Contemporary challenges in ethics and financial advice

What are the current challenges in ethics and professionalism ensuring advisers act in clients’ best interests at all times?

Businesses across all industries are beset with challenges. This article, proudly sponsored by GSFM, investigates a range of contemporary challenges that financial advice businesses and how those challenges might impact ethical practice.

Ethics in financial advice is important. It underpins some of the basic tenets of advice practice, such as acting in clients’ best interest always, avoiding conflicts of interest and acting with transparency and integrity in all dealings with clients.

Financial advisers are entrusted to guide clients through intricate financial planning and decision making, and their role necessitates a high level of ethical conduct and professionalism. For this reason, the Financial Planners and Advisers Code of Ethics 2019 (Code of Ethics) was introduced to provide a set of principles and core values in the areas of ethical behaviour, client care, quality process and professional commitment.

Advisers (and licensees) have to ensure ongoing compliance with the Code of Ethics amid a continually evolving business landscape…regulatory change, technological developments and educational requirements (to name but a few) can keep businesses on their toes. Irrespective of change, keeping up to date and delivering advice services that uphold the ethical standards that make up the Code of Ethics is essential.

Ethics and advice

The Code of Ethics imposes ethical duties on financial advisers and is designed to encourage higher standards of behaviour and professionalism in the financial services industry, aiming to build consumer trust and deliver better outcomes for all. These ethical duties exceed the requirements outlined in law.

