Ethics and aged care advice

The intricacies of aged care advice and its importance to a growing cohort of Australians.

It’s been well documented that Australians are living longer, increasing the need for aged care advice. This article, proudly sponsored by GSFM, explores some of the issues pertaining to aged care advice and how these issues may breach the adviser Code of Ethics.

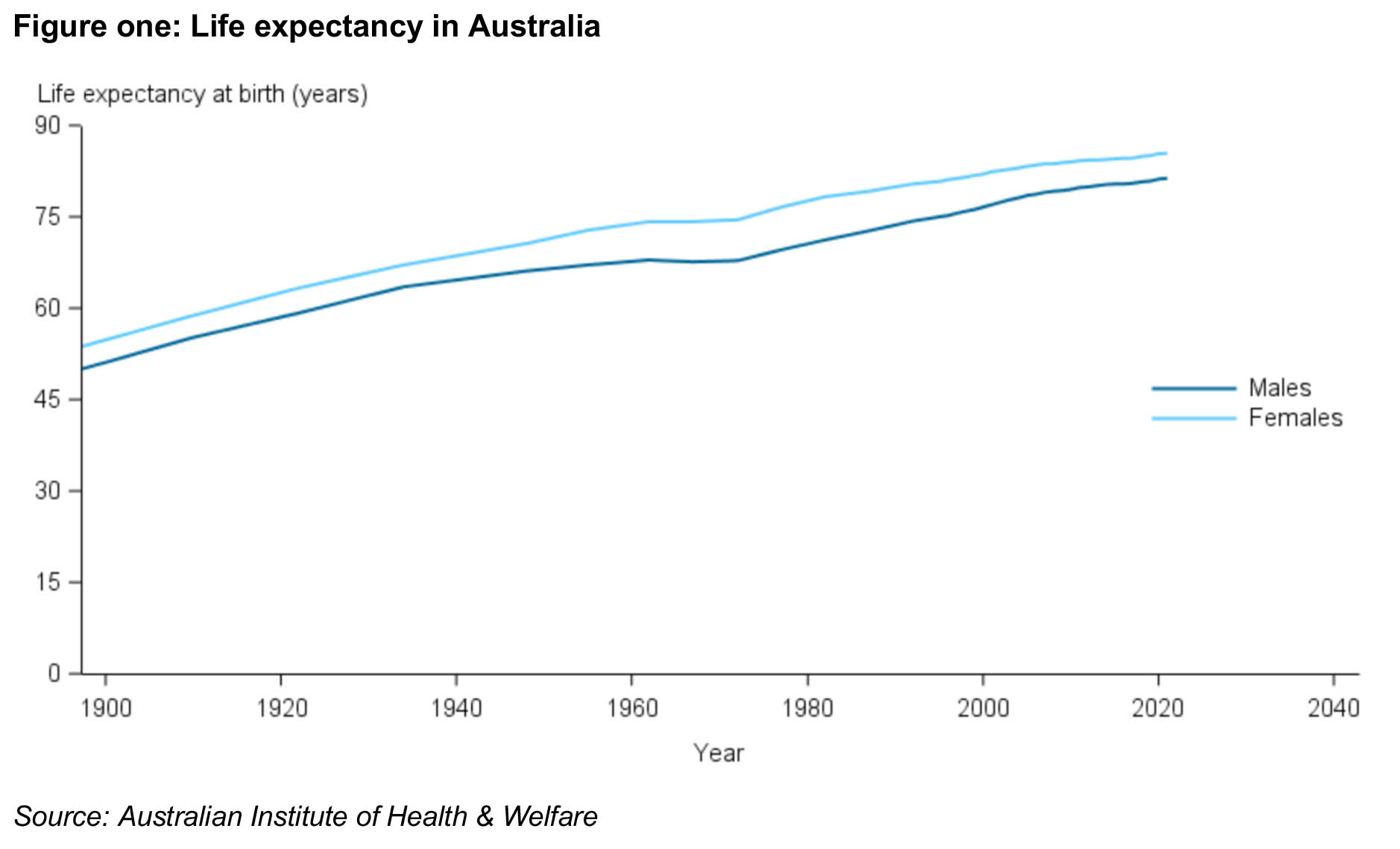

Since the implementation of the Superannuation Guarantee in 1992, Australians have gained a decade of longevity. Despite a small decrease in life expectancy during the Covid pandemic, Australians enjoy one of the highest life expectancies in the world. It is ranked fifth among 38 member countries of the Organisation for Economic Co-operation and Development (OECD)[1].

