Ethics and SMSF advice

Advisers need to understand how the Code of Ethics that relates to the provision of financial advice with respect to the establishment and ongoing management of SMSFs.

SMSFs comprise more than one quarter of Australia’s $3.4 trillion[1] superannuation sector, with 28,685 new SFSFs established in the year ended 31 March 2022[2]. SMSFs are subject to a number of rules and regulations and aren’t appropriate for everyone. This article, proudly sponsored by GSFM, examines the ethical considerations for advisers recommending SMSFs to clients.

Australians’ interest in managing their own super has not waned in recent times (figure one), despite the challenges thrown up by Covid-19 and its impact on financial markets – market volatility, supply chain issues that have led to rising inflation, inflation that’s led to rising rates. Only industry funds have a greater number of members1 (11.4 million accounts) and larger pools of assets under management ($1.1 trillion).

An SMSF is a privately run superannuation fund established for the sole purpose of providing retirement benefits to its members. SMSFs can now have between one and six members, and, as any adviser who has worked with SMSFs knows, come with innumerable rules and regulations.

Establishing an SMSF involves creating a trust with either individual or corporate trustees, who are responsible for managing the trust’s assets. It is essential that prospective trustees understand their responsibilities. These include: ensuring ongoing compliance with super and tax legislation, which includes an annual audit, as well as meeting their financial reporting and taxation obligations to the ATO.

The requirements of SMSF trustees

It is essential that your clients understand their responsibilities if they decide to establish an SMSF. They need to understand that they’ll be personally liable for all decisions made by the fund, including following any advice you or other service providers give them. Therefore, you must ensure your clients understand both their responsibilities and all advice they receive.

There are eligibility criteria for becoming an SMSF member – and therefore a trustee. In the first instance, a person must consent to becoming a trustee and accept their responsibilities by signing a trustee declaration.

SMSF members/trustees cannot:

- be a registered bankrupt

- have previously been disqualified as an SMSF trustee by a court, the ATO or ASIC

- have an employer/employee relationship with another fund member (unless they are related).

SMSF trustees are responsible for all decisions made about the fund and compliance with relevant laws. Obligations with which SMSF trustees must comply under superannuation and taxation laws include:

- maintaining the fund for the sole purpose of providing retirement benefits to SMSF members, or to their dependants if a member dies before retirement

- accepting contributions and paying benefits (pension or lump sums) to members and their beneficiaries in accordance with superannuation and taxation laws and the SMSF trust deed

- valuing the fund’s assets at market value for the preparation of financial accounts and statements

- having the financial accounts and statements for the SMSF audited each year by an approved SMSF auditor

- meeting the reporting and administration obligations imposed by the Australian Taxation Office (ATO).

Ensuring your clients understand their obligations is important; an SMSF trustee can be penalised for non-compliance in several ways:

- Their fund losing its concessional tax treatment.

- Being disqualified from their role as trustee – this means they can no longer be members of the SMSF, and they are unable to start a new one.

- Fines or imprisonment, depending on the seriousness of the breach.

Earlier this year, the ATO reported that it had disqualified 170 SMSF trustees during the 2021–22 financial year, with 83 disqualified in the March quarter alone[3]. In its role as regulator of SMSFs, the ATO has a number of enforcement actions it can take if trustees don’t comply with the super law, or the ATO is concerned about their suitability to be a trustee of a self-managed super fund (SMSF).

The ATO maintains a website where it keeps a register of individuals it has disqualified from being a trustee since 2012. The disqualified trustees register is updated on a quarterly basis and is publicly available; it’s regularly checked by SMSF professionals, including SMSF auditors. It may also be accessed by the trustee’s employer and financial institutions.

It’s important to note that disqualification action is taken only after the ATO considers all other enforcement actions; it prefers to help trustees rectify contraventions and comply with the law.

Under the super law, the ATO can disqualify an SMSF trustee, or director of a corporate trustee, if:

- the trustee has contravened the rules

- the ATO considers the trustee not to be a ‘fit and proper’ person for the role, having regard to the trustee’s personal character and circumstances.

