As the ASX goes down, the CX must rise – rethinking the concept of value in advice

A focus on client experience is critical to redefining the value of advice in the minds of consumers.

Is the single biggest challenge faced by the financial advice profession really the price of advice?

A glimpse at the financial media in recent times certainly reinforces that impression with headlines like these:

“100,000 quit advice as fees jump another 8 percent[1]” and “Escalating fees put advice out of reach for most Australians[2]”

leaving little doubt that increasing advice fees are driving people away from the sector.

And there’s no shortage of research to back such a contention up, with various studies – including ASIC’s Report 627[3] and Momentum Intelligence’s 2019 Client Experience Survey[4] – showing the cost of advice is possibly the biggest barrier to engaging a financial adviser, and the biggest reason to cease using one.

It’s little wonder then that we see an associated narrative focused on increasing efficiencies and reducing red tape to drive down the cost to serve. As if that is the key.

It’s little wonder also that much of the discussion around the value of advice, and how advisers can better articulate that value (to help ‘sell their fees’), is equally quantitative in nature, focusing on how advice can improve investment performance by a few percent each year, or shave thousands from a tax bill, or reduce debt.

Even discussion about the eagerly anticipated government review into the Quality of Advice (QAR) has – in most quarters – been distilled down to one about the cost and accessibility, rather than the quality, of financial advice.

The question then becomes, do we think that simply making advice cheaper – even a lot cheaper – will open the floodgates and see millions of previously inaccessible clients bang down the doors of adviser offices all over Australia?

Perhaps not.

And even if lower advice fees did encourage more people to at least consider seeking advice, would this in itself be enough to motivate them to pull the trigger and book an appointment with an adviser?

Even more importantly, is price the basis on which you want prospects to choose you over another adviser, and the basis on which you would want your existing clients to stay?

Or is it possible that we have missed the point all together, and the way people judge advice, and its value – and therefore their willingness to pay – is the way they judge other services?

Which is, of course, by the way they experience it and the way it makes them feel.

Put another way, should our efforts to make the value of advice so unquestionable and unassailable be focused not on the cost of advice, but on the experience of advice?

Expressing the value of advice in functional and quantitative terms is problematic

The concepts of price and value are intrinsically interconnected, with our decisions around purchasing a product or service at a given price involving – consciously or unconsciously – some level of calculation of price versus value. Some calculations can be simple and quick because they relate to low cost or low involvement categories (such as food or cleaning products), whilst others are more complex, because they relate to higher value or higher involvement categories such as fashion, cars or travel.

Various studies have, over the years, demonstrated the functional and/or quantitative value that financial advice can offer individuals, such as improved investment performance, lower tax bills, improved cash flow and lowering debt.

An equally functional approach has been seen in the approach of many firms to client care, with the focus being on service standards, such as the speed of answering phone calls and opening accounts, or the frequency of review meetings and newsletters.

Although grounded in admirable intentions, such an approach can be counterproductive:

- Firstly, tying your value, either explicitly or implicitly, to investment performance (or other financial metrics) can backfire in volatile markets. If you have tied your value as an adviser to investment performance, then recent client conversations will have been challenging.

- Secondly, a functional focus on customer service cannot differentiate you from your peers and does not help improve the perceived value of your advice. Customer service, even exceptional service, is a hygiene factor.

- Thirdly, thinking about the value of advice in functional terms overlooks the intrinsic emotional value clients can get from the advice process itself, which flows from feeling empowered and in control, and from seeing progress towards their goals.

A functional focus can lead to satisfaction, but as Australian research showed, satisfaction doesn’t always translate to loyalty.

A 2019 study of advice clients by Momentum Intelligence[5] found that whilst 94% of clients said they were satisfied with their adviser, less than half said they had a loyalty to their adviser. Ouch!

