How will AI impact corporates and the related investment implications?

Artificial intelligence is the topic du jour. It seems it will affect all aspects of life and provide a number of investment opportunities. In this article, GSFM’s investment partner TD Epoch examines these opportunities and answer the question – is AI a bubble or structural shift?

TD Epoch believes that generative artificial intelligence (AI) is destined to be the key driver of equity markets over the next decade or so. AI can be viewed as the fourth wave of digital technology after the PC, internet and mobile. Each stage has had a progressively greater impact on the labour market, productivity, sector concentration and free cash flow (FCF) generation. But first – is there a bubble?

Is AI overhyped? A bubble?

The adoption of artificial intelligence (AI) has driven huge gains in the US stock market over the past 18 months led by the greatest beneficiary of all – semiconductor company, Nvidia. The AI theme is likely to be an enduring one with winners including the biggest technology companies, as they are able to invest massive amounts of cash in this emerging technology.

Although Epoch does not believe AI is just another overhyped fad, a lot of rapturous commentary is reminiscent of previous episodes of speculative frenzy. Further, an awful lot of earnings growth has already been priced into several big tech names, particularly among the Magnificent Seven (Mag 7) and it is not at all clear the prevalent rife optimism will be proven justified. To illustrate, one of the Mag 7 names needs to growth earnings by 20 percent annually for the next eighteen years to justify its euphoric multiple, an incredible feat for any company and unprecedented for a firm of its size.