As illustrated in figure one, life expectancy in Australia has improved dramatically for women and men in the last century; compared with their counterparts in 1891–1900, boys and girls born in 2019–2021 can expect to live around 30 years longer.

Thanks to better nutrition, access to medical care and a general focus on health lifestyles, Australians can expect to live well into their 80s, highlighting the need for aged care advice. While most financial advice for those in their post-retirement years is focused on generating income and supporting lifestyle needs, less emphasis is given to planning and supporting aged care needs.

Aged care in Australia

Australians can access three levels of aged care services. These are:

Residential aged care: this provides accommodation and care at a facility on a permanent or respite basis. Permanent care is intended for those who can no longer live at home due to increased care needs.

In home care packages: these provide different levels of aged care services for older people in their own homes and aim to keep people well and independent in their own homes.

Home support: this program provides entry-level support at home for older Australians and their carers.

As most aged care advice focuses on access to and funding residential aged care, in-home care services are not discussed further in this article.

At 30 June 2023 there were 193,000 Australians using residential aged care, of which 58 percent were aged 85 and over and almost two in three were women[2].

Compared with in home care programs, people generally access residential aged care at older ages. This entry is often precipitated by an event: death of a partner, ill health or accident. As such, the lead time to source and fund entry to residential aged care can be short.

A major reason people access aged care advice is the complexity of fees associated with residential aged care. The following provides a brief overview of the fee structure, which – like many government programs – is subject to regular review and change. The same fee structure is applicable whether the aged care facility is run by local or state government or privately.

Aged care fees

The fees and costs associated with residential aged care depend on the chosen facility and a means assessment of the individual’s income and assets[3].

While not mandatory, a means assessment is important; if not completed, the individuals may be required to pay the maximum means tested care fee until the annual and lifetime caps are reached, as well as paying the agreed room price.

The income assessed to determine costs includes income support payments such as the Age Pension, deemed income from financial investments, income from rental property and superannuation.

The assets that are assessed include bank, building society, and credit union accounts, cash, shares, managed funds, investment property and personal effects (typically valued at $10,000).

Unlike the assets test for the Age Pension, part of the value of the family home may be counted in the assessment for residential aged care. If the family home is retained, a capped amount of $201,231.20 (at 20 March 2024) or the net market value of the home (if lower) is included in the assets assessment.

If a couple, each partner is considered to own half of the home; therefore, half of the net market value or the capped value is included as an asset – whichever is lower. The cap is applied to each half of the home.

Fees and charges

The different types of costs in residential aged care are[4]:

Basic daily fee: A flat fee paid by all residents to cover daily living expenses, set at 85 percent of the single person Age Pension. The daily fee is currently $61.96 per day (at 20 March 2024).

Means-tested care fee: A contribution that some people pay toward the cost of their care, determined by a means assessment and capped at $33,309.29 per year (at 20 March 2024); this annual cap is set by the government. A lifetime cap also applies to the means-tested care fee. Once this cap is reached, no more means-tested care fees will apply. The lifetime cap is currently $79,942.44. Annual and lifetime caps are indexed on 20 March and 20 September each year.

Accommodation fee: This covers the cost of accommodation and maintenance. The fee is set by the aged care facility and not the government, so each provider charges differently. The amount paid will depend on the individual’s means assessment.

The higher their income and assets, the higher the fee. This fee can be paid as a Refundable Accommodation Deposit (RAD) or a Daily Accommodation Payment (DAP).

