Risk claims handling – rethinking the advice approach post-QAR

Can reframing claims handling as claims advocacy capture value at claim time?

Ahead of the Quality of Advice Review’s final report being released, Michelle Levy gave some early clarity on the topic of commissions in life insurance, when she made public her recommendations [1] that 1) commissions remain permissible and 2) they should remain at the current levels (60/20).

Although the clarity was welcomed in many quarters (so called consumer advocacy groups being a notable exception[2]), several high-profile industry participants[3] have been quick to point out that, within the existing regulatory framework at least, providing compliant risk advice within a 60/20 model remains economically challenging.

Within this context, advisers must take the opportunity to examine their business model from many perspectives, including the ways they deliver value to clients, and how they in turn commercialise that value.

It is hard to argue that the true value of life insurance – indeed any type of insurance – is only realised in the event of a claim, and certainly assisting clients to lodge and manage claims is one of the most important services a financial adviser can offer.

But whilst traditionally most advisers have managed claims without charging any extra fees (arguing that the commissions they receive are in effect payment in advance for such a service), this approach is becoming increasingly questionable. This is especially true in light of both the aforementioned economic challenges, and the increasing complexity of life insurance claims, exacerbated by newer style IDII contracts and the growing number of people experiencing poor mental health.

It is a given that advised life insurance clients get better claims outcomes, and that many advisers regard claims management as one of the most rewarding aspects of their role. But unless the remuneration they receive for that role accurately reflects the work they do and the value they add, the incentive to cut corners and spend less time working and developing in this area will increase. And that could ultimately spell bad news for the client experience, the claims outcomes, and the adviser/client relationship.

Claims are now serious business

At the start of 2022, long mooted legislation relating to insurance (life and general) claims handling came into effect[4]. This legislation gave effect to a recommendation from the 2018 Hayne Royal Commission that insurance claims handling be regarded as a financial service, and be regulated as such. The main outcome of this was to require anyone involved in ‘claims handing and settling’ to hold – or be an authorised representative of – an AFS licence.

ASIC Information Sheet 253[5] sets out guidance around ‘claims handling and settling services’, defining such a service as:

These activities include:

- making a recommendation or stating an opinion in response to an inquiry about a claim or potential claim

- making a recommendation or stating an opinion that could influence a decision about making or continuing with a claim

- representing someone in pursuing a claim

- assisting another person to make a claim

- assessing whether an insurer is liable under an insurance product

- making a decision to accept or reject all or part of a claim

- quantifying an insurer’s liability under an insurance product

- offering to settle all or part of a claim, or

- satisfying a liability of an insurer under a claim.

These services include those provided to the insured person, and third-party beneficiaries.

To the extent financial advisers already operate under strict licensing and compliance requirements, the direct impact of this change on advisers and their employees was minimal[6], especially when compared to many participants not previously required to be licensed (including some insurers and claims advocates). Nevertheless, the introduction of the legislation underscores the expectations that claims must be handled to the highest standards of compliance, client care, and professionalism, and that the provision of these services will be under heightened scrutiny.

APRA’s latest claims statistics

In October 2022, APRA released the life insurance claims and disputes statistics for the 20/21 financial year[7].