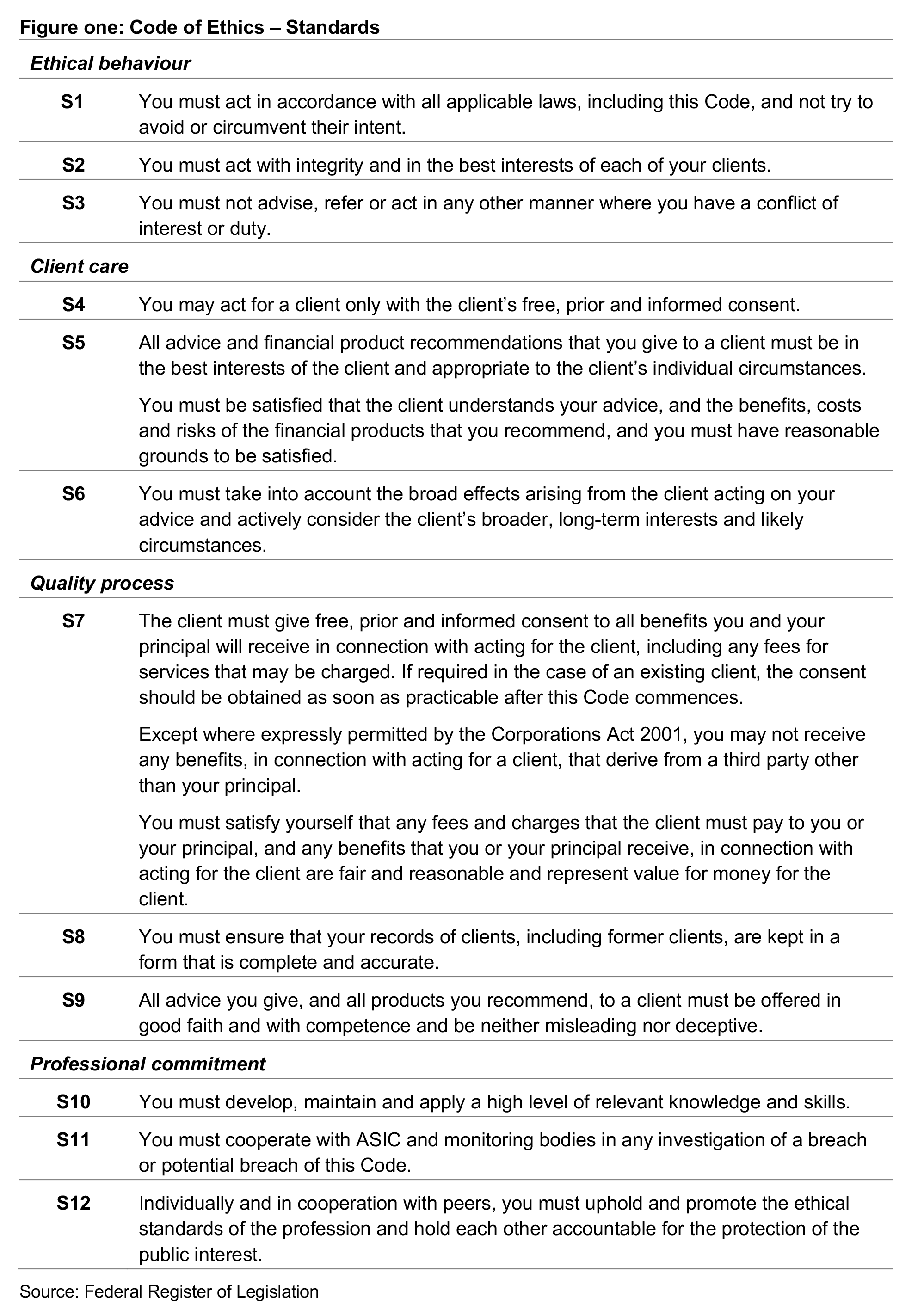

The Code of Ethics is comprised of twelve standards (figure one); these are grouped under four ethical competencies:

- Ethical Behaviour (standards one to three)

- Client Care (standards four to six)

- Quality Process (standards seven to nine)

- Professional Commitment (standards ten to twelve)

It is expected that advisers will exercise professional judgement against the ethical principles in each standard, depending on the particular circumstance. The Code of Ethics mandates that financial advisers must consistently act in a manner that aligns with its twelve ethical standards, with compliance monitored by ASIC-approved schemes.

Licensees play a crucial role under the Act; they must monitor and enforce adherence to the Code among all advisers operating under their authority. Licensees are expected to structure their business operations to facilitate ethical behaviour and ensure that advisers meet each of the twelve standards of the Code of Ethics.

While ethics may be defined in different ways, at its broadest, it can be distilled as a system of moral principles concerned with what is good for individuals and society. The term is derived from the Greek word ethos, which can mean custom, habit, character or disposition.

In the world of financial advice, it means treating your clients fairly, always acting in their best interests and acting with honesty, integrity and competence. In short, embodying the values upon which the Code of Ethics is based. These values are: trustworthiness, competence, honesty, fairness and diligence.

Contemporary Challenges

Regulatory compliance

Financial advisers operate within a complex regulatory environment designed to protect consumers and uphold the integrity of the financial system. Regulations establish standards for transparency, fiduciary duty and ethical conduct, aiming to mitigate conflicts of interest and protect investors.

The importance of regulatory compliance is highlighted by it being the subject of standard one in the Code of Ethics.

This standard requires that:

- advisers will take steps to understand their legal obligations, under both the law and the Code of Ethics

- advisers must ensure the advice they provide is not intended to circumvent the intent of financial services laws or the Code of Ethics

- advisers must not establish business structures to circumvent their ethical obligations

- advisers must always act in the best interests of their clients.

Importantly, standard one encourages advisers to consider both the legalities and ethics of each course of action they take. Because the Code is enshrined in legislation, a breach of the code will result in a breach of the law.

However, regulatory compliance is often a challenging and ongoing process. The financial industry is dynamic, and regulations continually evolve to address new market realities and emerging risks. Advisers must stay abreast of these changes, ensuring that their practices are always in alignment with current laws and standards, including the Code of Ethics. Non-compliance not only exposes advisers to regulatory scrutiny and in some cases, legal repercussions, but also erodes client trust and tarnishes the adviser’s reputation and that of the profession.

Best interests duty

Best interests is the subject of Section 961B of the Corporations Act 2001. The best interests duty and related obligations are designed to ensure that retail clients receive advice that meets their objectives, financial situation and needs, and that advisers act in the best interests of their clients when providing advice.

Acting a client’s best interests also underpins two standards in the Code of Ethics: standards two and five.

This standard requires that:

- advisers consider each client – and their needs – individually

- advisers are honest, open and frank in all dealings with clients

- advisers prioritise clients’ interests over their own or their licensees’ interests

- advisers honour commitments made to their clients.

The main premise of standard two is putting each and every client’s interests first. This requires that advisers ensure that the advice, products and services recommended are appropriate to meet the client’s objectives, financial situation and needs. This needs to include consideration of the client’s longer-term interests and expected future circumstances.

