Mind the gap – the impacts of inadequate retirement savings (part two)

Advisers can tap into various levers when working with clients to help them meet their retirement objectives.

When it comes to saving for retirement, each of your clients has unique financial circumstances and individual aspirations for life after work. How can you best support them to make the most of Australia’s superannuation system and attain their retirement goals? This article is proudly sponsored by Russell Investments.

As outlined in part one of this article, Russell Investment’s research into the impacts of inadequate retirement savings identified four key hurdles individuals must overcome to achieve an ‘informed position’. This prepares them to make and maintain optimal contributions. This is the first lever for closing the retirement savings gap.

Clearing the hurdles

It is believed many Australians are disengaged with their super – retirement is seen as a distant problem, outweighed by more immediate needs. Rising interest rates, cost of living pressures and volatile markets will only exacerbate this.

To understand the drivers of engagement, Russell Investments commissioned independent analysis of more than 3,000 Australians who currently don’t currently receive financial advice. The analysis highlights the significant challenges faced by Australians as they engage and try to take positive action to reach their retirement goals. Although the analysis is of non-advised clients, the insights are pertinent more broadly.

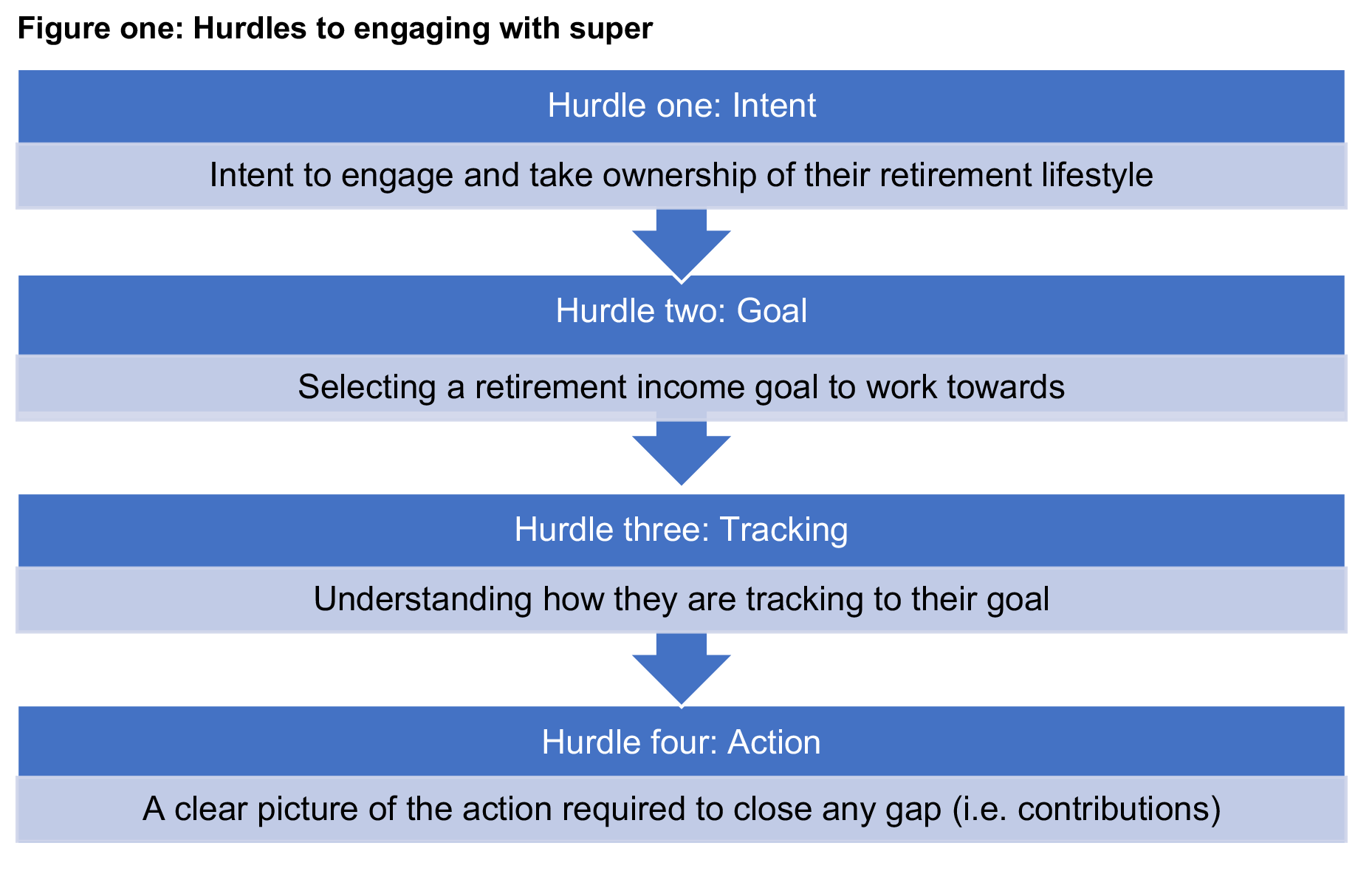

The analysis points to four key hurdles (figure one) each individual must overcome prior to being in an informed position, ready to make and maintain optimal contributions. Being able to identify where existing and prospective clients are in their retirement mindset and helping them to overcome these hurdles can be beneficial to both of you – a better retirement outcome for the client and a potential means to grow your business and/or provide a prospecting tool for attracting new clients.

Hurdle one: intent

The analysis found approximately one in five participants demonstrated little intent to engage with their retirement savings. These respondents had put little thought into their life after work and demonstrated little to no understanding of super and how their retirement savings were tracking.

Interestingly, the findings challenge the theory that engagement is primarily driven by proximity to retirement. The proportion of respondents who hadn’t thought about their retirement income goal showed no significant change between Millennials (21 percent), Gen X (20 percent) and Baby Boomers (18 percent).

When you consider a little under 15 percent of the Australian population live below the poverty line[1], it is evident that a material proportion of Australia’s population will have more pressing and immediate financial needs. Retirement adequacy will be further down the list of priorities; analysis indicates financial flexibility, or excess income, plays the most significant role in determining engagement and intent. More than a third of those who had little thought into their goal had an income below $50,000.

While most of your clients are likely to have established retirement objectives and be engaged with their retirement savings, there are some questions you can consider:

- Have all clients, particularly younger clients, set retirement objectives?

- Can you measure each client’s level of engagement with their superannuation?

