Complexity in advice – how it undermines financial consumer protection

The complexity which characterises the financial services sector undermines consumer protection, a fact acknowledged in the ALRC’s recent review.

Adviser’s don’t need to be reminded how complex the world they operate in is. Financial products, regulations, advice processes and documents are all inherently complex.

The deep irony is that while much of this complexity is a direct result of efforts to protect consumers, the end result is actually the opposite, with consumers confronted by a system in which complex products and impenetrable disclosures encourage sub-optimal decision making, and multiple layers of regulation drive the cost of expert advice beyond the reach of everyday Australians.

The extent to which complexity is the scourge of consumer protection was highlighted by the recently completed review into financial services law, conducted by the Australian Law Reform Commission. Their Report ‘Confronting Complexity: Reforming Corporations and Financial Services Legislation’ – was tabled in parliament and publicly released on 18 January 2024[1], containing no less than 58 recommendations to streamline and simplify financial services regulation, including several recommendations aimed at ensuring laws are easier to update and maintain.

Interestingly, the Report itself noted the extent to which the complexity of existing financial services laws was driving up the cost for all stakeholders.

In this article, we will examine the insidious impact of complexity in financial services, primarily through the lens of the ALRC’s recent Report, but also referencing studies conducted in the areas of disclosure and communication complexity, the interplay of which can place consumers at risk of poor decisions and poor financial outcomes. By gaining a deeper understanding of all these issues, financial advisers will be much better equipped to consider – and perhaps adjust – their own client engagement techniques and processes with a view to strengthening their inherent consumer protections.

Financial services law: ‘no longer fit for purpose’

The ALRC inquiry was part of the Government’s response to the Royal Commission into Misconduct in the Banking, Superannuation, and Financial Services Industry. Borne of the recognition that the complexity of financial services legislation (the Corporations Act is over 4,000 pages long and contains more than 600 terms with multiple definitions) was a contributing factor to some of the sector’s failings, the review had three specific areas of focus:

- Design and use of definitions

- Legislative design and hierarchy

- Reframing of Chapter 7 of the Corporations Act (where much of the legislation was contained)

The final ALRC Report – the result of years of labour by five ALRC commissioners, 22 ALRC staff, four consultants, 56 students, 17 advisory committee members and 24 expert readers[2] – concluded that existing financial services laws are ‘no longer fit for purpose’.

The Report stated:

“The existing legislative framework is unnecessarily complex, and the tools used to build and maintain the framework — such as notional amendments, conditional exemptions, and proliferating legislative instruments — often create more problems than they aim to solve. Much legislation is unclear and incoherent, and the objective of an adaptive, efficient, and navigable legislative framework remains unrealised.”[3]

Identifying the drivers of complexity

In what would hardly be news to advisers, the Report noted that financial services legislation had at various times been described by Judges as ‘porridge’, ‘tortuous’, ‘exceptionally complex’, ‘labyrinthine’, and as needing to be ‘deciphered’, rather than interpreted.

Specifically, the Report identified some of the key drivers of this complexity as including:

- Hard to navigate: In the sense of being hard to find (because of the number of different places users must look in the 4,000+ pages of the Corporations Act)

- Failing to prioritise key messages: Many provisions in Chapter 7 of the Corporations Act and Part 2 Div 2 of the ASIC Act are structured and framed such that their purpose and context are hard to discern, and fundamental norms of behaviour are not clearly communicated.

- Complex definitions: Terms are sometimes defined unnecessarily or inappropriately. The Corporations Act also uses poorly designed terms and definitions, such as unintuitive abbreviations, or definitions that impose obligations or vary the application of the law rather than clarify meaning.

- Definitions are often inconsistent: For example, key terms such as ‘financial product’ are defined differently in related Acts, and even in different provisions of the same

- Definitions are not always well designed: The Report noted numerous ways in which definitions in corporations and financial services legislation could be made more readable and navigable for users, including limiting the use of interconnected definitions, using intuitive labels for defined terms, and making clear whether definitions are exhaustive or inclusive.

Does the industry have itself to blame?