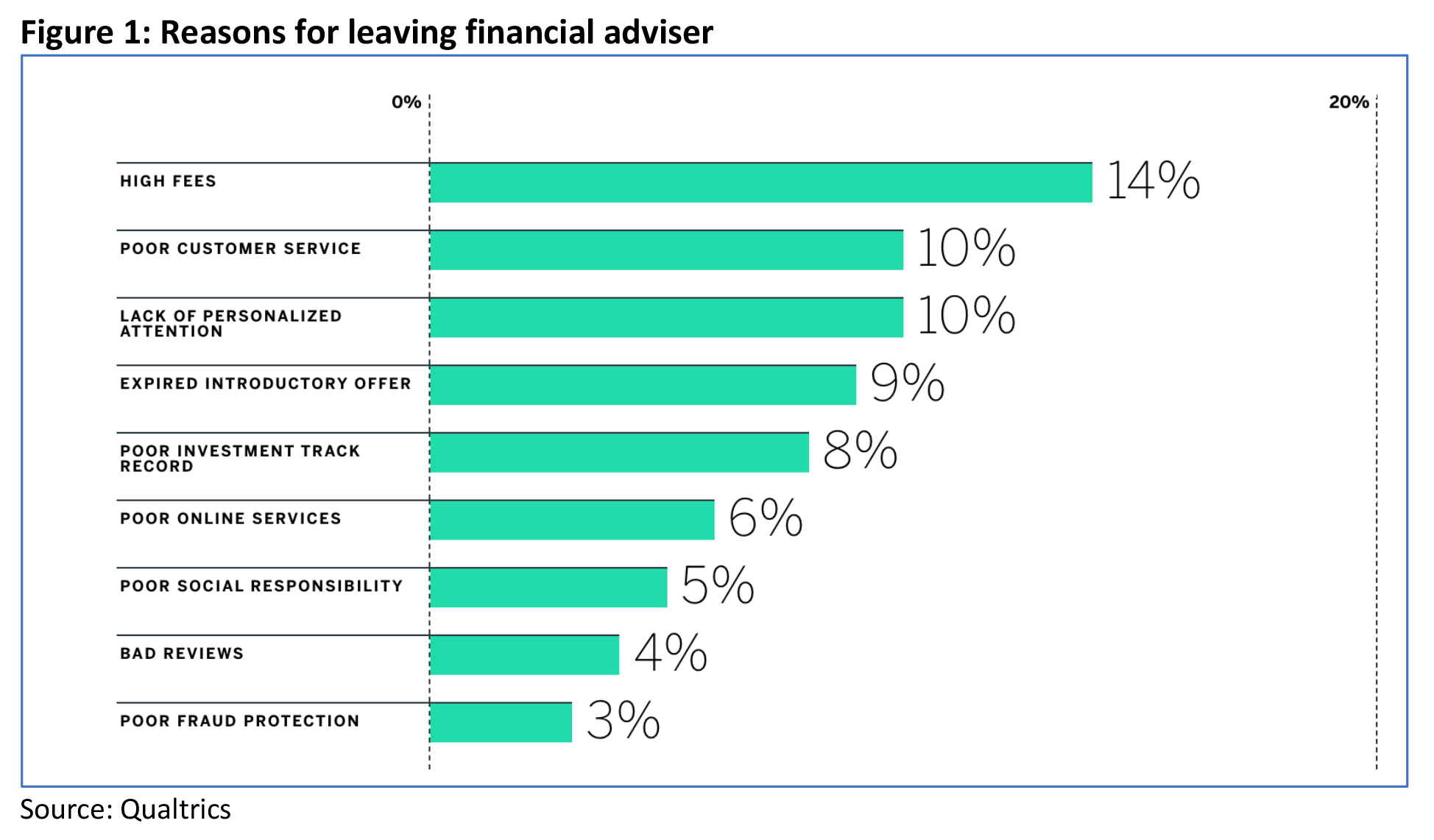

The best demonstration of how vulnerable such a ‘hard’ functional focus can leave you as an adviser can be seen in Figure 1 below, based on US research[6] into why clients choose to leave their adviser.

As can be seen, the top reasons for leaving an adviser revolve around an interconnected trio of customer service, poor investment performance and fees.

The interconnectedness relates to the way clients have perceived value as being tied up in service and investment performance, which is why when either of these fails to live up to expectations, the value vanishes, and the fees become too expensive.

The key then is to find a way to create value in a way which is beyond such functional metrics, and therefore makes clients more loyal in the face of service breakdowns, and more price inelastic when it comes to fees.

That way is to focus on the client experience (CX).

Customer service vs. customer experience

Fundamental to building an ‘unassailable’ advice experience is to first understand the difference between customer (client) service and customer (client) experience.

Customer service (CS) is generally functional and transactional in nature, and is reactive to a specific situation, such as a question or service issue with which a customer needs assistance. Service is ultimately provided by an individual. The functional nature of service makes it relatively easy to measure how effectively it is being delivered (call wait times, document processing times, complaints volumes, error rates etc).

Customer experience (CX) on the other hand is a more strategic, holistic approach that builds upon customer service in a way that affects how customers perceive all interactions with an organization. It’s about how you make a customer feel. CX encompasses every aspect of a company’s offerings, from its quality of customer care to its reputation, overall marketing, product and service features, and reliability. In contrast to CS, CX is much more subjective and based on general perceptions, which makes it difficult to measure.

