Quality small companies are well placed to outperform large companies going forward according to new research from ICE Investors, whose flagship ICE Fund is distributed by SG Hiscock & Company.

A research paper on small cap stocks from ICE Investors finds that the opportunity for quality small companies to outperform large cap stocks is largely intact, even after gaining in value in recent times. The chart below illustrates the recent rise of the S&P/ ASX Small Ordinaries Index following its underperformance since late 2021.[1]

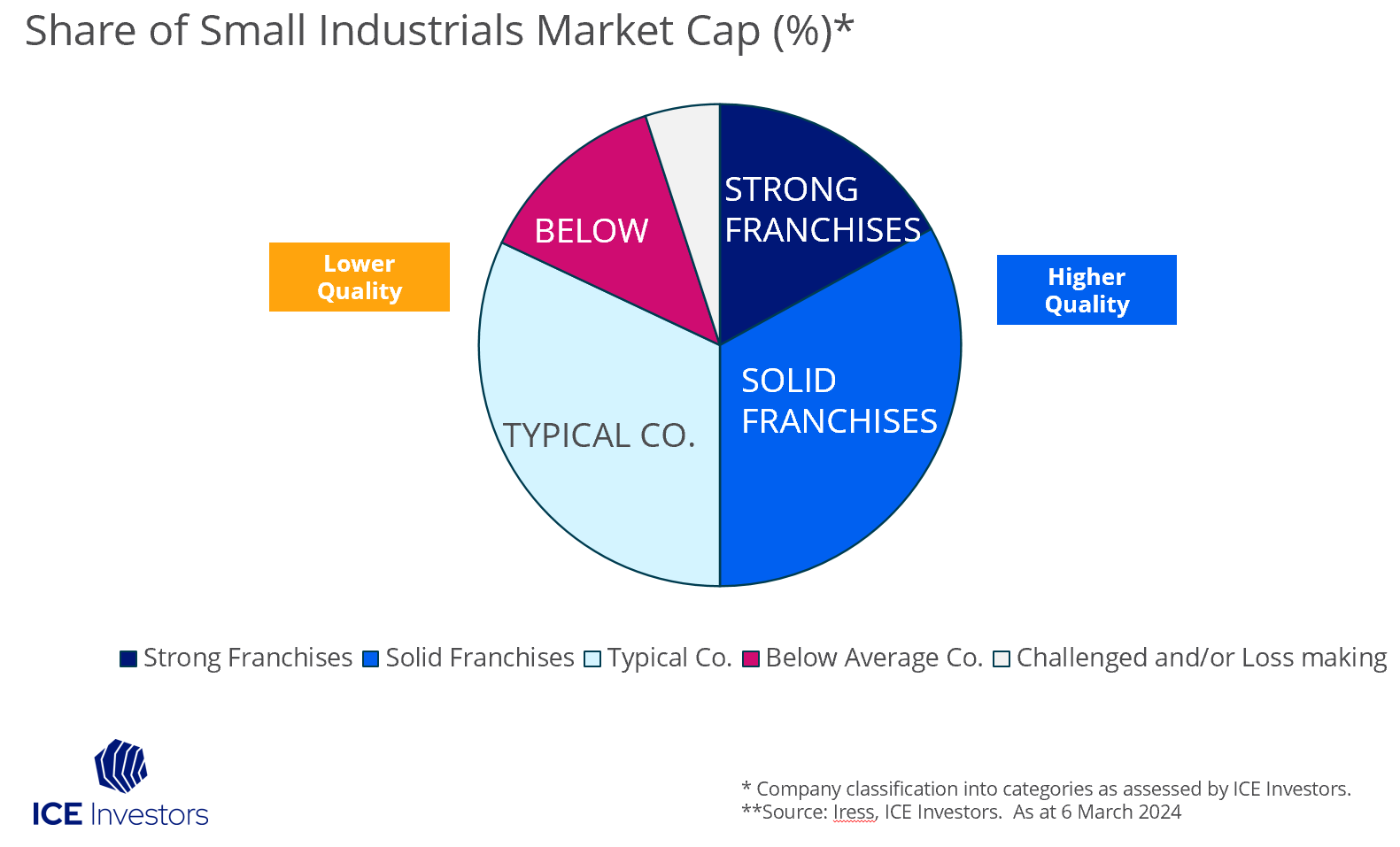

ICE Investors’ research adopted the ASX/ S&P Small Industrials Index as the control group. The companies were compared after they were split into five quality categories as shown in the chart below, using the ICE Investors Business Franchise Process: ‘strong franchises’, ‘solid franchises’, ‘typical company’, ‘below average company’ and ‘challenged and/ or loss-making’.