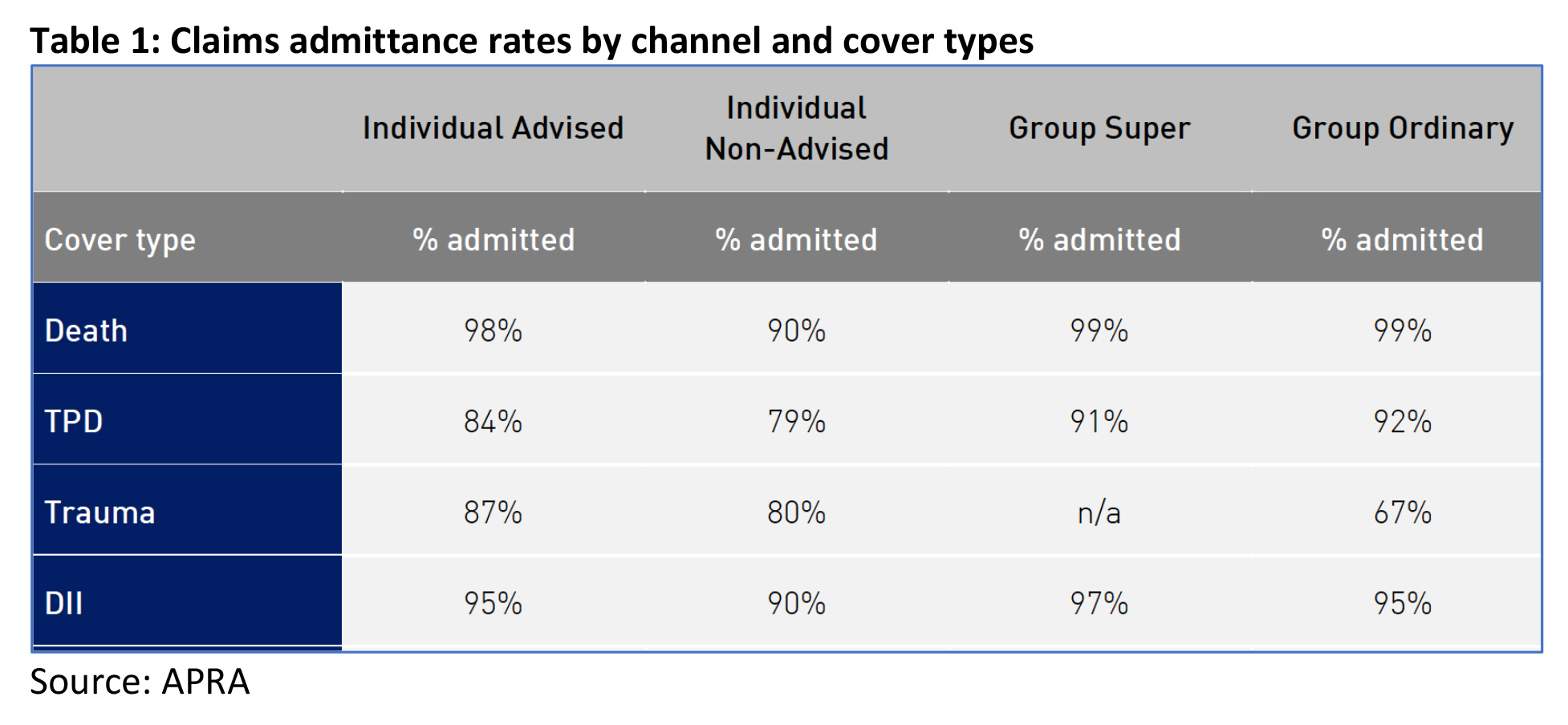

The data reinforces a number of important points about life claims, including the massive volume of claims being paid in any given year, the length of time it can take to settle claims, and the superior claims outcomes for advised claimants versus direct policyholders.

In terms of claims volumes, FY22 saw life insurers admit over 80,000 claims, including over 44,000 group super claims, and 16,132 retail advised claims. DII (income protection) had the most claims admitted, followed by TPD.

In terms of claim admittance rates, as Table 1 reveals, retail advised clients continue to achieve higher claims acceptance rates across all product types, relative to those holding direct policies (admitted rates for rates for group products are higher still because auto-acceptance removes non-disclosure as a factor).

Claims can be complex and time consuming

Life insurance claims can be complex and time consuming, due to a number of factors:

- complexity in product design making eligibility for benefits challenging to determine (this applies as much to new era IDII products as it does to older, legacy style products in all categories)

- complexity in the evidence required to support a claim, ranging from death certificates and probate forms to medical reports, and comprehensive financial documentation

- factors which impact the willingness and/or ability of claimants to assist in the process, such as their location, cognitive ability, or emotional state.

Benchmarking several years ago[8] revealed just how time-consuming claims could be:

- 34% of claims took 11-20 hours to manage

- 22% took between 20 and 30 hours

- 19% took more than 30 hours.

TPD claims, which are subject to more comprehensive medical evidence, and which can also throw up a number of tax traps for unwary claimants, are like to be at the upper end of these ranges.