Is an SMSF right for your client?

When determining whether an SMSF is appropriate for a client, advisers need to consider the client’s existing super fund/s and whether that or other retail or industry super funds may be better placed to meet their long term retirement funding goals.

When providing personal advice to clients – including advice about establishing and managing an SMSF – advice providers must meet the best interests duty and related obligations:

- act in the best interests of the client (section 961B)

- provide appropriate personal advice (section 961G)

- warn the client if advice is based on incomplete or inaccurate information (section 961H)

- prioritise the interests of the client (section 961J).

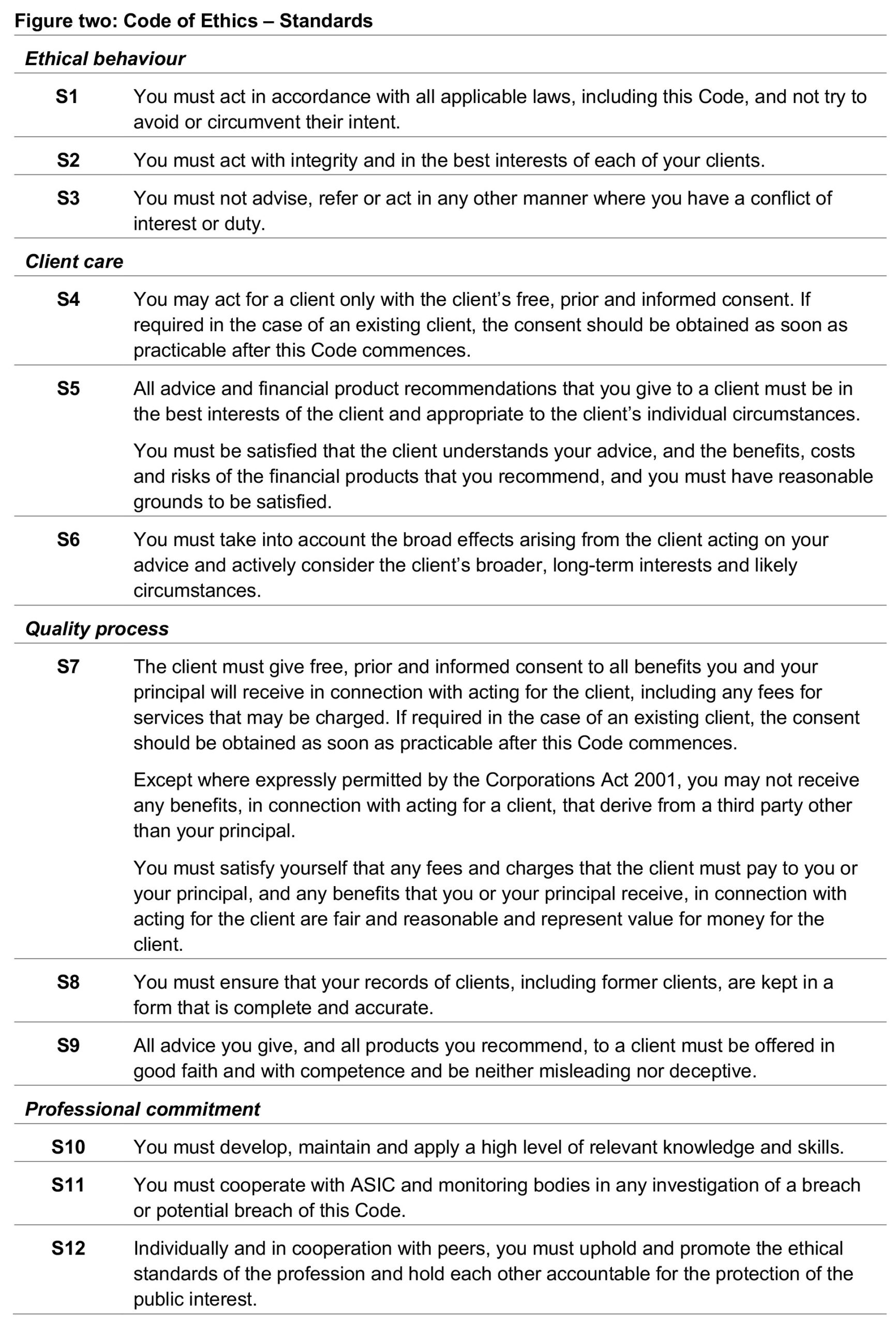

More specifically, ASIC provides guidance for AFS licensees and authorised representatives who provide personal advice to retail clients about self-managed superannuation funds (SMSFs). There are a number of relevant conduct and disclosure obligations outlined by ASIC, which also intersect with the financial advisers’ Code of Ethics. For each of the obligations detailed, the relevant ethical standards are identified.

1. Does your client want to be up to date with trustees responsibilities and ensure they maintain full compliance at all times? Do they have the time and capacity? Whether or not your client appoints a corporate trustee, he or she is legally responsible for managing the fund and making sure it complies with superannuation and tax laws. Industry, retail and corporate funds typically have professional, licensed trustees who take on the responsibility for legal compliance.

Failure to comply with obligations under superannuation and taxation laws can have significant consequences, such as the loss of tax concessions. All trustees are equally required to comply with trustee responsibilities and obligations and are liable for the actions of other trustees.

Areas of concern for ASIC are where an SMSF has been recommended to a client and there’s been no consideration of whether the client has the time, skills and knowledge to operate an SMSF, or whether they are able to appropriately develop their skills and knowledge to operate an SMSF.From an ethics standpoint, you need to ensure that establishing an SMSF is not only in your client’s best interests (standards 2 and 5), they must understand their responsibilities and accountabilities to be able to provide informed consent (standard 4). When recommending an SMSF, it’s essential to take into account the broad effects of your client acting on this advice, both now and in the future (standard 6).

- When giving advice to clients about establishing and/or switching to an SMSF, clients should be advised on the costs associated with setting up and/or switching to an SMSF. While the costs of running an SMSF vary according to a number of factors, ASIC requires that advisers provide appropriate information as detailed in its Information Sheet 206.[4]