But while CX may be harder to measure than CS, it is immensely more powerful, and can have a much greater impact – positive and negative – on a business.

It is also harder to replicate, and therefore more capable as a differentiator, and more impervious to external threats, a point neatly summed up by Kevin Kelly, noted futurist and founder of Wired magazine:

“You can draw a line in the sand. If you’re a business only focused on offering a service, you can be commoditised. Technology can replicate you and do it cheaper, faster, and better, all at the same time. But if you’re a business offering an experience, you’re immune. The human experience is one thing technology can’t easily copy.”[7]

In a way, CX gets to the heart of what a brand represents to a consumer – how that brand makes them feel. Whether we are talking about a cup of coffee or a Rolex watch, when the focus is on how that product makes a person feel, price becomes far less relevant (it’s why the café where the staff remember your name and your order is more likely to get your business than a café where they don’t, even if that café might be cheaper or make a better-quality coffee).

Raves versus rage – the business value of focusing on CX

While there is no shortage of research linking CX to business performance, a study[8] conducted by US customer experience advisory firm Watermark Consulting – examining the financial performance of wealth managers that focused on CX – is very pertinent and very recent. The findings of that study revealed the significant payoff (and penalties) associated with the quality of the customer experience in today’s wealth management marketplace.

Their study found that ‘admired brands’ with strong feedback ratings enjoyed shareholder returns significantly higher than firms with weaker ratings.

Commenting on these findings, Watermark founder Jon Picoult said:

“Over the long term, wealth management firms with a positive client experience are seeing shareholder returns that are on average 7.4 times greater than their less customer-centric competitors. That disparity in financial returns has nearly doubled over the past few years, widening the performance chasm between firms that lead in customer experience versus those that lag.”

What does a leading CX look like?

While service and experience are different, there is no doubt that service feeds into the overall client experience, and indeed, one way to think about client experience is as a composite of effectiveness, ease and emotions. Other experts talk about CX success as being built on client empowerment, participation and confidence.

One of the earliest books on the topic of CX was ‘The Experience Economy’ by Jim Gilmore and Joe Pine, released in 1998. One of the central concepts in their seminal work is the idea that time is the currency of value[9]. Consumers see value either in time well spent or in time well saved.

In an advice context, this means could mean streamlining processes and introducing automation that allows your client to spend LESS time on functional or peripheral interactions where this is little positive value to be gained (such as eSignatures), while improving the quality of, rather than reducing, the time spent in much richer interactions (such as face to face meetings).

Put another way, your website experience should be about fast transactions, quicker loading pages, easier navigation, and fewer clicks, whereas in physical channels the focus should be on building engagement and relationships.

Reducing friction is key

Customer friction is anything that makes it harder for a client to accomplish a goal, and as such, it is the enemy of a positive customer experience.

There can be many sources of friction in an advice context. To the extent financial services products are complex, a fear of the unknown or the unfamiliar – such as a client’s first meeting with you – automatically causes friction, as would the first time they receive a statement of advice (SOA).

When expectations aren’t clearly communicated, friction is the result. On your website, friction occurs when pages take a long time to load or if the navigation is complicated or users can’t get their basic questions answered. In your advice processes, friction occurs when a client has to explain the same thing to multiple people or the process for signing and returning a document isn’t quick or convenient.

With reduced friction, clients can achieve the same or better results with less effort, less stress and perhaps with less knowledge.

4 steps to building an extraordinary client experience

Julie Littlechild is a US-based expert on client experience and client engagement in financial advice. A frequent speaker at Australian adviser events, Littlechild has developed a 4-step plan[10] to help advisers elevate their focus from delivering great service to designing meaningful client experiences. A summary of these steps is provided below:

Step 1: Define an authentic niche

Littlechild believes that by using the right tools – such as a service matrix – it is possible to deliver high levels of service to all clients. But she believes it’s virtually impossible to deeply engage a diverse client base and provide a great experience when they have such different needs. It is far easier to personalise and co-create client interactions when you build your experiences around a narrow set of client needs and perspectives.

For this reason, she believes you need to identify a niche, either at the business level or by segmenting your client base (and focusing the experience around your most important segment).

An authentic niche is one that is compelling to you and the client. Questions to ask yourself when defining a niche would include:

- What are your areas of expertise?

- What characteristics define your ideal client?

- What niches are compelling to you, and how could you define them in a way that resonates with your clients?

Tip: defining a niche in terms of their age or lifestage or investable assets is unlikely to be compelling or authentic.

Step 2: Actively involve your client in co-creating the experience

The best way to understand what experiences your clients would view as extraordinary is to ask them. Select 5 – 10 of your ‘focus clients’ and ask them about their best client experiences outside of their dealings with you. You might ask them:

- What was your best ever service experience and why?