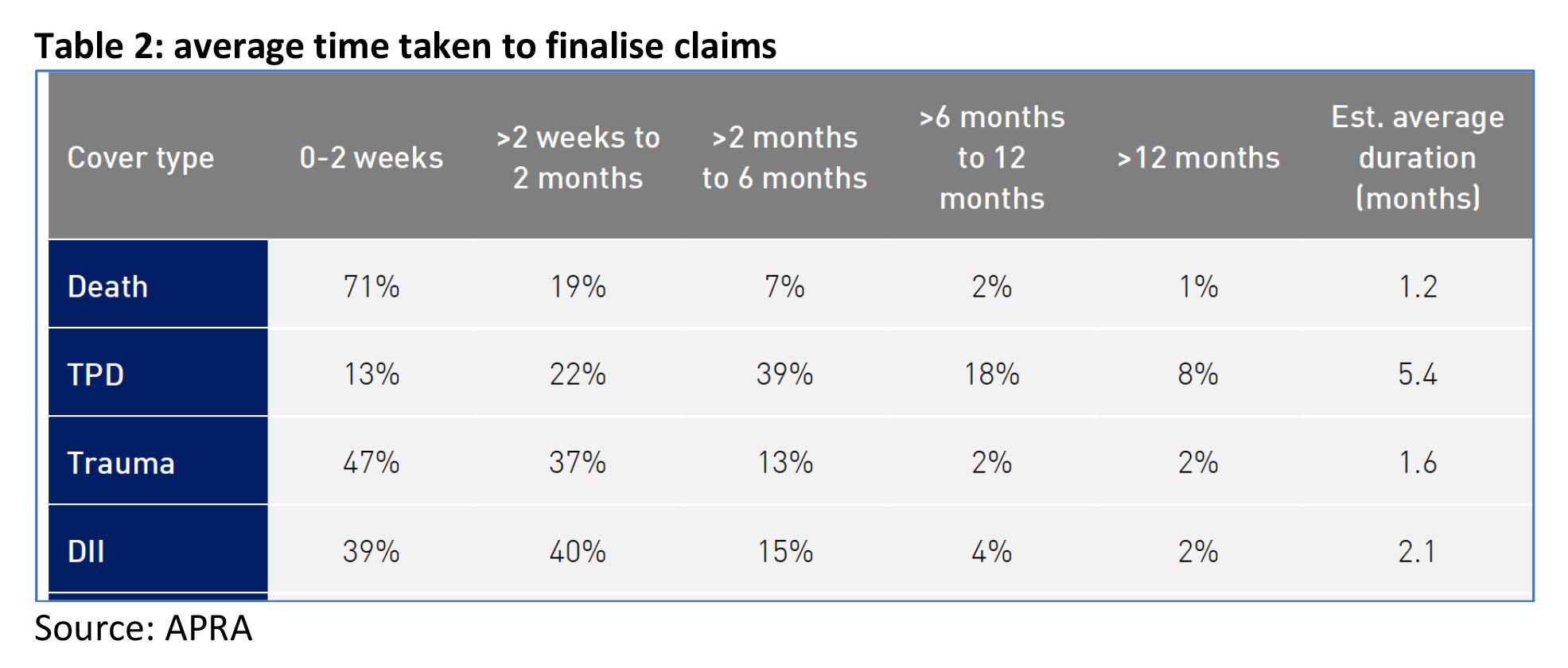

The total processing duration of claims can also be long too, even for relatively straightforward claims, meaning they remain as open tasks which require monitoring and reporting, often over a period of months not weeks (ongoing IDII claims can of course be open for years).

APRA’s reporting on average claims duration, as shown below[9], revealed the average claim duration ranges from 6 weeks to 6 months, and although averages can be misleading, the point is clear that claims are more likely to be open for months, not weeks. (Note, in the table, ‘duration’ refers to the processing duration).

From claims handler to claims advocate

Handling claims successfully for clients requires a great deal of technical skill, communications ability, and emotional intelligence. At the same time as needing to be able to understand and decipher complex policy wordings, some of which may date back decades, advisers need to understand the specifics of claims processes which differ from product to product and insurer to insurer, and they need to communicate with, and care for, clients likely to be in an emotionally vulnerable state, depending in the circumstances of their claim. Advisers need to show empathy and set expectations around timeframes and potential outcomes (positive and negative).

In other words, handling claims for clients is not simply a matter of helping them with paperwork, it is about being a professional advocate on your client’s behalf.

The business imperative to become a claims advocate

If we pull together the threads of the insurance claims narrative thus far, it is becoming clear that:

- managing claims is complex and demands specialised technical and relationship management skills

- the regulatory framework around claims is becoming more onerous

- managing claims within a framework of professionalism and high-quality service is very time consuming

- the cost of the adviser’s time in providing this service and keeping their skills up to date will often far exceed the remuneration they receive by way of commissions.

In other words, managing claims can be a loss maker, begging the question, is now the time to redefine the role of advisers from being that of claims manager or handler, to Claims Advocate?

How is Claims Advocacy different from simply helping my client at claim time?

The role of Claims Advocates is to help their client navigate the claims process with one or more insurers. A typical process could look like:

- Understand the claimable event.

- Investigate potential eligibility for claim, including examining policy terms and any applicable exclusions.

- Understand processes specific to the client’s insurer.

- Assist with the completion and submission of forms and gathering and provision of other requested documents.