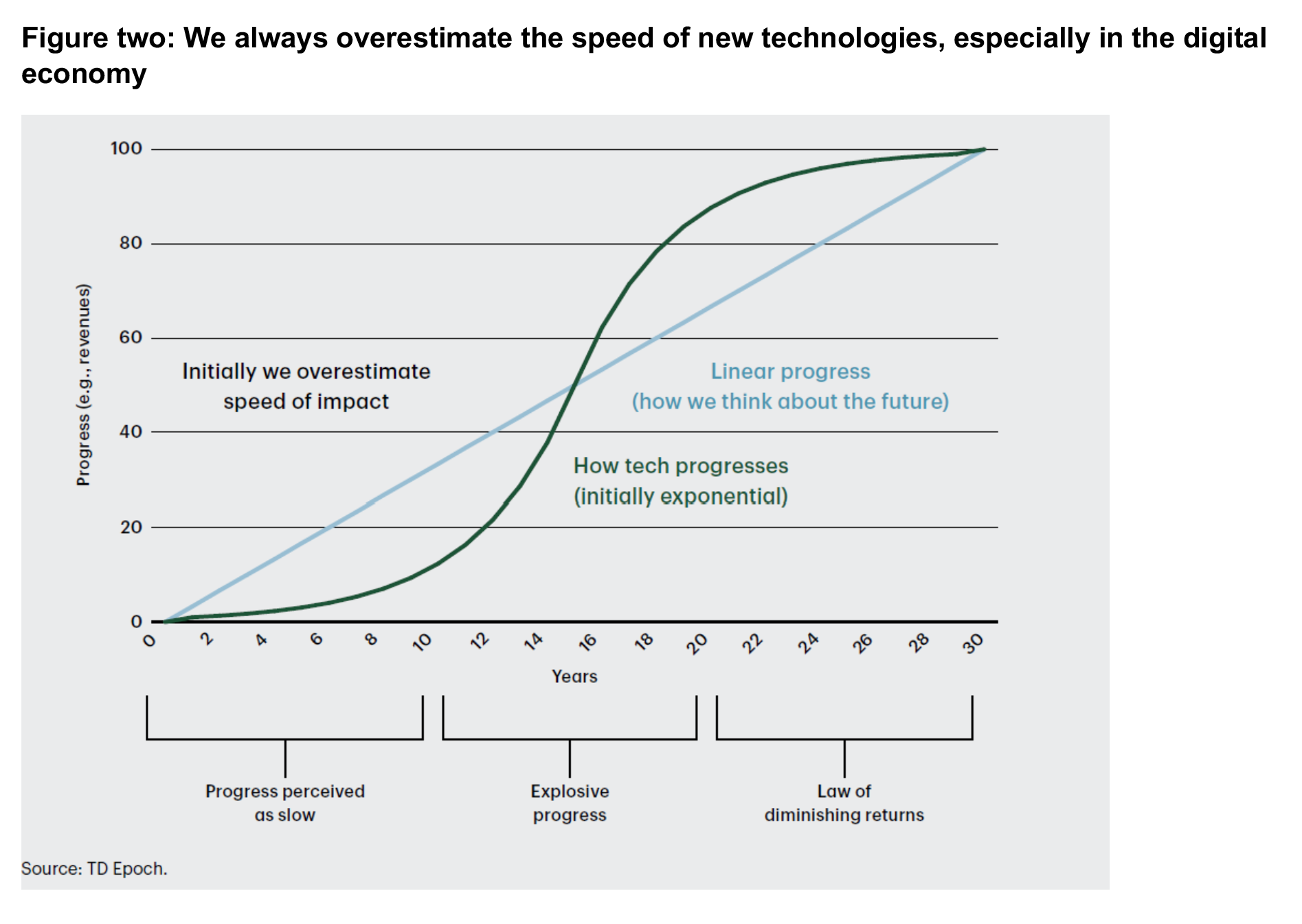

In most of the cases illustrated in figure one, the underlying asset classes were essentially sound (the jury is still out regarding Chinese equities and digital currencies), but market momentum and price action raced ahead of fundamentals. This is especially common with new technologies, such as the internet from the mid-1990s, and even further back to railways in the 1840s. Conceptually, we expect progress to be linear whereas digital tech typically proceeds exponentially (figure two). This can lead investors to swiftly pivot from euphoria to disillusionment when progress is perceived as occurring too slowly.