- Do those less engaged clients understand the importance of retirement savings?

If you have answered yes to these questions, your clients are likely to have cleared hurdle one. Where there are some clients who have not yet thought about retirement in any detail, it’s an opportunity to connect with them and ensure they’re engaged in a position to clear the remaining hurdles.

Hurdle two: goal

Roughly one third of participants in the survey had put some thought into their retirement savings, but had not set a retirement goal, such as the level of retirement income they would like to work towards.

Goal setting is a critical element and a key hurdle as individuals progress towards optimal voluntary contributions. There is a significant body of scientific evidence highlighting the positive impact goal setting has on an individual’s ability to achieve it. Despite this, many super funds place very little emphasis on the individual retirement goals of their members, a distinctive difference from the approach taken by a financial adviser.

When it comes to retirement planning, choosing an appropriate income goal can be challenging. For example, self-directed investors may assume a proportion of their current income would suffice, but fail to consider the impact of inflation, thereby targeting an income with significantly less future purchasing power than expected.

For those clients who are yet to establish explicit retirement objectives, there are some questions you can consider:

- Can the client articulate specific and measurable retirement objectives?

- Do clients understand the risks that can impact their objectives? This might include things like market volatility and sequencing risk, longevity risk, the impact of interest rates and inflation

- Do client objectives consider all stages of retirement? While many may think about the travel and fun goals of early retirement, have they also considered the potential need to pay for aged care in later years?

Hurdle three: tracking

Research[2] shows goal tracking can also play a significant role in engagement and improve the chance of attaining goals. An obvious example is the emergence of technology, delivering personalised goal tracking in the health and fitness industries, highlighting four significant benefits of tracking:

- Choice – goals focus attention and direct efforts toward goal relevant activities and away from perceived undesirable and goal irrelevant activities.

- Effort – goals can have an energising function, leading to more effort. The higher the goal, the greater the effort invested.

- Persistence – individuals become more determined to work through setbacks when pursuing a goal.

- Cognition – goals can activate cognitive knowledge and strategies, leading individuals to develop and optimise their behaviour.

Establishing a goal tracking program for clients to measure their retirement savings progress toward their end goal can help with engagement and encourage behaviours likely to see the client meet their objectives.

Hurdle four: action

Once a client understands and is tracking their objectives, they can build a clear picture of the actions required to achieve their goal. In many cases, this will be the additional voluntary super contributions needed to achieve the goals set. By providing your clients with guidance through each of these key hurdles, you can empower them to be in a better position to achieve their retirement objectives.