Interestingly, the ALRC has previously suggested that much of this complexity results from demand from industry and regulators for increased certainty4. In response, the laws adopt an overly prescriptive approach to regulation (rather than a broad ‘principles based’ approach), resulting in false certainty, with too much prescription actually obscuring the clarity of the law. For example, the principles-based obligation that ‘a provider must act in the best interests of the client in relation to the advice’ is 16 words long, but for several years has been tied to the current prescriptive ‘safe harbour defence’ that is 261 words long[5].

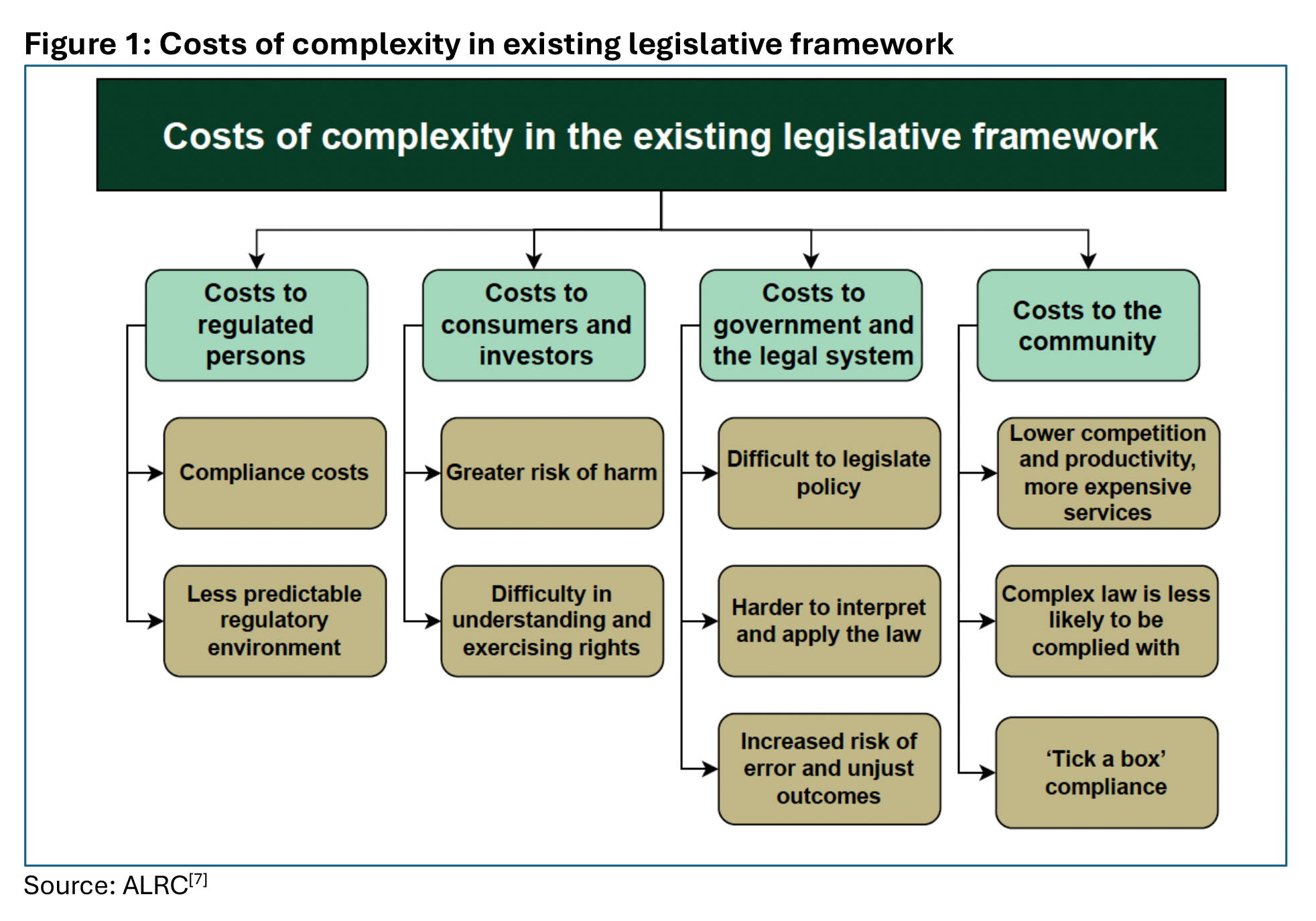

The cost of this complexity – to advisers and consumers

Rather than been an abstract concept, complexity comes with real – financial – costs to all stakeholders within the legal system, including businesses, consumers, and the community at large:

