Demand for new home loans eased in May, with first home buyer demand hit the hardest, while investors demand for mortgages also dipped, but remains very strong overall, leaving investors vulnerable due to any potential increase in interest rates should inflation remain above the central bank’s target band, according to Tim Keith, Managing Director of fund manager and private lender, Capspace.

Demand for new home loans eased in May, with first home buyer demand hit the hardest, while investors demand for mortgages also dipped, but remains very strong overall, leaving investors vulnerable due to any potential increase in interest rates should inflation remain above the central bank’s target band, according to Tim Keith, Managing Director of fund manager and private lender, Capspace.

New official data released today reveals that the value of new loans to investors for housing fell 1.3% in May to $10.7 billion but was still 29.5% higher than a year ago. The data from the Australian Bureau of Statistics (ABS) also shows the value of new loans to owner-occupiers (excluding first home buyers) fell 1.6% in May to $12.9 billion while first home buyer loans decreased the most, by 2.9% to $5.2 billion.

Notably, since May 2023, the value of new loans to investors has risen across most states and territories. The largest rises were in NSW (up 24.8%), Queensland (up 48.2%) and WA (up 73.9%). The value of new loans to investors in Queensland hit an all-time high of $2.4 billion in May, exceeding Victoria for the third straight month. The average loan size for investors in Queensland has risen 14.3% since May 2023 to $580,000 while the average loan size in Victoria has fallen 3.2% to $566,000, ABS said. NSW leads the nation with the largest loan size at $796,815.

“Investor demand for housing has eased in May due to higher interest rates, though strong growth over the past year has added to upward pressure on property prices,” said Mr Keith.

“Ongoing population growth will put further pressure on house prices and rents nationally in the coming year, keeping upward pressure on the size of household mortgages sizes, as well as inflation and potentially official interest rates,” he said.

Traders have priced a just-under even chance that the RBA will increase interest rates at its next meeting following stronger-than-forecasted inflation in May, according to Bloomberg.

“We believe that with the employment market remaining tight, and with no immediate signs of inflation falling below 3%, the RBA is likely to keep interest rates on hold at its August meeting and in the months to come or it could raise them again if inflation needs further taming,” Mr Keith said.

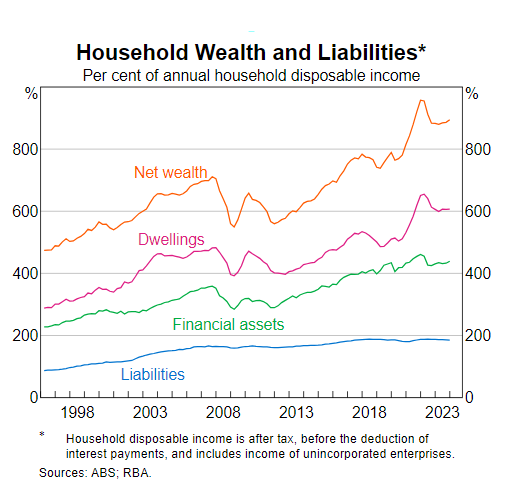

ABS data reveals that the key driver of household wealth gains in recent years has been rising property prices, which have outstripped growth in liabilities, as the chart below from the Reserve Bank show.

“With such a large proportion of individual wealth tied up in property, it makes sense for investors to diversify into other asset classes such as fixed income, to lessen the risk of their wealth falling should residential property prices pull back or interest rates rise,” said Mr Keith.

“While lower rates helped to boost asset values leading up to and after the Covid pandemic, higher interest rates could work to erode wealth in coming quarters should interest rates rise again this year. That indicates a positive outlook for the returns on private credit, as most corporate loans are floating rate and can increase with changes in the official cash rate,” he said.

According to Mr Keith, private credit offers an attractive level of regular stable cash income and return for investors, particularly in comparison to the long-run average returns of more volatile asset classes such as residential property.

“Over time, I expect individual investors to follow the lead of Australia’s largest superannuation funds and invest more in private credit investments, which do not attract a huge stamp duty impost or require a large initial deposit such as is required for residential property purchases.

“Private credit offers opportunities to younger investors as they can invest smaller amounts of money, unlike property investments which due to the high costs are beyond the reach of many Australians,” Mr Keith said.