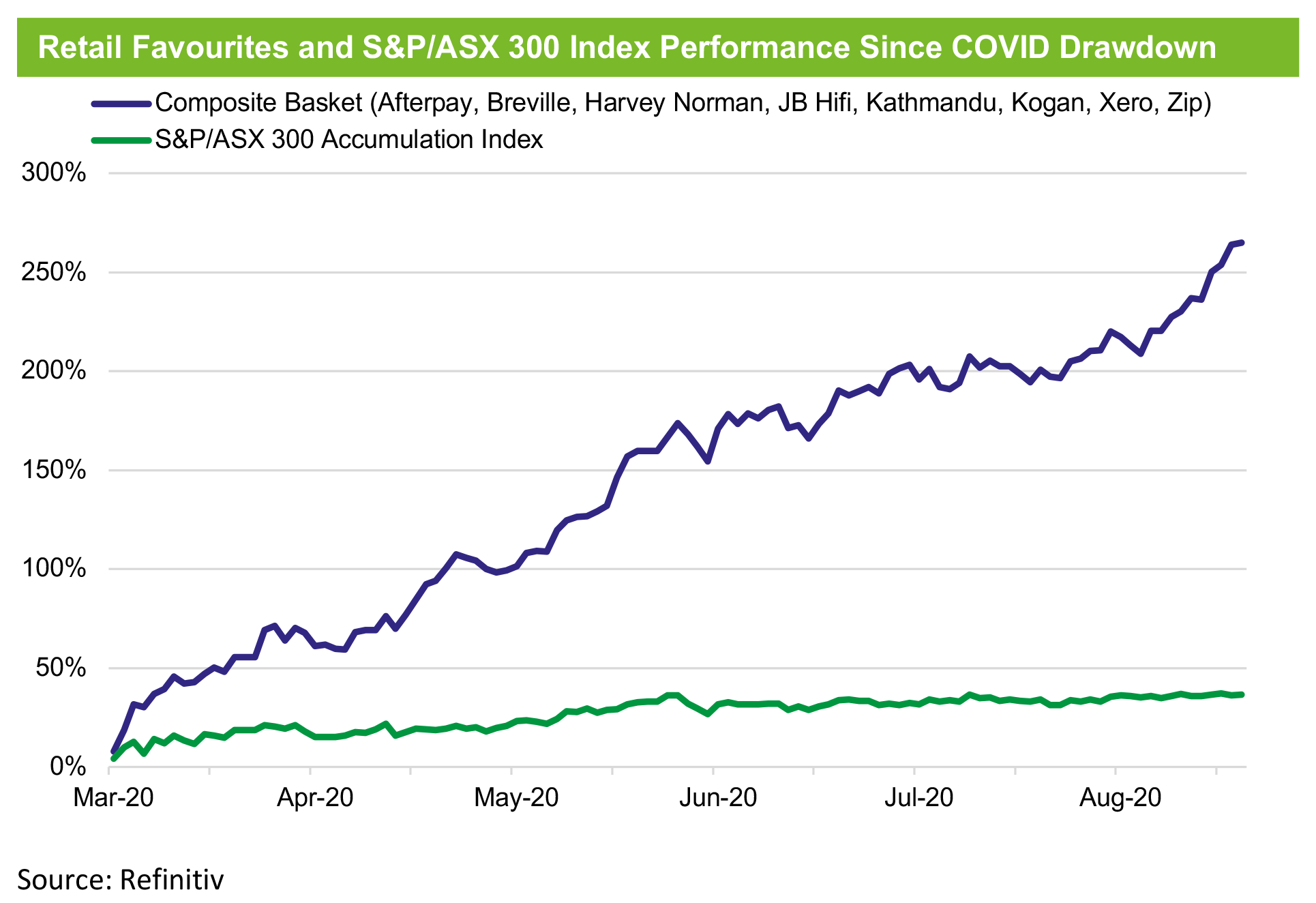

In our September 2020 article “Amateur investors beware: you’ve got to know when to hold ‘em, know when to fold ‘em”, we highlighted the dangers of a ‘do it yourself’ approach to investing. By the end of August 2020, popular stocks, defined as those with strong brand recognition and historic price momentum, materially outpaced the broader market, as displayed in the chart below.