The standard requires that all advice and financial product recommendations given to a client must be in the best interests of the client and appropriate to their individual circumstances. Further, advisers must be satisfied – and have reasonable grounds to be satisfied – that the client understands the advice and the benefits, the costs and risks of the financial products recommended.

This standard requires that:

- advisers ensure that financial advice and product recommendations are appropriate to each client’s individual circumstances

- advisers are aware of, and knowledgeable about, available financial products that would meet each client’s needs

- advisers focus on each client’s individual circumstances and do not apply a ‘one size fits all’ approach to advice and recommendations

- advisers provide the advice and information in a way that ensures client understanding; this may mean a different approach for different clients, depending on their sophistication and understanding

- advisers must be satisfied that each client understands the advice received and the products recommended – this includes benefits, risks and costs associated with each product or service.

In the current market, advisers may face a number of challenges when acting in a client’s best interests. Global economic uncertainties and market volatility can make it challenging to provide advice that consistently aligns with clients’ best interests, especially in predicting and managing risks.

At the same time, clients may have unrealistic expectations or exhibit behaviours influenced by market trends, media and word of mouth. Advisers must manage these expectations while providing advice that aligns with clients’ best interests. Balancing ethical considerations with client satisfaction (and sometimes, their best interests) can be challenging.

Conflicts of interest

One of the most pressing ethical challenges in financial advice is managing conflicts of interest. Standard three – one of the most contentious standards in the Code of Ethics – focuses on an actual conflict that might arise between the duty an adviser owes to a client and any personal interest they have or duties they owe another individual or organisation, such as their practice or licensee.

Avoiding conflicts by putting client interests first demonstrates the five values that underpin the Code of Ethics and also links to that pivotal requirement of always acting in the clients’ best interests.

This standard requires that:

- advisers make an assessment as to whether their personal interests are compatible with the best interests of their client

- advisers must ensure the advice they provide is not in conflict with personal interest

- advisers must remain aware of changing circumstances and whether than can result in conflicts of interest with some or all clients.

Despite regulations, conflicts of interest can arise, and it is incumbent on advisers to manage them to always put the client first.

Transparency

Transparency is a cornerstone of ethical advice and a value that spans several of the standards in the Code of Ethics.

Clients must be fully informed about the fees they are being charged (standard seven) and the risks associated with various financial products (standard five). The complexity of financial products can make it difficult for clients to fully grasp the advice they receive. Financial advisers, therefore, have a duty to communicate clearly and effectively, ensuring that their clients have a thorough understanding of the financial strategies being recommended (standard five).

Advisers should disclose all relevant information in a straightforward manner; it’s important to avoid jargon that could confuse or mislead clients. This includes being upfront about all fees, the potential risks and benefits of proposed investments, and any affiliations or relationships with product providers that could influence recommendations. By fostering a culture of transparency, advisers not only build trust but also empower clients to make informed decisions about their financial futures.

The continual changes in financial markets, regulations, compliance requirements and the increasing complexity of financial products can significantly impact a financial adviser’s ability to provide transparency to clients. This environment creates challenges such as information overload, a heavy compliance burden and difficulties in explaining complex products clearly. Advisers must continuously update their knowledge, which competes with the time needed for client communication.

Limited resources, especially for smaller practices, can affect the quality of transparency, and integrating new technologies requires investment and training. Increased documentation demands can detract from client interactions, and rapid changes heighten the risk of miscommunication. Additionally, maintaining client trust becomes more challenging, as advisers may focus more on short-term compliance rather than long-term client education and understanding. These factors can complicate the delivery of clear, transparent advice to clients.

Continuing education

A commitment to continuing education is a requirement of financial advice in Australia. Financial advisers must comply with CPD requirements by completing 40 hours of CPD each year, with minimum hours across the following mandatory categories:

- Technical competence (five hours)

- Client care and practice (five hours)

- Regulatory compliance and consumer protection (five hours)

- Professionalism and ethics (nine hours)

Continuing education also supports advisers to meet standard ten, which requires that financial advisers have and maintain an appropriate level of relevant knowledge and skill to provide competent financial advice that is in the best interests of their clients.

Continuing education involves more than just fulfilling regulatory requirements. It means actively seeking out opportunities to expand expertise, such as attending industry conferences, participating in training programs and pursuing advanced certification.