The refundable accommodation deposit (RAD)

The RAD is one aspect of aged care cost about which families seek advice. Large sums of money are often involved, and in-demand aged care facilities in major cities can command RADs of a million dollars or more.

The RAD is a form of loan made to the facility by the individual, one that’s repaid when your client leaves. Individuals with income over $82,425.72 or assets valued over $201,231.20 are required to make a full accommodation payment.

The family home is assessable unless an immediate family member or carer had been living with the individual and remains in place. If the home is empty, total assets will likely exceed $201,231.20 and a full accommodation payment will be required. An important financial decision about funding the deposit is often required.

Daily accommodation payment (DAP)

If an individual does not have access to sufficient funds to pay a RAD, the alternative is the DAP. This is a daily fee calculated against the overall accommodation fee required. The cost is calculated daily and charged monthly. It includes an interest component, calculated at a rate set by the government.

Additional service fees: Fees for services beyond the minimum care and service requirements; such fees may cover pay TV or streaming services, or access to the internet.

Extra service fees: Some residential aged care facilities homes offer an extensive range of extras that incur additional costs; hairdressing or beauty services, regular outings or a glass of wine with dinner.

Aged care advice

Access to quality aged care financial advice is critical when it comes to making well-informed aged care decisions. Firstly, it’s important that clients understand the complexities of aged care fees and costs and, therefore, how to best structure finances to afford the care needed.

However, there’s a problem with aged care advice.

It’s an issue for the broader advice industry as well as a potential minefield for the client/s. The issue is this: a lot of “aged care advice” is provided by individuals who are unlicenced, not authorised, not on ASIC’s Financial Adviser Register. It may be provided by a range of people – professionals such as lawyers or accountants, individuals working in the aged care sector or with ancillary services and, in some cases, former (i.e. deregistered) financial advisers.

It can often be difficult for families to source help and to understand the differences in the advice on offer. Are they receiving information only, general advice or comprehensive personal advice?

Information versus advice

In many cases, the ‘client’ is the family of the person entering aged care and the move is often event driven. As the event is generally negative and emotive – an illness, a fall, the death of a partner – emotions can be running high and there can be a high level of stress on the part of those seeking advice. As such, those seeking advice often don’t have the luxury of time or the emotional clear headedness to check the credentials of someone offering aged care advice, or to be sure the guidance they provide will be in their best interests.

A range of information can be provided that does not cross the line into advice. This includes explaining aged care fees (including calculations for an individual’s fee scenario), explaining Centrelink entitlements and sourcing appropriate accommodation. If the professional in question is simply providing information without affecting any decision…that’s information, not advice.

However, once the aged care adviser influences an action, such as discussing options as to how the client can pay for the aged care fees, discussing options and classes of products, this is likely to cross the line into personal advice.

This is the case even where the adviser doesn’t make a recommendation; simply influencing the client to make a decision about a specific product or product class falls into realm of personal product advice. The Corporations Act 2001 outlines two steps to determine whether a professional is providing personal product advice:

- The adviser knows personal information about the client

- There is a suggestion or inference to make a change in respect to assets or products, or a class of products, and influencing the client to make a decision about those assets.

Finding and funding accommodation is usually only the first step in holistic personal financial advice; there can also be financial, tax, social security and estate planning considerations. These should be the purview of a registered financial adviser providing aged care advice.

For many consumers, the difference between information and advice is not clear. Decisions can be made in haste at a time when those making them are emotional or vulnerable. Given the expenses associated with aged care, decisions about the advice may be driven by cost without an understanding of the implications.

Unregistered advisers may be cheaper because they don’t have applicable professional indemnity insurance, aren’t members of AFCA (thereby denying their clients an opportunity for redress), aren’t required to have memberships of professional associations, or avoid ongoing educational requirements. Importantly, if an unregistered adviser, the individual offering the advice is not bound by the Code of Ethics.