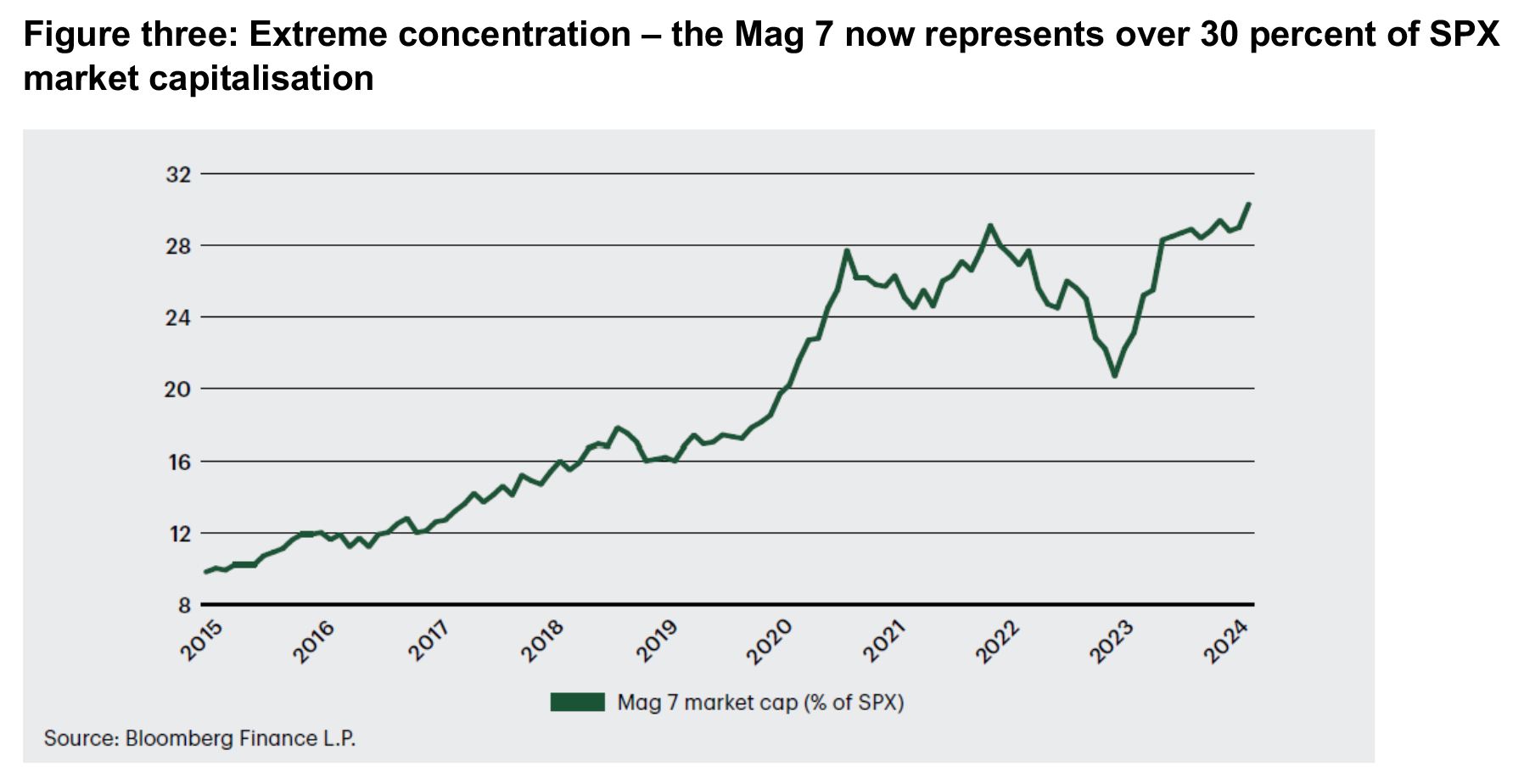

Does AI represent just another bubble? The next three charts demonstrate why a vocal minority of commentators argue that is the case. For a start, the enormous appreciation of the Mag 7 has represented 45% of the S&P 500’s market cap gain since 1/2015 and 66% since 1/2023 (figure three).

