An improved knowledge of private credit markets and understanding the investment opportunity available to clients from an allocation to private credit.

Private credit offers investors an attractive opportunity to benefit from regular income, strong investor protections and low volatility, irrespective of the economic conditions that prevail during 2024. This article from GSFM examines this asset class, provides an outlook for the year ahead and explores the investment opportunity private credit presents for your clients.

Private credit or private debt – terms that are used interchangeably − is an asset class comprised of privately negotiated loans and debt financing from non-bank lenders. It operates independently from the traditional banking system and serves as an alternative source of financing for privately held companies in the form of loans, bonds, notes, private securitisation issues or asset backed financing. In effect, it spans any non-listed debt product. Private credit covers a wide range of risk profiles, from the largest investment grade blue chip corporates all the way to small startup venture capital types of businesses.

The sector been on a strong growth trajectory worldwide, as the reluctance of traditional lenders to lend has widened the opportunity set for investors. Total assets in private credit have nearly doubled since 2020 to $1.6 trillion and are projected to increase to $2.3 trillion by 2027[1].

Private credit has continued to surge in Australia. Super giant AustralianSuper has more than $4.5 billion invested in private credit globally. Furthermore, the fund expects to triple the exposure to private credit in the coming years[2].

All this means increased opportunities for investors as traditional lenders shift their focus toward servicing larger corporates. This move has left a large number of smaller borrowers looking elsewhere to meet their funding needs. Consequently, there’s been a large number of private credit providers enter the market to fill this gap, and an increase in the number of private credit funds available to investors.

Borrowers seek private credit for various reasons, including:

- An inability to access public credit markets or traditional bank financing

- Bank financing is too restrictive for the borrower’s needs

- Does not wish to be diluted by issuing new equity

- Requires funds quickly.

Why invest in private credit?

Investing in a private credit fund can offer several potential benefits to investors, including:

- Potential for attractive returns: private credit funds generally offer higher returns than traditional fixed-income investments because they invest in non-publicly traded debt instruments, such as private loans or structured credit, which typically offer higher yields.

- Diversification: private credit funds provide diversification benefits to an investor’s portfolio because investors gain exposure to a range of different debt instruments and borrowers, which can help to spread their risk and potentially improve the overall performance of your clients’ portfolios.

- Lower volatility: private credit funds can offer lower volatility amid geopolitical uncertainties, inflationary pressure and historically high asset valuations when compared to more traditional investment products.

- Access to institutional-quality investments: private credit funds have historically been only accessible to institutional investors or high net worth individuals. By investing in a private credit fund, individual investors can gain access to institutional-quality investments.

- Potential for downside protection: private credit funds generally have tight covenants in place that provide downside protection. These covenants reduce the risk of capital loss and help to ensure that appropriate returns are maintained relative to any changes in the credit risk of an underlying investment.

Private credit – an attractive opportunity amid uncertainty

Private credit finished 2023 with strong performance, which is expected to continue into 2024. Australian equities and residential property surprised most market participants by finishing the year near all-time highs. This was on the back of the global economy avoiding an expected recession, as well as positive market sentiment on lower inflation and expectations of early central bank rate cuts. However, given an expectation of slower global GDP growth, valuations for these asset classes appear stretched.

Despite strong performance over the past year, investor outlook for 2024 remains complicated by a number of concerns that are yet to be resolved:

- Although inflation has moderated, it remains above central banks’ targets of 2-3 percent, risking interest rates being maintained higher for longer to contain any upside risks

- Higher interest rates are negatively impacting consumers and businesses with the full impact of higher rates likely to be felt in 2024

- While a recession was avoided in 2023, the risk of economic contraction in 2024 still looms over key markets.

- Historically expensive valuations: of note equity risk premia at extremely low levels (US S&P 500 at 1.6%, lower only during the Great Depression and 2000 Nasdaq bubble.

- Poor and deteriorating affordability for Australian residential property (median dwelling value-to-income ratio of 8.1 times)[3], while commercial real estate is grappling with ~US$6.5 trillion in debt[4].

- Fraught geopolitics with ongoing conflicts in Ukraine and the Middle East, while elections in 60 countries including major markets such as the US and India during 2024 are likely to add further volatility.

With so much uncertainty, it remains a challenging environment for investor allocations. While cash rates at ~4% now arguably offers a reasonable return in nominal terms, it is less attractive in real terms considering inflation.

In this environment, private credit offers investors diversification into an attractive, defensive asset class with features and characteristics that mitigate several investor concerns:

- Attractive return profile – private credit provides regular income and attractive risk-adjusted returns.

- Hedge against inflation/interest rate risk – private credit continues to benefit from higher-for-longer interest rates with its floating-rate yield profile.