The disclosures referred to in ASIC’s Information Sheet should be provided to your client at the time of the advice, both in person and by way of an SOA.

Standard 5 of the Code of Ethics requires that you must be satisfied that your client understands your advice, and importantly, the associated costs – and you must have reasonable grounds to be satisfied of their understanding.

- Clients should also be advised as to the appropriate structure when establishing an SMSF. Selecting the most appropriate structure – a corporate or individual trustee structure – can have tax and succession planning implications for clients. It can be costly to change structures, ownership of assets and trustees once the SMSF has been established.

ASIC takes a keen interest in whether clients have been adequately advised on SMSF structures and are likely to be concerned where there’s no evidence of consideration of the appropriateness of the SMSF structure, or if the client has been directed to a particular type of SMSF structure without consideration of its appropriateness.

A failure to advise an appropriate structure could breach several ethical standards, including best interests (standards 2 and 5), a failure to consider long term ramifications of your advice (standard 6) and providing competent advice (standard 9).

- Under superannuation laws, SMSF trustees must develop an investment strategy to ensure the SMSF is likely to meet members’ retirement needs. The trustees are responsible for their fund’s investment strategy and make all investment decisions, even if those decisions are advised by professionals. Members of public super funds have some degree of choice when it comes to broad asset allocation, however each funds’ trustees make, and are responsible for, asset allocation and investment decisions.

SMSFs can only have six members, which can limit the number or type of assets the members can invest in. For example, a public super fund with hundreds of members has the scale to invest in private equity or direct infrastructure, investments that generally require significant investment capital to access.

In an audit situation, ASIC is likely to examine the advice clients receive about their SMSF investment strategy and whether this advice was appropriate to the clients’ risk appetite and investment goals.

A failure to provide appropriate advice about the SMSF’s investment strategy will likely breach a number of ethical standards including: a failure to meet best interests (standards 2 and 5), the broad, long-term effects of the client acting on your advice (standard 6) and financial product advice must be offered in good faith and with competence (standard 9).