Ethics and aged care advice

A registered financial adviser offering aged care advice is obliged to adhere to the Financial Planners and Advisers Code of Ethics (figure three).

The Code of Ethics was introduced to provide a layer of consumer protection and engender trust in the financial advice profession. The Code of Ethics requires financial advisers meet their obligations in the law in respect of the advice provided to each client, including:

- The best interests’ duty

- The appropriateness of advice

- Prioritisation of client’s interests

- Additional requirements for product replacement recommendations

- Australian Taxation laws.

Further, licenced financial advisers are required to

- Know your client

- Work out their situation, objectives, needs and their financial literacy level

- Have a reasonable basis for advice

- Know your product and the consequences of your advice, and ensure the advice is appropriate for the client

- Comply with statement of advice (SOA) requirements.

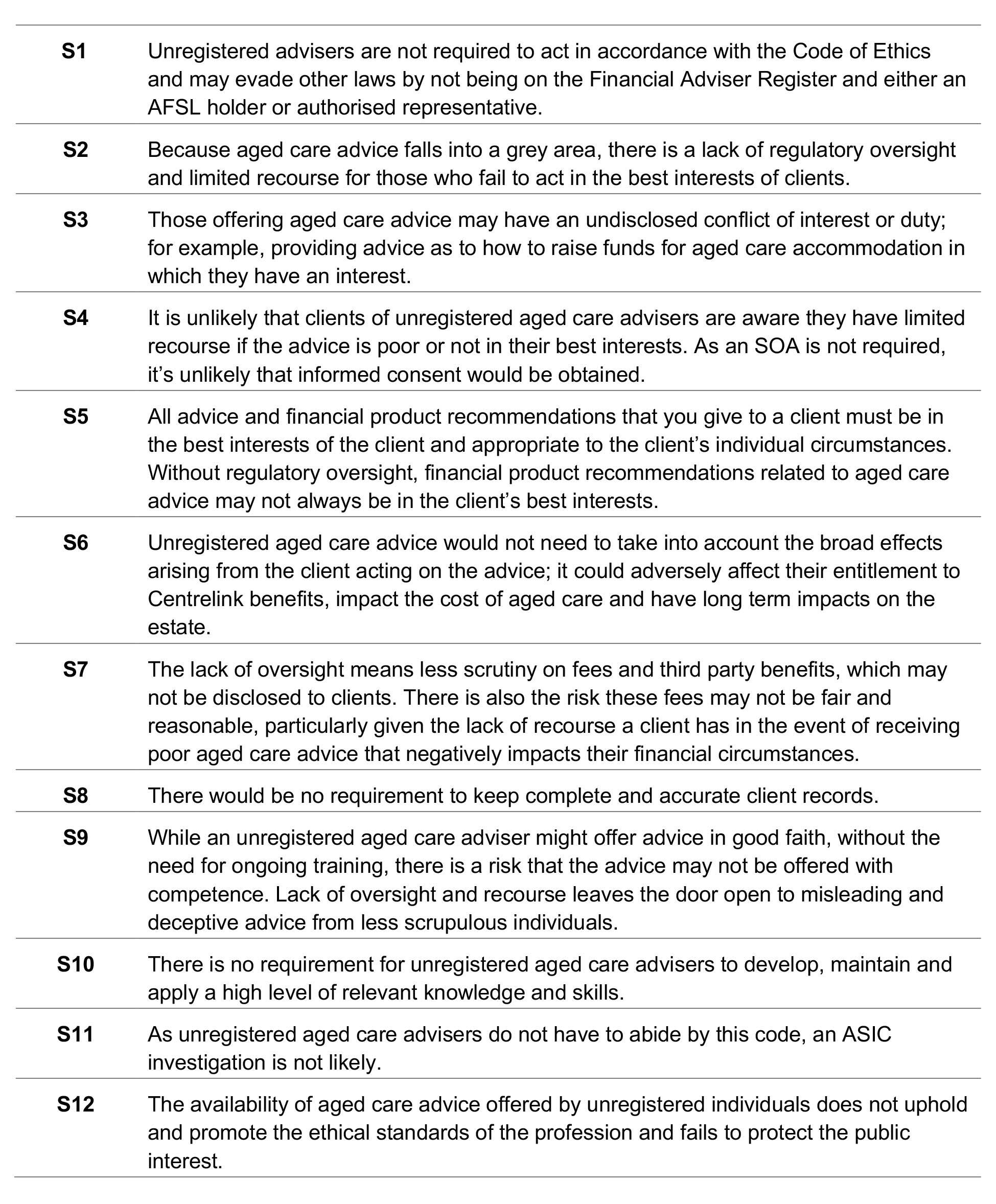

Those individuals who provide aged care advice (not just information) and are not registered advisers operate outside of this code and the requirements outlined above. This has implications for consumers and the potential for grievous outcomes for society’s vulnerable elders.

At best, it can have mediocre outcomes for clients; at its worst, it can lead to elder abuse, in particular financial elder abuse. This is defined by the World Health Organisation as “The illegal or improper exploitation or use of funds or other resources of the older person” and is the subject of an earlier article in this series, Ethical practice in the face of financial elder abuse. [link to: https://www.adviservoice.com.au/2024/01/cpd-ethical-practice-in-the-face-of-financial-elder-abuse/]

Registered financial advisers who provide aged care advice are licensed and regulated under the Corporations Act. Among other protections, their clients can take complaints to the Australian Financial Complaints Authority (AFCA).

Unregistered aged care advice is both a consumer protection and ethical issue for the industry. Although some clients receive personal product advice, they are not eligible for the protections available to clients of registered financial advisers, including access to AFCA.

Although not beholden to the Code of Ethics, unregistered advisers providing aged care advice fail to deliver important outcomes for clients that can be unpacked in reference to the Code and its standards.

