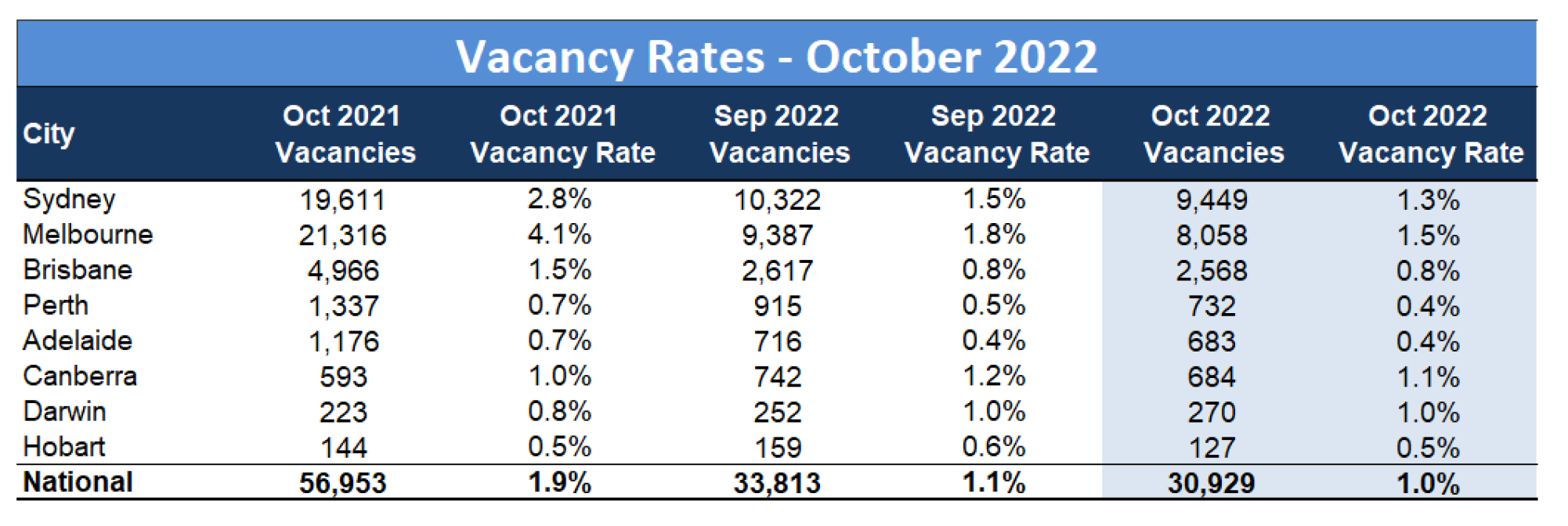

SQM Research has revealed national vacancy rates fell in October to 1% from a revised* 1.1% recorded in September.

The total number of rental vacancies Australia-wide now stands at 30,929 residential properties, which is a decrease from 33,813 in September.

Sydney, Melbourne and Canberra vacancy rates fell from 1.5%, 1.8% and 1.2% to 1.3%, 1.5% and 1.1%. Darwin remained constant at 1%, and in the smaller capital cities, Brisbane, Perth, Adelaide and Hobart, vacancy rates sat well below 1.0% over October.

Vacancy rates in the Sydney CBD rose to 3.5%, Melbourne CBD and Brisbane CBD fell to 2.6% and 1.2%, respectively. SQM also records an increasing number of regional townships and regions recording a rise in vacancies. Some of the regions include Sydney’s Blue Mountains, Wollongong, NSW North Coast, Northern Victoria, and Gippsland as some examples.

SQM’s calculations of vacancies are based on online rental listings that have been advertised for three weeks or more compared to the total number of established rental properties. SQM considers this to be a superior methodology compared to using a potentially incomplete sample of agency surveys or merely relying on raw online listings advertised. Please go to our Methodology[1] page for more information on how SQM’s vacancies are compiled.