- Liaison with insurers, medical specialists, employers, trustees, and other external parties as part of step 4.

- Educate, update, and inform the client throughout the process.

- Where appropriate, advise on any tax or other financial implications of the claim payout.

- Facilitate payment.

For some advisers, particularly risk specialists, this process may seem virtually identical to that they already follow when managing a claim for a client. And whilst that is largely true, Claims Advocacy has a few key distinguishing features:

- it is a true end – to – end service

- it is a specialised service which requires the Claims Advocate to gain a deep understanding of the claims processes of different insurers and become an expert in dealing with medical practitioners and other experts (according to one study[10], only 50% of advisers dealing with claims have ever been trained in this area)

- it is articulated and documented as a separate service, which the Claims Advocate provides as a core offering (rather than a value add)

- it is a service that can be provided to clients who didn’t obtain their insurance through you, and – crucially

- it is a service for which there is a clearly documented cost of provision, and for which the client is charged.

Will clients pay for Claims Advocacy?

The best answer to this question lies can be seen in the number of businesses actively providing and charging for such services.

In the area of Claims Advocacy, legal firms – many operating on a ‘no win, no fee’ basis – have become highly active in this space in the last few years. Some larger legal firms have even invested in advertising campaigns, many of which target superannuation fund members who may be unaware they even have any cover.

Examples of such targeting can be seen on the first page of a Google search for ‘TPD claim’ (at the time of publishing, 5 of the first 6 results for this search were law firms).

With some ‘no win, no fee lawyers’ taking as much as 40% of a successful claim payout in legal fees[11], their involvement is the source of ongoing – often heated – debate within the financial advice profession. Regardless, it suggests clients are more than happy to pay a fee for a valuable service, provided there are claims proceeds from which to pay that fee.

Happily, we are starting to see the emergence of Claims Advocacy firms from within the financial advice profession. In some cases, this is purely done as a way of elevating the quality of the service provided to existing clients, in others, advisers are looking to provide this service to non-clients, some with a growing number of financial advisers incorporating Claims Advocacy into their service offering, some even going so far as to establish standalone businesses to do this at scale. (These firms undoubtedly view the tens of thousands of ‘unadvised claims’ – such as those made by super fund members and direct policyholders – to be an obvious target for such a service.)

Clients don’t automatically expect advisers to do this work

The other data point that can help us gauge the client’s willingness to pay for claims advocacy is research which revealed – perhaps contrary to expectations – that most clients don’t instinctively expect to approach their adviser in the event of a claim. The Beddoes/AFA Whitepaper[12] found many policyholders “expect to go direct to their insurance company in the event of a claim, irrespective of the channel through which they took out their policy”.

In other words – the number of clients who expect you to do this work could be small, and the number who expect you to do it on an unpaid basis, could be even smaller.

How much should you charge for Claims Advocacy?

There is no definitive answer to this vexed question, although avoiding the approach used by the no win no fee lawyers could be the way to go if maintaining client relationships is important!

One starting point is obviously to base a fee purely on the hours spent managing a claim. So, a total of 30 hours spent managing a claim might cost $9000 at $300 per hour. Whilst seeming equitable to both client and adviser, this can become problematic if a claim is complex but low value.

Conversely a flat fee, agreed in advance, gives certainty, but can be problematic if the actual time spent is far greater or far less than that estimated.

A percentage-based fee may be easy to sell to a client (especially if it is a reasonably modest one), however complexity often bears no relation to size of the claim, and so this approach could prove unfair to either the claimant or the adviser.

Some standalone claims advocates use a combination of all these methods, charging a flat fee in conjunction with a modest percentage (capped in some cases). Also seen is the application of different fees to different product types, with TPD and IDII claims attracting higher fees than death and trauma.

Ultimately, the right approach will vary from adviser to adviser and client to client.

In summary

Claims management is a core propositional element for most advisers active in the life insurance space. Yet a reliance on historical commission streams which bear no relation to the cost of providing claims services, can end up short-changing the adviser. When claims become a loss-making service, in an already challenging economic framework for risk advice, this can act to diminish an adviser’s incentive to invest their maximum energy in developing and maintaining critical claims management knowledge, and in providing a high quality, professional claims service.

To the extent that consumers with a pending claim can more easily understand the end benefit of Claims Advocacy services, they are likely to be more willing – and able – to pay for such support, especially when those fees can be paid from the proceeds of a successful claim. As a result, reframing claims management as Claims Advocacy not only helps elevate the professional reputation of advisers, it also creates opportunities for advisers to both provide, and capture, more value at claim time.

![]()