- Insurance costs tend to be higher for SMSF members; industry and retail funds can get scale related discounted premiums not available to smaller funds and individuals.

ASIC notes that in the event of an audit, it is likely to be concerned where the client had an existing life and TPD insurance policy, but the adviser did not consider the risk of losing this cover when recommending the establishment of an SMSF. A lack of consideration of the client’s life and TPD insurance needs when they are not yet a retiree and have not accumulated a superannuation balance to be sufficiently self-insured would be another area of concern.

As well as not meeting best interests duties (standards 2 and 5), a failure to consider insurance needs would also likely breach standard 6, as long term impact on the client has not been considered.

- Trustees also need to consider an exit strategy, even when establishing an SMSF. There can be many reasons a trustee needs or wants to wind up an SMSF – the compliance requirements may become too onerous or costly or the more active trustee dies or becomes incapacitated. ASIC will consider whether clients have been made aware of what may be required to wind up their SMSF and the likely costs involved.

A failure to consider an exit strategy and advise clients as to the likely process and costs, could potentially breach several ethical standards, including: best interests (standards 2 and 5), the broad and the long-term effects of the client acting on your advice (standard 6).

- SMSFs are not subject to the same government protections that are available in APRA- regulated superannuation funds, such as statutory compensation in the event of theft or fraud.

Further, when advising a retail client to transfer the whole or part of the balance of an existing account with an APRA-regulated superannuation fund to an SMSF, ASIC emphasises the importance that the client should be made aware that SMSFs are not subject to the same government protections available in APRA-regulated superannuation funds, such as statutory compensation in the event of theft or fraud.

In the event of an audit, ASIC is likely to look at whether the client received advice on the lack of statutory compensation when they received a recommendation to switch their superannuation from an APRA-regulated superannuation fund to an SMSF.

Advisers must include additional information in an SOA when the advice recommends replacing one product with another (switching advice) (section 947D Corporations Act 2001). Failure to do would breach standard 1, failure to comply with legal requirements, as well as standards pertaining to best interests.

Case studies

The following case studies are based on real events; however, the names of people and organisations have been changed, and some details altered. The case studies have been drawn from ASIC or the Australian Financial Complaints Authority (AFCA) or its predecessor organisation. For each, potential breaches of the Code of Ethics are identified.