For example, by helping people optimise contributions (contributing up to 5% of their salary in additional contributions when tracking behind or reducing contributions when tracking ahead), Russell’s analysis demonstrated the proportion of individuals on track to their goal would increase by more than half.

Optimising asset allocation

The second lever you can use to close the retirement savings gap is the optimisation of asset allocation. Independent research highlights the strong influence asset allocation has on investment returns, driving 85% or more of the outcome[3].

Asset allocation is fundamentally the balancing of risk and return. Too little risk and retirement savings won’t grow as much as needed. But too much risk at the wrong time can jeopardise those savings.

Given the importance of investment returns, it may come as a surprise to many that most Australians don’t have an asset allocation well suited to their needs. When it comes to superannuation, many Australians are defaulted into options that significantly compromise.

The vast majority are defaulted into one- size-fits-many options that apply a single asset allocation to all members or an age-based cohort. This approach ignores the other additional personal information that could improve asset allocation, such as the superannuation account balance, contributions and the individual’s retirement income goal.

While some individuals will have the expertise to do that themselves, many others are constrained by poor financial knowledge, unreliable information sources, overconfidence and emotional biases in their decision making. This is where professional financial advice can help.

By optimising asset allocation – the single most influential factor on investment earnings – at the individual level, you can materially improve your clients’ retirement adequacy.