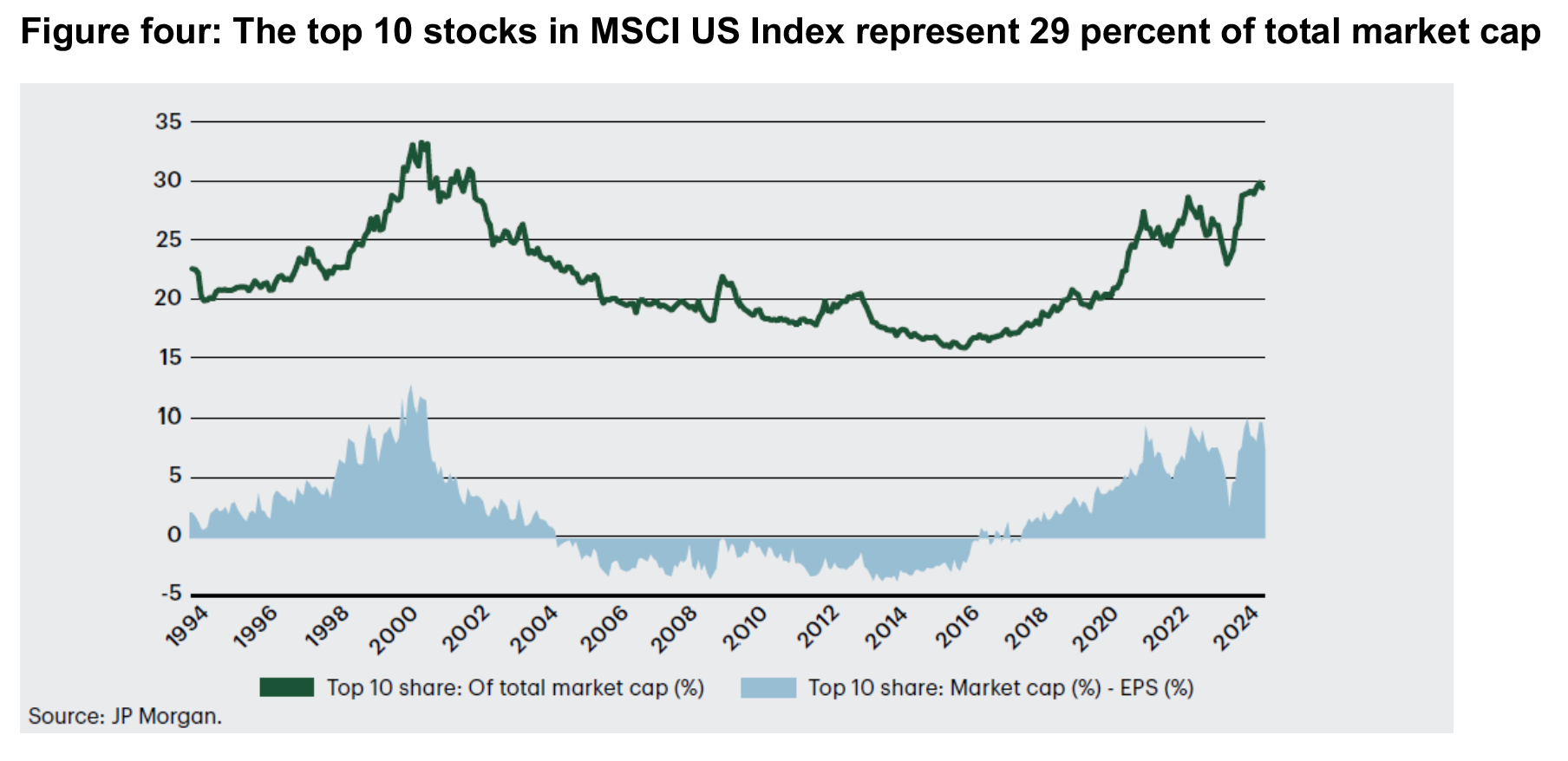

A second sign of potentially ‘bubblish’ behaviour can be seen by looking at the weight of the top ten stocks in MSCI US Index over the last thirty years (figure four). They currently represent 29 percent of total market cap, which is the highest attained since 2001 (or since the tech bubble collapsed in 2000–2001) and leagues above the historical average of 21 percent. Further, they only represent 22 percent of forward earnings per share (EPS), which is just slightly above the 30-year mean of 20 percent. Moreover, the gap between the shares of market cap and EPS, is the largest since the tech bubble and four times the historical norm.