The lack of registration requirements, and consequential exemption from the Code of Ethics for aged care advisers raises significant concerns regarding consumer protection and the quality of advice provided in the aged care sector. Without mandatory registration, there is no formal mechanism to ensure that aged care advisers possess the necessary qualifications, skills and expertise to effectively assist consumers in making informed decisions about their – or their loved ones – aged care needs. This absence of regulatory oversight creates a potential risk for consumers who may inadvertently seek advice from individuals lacking the appropriate training and knowledge, leading to suboptimal outcomes such as inadequate financial planning or unsuitable aged care arrangements.

Not having to abide by the Code of Ethics further compounds the risk of suboptimal outcomes for consumers. The Code of Ethics sets out clear standards of conduct and ethical principles that financial advisers must adhere to, including obligations to act in the best interests of clients, provide transparent and unbiased advice, and manage conflicts of interest appropriately. By not being bound by these ethical standards, aged care advisers may not be held to the same level of accountability and transparency in their dealings with clients. This lack of regulatory oversight could potentially create an environment where advisers prioritise their own interests or those of affiliated institutions over the welfare of their clients, leading to biased or misleading advice that does not fully align with the best interests of consumers.

Finally, the complex and evolving nature of the aged care system, including its interplay with financial planning and investment strategies, necessitates a high level of expertise and specialisation from advisers. Without robust regulatory requirements and ethical standards in place, there is a heightened risk of consumers receiving outdated or inaccurate advice that fails to adequately address their unique financial and care needs. The absence of registration and ethical oversight for aged care advisers can undermine consumer confidence and may result in suboptimal outcomes that could have long-lasting repercussions for individuals and their families.

Case studies

The following case studies highlight the benefits of obtaining aged care advice from registered financial advisers through the lens of the standards comprising the Code of Ethics.

Case study one: A turnaround story

Luke and Barbara Smith, a retired couple in their late 70s, faced the daunting task of arranging residential aged care for Luke due to a deteriorating health condition. Seeking guidance, they turned to an aged care adviser recommended by their neighbour. Unbeknownst to them, the adviser operated independently and was not a registered financial adviser.