Case study one: SMSFs the victim of fraud

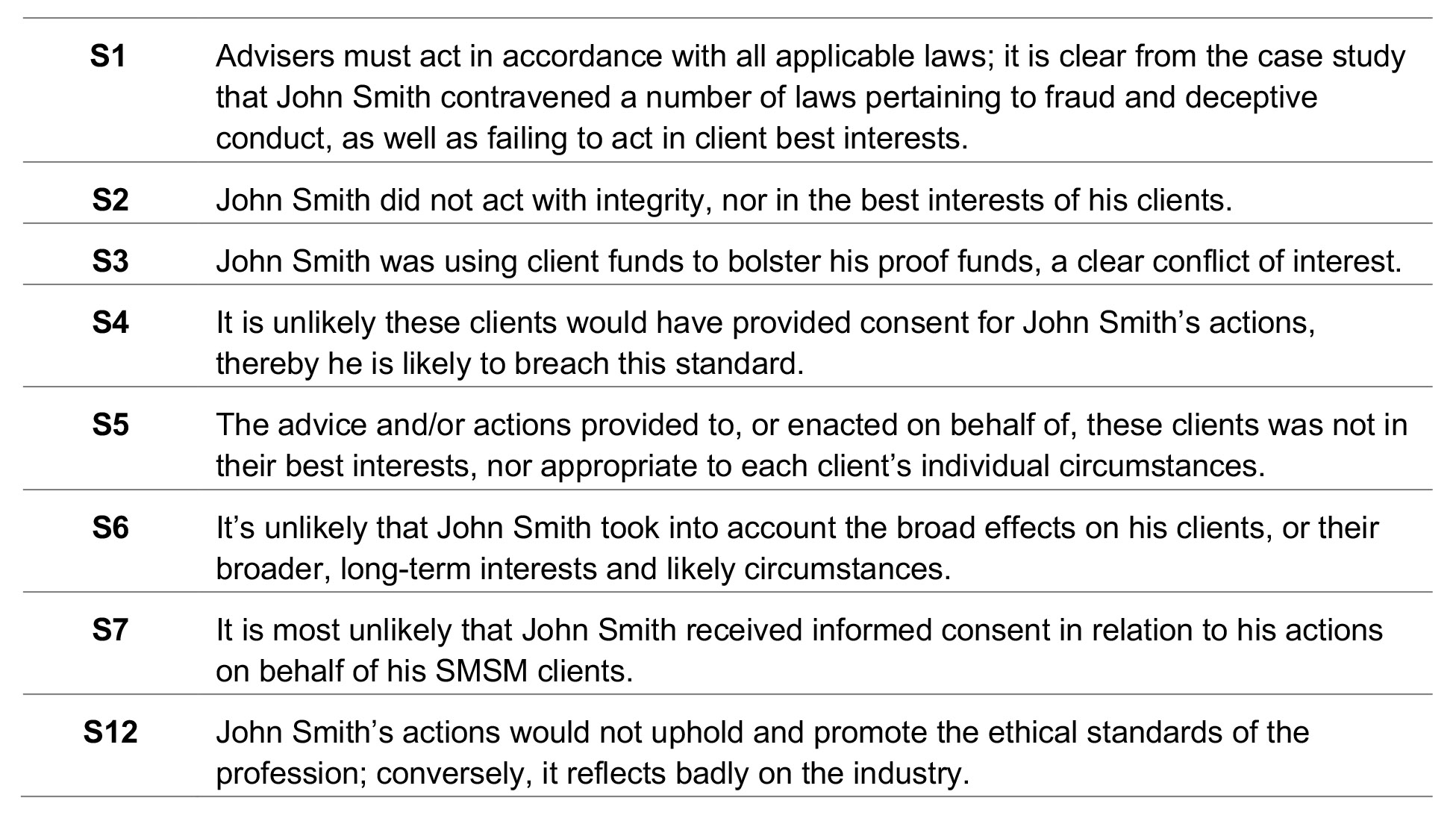

The trustees of SMSF ABC Auto Superannuation Fund initiated proceedings against their financial adviser John Smith and his business Smith Holdings for unpaid returns and money held in trust.

Although a licensed financial adviser, John Smith primarily operated as a private investor and traded in bank instruments. He invested in private placement programs (PPP) which required capital as proof of funds in order to trigger a line of credit enabling him to facilitate arbitrage transactions involving bank instruments in the US and Europe.

He began obtaining money from outside investors, primarily SMSFs to increase his proof of funds to the required levels for trading.

Following an ASIC investigation, it was alleged that John Smith defrauded $38 million from eleven SMSFs. The maximum penalty for each offence of fraud in the state John Smith operates is seven years imprisonment, or 10 years if the person deceived is 60 years or older.

As well as potentially contravening a number of laws, John Smith also hypothetically breached the following standards in the Code of Ethics.

Case study two: Incorrect advice re use of bare trusts

For an SMSF to borrow through a limited recourse borrowing trust, otherwise known as a bare trust, it’s essential that the bare trust is established correctly from the outset. This includes:

- providing the SMSF the beneficial interest in the asset that’s being acquired by the bare trust using borrowed money

- allowing the SMSF the right to acquire the asset from the bare trust after one or more payments have been made.

Adviser Margot Egan has established herself as a specialist with respect to SMSFs and works closely with both accounting and legal practices to ensure appropriate tax and legal structuring for her SMSF clients.

Margot had a new client meet with her to review their existing SMSF and provide advice with respect to the investment strategy. The SMSF had signed a contract to invest in two residential properties through a bare trust, however they were concerned about the correct establishment of that trust.

