When your client lacks ethics

Ethics is at the core of what most advisers do, day in and day out. However, consider the circumstances where a financial adviser is instructed by a client, but cannot act on that instruction without breaching an ethical standard? This article, proudly sponsored by GSFM, will examine client driven ethical dilemmas.

Ethics is at the core of what most advisers do, day in and day out. However, consider the circumstances where a financial adviser is instructed by a client, but cannot act on that instruction without breaching an ethical standard? This article, proudly sponsored by GSFM, will examine client driven ethical dilemmas.

Pause for a moment and ask yourself: do you consider yourself ethical? Most people reading this article would confidently say yes. However, it’s important to recognise that different value systems mean one person’s moral code—and their concept of ethics—may not align with another’s. While most individuals act ethically most of the time, challenges may arise when a client requests something outside your ethical boundaries.

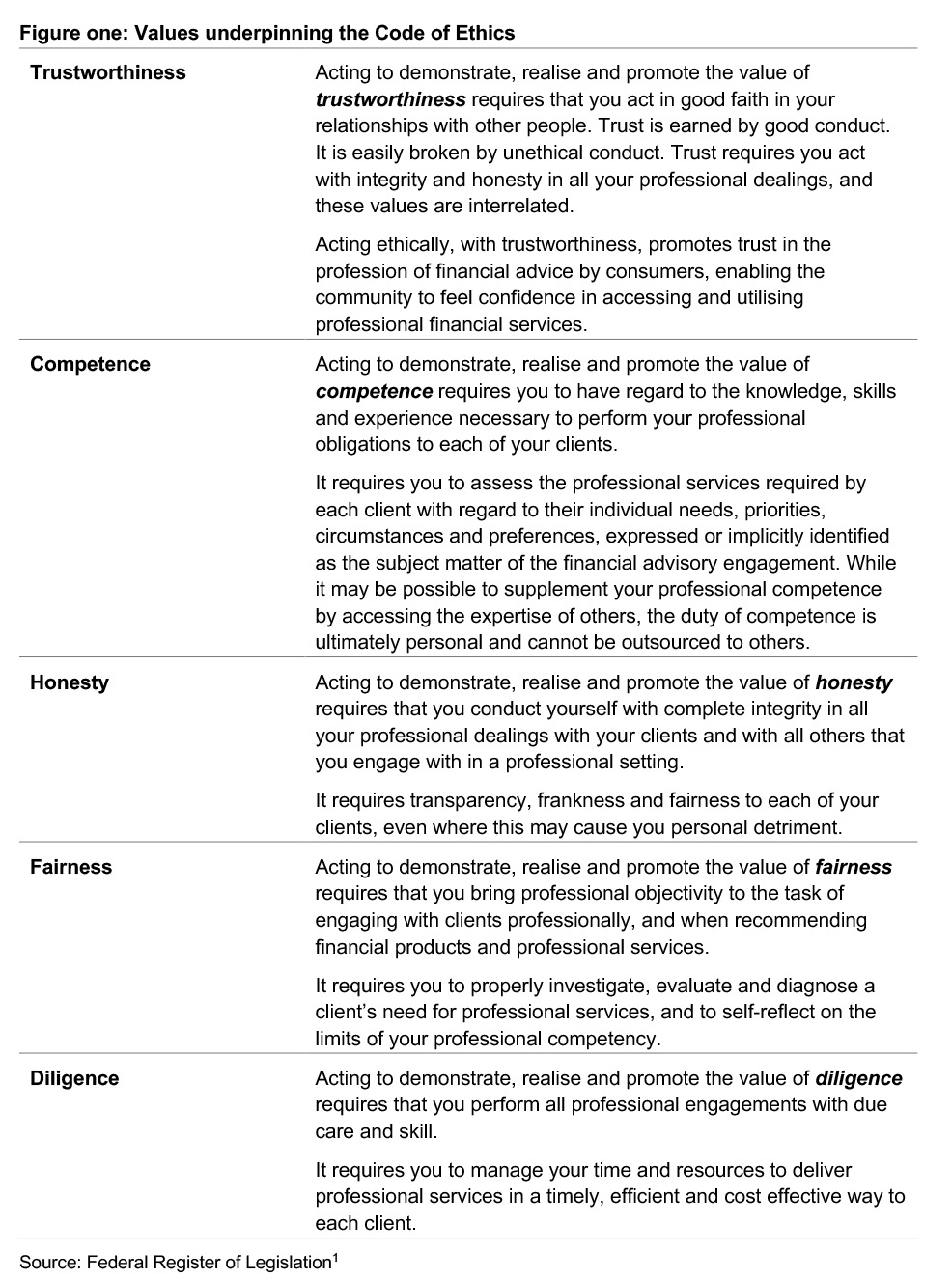

For the majority of advisers, ethical practice has always underpinned their service offering. Since 1 January 2020, this has been enshrined in law within an ethical framework that includes five values (figure one) and twelve standards. Even though advisers may understand and appreciate this framework when providing financial advice, their clients might sometimes have different perspectives.

Take the case of Jim (not his real name). He was approached by a friend wanting financial advice. He didn’t want to do a fact find, he didn’t want to pay for an SOA and ‘all that compliance stuff’ – he just wanted some investment advice. This friend would expect Jim to adhere to these values – be trustworthy, competent, honest, fair and diligent – yet he asked him to act in a way contrary to the regulatory and ethical codes that Jim is bound to. Further, Jim’s friend wanted investment advice that would help him avoid paying tax…so, not simply asking Jim to operate outside of his compliance requirements, but to advise in a way contrary to tax laws, the Corporations Act 2001 and the Code of Ethics.

Encountering ethical dilemmas with clients is not uncommon. The best defence against this situation is a good offense…by being aware of foreseeable conflicts and discussing them frankly with your colleagues and clients, you can avoid the misunderstandings and challenging situations that lead to greater problems.