- For businesses (including AFSLs and product providers), complexity stifles innovation by creating uncertainty over legal interpretation, and adds to the cost of operating in the form of expensive legal and compliance resources needed to ensure adherence to the law. Spending hundreds of thousands of dollars on such resources is common, which can be a crippling overhead for smaller practices.

- For consumers the costs are many, including picking up the tab for the legal and compliance resources required by businesses. It can also be more costly for consumers to understand and enforce their rights.

- For the community at large, legislation that is harder to understand is less likely to be complied with, which can lead to consumer harm from suboptimal products and sales practices. A loss of trust emanating from this complexity can also deter them from embracing advice at all, increasing the likelihood of poor decision making. The barriers to entry for new firms or international competitors – who must have both the resources and the willingness to confront the complexity of the existing legislative framework – ultimately denies the community access to a more innovative, competitive marketplace. (The reluctance of international digital advice platforms to enter Australia under the current legislative regime is just one example[6]).

58 ways to solve the problem

The ALRC has noted reduced costs of compliance and enforcement as a desired key outcome of their proposed reforms, which the Report distils into 58 recommendations to streamline and simplify financial services regulation, addressing technical simplifications and structural changes in legislation governing financial products and services.

Recommendations 1-23, previously outlined in three interim Reports, focus on technical simplifications without significant policy implications. Thirteen of these recommendations have been partially or fully implemented already[8].

Recommendations 24-58, introduced in the Final Report, centre on overhauling the structure of existing legislation related to financial products and services, specifically in the Corporations Act 2001 and the Australian Securities and Investments Commission Act 2001. The aim is to facilitate easier updates and maintenance of laws in the financial sector.

Recommendations specific to advice, disclosure, and consumer protection

Among the recommendations of the Final Report are several aimed at simplifying and consolidating existing provisions within the legislation, to improve clarity and navigability. In simple terms these involve ‘grouping’ provisions in the one place. Groupings include consumer protection, financial advice, disclosure, misleading and deceptive conduct, and civil penalty provisions.

Recommendation 38 – relating to financial advice – recommends “grouping and (where relevant) consolidating”:

- Sections 912EA and 912EB

- Part 7.6 Divs 8A, 8B, and 8C

- Part 7.6 Div 9 Subdivs B and C

- Part 7.7 Div 3

- Section 949A

- Part 7.7A Divs 2, 3, 4 (excluding s 963K), Div 5 Subdiv B, and Div 6, and

- Sections 1012A and 1020AI.

Implementation roadmap

The architects of the proposed reforms incorporated several mechanisms designed to make implementation of their proposals quicker and easier.

Firstly, while they proposed the creation of a dedicated group of provisions that would be called the Financial Services Law (FSL), to be enacted as a schedule to the Corporations Act, they have structured their recommendations so that even if the FSL Schedule approach is rejected, recommendations 33 to 40 (which include those relating to consumer protection and financial advice)) “may be implemented independently”.

In other words, they have ‘futureproofed’ their proposals.

Secondly, they have recommended an implementation roadmap, built around the following 6 pillars:

- consumer protection

- disclosure

- financial advice

- other regulatory obligations and licensing

- miscellaneous

- policy evolving provisions.

These pillars are designed to ensure they could be implemented withing a single term of parliament, and may also be implemented sequentially or simultaneously.