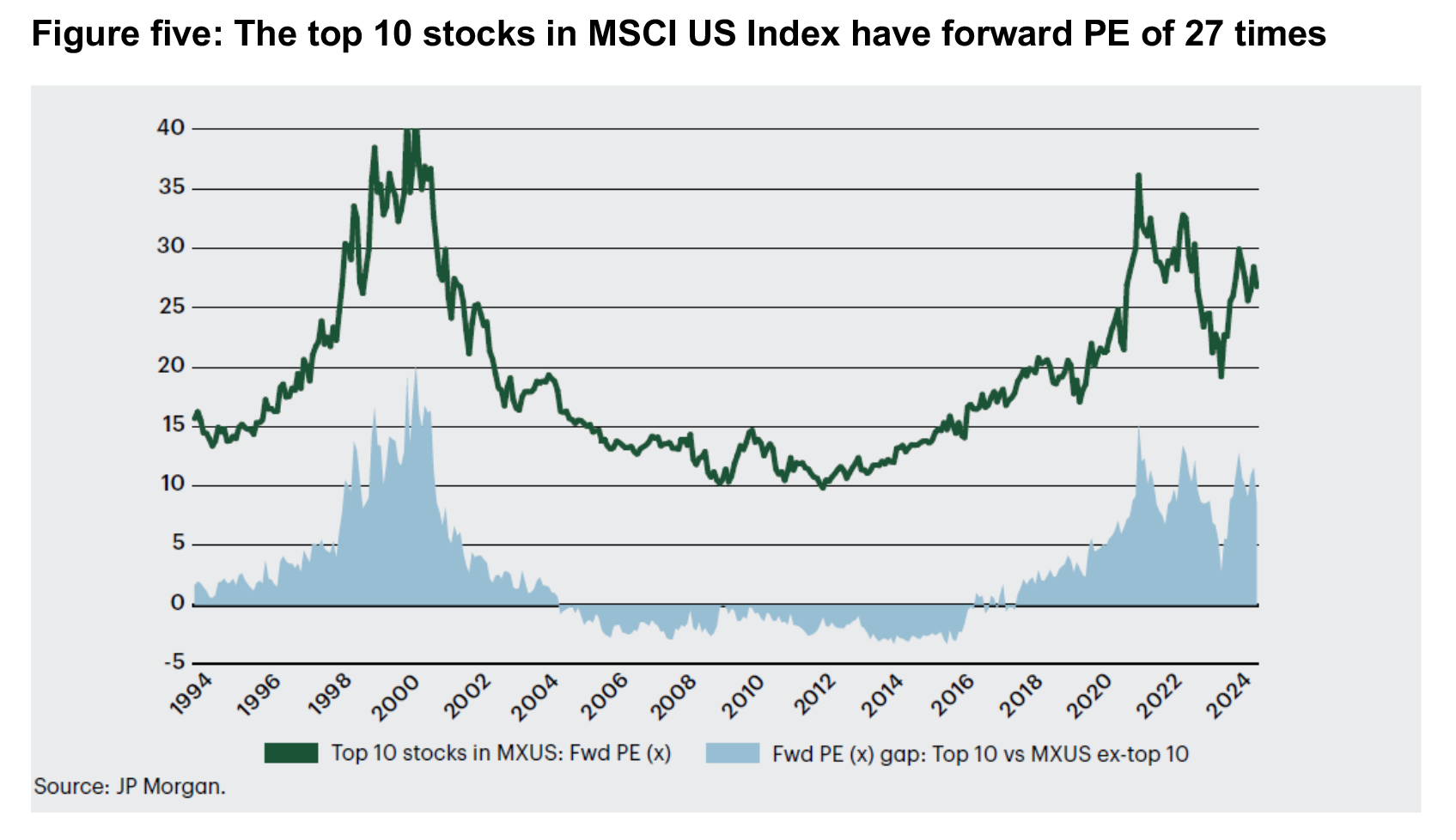

Regarding valuations, the top 10 stocks in MSCI US Index have a vertiginous forward price to earnings (PE) of 27 times, while the remaining 599 names possess a multiple of 18 times, which is only slightly above 30-year mean of 16 times (figure five). Further, the gap between the PEs of the top 10 and the bottom 599 is stretched at four times the historical norm (or the 92nd percentile).

Winner takes most

The case for a bubble, as shown in the previous figures, implicitly assumes AI does not represent a structural change in the distribution of FCF, margins and returns. However, digital tech and substitutes of ‘bits’ for ‘atoms’ invokes powerful, capital-light business models that exploit formidable economies of scale and network effects.

One key feature is that the pursuit of market dominance leads tech firms to invest massively in intangible rather than tangible capital, which involves huge fixed costs but drastically lowers marginal costs. This is what drives ‘winner takes most’ dynamics and produces a smaller number of superstar firms.