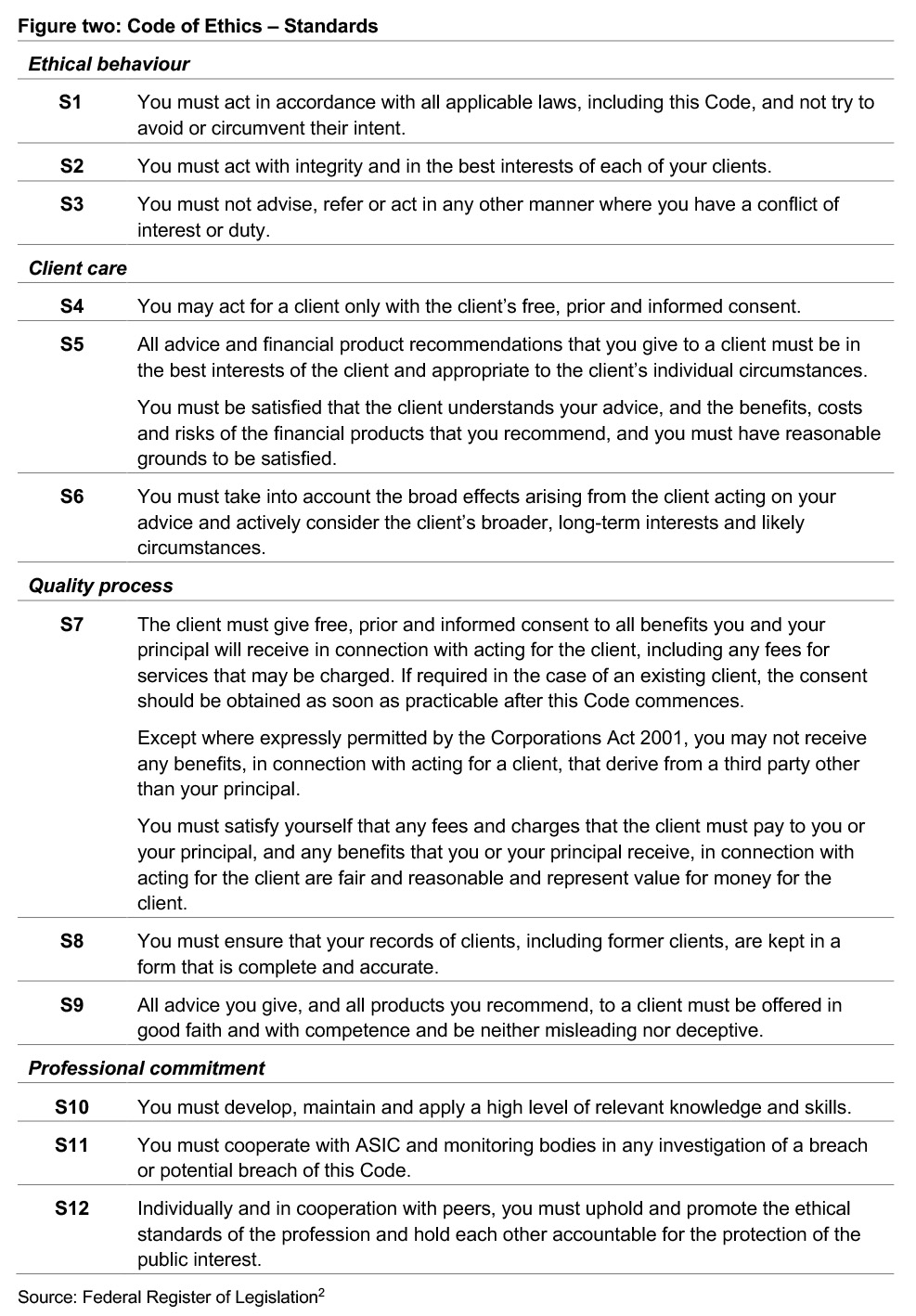

Understanding your clients’ attitudes and beliefs is important – after all, everyone has different value systems. While aligning your values and beliefs with those held by a client is not a prerequisite for working with them, the proper handling of any ethical dilemmas that arise is a requirement. No adviser wants to face enforcement action by ASIC for breaching any of the twelve standards (figure two) in the Code of Ethics (the Code).

The standards within the Code are not meant to provide definitive guidance. Individual circumstances will vary, and the Code allows for differences in professional opinions on applying the profession’s ethical rules in specific cases. Ultimately, it’s important to remember:

“Doing what is right will depend on the particular circumstances and requires you to exercise your professional judgement in the best interests of each of your clients.

Ethics, morals and values – same, same or different?

The terms ethics, morals and values are sometimes used interchangeably; while they are closely related concepts, they differ in significant ways.

Ethics are the principles and standards that govern behaviour within a specific context, such as a profession or society. They provide a framework for determining what is considered right or wrong in various situations, often derived from philosophical theories, legal guidelines or professional codes of conduct. Ethics help to maintain order and ensure that individuals act in ways that are consistent with the expectations of their community or profession.

Morals are the personal beliefs and values that an individual holds regarding what is right and wrong. These are typically shaped by cultural, religious and familial influences and are deeply ingrained in an individual’s conscience. Morals guide personal behaviour and decisions, reflecting one’s sense of integrity and ethical convictions on a more personal level.

Values are the core principles and standards that an individual deems important and worthwhile. They influence attitudes, behaviours and choices, and serve as a personal compass for what is meaningful in life. Values are fundamental beliefs that guide how people live and interact with the world, shaping priorities and motivations in various aspects of life.

In essence, ethics are more about external guidelines and frameworks, morals are internal beliefs, and values are the core principles that drive one’s actions and choices.

Client directed unethical behaviour

Ethical dilemmas arise in situations where there’s a difficult choice to be made between two or more options. Where this dilemma arises because of a client’s request or action, the adviser is often faced with an option that doesn’t align with the Code and/or societal norms, including codes of law. This often negatively impacts the adviser’s moral code and values.