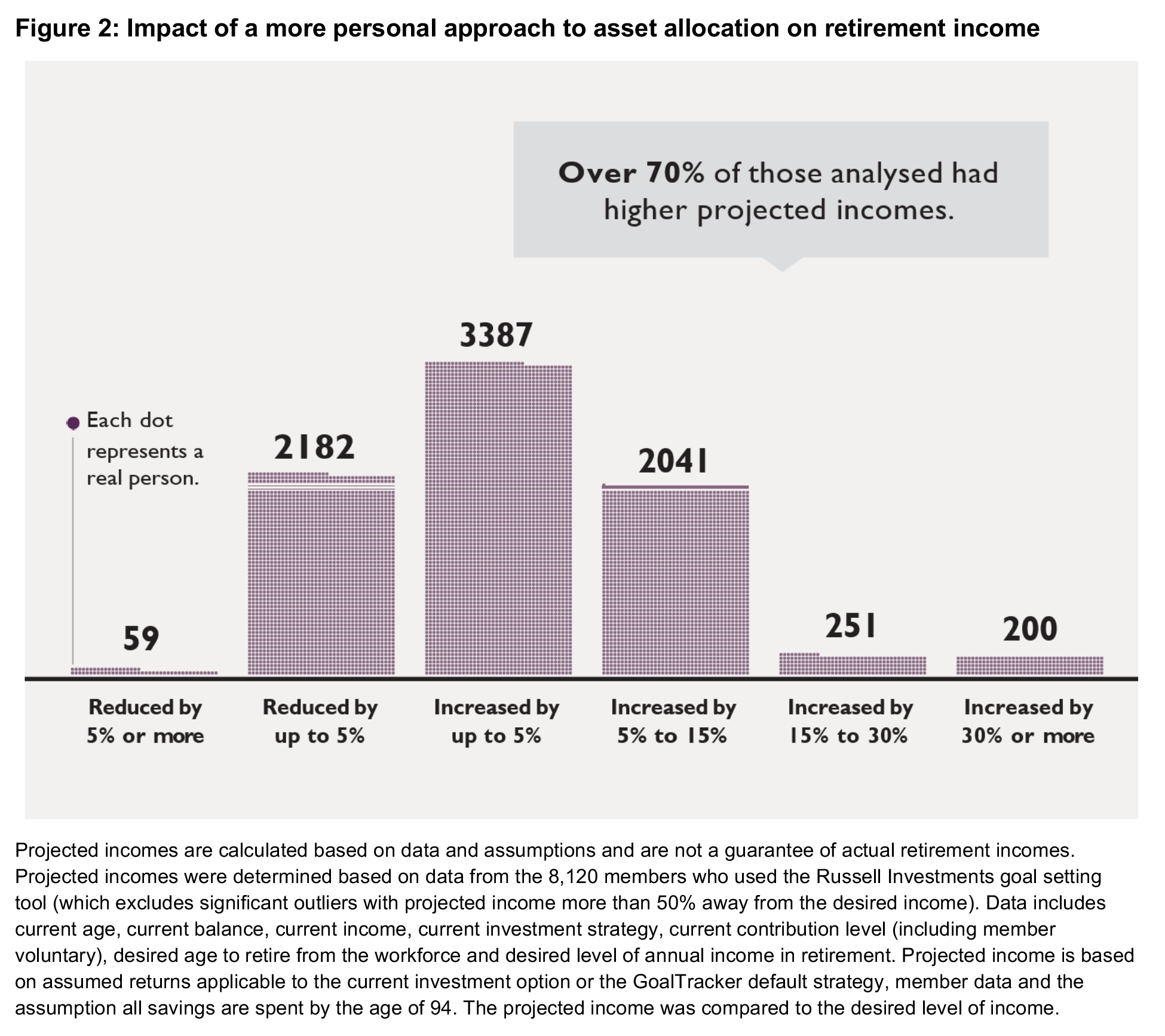

Russell’s analysis of around 8,000 individuals shows a more personalised approach— individually increasing growth allocations earlier in life and more precisely reducing growth allocations when approaching retirement—can increase the projected retirement income for more than two out of every three people, while simultaneously reducing the impact of a significant market event later in life.

In addition, by incorporating the individual’s desired income, asset allocation can be further optimised to reduce the chance of falling short. For example, if an investor is on track to their retirement income goal, but not above, a more defensive growth allocation can help ensure they don’t fall below their target income.

Why optimise asset allocation at the individual level?

Asset allocation is fundamentally the balancing of return expectations and risk, or uncertainty, using a range of asset classes. Each asset class typically has an expected return and an expected level of volatility.

For younger savers, high allocations to growth assets can improve the expected retirement income, as they have the time to outlast any negative volatility. Closer to retirement, high growth allocations can be risky. Investors may need to draw on their savings before they have time to recover their losses, either reducing retirement income or delaying retirement.

The investor’s goal can also play a significant role. For example, if an investor is on track to their desired retirement income, reducing growth allocations will help ensure they are less exposed during market volatility. However, an investor significantly ahead of their goal doesn’t need to sacrifice the upside potential, as they have the savings needed to fund their income, irrespective of short-term volatility.

Current default options compromise asset allocation

Saving for retirement is usually a 40+ year journey. Over this time, investors in a default option will experience significantly compromised growth allocations, materially reducing retirement adequacy.

This is supported by analysis conducted by Rice Warner. The analysis found, for an individual aged 30 with an opening balance of $26,000, a multifactor lifecycle product that considers more of the investor’s personal circumstances had a 91.8 percent chance of outperforming a balanced fund by retirement at age 63. In more compromised cases, the research found the income a member receives in retirement was up to 35 percent higher relative to a balanced fund with a 70 percent allocation to growth assets[1].