Retail investors who backed these popular stocks had every right to question the notion of handing over their hard-earned savings to a professional investor.

What’s happened since?

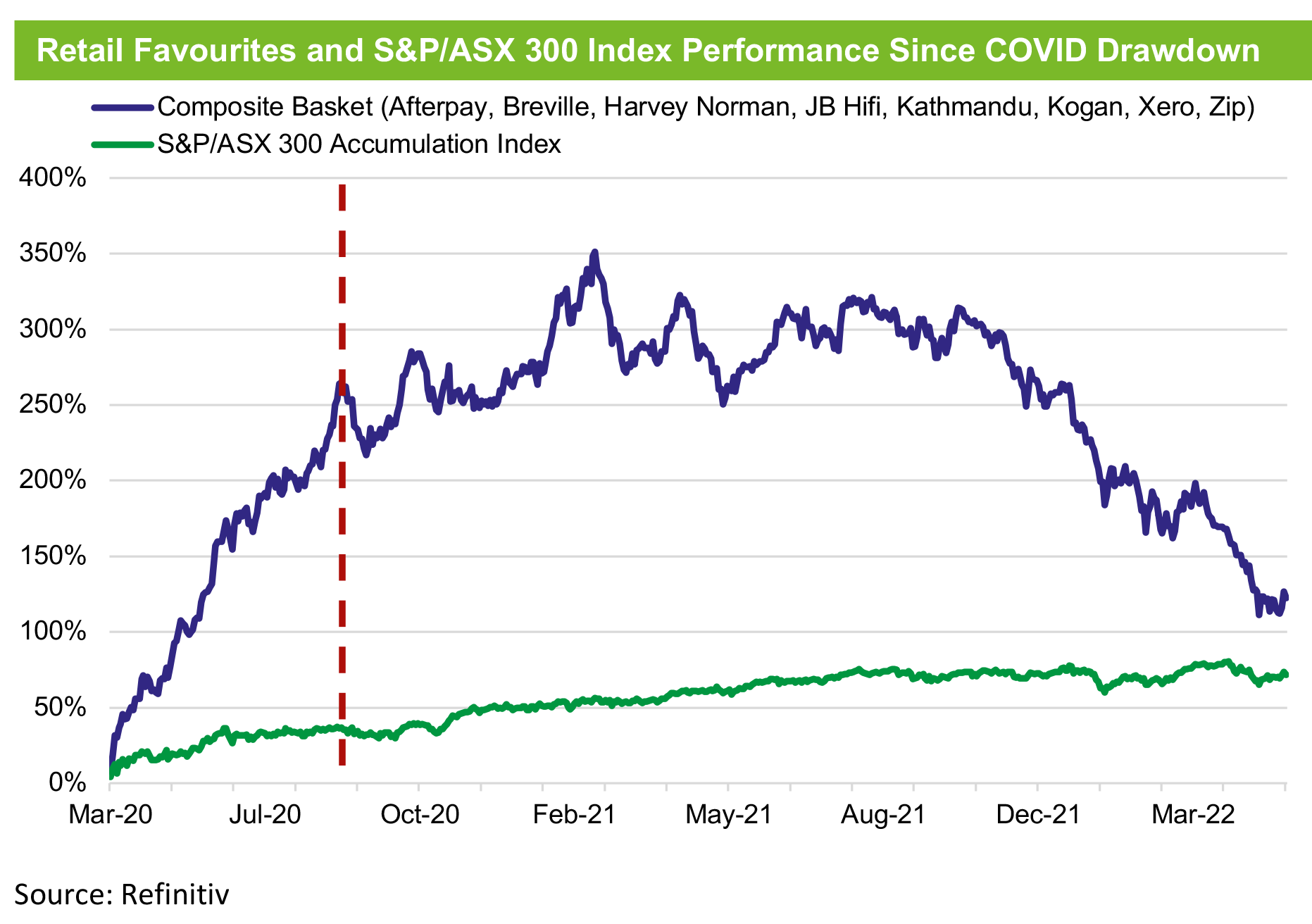

Fast forward almost two years, have the same popular stocks run out of steam? The below chart shows the performance of these stocks relative to the broader benchmark since our initial note in September 2020, as represented by the dashed line.

The basket of popular stocks has experienced a significant sell-off since September 2020, falling approximately 39% (as at 31 May 2022). Comparatively, the broader benchmark continued its upward trajectory, rising 27% and outperforming the basket by 66%. Furthermore, if an investor was caught up in the frenzy and purchased the basket at the peak, they would have experienced a drawdown of approximately 51% (as at 31 May 2022). We note that, following recent market movements, the basket’s drawdown has extended a further 11% (as at 17 June 2022).

How can professional long/short managers capitalise on this?

Active fund managers seek out market inefficiencies, which in this instance, potentially appeared when the share prices of the popular companies began rallying with arguably minimal fundamental basis. Unlike long-only managers who are restricted to purchasing stocks, long/short managers can capitalise on these inefficiencies by short selling stocks that they believe are overpriced or overhyped.