In financial advice, ethical behaviour can be distilled into acting in the client’s best interests at all times, acting with competence, honesty, integrity and fairness. In short, upholding the values that underpin the Code and in the way any one of us would like ourselves and our family members and friends to be treated by any professional service provider.

The unethical client will generally reveal themselves to you by what they say. While some unethical clients may be quite direct, others may take a more subtle approach, such as talking in hypotheticals. For example: “I have information that ABC Limited is subject to a takeover at $X per share; I’d like to buy shares in it to benefit from the anticipated share price increase” versus “If I was to come into information that would impact a company’s share price, could we use that to add value to my portfolio?”.

If a client asked you to do something unethical (which might also be illegal) you may face one of the most challenging dilemmas of your career. This can be an extremely difficult situation, one which could have serious consequences for you and your licensee (and potentially, other authorised representatives working under that licence). Some actions – such as the insider trading example used above – can also have serious consequences for the client.

Repercussions for advisers that can arise from acting on an unethical client request might include:

- a breach of the law

- a breach of one or more ethical standards

- damage to your reputation and credibility

- losing your right to practice – and, if independently licenced, your AFSL

- the potential for your licensee to lose their AFSL or have conditions imposed

- the risk of being charged, incurring a fine and/or imprisonment.

Such repercussions won’t necessary be limited to you – they can impact:

- your colleagues, who may need to find a new licensee and whose reputations may be damaged by your actions

- your Licensee, which might be subject to a range of penalties

- your family, as they lose an income and have to deal with the added impact of financial penalties and potential incarceration

- your other clients, who will need to transition to a new financial adviser/licensee.

How to respond to a client’s unethical directive

Not every situation is clear-cut; ethical dilemmas often present themselves in various shades of grey, so it can be a challenge to discern the right course of action.

Some client requests are overtly suspicious and immediately raise red flags. However, other requests might be more subtle and not as immediately alarming. When confronted with an ethical dilemma, it’s common to feel overwhelmed by emotions, making it challenging to think clearly.

Examples might include:

Clear ethical concern: A client asks you to establish a managed account in his wife’s name (using her maiden name) so he can trade his company’s shares.

Subtle ethical concern: After some poor decision making by SMSF trustees, the trustee client requests that you slightly overstate the projected returns on their SMSF to make the poor decisions less apparent.

An overwhelming situation: A colleague asks you to sign off a friend as meeting the sophisticated investor requirements so they can get access to a particular wholesale investment. This request puts you in a difficult position as such a move compromises your professional integrity.

In such scenarios, it’s crucial to pause, reflect and seek guidance to navigate the ethical complexities. The following ‘do’s and don’ts’ are based on insights from Amy Gallo of the Harvard Business Review[3]:

Do…

- Question your assumptions because fear of confrontation or retaliation can result in rationalising an action you know isn’t right.

- Gain perspective and try to understand what is motivating the request; this can help form a response, particularly when there’s an ethical way to achieve the same goal.

- Have a conversation: With the exception of extreme ethics violations, confronting the individual directly first is often the best way to manage a situation. Provide an opportunity for the person to explain his actions or to correct the behaviour first. If a direct conversation doesn’t resolve the issue, you may need to inform your manager, HR department or a company ethics hotline.

Don’t…

- Forge ahead without a plan – a planned approach is important to adequately address the situation.

- Make accusations, rather maintain a focus on understanding the situation and request.

It is critical that you maintain your ethical awareness, particularly in the context of the twelve standards that comprise your Code, while also practicing sound judgment as you determine the appropriate steps to deal with ethical dilemmas.

The following can assist you to make better-informed decisions, ones that align with your values and enable you to provide an ethical example to the other members of your team. When all team members are aligned with respect to ethics and values, your advice practice will be more effective.

1. Clarify the client’s request

Make sure you understand exactly what the client is asking you to do. What is their desired outcome from this action? How exactly do they want this to play out and what is their role?