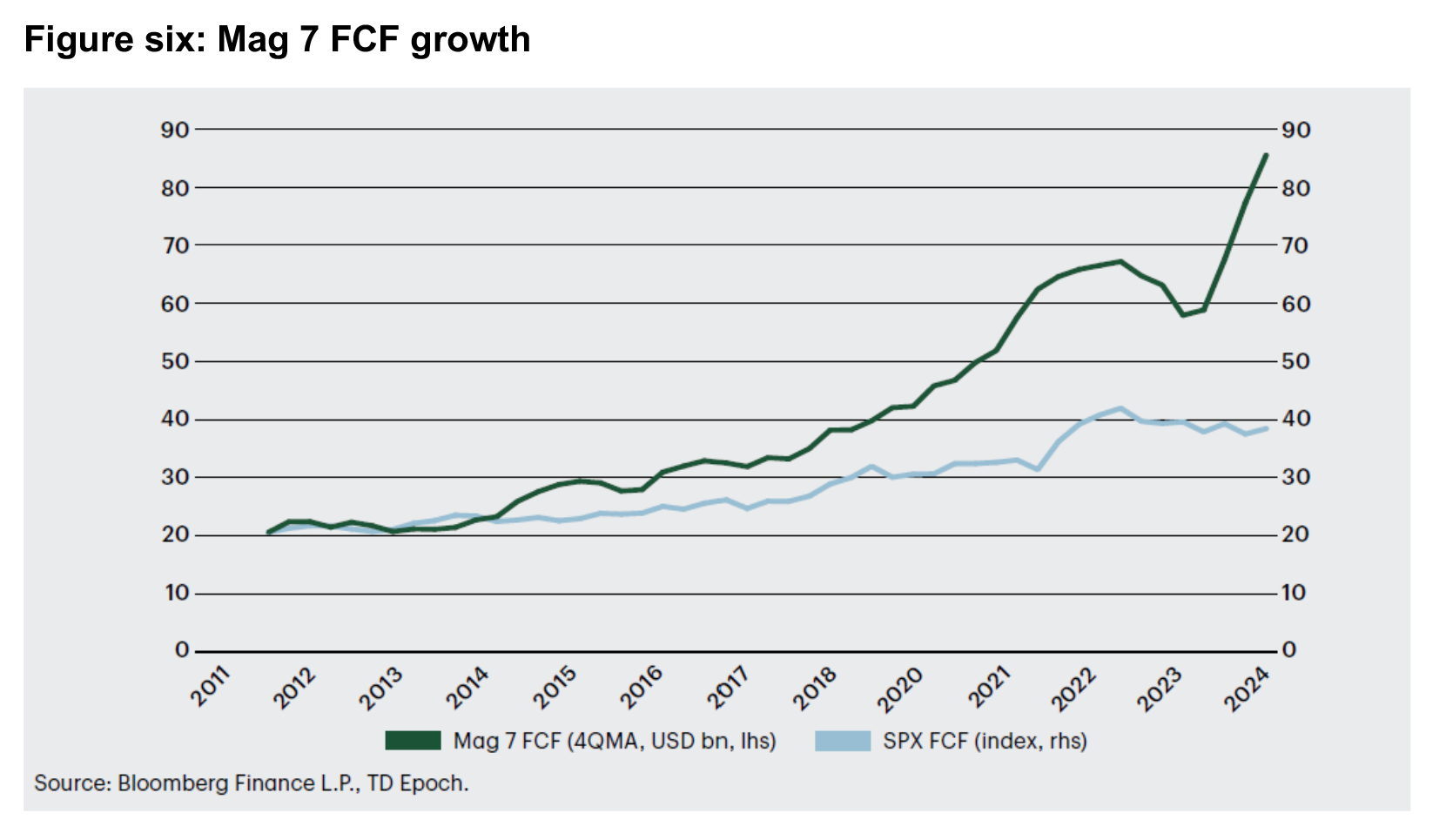

Figure six demonstrates this powerful impulse which Epoch believes is still in its early innings. For a start, the Mag 7 has produced average annual FCF growth of 15 percent over the last decade and 17.5 percent over the past five years.

By contrast, the S&P500 has delivered only five percent growth, roughly in line with US gross domestic product (GDP). Moreover, the S&P493 (less the Mag 7) has generated only three percent FCF growth over the last decade, well below that of the overall economy.

The dichotomy can also be seen in consensus expectations for 2024 EPS growth, which is 12 percent for the overall S&P500. However, underneath lies an extreme bifurcation, with the Mag 7 at a staggering 55 percent and the S&P493 at a paltry five percent.

Echoes of the Late-1990s Tech Boom?

The above analysis has three takeaways. First, a significant amount of earnings growth is currently priced into the tech sector. Second, investors can swiftly pivot from euphoria to disillusionment when progress, especially in FCF growth, is perceived as too slow relative to what’s priced in. Third, AI is not just another overhyped fad, as demonstrated by an impressive track record in generating FCF, OPM and ROIC.

The first two takeaways would have been equally applicable to the internet boom of the late 1990s. However, the third is different. Investors in the internet boom were not sufficiently sceptical of hype stocks that promised future earnings somewhere far down the road but remained negative FCF at the time.

This time, in sharp contrast, the Mag 7 is generating impressive FCF, and consensus expects the group to grow earnings by 55 percent in 2024. Much of this represents revenue from infrastructure build, including blitz-scaling AI platform. Additionally, other companies are reaping early returns from the use of AI to replace coders, marketing copy writers, call centre workers and so on.

These are examples of what economists call “process innovations”; that is, making existing businesses more efficient by lowering operating costs.

However, the vast majority of the value-added from general purpose technologies (GPTs) like AI (as well as the internet, electricity and steam engine) always come from ‘product innovation’. That is, entirely novel goods and services that were not foreseen when the GPT was first commercialised. For example, the steam engine was designed to drain water out of coal mines and electricity’s first commercial product was the light bulb, invented to replace gas lamps which were terrible fire hazards. No one had any idea this would lead to the modern factory, global telecommunications, semiconductors…and AI.

The good news is that this really moves the needle on earnings, creating enormous value. The bad news is, no one ever knows how it will play out and, in sharp contrast to process innovations, it can take years and even decades to be realised. The risk here is that AI is not in fact a GPT. However, essentially all commentators believe AI will: (a) affect many different sectors, (b) create numerous spillover effects and (c) improve over time as it comes to be used widely across the economy. These three characteristics are actually the definition of a GPT.