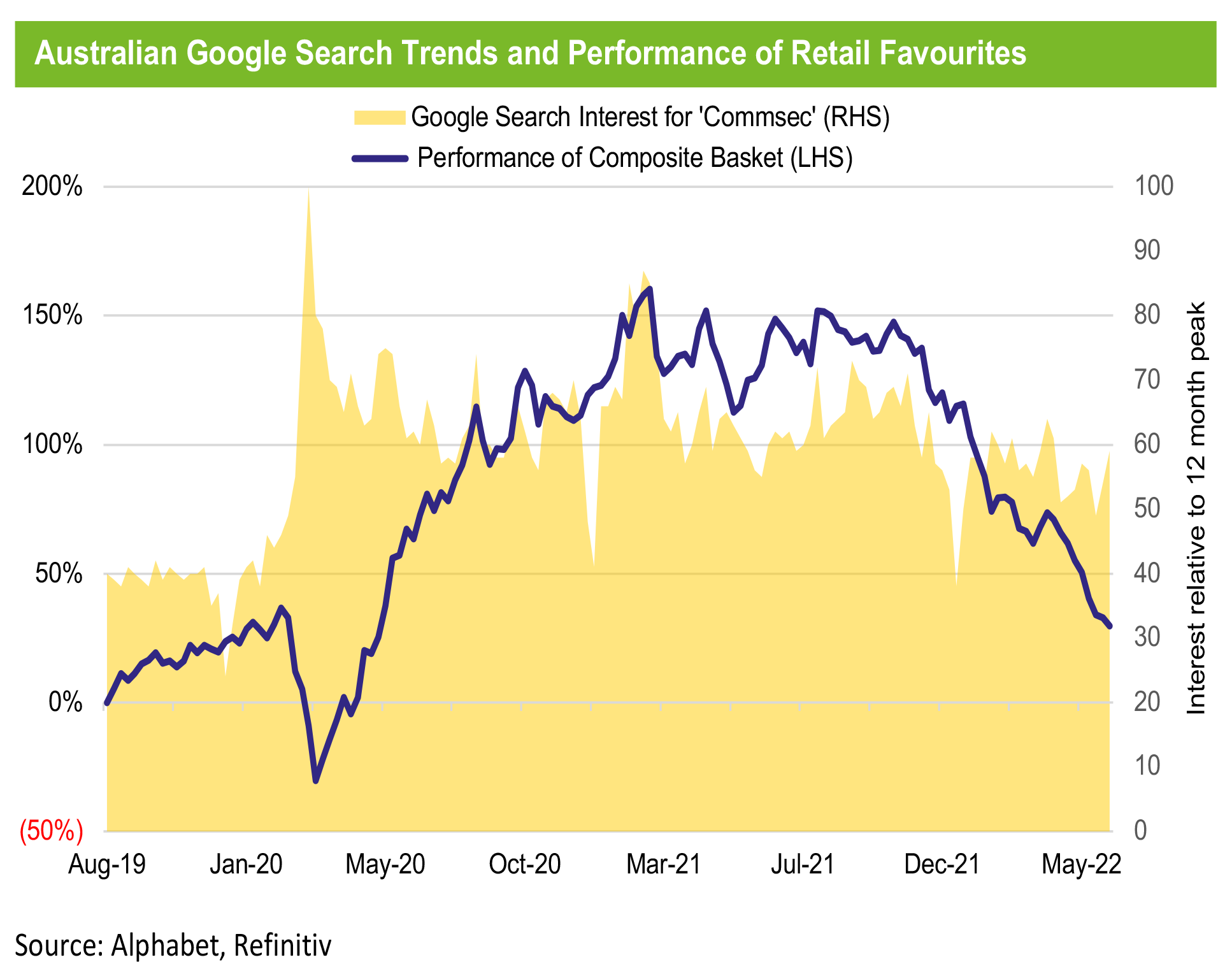

Following the COVID-19 market crash, retail interest in share trading accounts was at an all-time high, which we believe fuelled the meteoric rise of the popular stocks. Whilst this trend has persisted above pre-pandemic levels, interest has begun to wane, illustrated by the following chart.

As shown above, using the Google search term ‘Commsec’ as a proxy, retail interest in trading accounts hit an all-time high in March 2020 during the peak of the crisis. Furthermore, as the performance of the composite basket reached its highest point in February 2021, retail interest in trading accounts followed suit, rising to its second highest level over the assessed period. However, in line with our expectations, the recent challenged performance of the popular stocks saw retail investor interest decline.

Have investors been shorting these popular stocks?

The chart below shows the average shares held short as a percentage of total shares outstanding (‘short interest’) for the basket of popular stocks relative to its performance.

Evidently, short sellers have benefitted from the price decline of popular stocks. Short interest declined as the popular basket rallied from its COVID-19 trough. Following a period of price stagnation and relative stability in financial markets, the short interest of the popular basket of stocks increased again, with investors seeking to capitalise on what they believed were overhyped stocks.

How have professional investors performed in recent market volatility?