Examining the client’s intent with probing questions is sometimes enough for a client to recognise they have asked you to do something unethical. Some clients may ask you to do something unethical because they don’t know better. Others may know all too well what they’re asking and may be less than honest; it is a good habit to ask probing questions and take detailed notes.

Use questions such as “Can you help me understand?” or “Can you see an issue with that approach?” can help establish whether your client is open to a productive discussion.

2. Reaffirm their request

Repeat back what you think the request is to ensure you have complete clarity. This may resolve the issue, either because you’ve misunderstood or because the newfound perspective has made the client rethink their request. If the client wishes to persevere with the course of action, you can ideally deliver a strong and immediate response.

However, there may times you are blindsided by a request and need some time to consider the issues and formulate an appropriate response. In such a case, it’s best to advise the client that you’ll need to defer the discussion.

If simply reaffirming the request aloud does not work, probing the client with questions about the reason and motivation behind the request can help to create a more transparent dialogue and also help deter them.

3. Consider the big picture

You’re clear on what the client has asked you to do, the client is clear that you understand what they want to do, but the client has not had a ‘light bulb’ moment and has not recognised they have put you a position that could range from difficult through to untenable.

Note down the issues you have with their directive:

- How does it sit within your moral code and values? How will it affect the ethical code and standards you’re obliged to follow?

- Consider each of the twelve ethical standards and how actioning your client’s request might beach them.

- Give thought to the Corporations Law and any potential breaches of that too.

- How might this impact your licensee, colleagues and family – and how might it reflect on the broader advice profession

4. Articulate your concerns

A client directed ethical conundrum presents a complex challenge. While your goal is to help each client achieve their financial objectives, it’s crucial to address any request that conflicts with the ethical principles and standards you’re bound to uphold, as well as your own values. In discussing this with your client, you could explain:

- How their request would violate your personal ethical and moral boundaries.

- How their request would contravene the Code and legal standards of your profession.

- The potential consequences for both of you, including damage to your reputations, possible job loss and broader impacts on family and others.

- The potential legal and financial penalties you could both for engaging in unethical and illegal actions.

Ultimately, you need to ensure that you can live with the final decision…even if it means losing a client.

5. Offer an alternative solution

At this point it’s important to keep your cool; being faced with an ethical dilemma can see emotion take front seat.

If you can find an alternative that does not result in you having to compromise your principles or the Code, explain that to your client as tactfully as you can.

Let your client know that you’re uncomfortable with their request by articulating your concerns (step four), but if possible, offer an alternative solution. If your alternative approach is rejected – or there is no alternative approach – the best thing for you and your practice is to walk away.

Importantly, if you do decide not to have any further dealings with the client, you need to offboard them and be sure to keep a detailed file note, lest they return, or some issue arises in the future.

Case studies

The following case studies are based on real events, but some details have been amended to make them relevant to the article’s topic. Names of people and organisations have been changed. The case studies have been drawn from the Australian Financial Complaints Authority (AFCA) or ASIC. For each, potential breaches of the Code of Ethics are identified.

Case study one: Faking it

Queensland based financial adviser Alexander worked with three colleagues at ACME Advice on the Gold Coast. He had a number of friends to whom he provided personal advice, but without fulfilling the required compliance paperwork. This was at the friends’ behest as they wanted advice without the associated paperwork and cost burden.

In its investigation, ASIC found that as the general manager of ACME Advice, Alexander had asked a subordinate, an authorised representative of the licensee who was on maternity leave, to sign documents that stated that personal advice had been provided by the authorised representative when it had not been.

In this way, Alexander felt he was able to provide the advice his friends sought, while on face value meeting his compliance requirements. However, ASIC took a dim view of his actions and permanently banned Alexander from:

- providing any financial services

- performing any function involved in the carrying on of a financial services business

- from controlling an entity that carries on a financial services business.

ASIC claimed that Alexander’s conduct gave reason to believe that he lacks the fitness and propriety to provide financial services or manage or control those who do.