The first three pillars are noted as being the ‘priority pillars’. In relation to the financial advice pillar, the Report notes that:

“Financial advice provisions are significant because they regulate one of the key means through which consumers access financial products and services. Multiple governments have reiterated the importance of effectively regulated and affordable financial advice. A simplified legislative framework would be an important step to reducing the costs of advice, supporting advisers to understand their obligations, and promoting higher quality advice.”[9]

At the time of writing, while the Federal Government had made the ALRC Report public, it had not formally responded, although it is clear that the substance of the recommendations is unlikely to cause any controversy.

Complexity in the real world

To give further reinforcement to the real-world manifestation of complex financial services law, the conservative ‘over-compliance’, and the resulting costs to consumers, it is worth revisiting a number of studies conducted specifically in the areas of disclosure and communication.

There is an increasing realisation that disclosure – once regarded as a key pillar of consumer protection – can actually work against consumers, overwhelming them with long, complex disclosure documents which make it harder, not easier, to make a good decision.

ASIC has released a number of Reports touching on this topic, including REP 384[10] (‘Regulating Complex Products’) and REP 632[11], their joint Report with the Dutch financial markets authority AFM (‘Disclosure: Why it shouldn’t be the default’).

In REP 384, ASIC noted that ‘where disclosure is not clear, concise, and effective, there is a greater risk that investors will not make an informed decision when acquiring a complex product, which in turn may result in the selection of a product that is not suitable for their circumstances’[12].