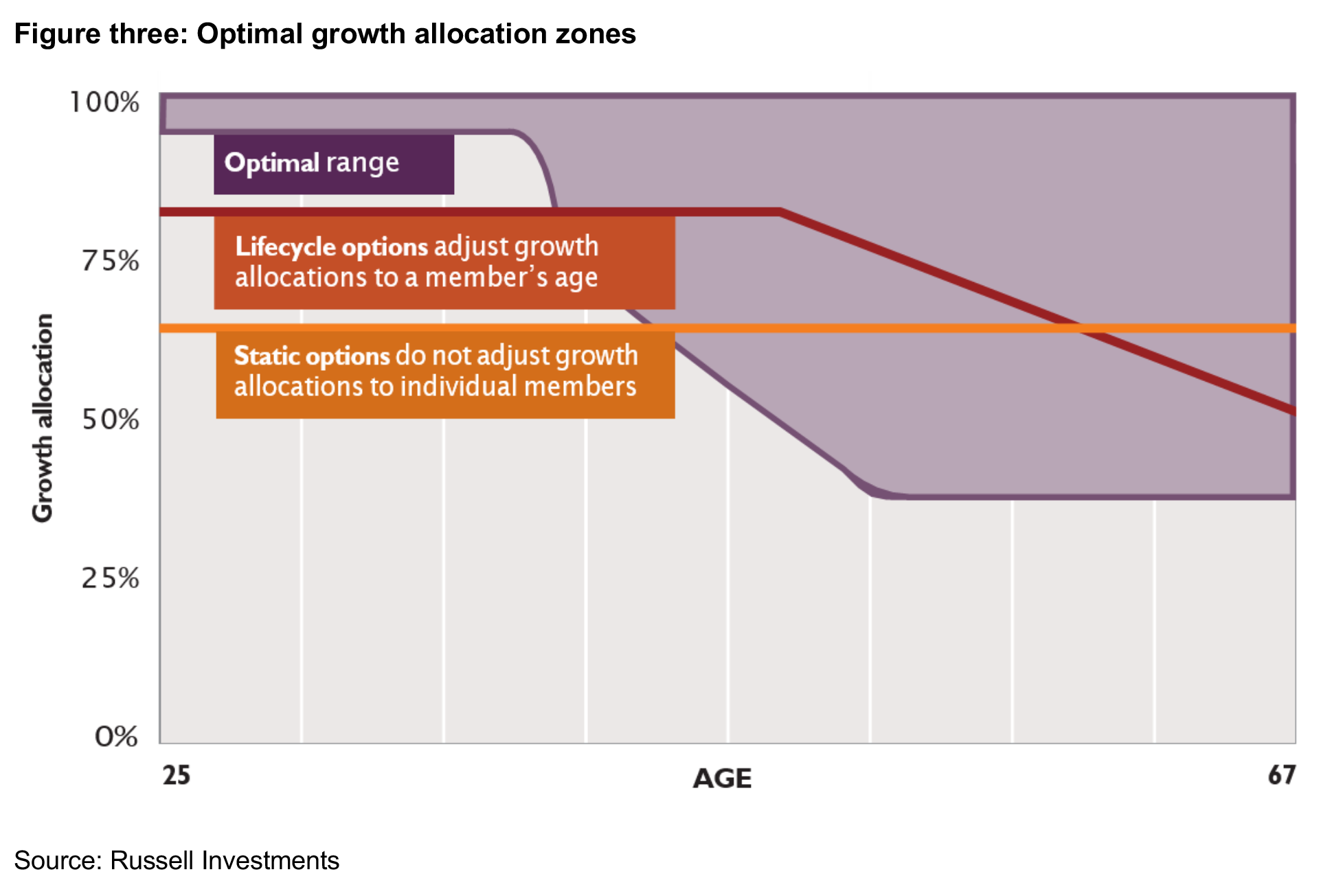

To understand these compromises, it’s helpful to know how growth allocations are determined for default options. The growth allocation is designed in one of two ways:

- static options share a single target growth allocation across all investors, and

- lifecycle options share growth allocations across age-based cohorts.

Both approaches share the same fundamental flaw: allocations designed for a cohort, at the expense of individual appropriateness.

Static options have a very broad membership with potential to create significant compromise. For example, a 25-year-old will sacrifice substantial growth potential and a 65-year-old will take on significant investment risk, with a single asset allocation designed to accommodate both.

Age-based lifecycle options do reduce this compromise. Yet, optimal asset allocation can still differ significantly within age bands. These options ignore the nine additional data points needed to determine an optimal growth allocation. For example, an investor with significantly more savings than needed can maintain a higher growth allocation when approaching retirement. The excess savings will allow them to maintain a comfortable income through a negative period and into the future recovery as they can draw income from the excess, ensuring their savings don’t fall below the point needed to meet their needs.

An optimal personal growth allocation can be anywhere within the purple range, while a static or lifecycle option only follows a single path.

In conclusion

The impact of the COVID-19 pandemic and the subsequent ‘cost of living crisis’ has brought retirement adequacy sharply into focus, again highlighting the challenges and misconceptions many Australians face when saving for retirement. Yet, with every crisis comes the opportunity for positive change.

Each individual has a different idea of the retirement lifestyle they aspire to, and their ideal retirement income will be unique to their needs. Financial advisers understand the importance of understanding financial goals to any optimal asset allocation. Typically, when working with an adviser, a substantial amount of time will be dedicated towards understanding what the client wants to achieve, so the advice can be tailored to achieve their goals.

Without such guidance from an advice professional, investors are at risk of selecting inappropriate super funds with an asset allocation that will enable them to meet their financial objectives for retirement. They may not set the right investment strategy for their circumstances, and many investors lack the knowledge and/or time to research the myriad of options available. With the renewed focus on super fund performance metrics, there’s the added risk of investors chasing performance or overreacting to market volatility, something that’s particularly important in the current environment.

Therefore, financial advisers are ideally placed to help Australians understand their retirement goals and use the levers to close the retirement gap. Helping clients overcome the four hurdles described in this article and optimise their asset allocation to achieve their goals can add significant value to an individual’s retirement savings over the long term.

Read CPD: Mind the gap – the impacts of inadequate retirement savings (part one)

———-