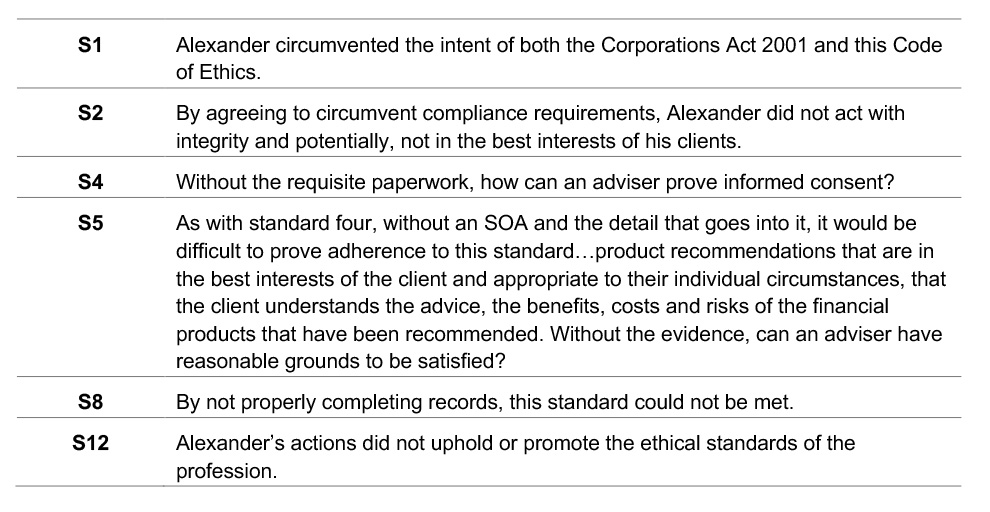

By meeting his friends’ request, Alexander’s actions saw him potentially breach the following standards in the Code:

Case study two: Elder abuse

Jack and Rose are a married couple in their mid-80s. They are not separated, but due to the different levels of care each requires, the couple resides in different aged care facilities. Rose has dementia and needs a higher level of care than Jack, who retains a high degree of autonomy and independence. Their retirement funds are held in a joint account, and their financial adviser, Elizabeth – an authorised representative of ACME Retirement Advice – oversees their financial affairs.

Jack and Rose did not have children together. However, each had been previously married and had children from their first marriages. Several years before entering residential aged care, Jack and Rose signed a power of attorney that provided Jack’s daughter and Rose’s son with an authority to view financial statements online and pay their bills, but no authority to withdraw or transfer funds.

An issue arose when Jack’s daughter contacted ACME Retirement Advice to report what she believed to be an unauthorised transaction with respect to the joint account.

Rose’s son took his mother to see Elizabeth. Rose instructed the financial adviser to close the joint investment account she held with Jack, redeem the investments and transfer the funds into a bank account in her name only. These funds totalled nearly $200,000 and 75 percent of the funds were subsequently transferred to Rose’s son.

Jack, with the assistance of his daughter, said Elizabeth should not have allowed Rose to close their joint investment account and transfer the funds into her name without his knowledge or consent.

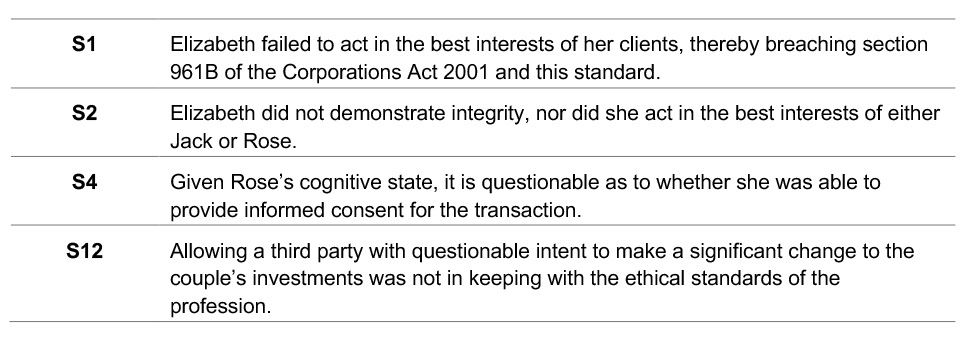

The dispute was referred to AFCA. Although the findings agreed that Elizabeth’s notes had considered whether Rose had capacity to conduct the transaction, it believes she failed to make enquiries of Rose in the absence of her son before acting on the request. She should also have contacted Jack to ensure he consented to the transaction.

