higher equity risk premia and prioritise reliable earnings, which implies a focus on quality and sustainable FCF.