Four key implications of AI

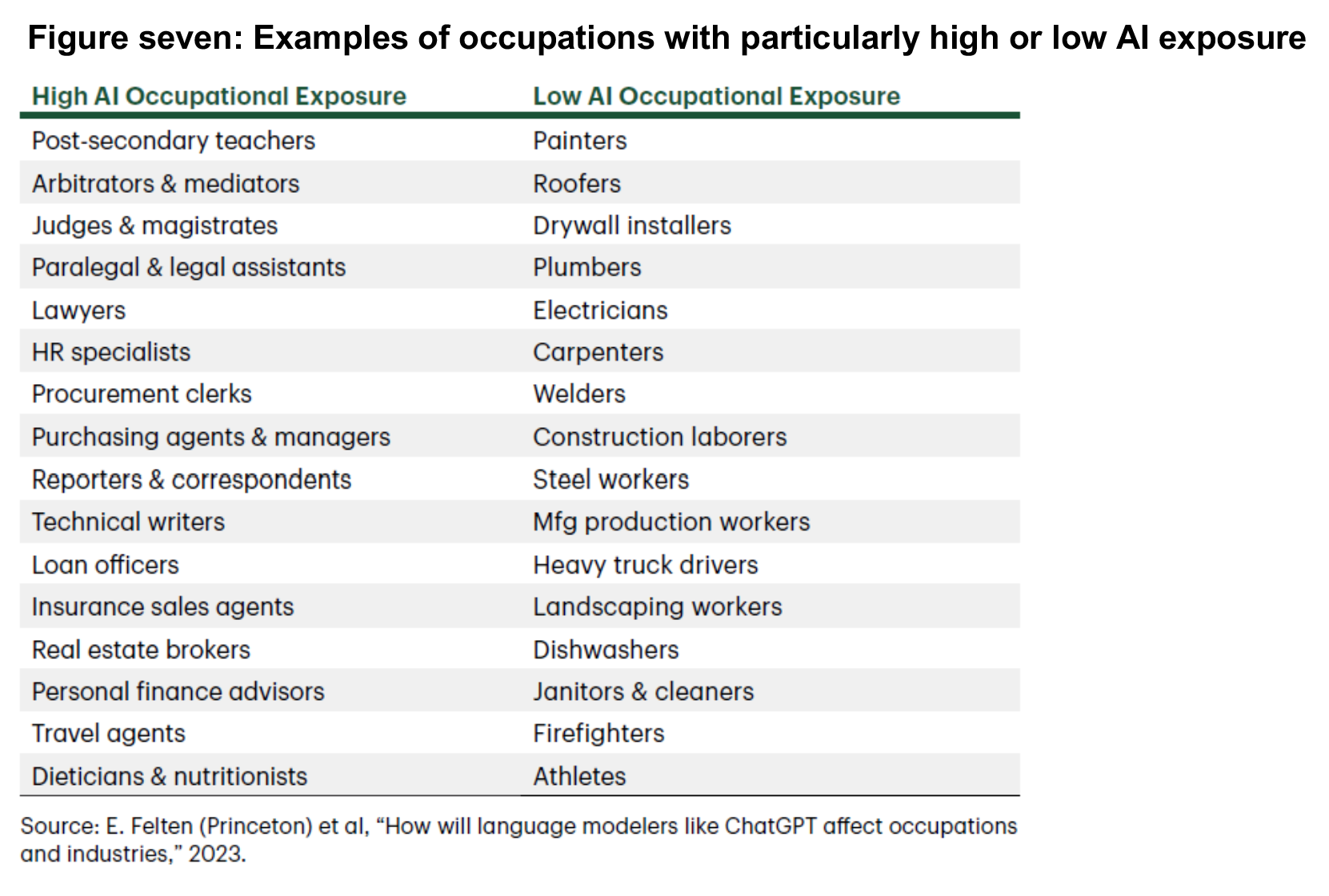

First, AI will be highly disruptive to labour markets. While jobs are not going to disappear, around 60% of tasks and occupations in the United States will be changed materially over the next two decades (figure seven). While overall employment and real wages are expected to rise, this will be accompanied by dramatic shifts across vocations. Further, and different from previous tech shocks, high wage sectors are most exposed to AI.

Second, the diffusion of AI across the economy is likely to increase US productivity by roughly 20 percent over next two decades; this will likely be replicated worldwide. This includes increased efficiency by call centre workers, taxi drivers, coders, writers, radiologists and so on. Early estimates suggest around 60 percent of jobs will have their productivity increased by 30 percent[1].

Further, while most commentators emphasise efficiency gains, the bulk of value generated will come from the innovation and creative destruction AI unleashes, with new products and services that are fated to astonish and baffle us all[2]. Moreover, most of productivity benefits will accrue to larger firms, which exhibit a much higher tendency to adopt advanced technologies[3].

Next, digital tech always features “winner-takes-most” dynamics and that will certainly be the case with AI, as prediction machines invariably scale[4]. Huge fixed-cost investments combined with near zero marginal costs imply enormous economies of scale. This means the lion’s share of value created is captured by a small number of companies and we are likely to witness increased concentration in most sectors.

However, it is always the case that “titans rise and titans fall” so not all of last decade’s winners will remain above the precipice. And this is a good thing, as the displacement of seemingly entrenched incumbents, something the US excels at, is critical for innovation to flourish and radiate across the economy.