The analysis shows that about half of the Smaller Industrials index consists of higher quality companies. These higher quality companies have better earnings growth, slightly lower debt levels and similar profit margins as compared to the top 100 companies.

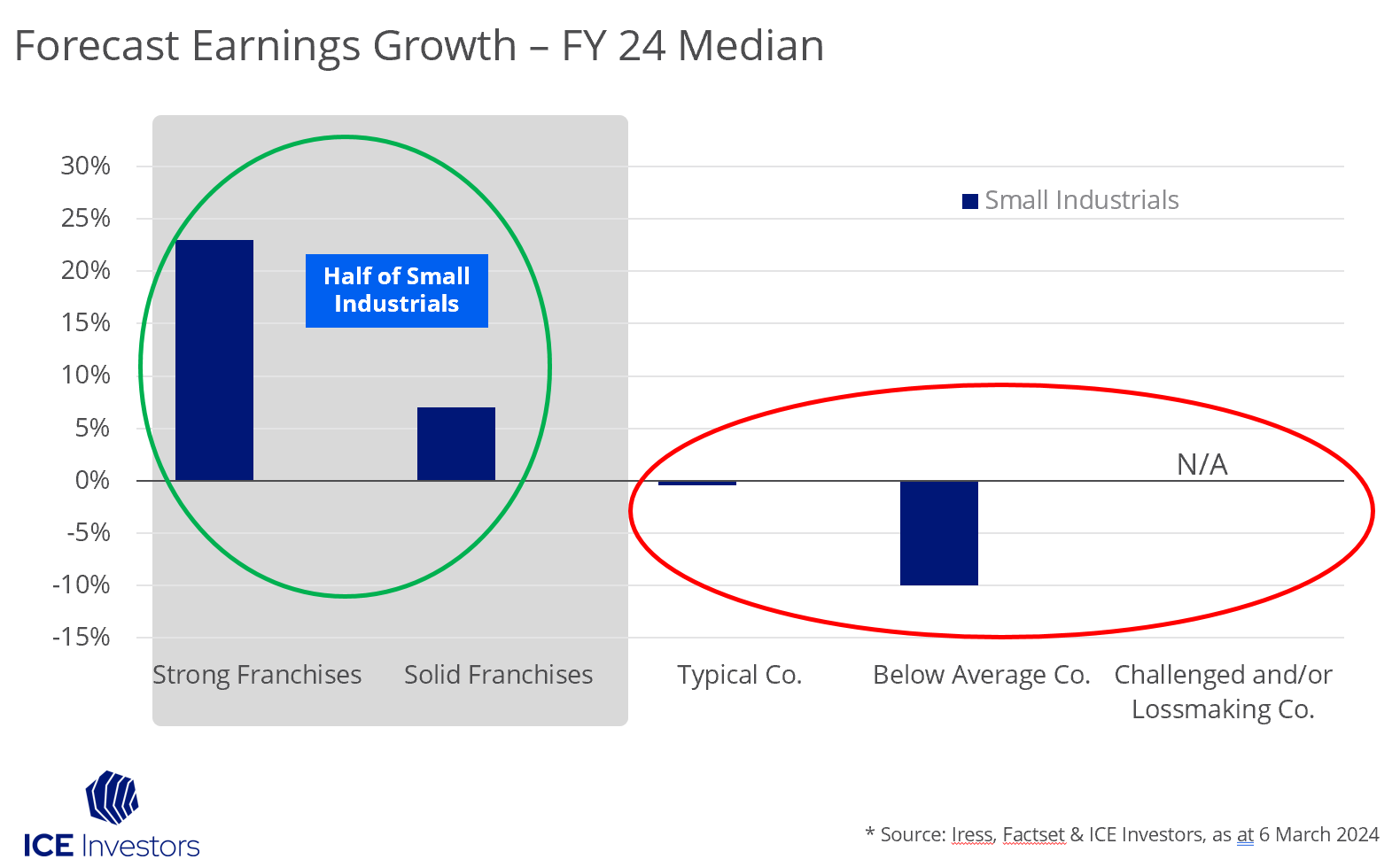

The consensus earnings growth forecast for the year to 30 June 2024 was calculated for each company and the median for each category, as shown in the chart below:

Companies that fall into the three lower quality categories have minimal, and inferior earnings growth which justifies these companies trading at a discount. In contrast, the selloff versus large cap stocks is highly likely to have created opportunities in the higher quality half.