Rents

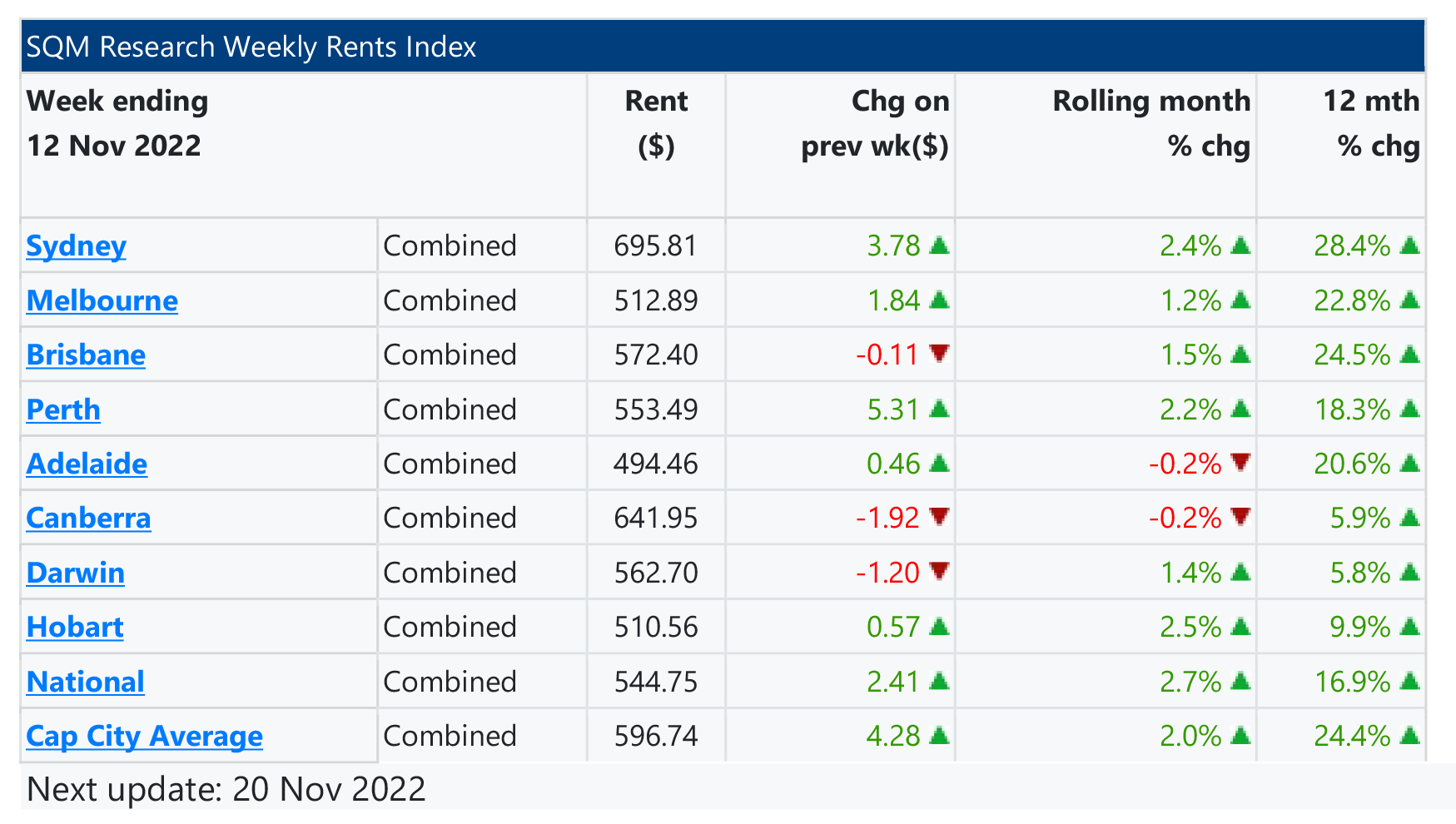

Over the past 30 days to 16 November 2022, capital city asking rents rose by another 2% with the 12-month rise standing at 24.4%. While broader national rents, taking into accounts all regions, rose by 16.9% for the same 12-month period.

The national median weekly asking rent for a dwelling is recorded at $596.74 a week. Sydney recorded the highest weekly rent for a house at $871.37 a week.

While Adelaide units offer the best rental affordability of all capital cities at $494.46 a week. Page 2 of 2 Louis Christopher, Managing Director of SQM Research said: “The national rental market is still very much in favour of landlords, particularly for our capital cities where there is no evidence yet of any easing in the rental market. However there is some good news for tenants in a number of townships and regions outside the capital cities whereby SQM Research is now recording a consistent rise in rental vacancy rates, albeit from a very low base.

This easing might be attributed to a population flow back into the cities whereby an increasing number of white-collar workers are being asked to come back into the office. However, if we are correct in this assessment, this means the capital city rental market will continue to be under great strain for tenants over the foreseeable future and may not ease until late 2023 at the earliest.

And as we can see through the asking rent increases over the past 30 days, the capital city rental crisis remains with us to this day.”

*Revision Note

Once every five years after the Census release, SQM Research revises its rental vacancy rate series to reflect the new information surrounding national dwelling counts. This ensures our rental vacancy rates remain accurate and reflect the most recent and most comprehensive information surrounding the number of rental dwellings across Australia. The revision effects the denominator (number of established rental dwellings). In the past, the revision has meant between 0.1% to 0.3% differences on the stated vacancy rates just prior to the revision. For the 2021 census update, the impact was a revision upwards in the vacancy rates by an average 0.3%. Some postcodes recorded larger revisions upwards and some downwards.

——-