Finally, business strategies for the AI era are capital-light, which is positive for margins, FCF, return on invested capital (ROIC) and shareholder yield. This means companies and sectors with relatively high AI exposure are likely to significantly outperform over the medium-term. Regarding country-level allocation, the diffusion of AI is more important than the number of patents or journal articles. This favours the United States with its unrivalled network of innovative titans relative to China, Japan or Europe.

What AI means to the labour market: augmented intelligence

The occupations with the greatest exposure to AI are typically white collar, with high levels of formal education. On the other hand, those with the lowest exposure to AI feature physical skills that will remain beyond the aptitude of AI-enabled robots for the foreseeable future.

For an alternative perspective, AI exposure metrics vary with the skills underlying different occupations. Labour economists often characterise occupations by the degree to which they involve combinations of routine versus non-routine, cognitive versus manual, and analytical versus interpersonal features. They find that occupations with higher AI exposure are more likely to involve non-routine cognitive analytical skills or routine cognitive skills, and less likely to involve different kinds of manual or interpersonal skills.

So, is being in a highly AI exposed occupation a good or a bad thing?

For employers it is unambiguously positive, as it increases opportunities for efficiency and innovation. For employees, it’s a bit more complex. In some cases, being in a highly exposed occupation is challenging as the new technology acts as a substitute, allowing firms to replace workers. To provide a historical example, following WWII a lot of automation was introduced into coal mining. As a result, since 1949 the sector’s productivity rose by 832 percent, but employment plummeted by 89 percent, according to the Energy Information Administration. Analysis by McKinsey suggests that occupations in a similar situation today include office support, customer service and sales, and food services, where AI will probably replace some workers[5].

It is more common for new technologies to act as a complement, that is augmenting labour demand through the creation of new tasks. Historically, GPTs such as the steam engine or electricity, have on net, created an enormous number of jobs as entirely new products, sectors and occupations emerge. AI is a GPT, and history strongly suggests it will likely have a similarly positive impact. McKinsey’s analysis is especially constructive regarding the outlook for STEM professionals, creative workers, and business and legal professionals.

What are the implications for wage inequality? Previous technology shocks have primarily affected lower income individuals and exacerbated wage polarisation[6]. And that certainly has been the case over the last four decades with digital technologies. However, some commentators have argued this time is different, as it appears AI will primarily impact high wage occupations, thus resulting in wage compression.

Winners from the AI movement

As canvassed earlier in this article, digital tech always features winner takes most dynamics and AI will not prove an exception. This means aspiring titans need to move fast and invest enormously. There is room for only a small number of winners in each segment and those companies will reap the vast bulk of free cash flow and profits going forward.

Computer chip design company Nvidia illustrates this dynamic. It has led the AI gains to become almost as large as Microsoft and Apple; in mid-June it momentarily became the largest company in the world. Nvidia’s price now assumes that it will grow earnings by 20 percent a year for the next 18 years. Other companies have done that – Apple did it, Microsoft did it. But they did it when they were much smaller companies…can a larger company such as Nvidia repeat this feat?

Other potentially interesting companies aboard the AI zeitgeist include Taiwan Semiconductor Manufacturing Company (TSMC), the Taiwanese contract manufacturing company. It fabricates the vast majority of leading-edge chips, including those designed by Nvidia.

Semiconductor equipment company, ASML is also interesting. Dutch-based ASML has overtaken the French luxury giant LVMH as Europe’s second largest company, second only to drug maker Novo Nordisk. ASML has for a time been Europe’s largest technology company, making the lithography machines that are critical to chip manufacturing. It possesses a near monopoly in this segment, a result of almost four decades of intense research and development.

AI and the labour market: Investment implications

Advances in AI are ushering in an era of extreme uncertainty as it creates a structural shift. It will likely be extremely disruptive to the labour market, with roughly 60 percent of tasks and occupations directly affected. Still, overall employment and real wages are likely to rise, as typically occurs with GPTs such as AI. However, as with previous waves of technology, it is expected that AI will drive further wage inequality.

Productivity, in economist Paul Krugman’s famous formulation, “isn’t everything, but in the long run, it’s almost everything.” On that note, the diffusion of AI is expected to increase US productivity by 20 percent over next two decades. While this is a very rough guess, we can be more certain that a relatively small share will come from efficiency gains (doing things we already do, but with a bit less labour), with the lion’s share generated by innovative new products and services.

Increased concentration in most sectors is anticipated, with a small number of companies capturing the vast majority of gains in value creation. Finally, business strategies for the digital age are capital-light, which is positive for margins, FCF, ROIC and shareholder yield. This is especially true for companies that establish themselves as global champions in the AI era.

———-