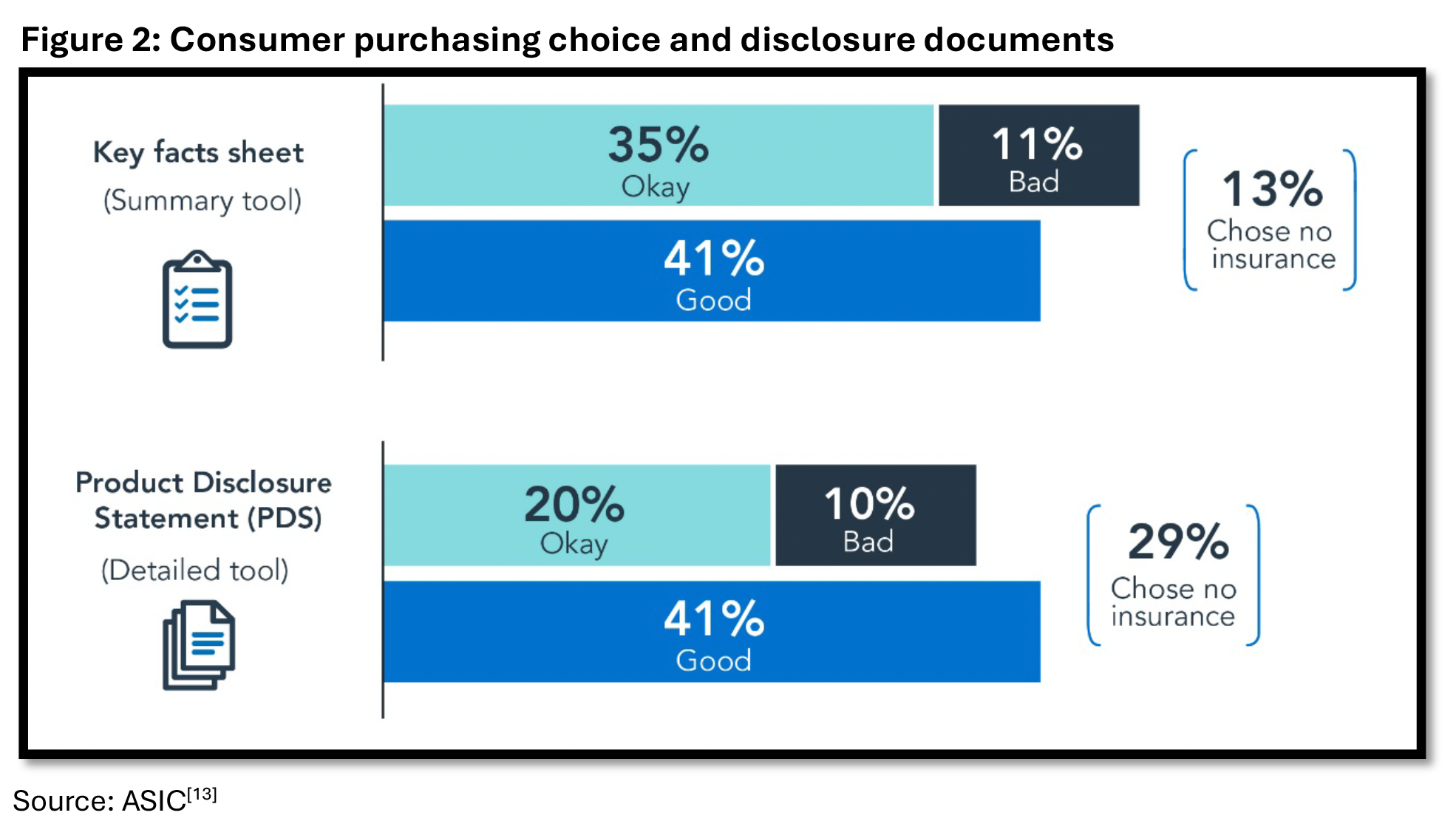

Their work with AFM went one step further, conducting a number of studies involving disclosure documents of varying length and complexity, and the resulting impact on consumer decision making.

These studies involved different categories of products including insurance and investment bonds. In both cases, a clear correlation was found between the length of the disclosure document and the quality of the consumer decision making.

Figure 2 below shows the results for the experiment involving home insurance. Half the participants were given the full PDS for a home insurance product, with the other half given a shorter Key Features Statement. ASIC found those using the Key Features Statement were significantly more likely to make a choice rated as good or ok. Those given the full PDS were significantly more likely to choose no insurance (itself a bad outcome).

SOA complexity

Notwithstanding that the SOA is finally being scrapped – as recommended in the QAR Final Report – understanding the power of the SOA to affect consumer comprehension, trust, and decision making, may help advisers and AFSLs when designing their new advice documents.

While it would hardly come as a surprise that the SOA – or at least, the way some AFSLs choose to produce it – can actually work against the concept of informed consent, and reduce, rather than increase, the understanding consumers have of the advice they receive, it is still instructive to examine the findings of a recent university study of SOAs.

Conducted by Ben Neilson for the University of Southern Queensland, the empirical study[14] of Australian SOAs set out to examine the impact financial content structure had on consumer appreciation, decision making, and relationship quality.

The 2023 study, which introduces new datasets surrounding SOA documents and their impact on comprehension, value, and trust, concluded that the clarity, organisation, and formatting of SOAs are particularly important to assist with consumer decision making.

Using a reimagined financial content structure that incorporated language improvements, explanatory videos, and hyperlinks, Neilson compared this structure to a selection of SOAs sourced from around the market.

According to Neilson:

“The findings revealed that the structure of financial content significantly influences consumer appreciation, particularly with respect to clarity, organisation and formatting, all of which play pivotal roles in shaping decision-making processes. Notably, our restructured financial content received higher levels of consumer appreciation, suggesting the potential for a shift in Australian professional practice.”[15]

In summary

The complexity which characterises the financial services sector undermines consumer protection, a fact acknowledged in the Australian Law Reform Commission’s (ALRC) recent review.

While designed with the intention to safeguard consumers, the intricate web of regulations, definitions, and disclosure requirements results in a system where consumers exercise suboptimal decision-making and advisers’ costs soar. The ALRC’s Report, ‘Confronting Complexity: Reforming Corporations and Financial Services Legislation,’ identifies both the drivers of complexity – including hard-to-navigate legislation, poorly designed definitions, and inconsistent terminology – and the associated costs to businesses, consumers, and the community. The Final Report contains 58 recommendations to simplify the regulatory framework – addressing both technical and structural aspects – and proposes an implementation roadmap with six pillars, prioritising consumer protection, disclosure, and financial advice.

Additionally, several other studies, including those by ASIC, reinforcing the positive impact that reducing complexity in advice processes and documentation can have on consumer comprehension, decision making, and trust in their adviser.