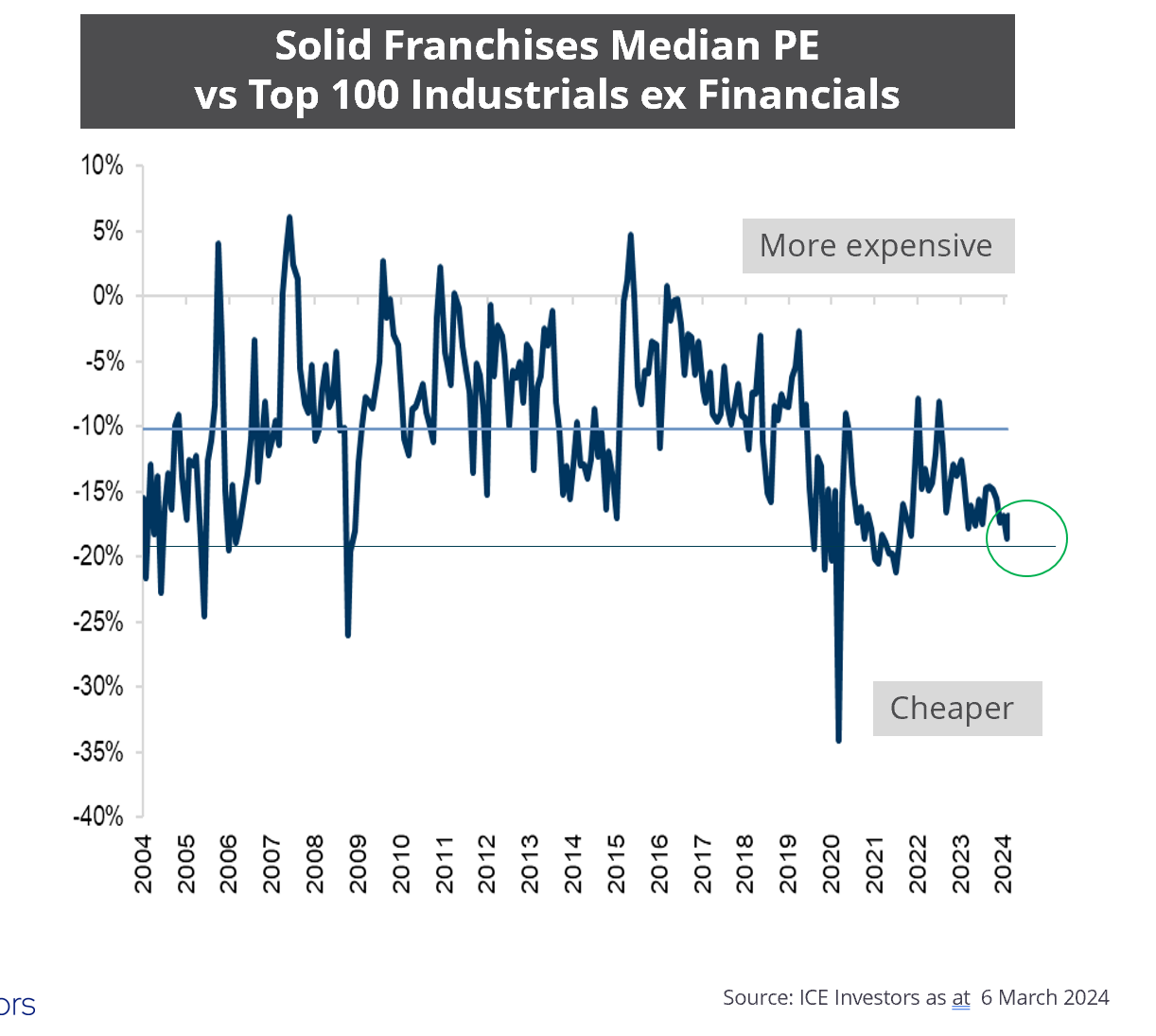

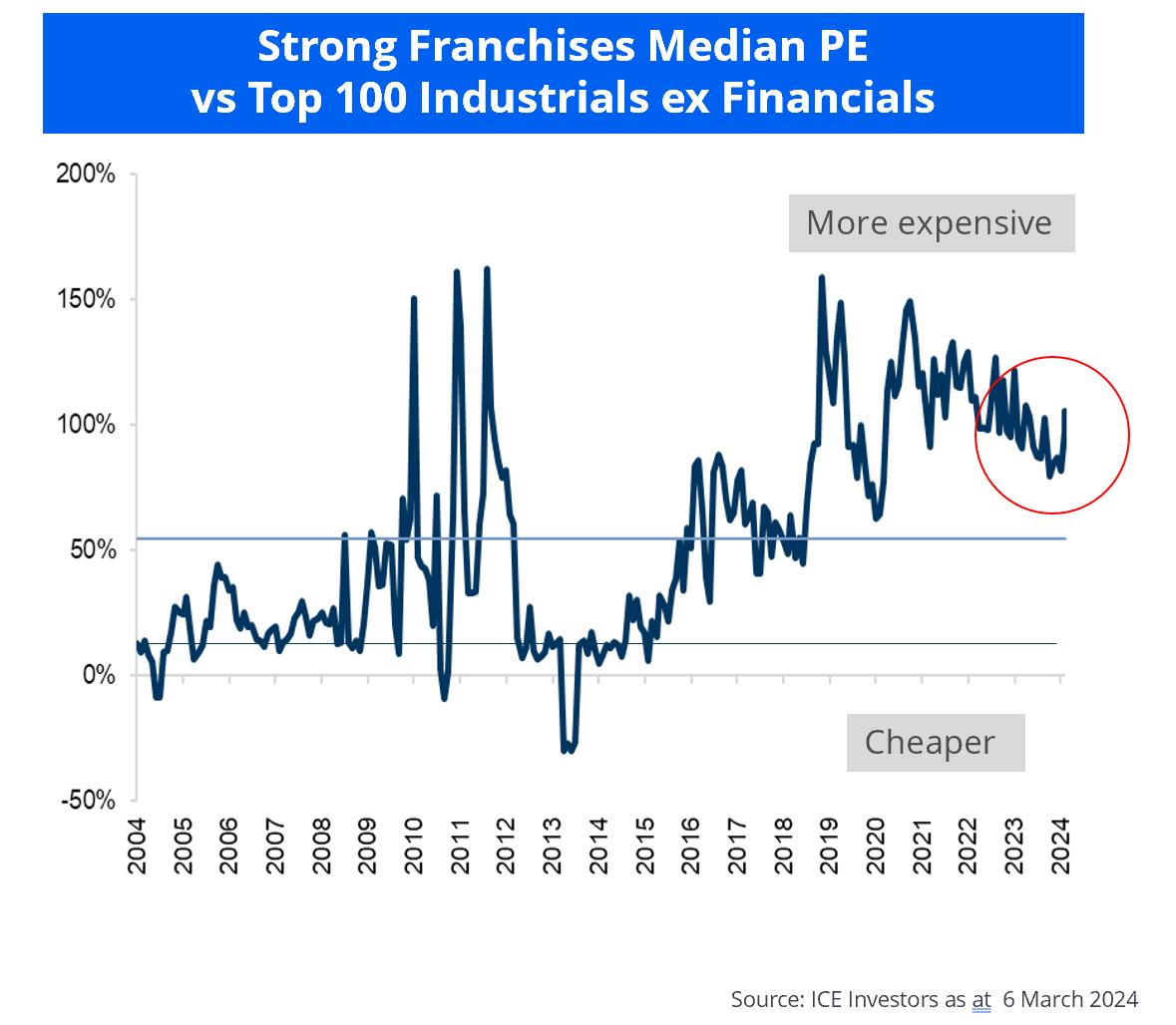

To explore where the best opportunities may lie in the prospective higher quality half of the Small Industrials, the median Price Earnings ratio for the Strong Franchises and Solid Franchise categories was calculated and compared to that of the Top 100.

The research showed that some of the best opportunities on offer in the small cap space are for ‘solid franchise’ businesses, whose valuations are attractive relative to large caps and their own history (as the chart below shows).

The strong franchise category trades at a premium in absolute terms and relative to its own history, indicating the more challenging investment environment has unsettled investors and they have responded by buying into this group. These are excellent companies, but the valuations are far more attractive in the solid franchise category.

Other categories should be avoided because of their weaker business models or prospects and earnings which are not growing as much as they are contracting.

Overall the research indicates the best opportunities are likely to reside in the solid franchise category – the only one which the constituent companies overall have a durable advantage, growing earnings and trade at a valuation discount relative to large caps and their own history.

———-