By staying informed and educated, financial advisers can offer relevant, up-to-date advice and adapt to the changing needs of their clients, putting themselves in the best position to uphold their ethical obligations.

Impact of technology

Technology has revolutionised the financial advice industry, bringing both opportunity and challenge.

It has changed administration and record keeping, moving from paper based files to sophisticated software and digital platforms. Record keeping is the subject of standard eight and requires financial advisers to maintain complete and accurate records of advice and services provided to clients. It also requires that:

- advisers meet legislative requirements relating to the secure storage of client records

- client records must be both complete and accurate for both current and former clients

- records should include file notes of discussions

- client records must be easily accessible.

One of the contemporary challenges that comes with technology is cybersecurity. As advisers increasingly rely on digital tools and platforms to store and manage client information, the risk of cyberattacks and data breaches grows. Unauthorised access to client data can lead to data corruption, loss, or theft, jeopardising the accuracy and integrity of these records.

Advisers must implement robust cybersecurity measures, such as encryption, multi-factor authentication, and regular security audits, to protect client information. However, these measures can be resource-intensive and may require continuous updates to address emerging threats. Additionally, the need for secure backup systems and disaster recovery plans adds another layer of complexity. Ensuring the confidentiality, accuracy, and availability of client records amidst these cybersecurity challenges is essential for maintaining trust and compliance with regulatory standards.

Case studies

The following case studies are based on real events; however, the names of people and organisations have been changed, and some details altered. The case studies have been drawn from the Australian Financial Complaints Authority (AFCA) or ASIC. For each, potential breaches of the Code of Ethics are identified.