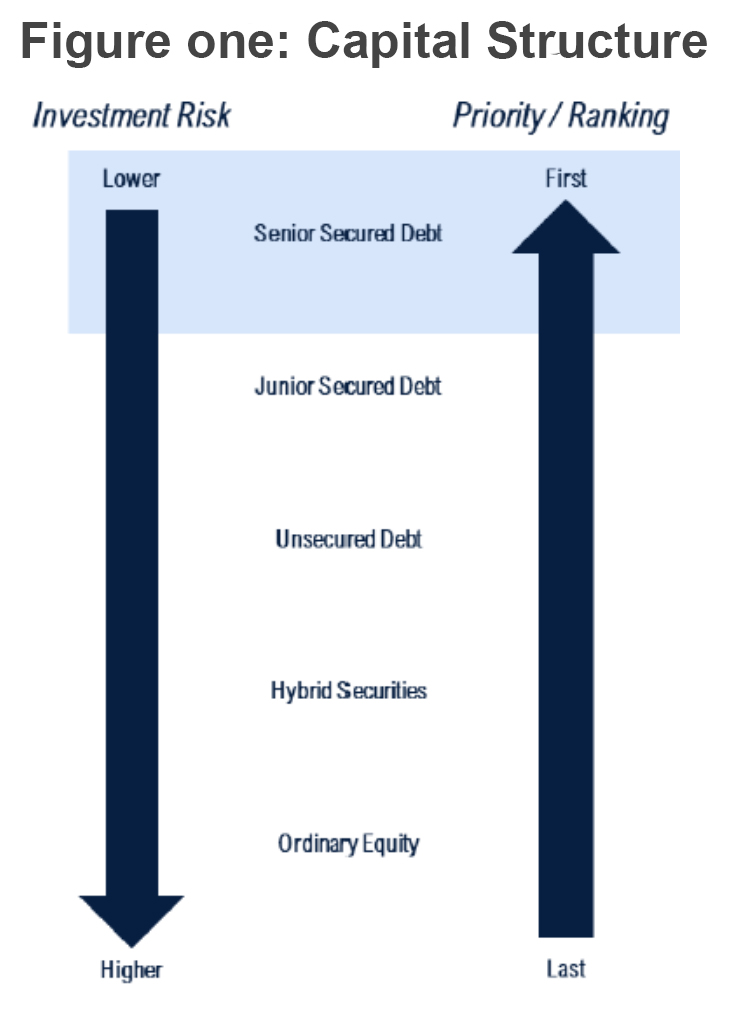

- Alternative to asset classes with stretched valuations – private credit investments are senior in the capital structure (Figure one) and that provides a meaningful equity buffer against deterioration in valuation and has low correlation with other asset classes

- Managing risks during economic downturns – private credit has strong downside protection features that helps to manage the risk of underperforming borrowers during economic downturns. These might include:

- Senior ranking security that provides first right to cashflows and assets of borrowers hence providing a buffer against deterioration in earnings.

- Regular testing of financial covenants that can provide an early warning signal against deterioration in credit quality of the borrower. This enables the private credit manager to take action if required to protect the investment.

Australian private credit market update

The Australian private credit market has continued to grow in profile and size. Private credit specialists Tanarra Credit Partners expects this momentum to continue over the coming year as the fundamental growth drivers remain in place:

- Basel III/IV is forcing banks to pull back their lending activities, with private credit lenders filling the void left by those banks

- Borrowers continue to seek greater flexibility in lending terms, as well as the certainty and speed of execution offered by private credit versus traditional bank lenders.

During 2023, there was continued bifurcation in the market between large-scale financings and the smaller mid-market financings. The large-scale deals have seen spreads tighten with terms increasingly in favour of borrowers as competition intensified amongst the large global credit providers that target this segment of the market. In contrast, the mid-market remains less competitive (mainly the domestic banks) with typically more attractive pricing and stronger lender protections available.

In terms of activity, 2023 was a year of two halves. Deployment was slower than usual in the first half of 2023, mainly driven by a lack of merger and acquisition volumes with the sharp increase in interest rates and uncertainty driving up the valuation gap between buyers and sellers.

In contrast, the second half of 2023 was a busy period with merger and acquisition activity and investment volumes picking up. Tanarra Capital Partners expects this momentum to continue into 2024 given a strong pipeline and anticipates higher refinancing demand during 2024 from private equity sponsors facing challenges in exiting portfolio companies due to slow IPO markets.

Private credit is clearly under the spotlight for investors as an asset class well-suited to navigate the complex economic environment ahead in 2024. As such, it is important to invest with an experienced fund manager to maximise the benefits offered by the asset class. A manager with a strong focus on deal selection will be key to success in 2024.

Important too is a manager that will maintain investment discipline through careful deal selection, rigorous due diligence and by ensuring deals are structured with a number of key downside protection features. This ensures the performance of the portfolio will be resilient even in the event of economic slowdown and that your clients are able to benefit from the opportunities presented by this asset class.

———