The adviser, Bob, provided the Smiths with a detailed costing of the aged care options for Luke and suggested they sell the couple’s residence to pay for the Refundable Accommodation Deposit and then use the remainder of the sale proceeds plus their savings to buy small unit for Barbara. While advice about buying or selling property, including the family home, is exempt from AFS provisions, the advice pertaining to the use of the couple’s savings is not. However, Barbara did not wish to move; the couple had already downsized and where would she go? She was close to her children and comfortable in her community – and she loved her small garden.

Encouraged by their children, Luke and Barbara sought a second opinion, this time from a registered financial adviser from ACME Aged Care Advice. Their new adviser, Sue, explained that, as clients of a registered financial adviser, they had a range of protections – and she had training and education related to the aged care sector.

Sue helped the family understand the intricacies of the aged care fees they would incur and developed a strategy to ensure they would retain their residence so that Barbara had somewhere to live once Luke moved into aged care. Sue was able to recommend several strategies to rearrange the couple’s investments. She presented to two funding options to determine which worked best for them. With tailored advice and support, the Smiths were able to fund Luke’s aged care needs and implement a financial plan that prioritised their long-term wellbeing.

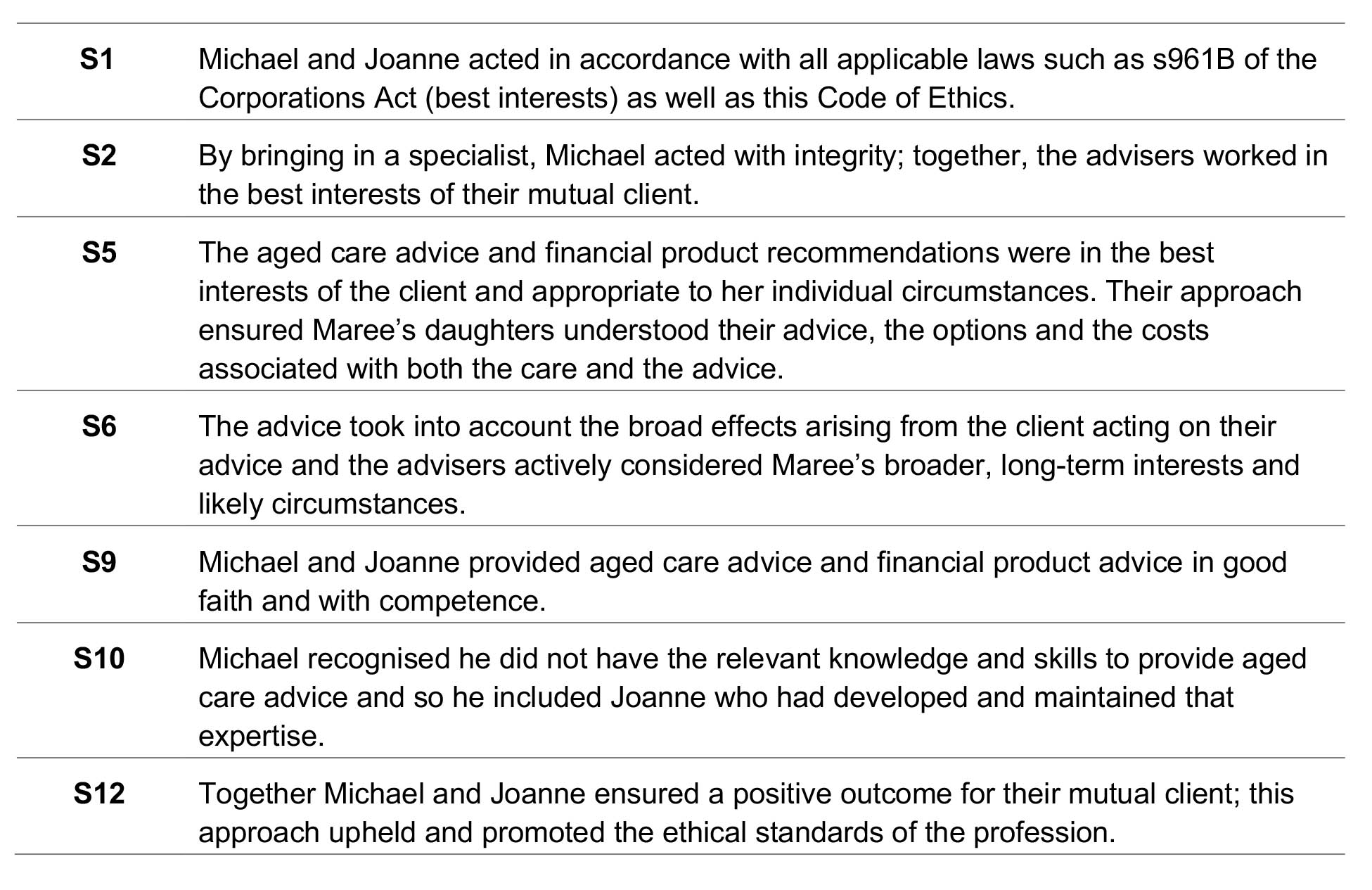

As a registered financial adviser, Sue is bound by the Code of Ethics. Her conduct in this case study saw her meet her requirements under the Code, specifically in relation to the following standards:

Case study two: Meeting aged care needs

Maree, a widow of 82, had a nasty fall and broke her pelvis; as she proceeded through her rehabilitation in specialist facility, Maree’s medical team recommended to her two daughters that she move from her family home into residential aged care.

Her daughters were joint Powers of Attorney – one held medical POA, the other financial. Together they visited her financial adviser to discuss the options fund her move into aged care. Maree’s adviser Michael was not a specialist aged care adviser but recommended they include his colleague Joanne in their discussions. As well as being an authorised representative of the same licensee, Joanne had undertaken specialist courses to ensure she was up to date with all aspects of aged care.