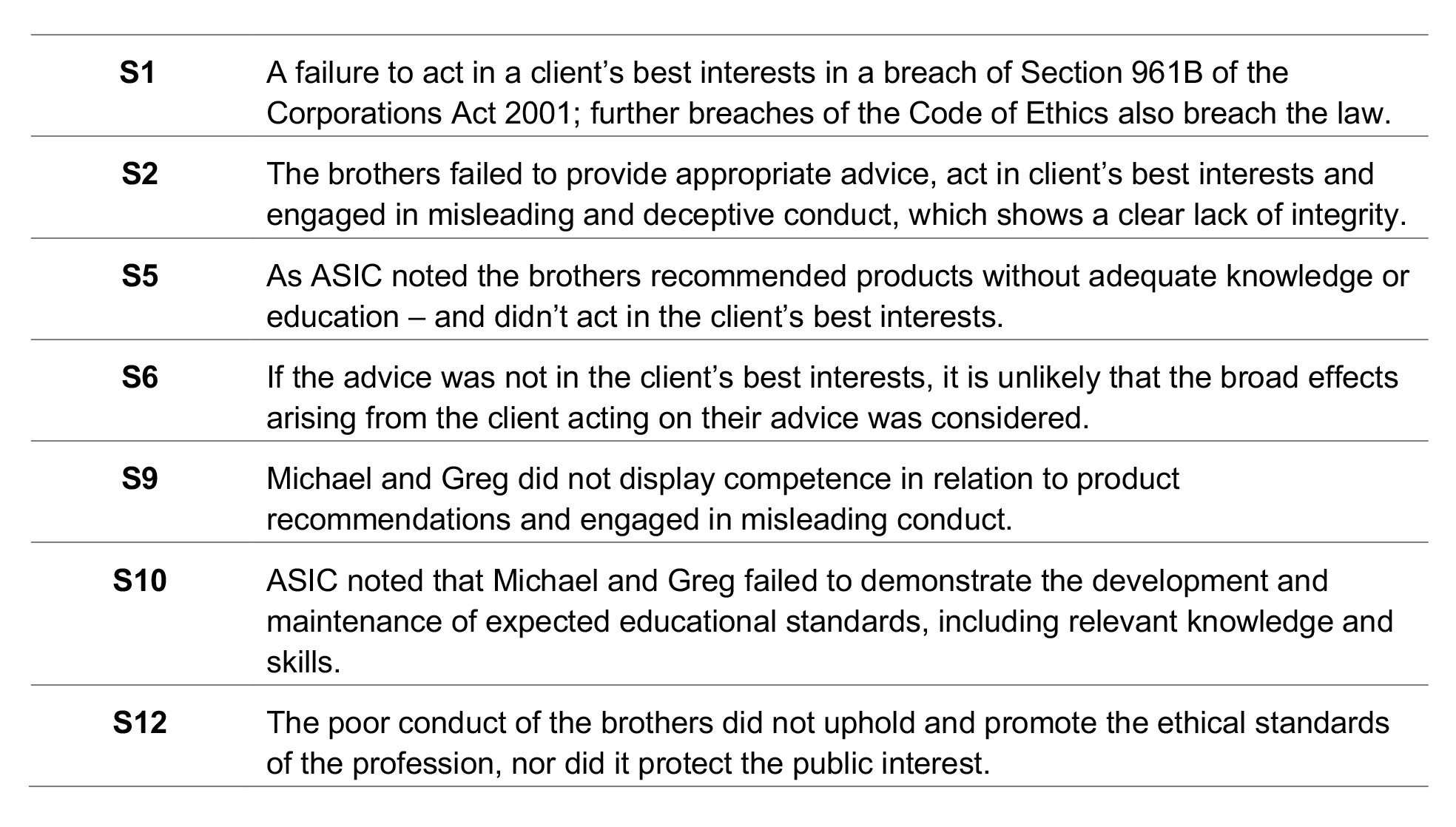

Case study one – failure to maintain knowledge and act in client best interests

ACME Advice was operated by brothers and business partners Greg and Michael on Queensland’s Gold Coast between 2014 and 2021. The business model was centred around two key strategies: a managed discretionary account service and a superannuation rollover business. ASIC cancelled ACME Advice’s AFSL following concerns that Greg and Michael had breached a number of their legal obligations.

A hearing before the Administrative Appeals Tribunal (AAT) in 2023, found that the brothers’ contraventions included:

- recommending products without adequate knowledge or education

- failure to maintain educational standards

- misleading and deceptive conduct

- failing to provide appropriate advice

- failing to act in the best interests of clients

The AAT upheld ASIC’s decision to cancel ACME’s Australian financial services licence.

Greg and Michael potentially breached the following standards of the Code of Ethics:

Case study two – conflict of interest

Candice was the sole director of CC Advice and an authorised representative of an AFS licence holder, ACME Financial Planning. She recommended her clients invest in the ACME Income Opportunity Fund, a registered managed investment scheme operated by her licensee.

An ASIC investigation found that over a three year period, Candice recommended that the majority of her clients invest in the ACME Income Opportunity Fund; although it was positioned as a fixed income fund, it was in fact invested in high risk structured credit vehicles, such as collateralised debt obligations. As such, it was considered to be a high-risk financial product. Candice had a specific interest in the Fund via personal borrowings that she invested in the Fund and ASIC found that she failed to prioritise her clients’ interests above her own when recommending they invest in the Fund.

Further, the high-risk nature of the investment did not match her clients’ risk profiles or experience, and Candice was found to have failed to conduct a reasonable investigation into alternative financial products that would have better met her clients’ needs.

ASIC banned Candice from providing financial services for three years.

Candice’s actions potentially breached the following standards of the Code of Ethics:

Case study three – product knowledge

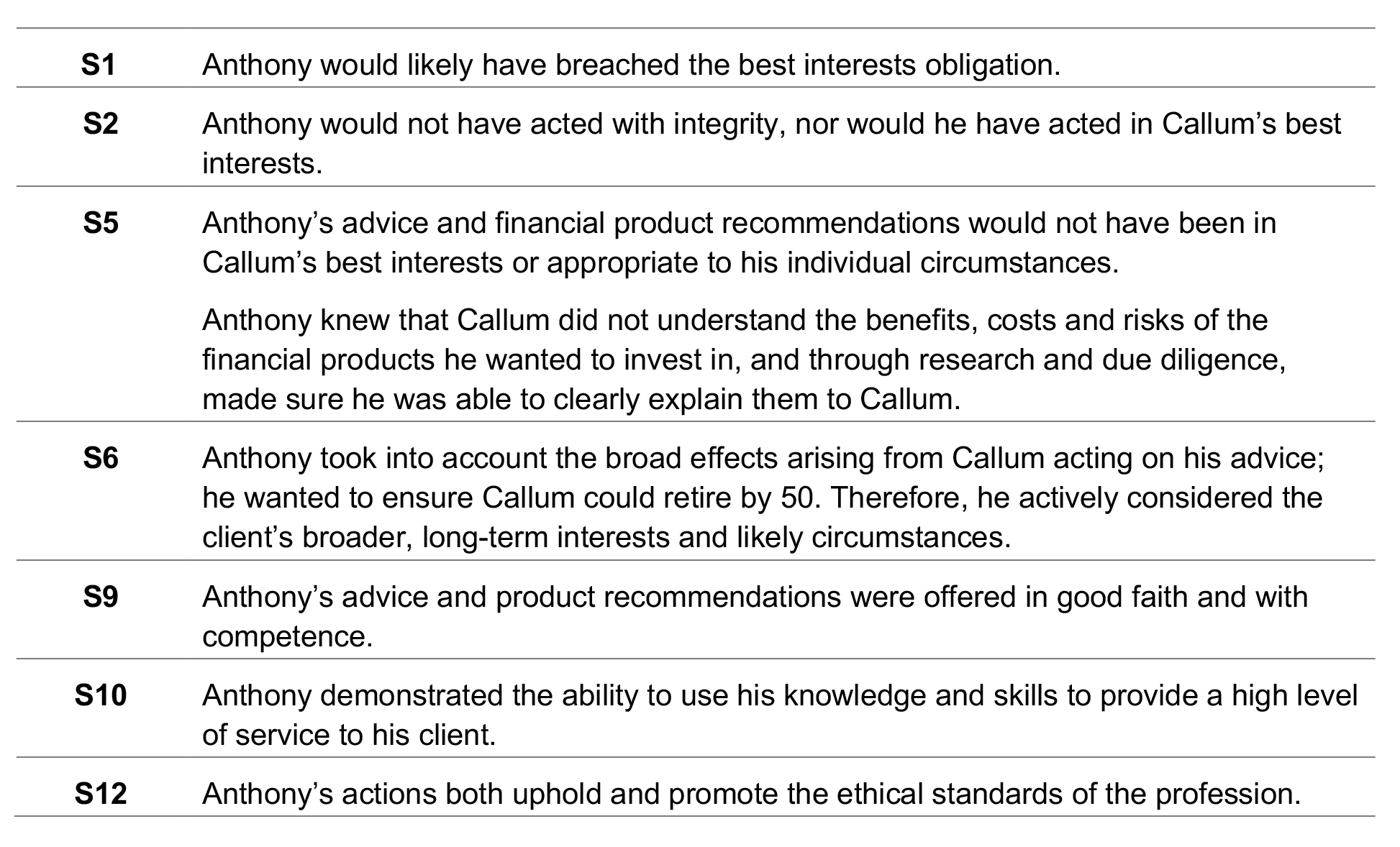

Anthony is a financial planner who is meeting with a new client, Callum, aged 38. Callum holds an executive role and earns $275,000 per annum. He wants to establish a financial plan with the key objective to retire by age 50. Anthony understands Callum’s financial objectives and personal situation and is providing personal advice.

The adviser and client discuss a range of financial products that might be appropriate for Callum. Callum has friends who, in his words, are ‘big in investment’ and he wants to take on board some of their recommendations. As Anthony was not familiar with some of the investments Callum wanted to include in his portfolio, he asked Callum for a list of proposed investments and said he would need to undertake some research and due diligence before they proceeded.

At their next meeting, Anthony explained the high risk nature of the investments Callum had identified and explained why he believed they should not form part of Callum’s investment portfolio. Although Callum followed Anthony’s advice, he separately followed his friend’s recommendations also, with mixed results.

Although Callum’s total outcome was not as good as it may have been, Anthony did the right thing by doing his due diligence on products he was unfamiliar with. Had he blindly accepted Callum’s request, he may have breached several standards in the Code of Ethics including:

Case study four – regulatory compliance

Case study four – regulatory compliance

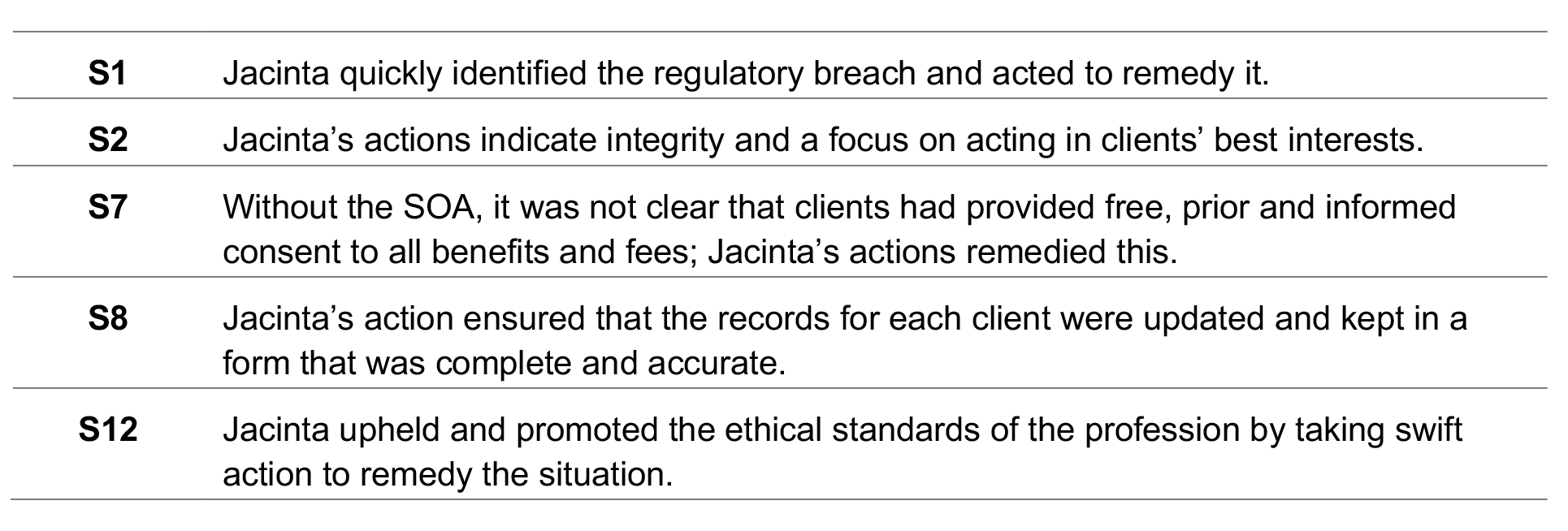

Jacinta has been a financial adviser for many years and operates under her own AFSL. Business in the southeastern suburbs of Melbourne was booming and she took on a younger financial adviser to work with her. Lisa had completed her professional year, passed her Financial Adviser Exam and had two years’ experience with another practice.

At a client event, Jacinta heard in passing from a new client that they had not received a Statement of Advice from Lisa, but that they were very happy with the plan she had developed for them. Jacinta followed up with Lisa post the event. She discovered that Lisa believed the Statement of Advice was a waste of her and the clients’ time, that she believed they were rarely read and that she could provide a better outline of her service to clients.

Jacinta reviewed the number of clients this related to (10). She explained to Lisa that an SOA is required when providing personal advice, making a recommendation to acquire or dispose of a financial product, when there is a change in a client’s circumstances, or when recommending a new product or strategy. Further, the provision of an SOA is a regulatory requirement and therefore not negotiable. She gave Lisa seven days within which to produce and provide SOAs to the affected clients, with a letter of apology and explanation of next steps. Jacinta also informed Lisa that her action was reportable to ASIC and would have to be done within 30 days – however, she wanted to be able to report that the situation had been remedied with no adverse consequences to clients.

Had Jacinta not taken the actions she did, as licensee she would have potentially breached the following standards:

The field of financial advice can be fraught with ethical challenges that demand a high level of professionalism and integrity. Conflicts of interest, transparency, regulatory compliance, continuing education, and the impact of technology are all critical areas where ethical dilemmas frequently arise. Financial advisors must navigate these challenges with a steadfast commitment to ethical conduct, placing their clients’ interests at the forefront of their practice.

By fostering a culture of transparency, adhering to regulatory standards, continuously educating themselves, and responsibly integrating technology, financial advisers can uphold the principles of ethics and professionalism. This not only enhances the trust and confidence clients place in them but also contributes to the overall health and integrity of the profession. As the financial landscape continues to evolve, a commitment to ethical practice will remain a cornerstone of effective and responsible financial advice.