- Which brand or professional had the most profound impact on you and why?

- Can you walk me through the entire end to end experience?

Asking these same questions of a group of clients will uncover themes around which you can start to design a new experience. Overlay those themes with your own positive and negative experiences as a customer, and you start to have a rich foundation.

And remember, even in the context of a highly regulated sector like advice, there is still scope for genuine co-creation or experiences, for example in obvious areas such as communications channels and frequency, but also in more fundamental areas such as the number of meetings involved in designing a financial plan, the way that plan is presented, and the onboarding process.

Step 3: Map the client journey

Mapping out the entire lifecycle of your client’s interactions with you is an invaluable way of understanding the touchpoints where an experience is delivered, and the way your client’s needs evolve through that lifecycle. This lifecycle usually starts before they have even become a client, and are doing their initial research, which is why your website is so crucial in shaping that first impression.

Is your website designed to create a feeling in your client, give them an experience, or does it really just showcase your service offering and qualifications?

Journey mapping involves identifying all the steps the client takes to solve their problem and trying to define what they are thinking at each stage of that journey and what pain points they may encounter along the way.

Although journey mapping has typically been done by large brands and organisations, there are tools available that make it scalable to the needs of smaller advice practices. A number of providers have developed downloadable toolkits[11] to enable advisers to map out the client experience – from the client’s very first interaction with your business (perhaps via your website or your office reception) to ongoing engagement.

A truly engaging experience needs to be based on real customer insight and input, and delivered consistently by all staff across the entire business. For that reason, a process where staff and clients map out the client journey and co-create solutions to pain points is optimal.

In a world where clients engage across multiple channels, consistency of experience is critical. An example might be how you treat new prospects who ring your office versus those who complete the enquiry form on your website. Is the experience delivered to them the same in terms of timeliness, detail and quality?

Step 4: Innovate

Personalisation is key to building a memorable client experience, but to achieve this across a diverse client base may require innovative thinking. Fortunately, even small changes, such as developing unique communications for specific segments within your client base can pay dividends.

Technology can play an obvious role here. One simple example might be the introduction of an online booking system for appointments, allowing clients complete freedom and convenience in booking appointments.

Examples of great client experiences

Over and above exceptional service – which is expected – there are many different ways to deliver an engaging, memorable client experience, with the only limit being your imagination. As a catalyst for your thinking, think about the opportunities that exist beyond the core advice processes – in your communications, in your office experience, in your onboarding, and in your client events.

Communications in particular remains a weakness for many advisers. According to the Business Health Future Ready 2019 Report[12], only 27% of advisers claim to contact their best clients 10 times or more per year, and in a survey of 52,000 advice clients, communication was rated as the second worst performing element of the client experience.

- Rather than having a sterile reception area, have a tv playing TED or TEDx talks on loop, so your clients can learn something while they wait.

- Provide a personalised leather binder (vegetable leather if you want to be more ESG friendly) for advice documents.

- Communicate with clients in their preferred channels, which may include WhatsApp or social DMs, or even short video messages (obviously don’t use these channels for sensitive communications or documentation).

- Think about whether your office décor and your dress code reflect your target clientele.

- Have a range of premium merchandise, with very subtle branding, for special clients.

- Personalised metal credit card style client/membership cards with contact details and other information convey a very premium feel.

- Think about providing ‘money can’t buy’ experiences – either as events or gifts.

- Remember some clients have little interest in attending your events, if you have an allowance for hospitality, allow them to experience it in their own time, such as via gold class cinema tickets or via a premium in home dining experience (like Providoor).

- Team up with a life coach or counsellor and offer complimentary sessions and resources that help them define their values and goals.

- Make regular reading recommendations and provide selected clients with a copy of the latest ‘it’ book on business, personal effectiveness or personal finance.

- Provide access to free or subsidised cash management and budgeting software/apps.

Of course, the most important way to create a memorable experience is to truly understand your client as an individual and interact and engage in way that is deeply personal.

Conclusion

Against a backdrop of volatile investment markets and rising inflation, access to financial advice has never been more important, yet the rising cost of advice is creating a barrier to both prospective and existing clients engaging with an adviser. Whil opportunities to lower the cost of advice will be welcomed, to make advice truly unassailable – by making advice clients more inelastic to the price – advisers need to think about value differently and elevate their focus from customer service to client experience. A truly memorable and engaging advice client experience, beyond the more functional and financial aspects of advice will render the cost of advice far less relevant to clients assessing the real value of their adviser.