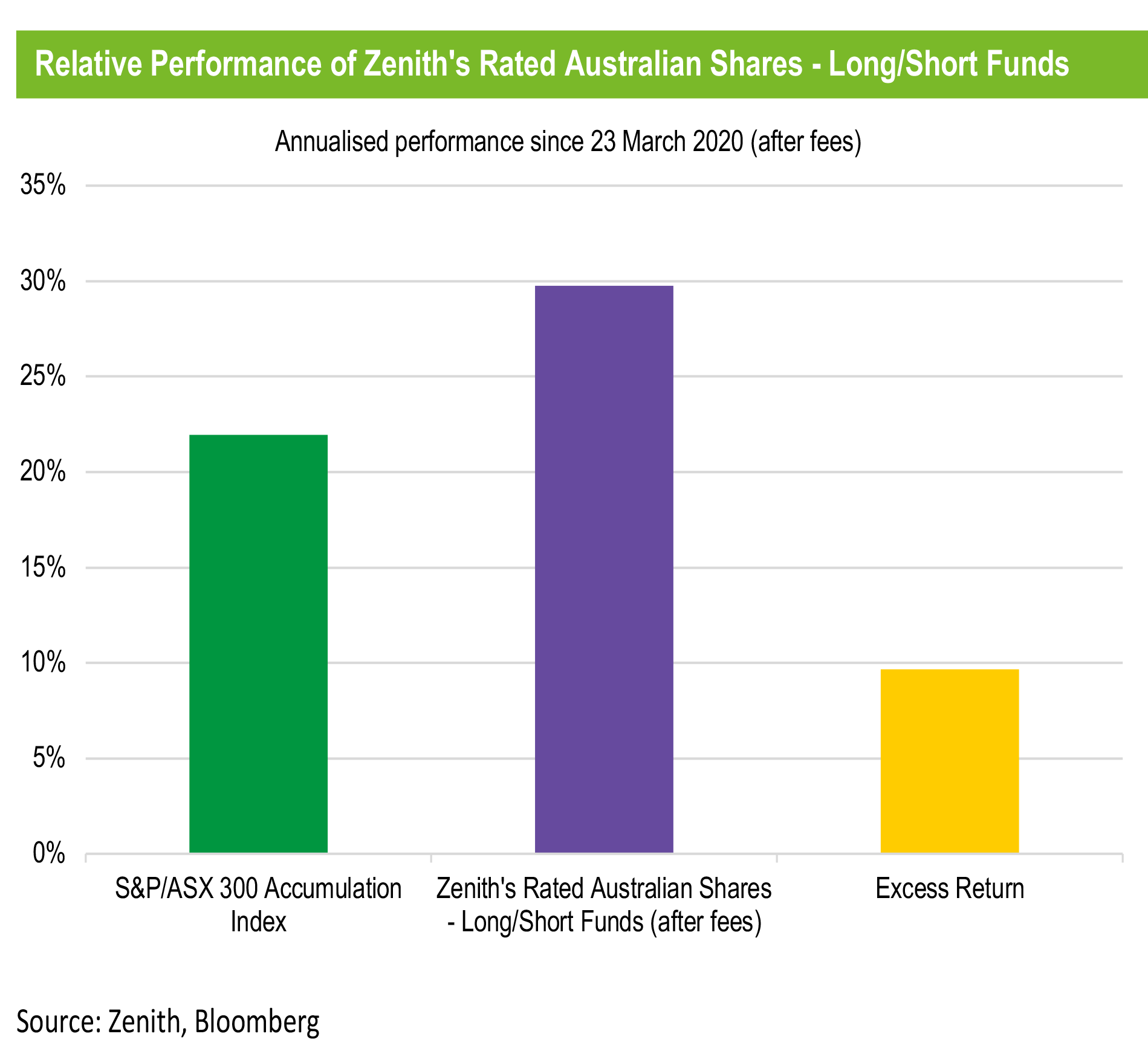

The natural question to ask is whether or not active managers were able to add value during this turbulent period. The chart below highlights the relative performance of Zenith’s rated Australian Shares – Long/Short funds (after fees) and the S&P/ASX 300 Accumulation Index.

Pleasingly, our rated Australian Shares – Long/Short funds outperformed the S&P/ASX 300 Accumulation Index from 23 March 2020 (the bottom of the drawdown) until 31 May 2022, achieving excess returns of approximately 10% p.a. (after fees).