Joanne was able to provide detailed cost options to the sisters and, together with Michael, they developed some alternative strategies to pay for the care. Maree was adamant that her home not be sold and her daughters knew that if it was necessary to fund her care, it would need some renovations before it could be sold for a reasonable price.

Joanne suggested they pay the Daily Accommodation Payment (DAP) rather than a RAD, and Michael was able to realign her investments to fund a monthly payment to the aged care facility that paid the DAP. Together the advisers ensured Maree’s daughters understood the advice, the costs and how those would be paid.

Working together, Michael and Joanne were able to provide Maree and her daughters with positive outcomes to ensure Maree’s care needs were met and her financial security assured. Their conduct in this case study saw Maree’s advisers meet her requirements under the Code, specifically in relation to the following standards:

The complexities around aged care and its funding, along with Australia’s ageing population, means this is an area where consumers will increasingly seek assistance, whether for themselves or ageing parents or relatives. In many cases, the need for residential aged care requires fast action and decision making at a time when family members are stressed, reinforcing the need for reliable advice from a trusted adviser.

The ‘grey area’ in which aged care advice currently sits has resulted in people offering aged care advice who are unregistered, unregulated and exempt from the Code of Ethics. This poses significant risks to consumers seeking guidance to navigate the intricacies of aged care decision making, especially when it comes to funding residential aged care.

Without regulatory oversight, there is no guarantee of the qualifications or competency of aged care advisers, potentially leaving consumers vulnerable to receiving advice from individuals lacking the necessary expertise. Furthermore, not being bound by the Code of Ethics leaves room for conflicts of interest and biased recommendations, undermining consumer trust and jeopardising their financial security.

As ageing populations increasingly grapple with the challenges of planning for their long-term care needs, it is imperative that policymakers and industry stakeholders prioritise consumer protection and advocate for the requirement that aged care advice be delivered by registered financial advisers. By ensuring transparency, accountability and adherence to best practices, consumers be empowered to make informed decisions that safeguard their wellbeing and financial future.

——–