Margot discovered three problems with the inappropriate provisions being included in the terms for the bare trust. Firstly, although the SMSF was investing in several assets, only one bare trust had been established. Limited recourse borrowing, or a bare trust, can only be used to acquire a single asset.

Secondly, contracts had been signed to acquire the assets, whereas the bare trust/s need to be established prior to contracts being signed.

Finally, there are restrictions on the changes or improvements that can be made to an asset while it is owned by a bare trust. Margot’s clients intended to significantly renovate the properties they had purchased, which raised doubts about their ability to use a bare trust to hold the assets.

Working with the tax and legal advisers, Margot was able to advise an appropriate structure for her SMSF client and recommend an investment strategy for the fund.

In this case study, Margot has met her ethical obligations to her client, particularly by meeting the following ethical standards.

Case study three: Misuse of SMSF structure

Ken Martin is a financial adviser of Martin Financial Planning, which holds its own AFSL, and director of Martin Management Systems Pty Ltd (MMS). An ASIC investigation found that Ken Martin allegedly recommended that clients who were under financial pressure roll over their APRA regulated super fund to an SMSF and invest in MMS. He also encouraged his clients to borrow some of what was invested in MMS, on the understanding there was no obligation to repay what was lent.

ASIC claims that Ken Martin’s clients relied on his advice and assumed that the investing of superannuation in MMS, and the receipt of loans from MMS, was legally permissible and appropriate.

Instead, the recommended strategy resulted in his clients breaching restrictions on the early release of superannuation benefits, and their SMSF not satisfying the requirement that it meet the sole purpose test.

ASIC also found that the adviser’s conduct demonstrated he was not adequately trained or competent, was not a fit and proper person, and was likely to contravene a financial services law in the future.

Ken Martin was banned from providing financial services for five years and in addition, ASIC cancelled the firm’s AFSL. The ban prevents Ken Martin from providing any financial services and from being involved in managing, supervising, or auditing the provision of a financial service and the provision of training about a financial service or a financial product.

The advice he provided to the clients that were the subject of this ASIC investigation would have potentially breached the following standards of the Code of Ethics:

Case study four: Inappropriate recommendation of an SMSF

Case study four: Inappropriate recommendation of an SMSF

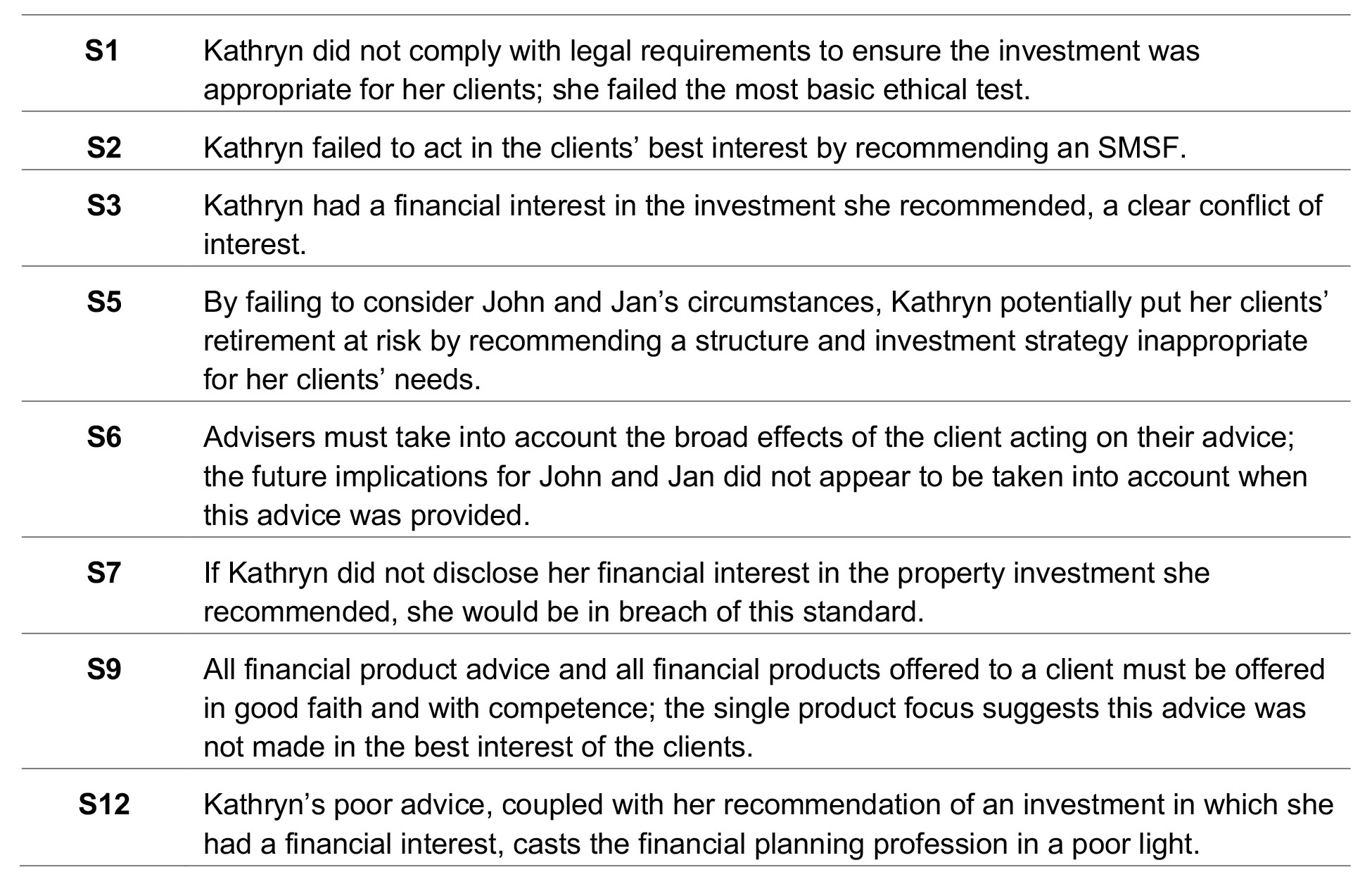

Jan and John, both in their late 50s, are inexperienced investors. Although John works full time, Jan has only worked part time for the past 20 years. As retirement approached, they sought financial advice from financial adviser Kathryn King to prepare them for retirement. They were uncertain as to their preparedness for retirement and concerned about their financial position.

Jan and John and had two financial objectives:

- To eliminate their debts prior to retirement, including paying off their mortgage more quickly.

- To save for a holiday to the United Kingdom to visit Jan’s family.

The couple’s combined income was $135,000 per annum, and their combined superannuation balance was $112,000. Their outstanding mortgage was $195,000 on a home worth $745,000. They also had other loans and credit cards totalling $45,000.

Kathryn recommended that Jan and John set up an SMSF, roll over their existing superannuation funds, and purchase units in a property trust in which Kathryn had a financial interest.

Jan and John did not have the requisite financial skills to manage an SMSF for which they would be personally liable, something that should have been obvious to the adviser. The couple was struggling to manage their finances, had a low combined superannuation balance and limited capacity to significantly increase its balance.

An ASIC investigation found the advice provided was not appropriate for Jan and John, and failed to meet their needs or objectives. From the details provided in the case study, Kathryn potentially breached the following standards in the Code of Ethics.

Retirement and retirement funding has been in the spotlight of late. With more than five million Australian baby boomers reaching retirement over the coming decade, the importance of retirement planning intensifies. While SMSFs continue to be a significant segment of the superannuation landscape, it’s important to note that they are not appropriate for all clients.

While an SMSF can be a valuable investment vehicle for many, the time, cost and skill required to manage one’s own superannuation may outweigh the benefits. The rules and regulations that govern SMSFs places a significant amount of responsibility and accountability on anyone operating a SMSF and therefore may not be suitable all clients.

When recommending the establishment of an SMSF, as with all financial advice, it’s critical that you consider what is in the client’s best interests – today and into the future.

———-