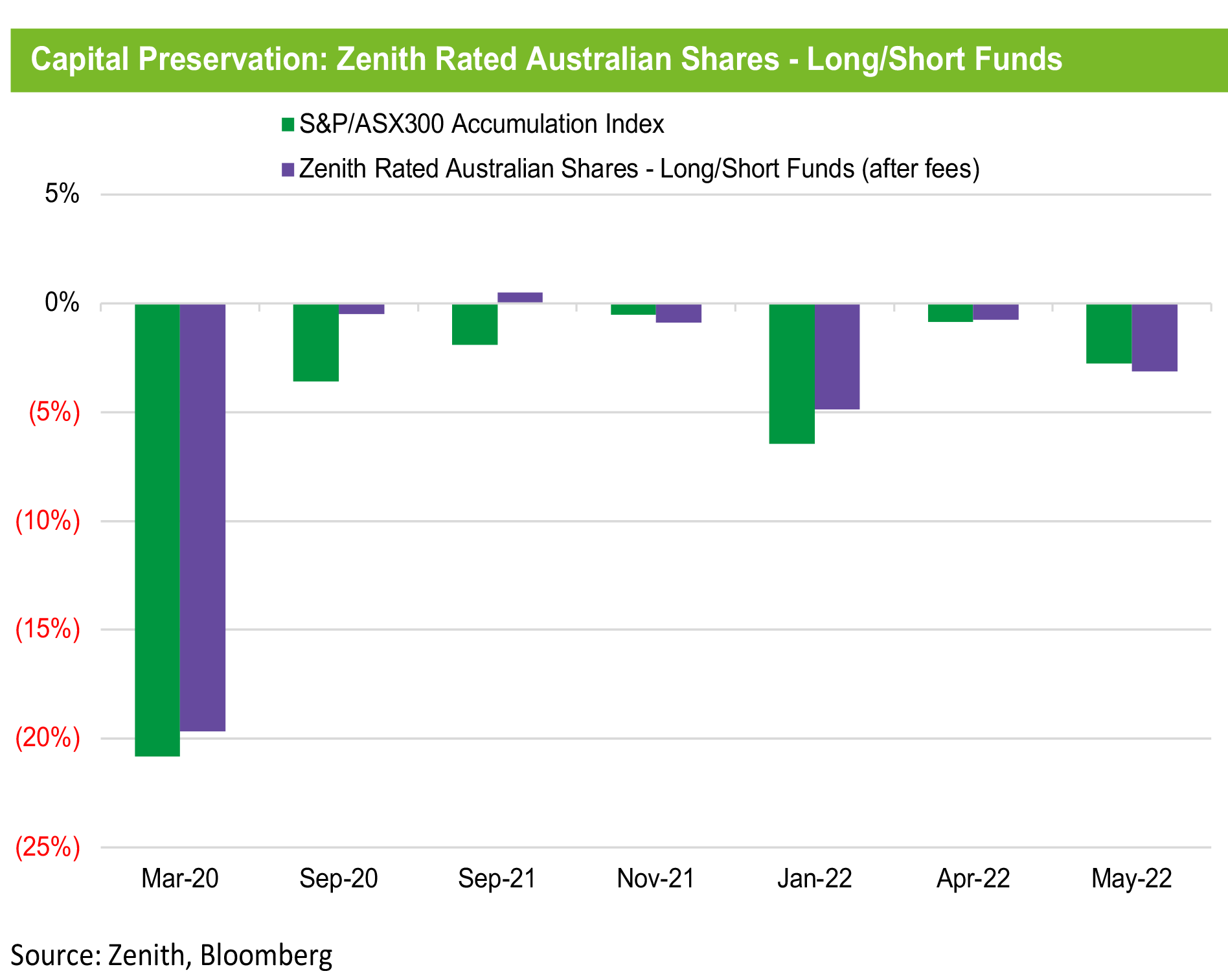

In addition to the peer group achieving higher absolute returns than the benchmark, it also protected investor capital. The chart below shows the outperformance of the peer group in months where the benchmark recorded a negative month.

As we can see, the peer group underperformed the benchmark when it fell in only two instances. Moreover, we note that the peer group’s downside protection during these periods contributed to approximately a third of its 10% p.a. outperformance over the assessed period.

Leave it to the professionals

Whilst we acknowledge that cognitive biases and specifically, the fear of missing out, are difficult to control, we believe it’s imperative that investors look through the noise when selecting their investments. Moreover, we believe professional active managers, who have substantial experience in a variety of market environments, are best placed to do this and achieve strong, risk-adjusted returns over the long term.

By Tom Goodrich, Senior Investment Analyst