AFCA concluded ACME Retirement Advice did not exercise appropriate care and skill in response to the following ‘red flags’:

- the unusual nature of the disputed transaction

- the wife who conducted the transaction was in her 80s, in a wheelchair and known to have cognitive issues

- the discussion and transaction was conducted in the presence of a third party who may not have had the client’s best interests at heart.

Consequently, AFCA determined ACME Retirement Advice did not comply with good industry practice to protect the applicant from potential financial elder abuse, and Elizabeth was required to transfer half the funds, plus interest, into an account nominated by the applicant.

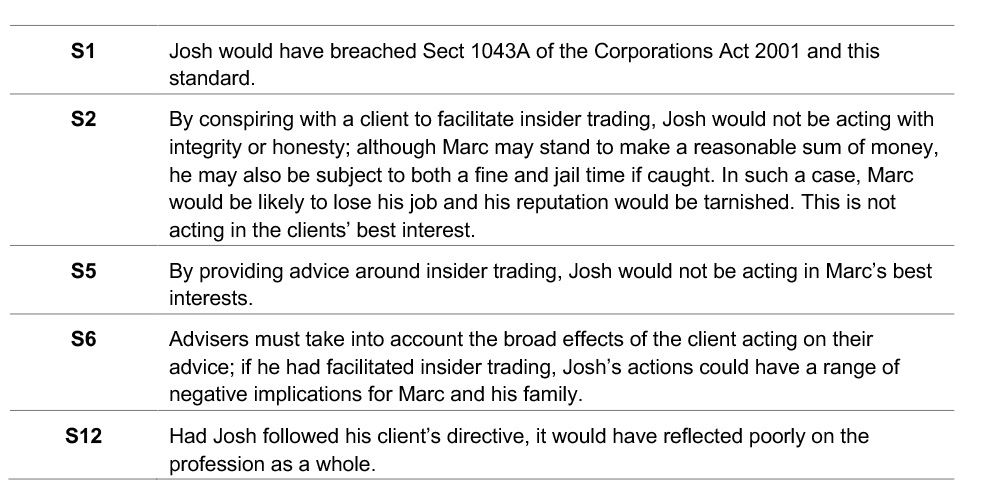

Case study three: Insider trading

Marc is the Chief Financial Officer of ACME Biotech Limited, a small, ASX listed company in the biotech sector. It had been a beneficiary of the Covid pandemic and in the following years, Marc’s salary and benefits package grew substantially.

Marc made an appointment to see his adviser Josh from ACME Investments, who had been looking after his financial advice needs for several years. Josh was curious…Marc usually stuck to his biannual appointment cycle; this appointment was out of the blue and he’d requested to see Josh as soon as possible.

When the two sat down, Josh could see Marc was excited. He told Josh that ACME Biotech had hit the big time and been awarded two large government contracts worth many tens of millions each. As soon as the contracts were signed, the Australian Securities Exchange would be advised, and the market would respond accordingly. A significant jump in the company’s share price was anticipated.

Marc wanted to make money from this anticipated rise in the share price. He asked Josh how he could structure things so he and his family could invest and benefit. He had hopes of buying a holiday home with the profits and wanted to benefit from his hard work on negotiating the contracts.

Josh has two choices.

- He explains to Marc that this is insider trading and in contravention of both the law and the Code of Ethics to which he is bound, or

- He finds a way to help Marc buy shares in the company and works out a post announcement sales plan to realise the anticipated profit and purchase his holiday home.

Josh chooses the first option. If he had chosen option two, he would have potentially breached the following standards in the Code:

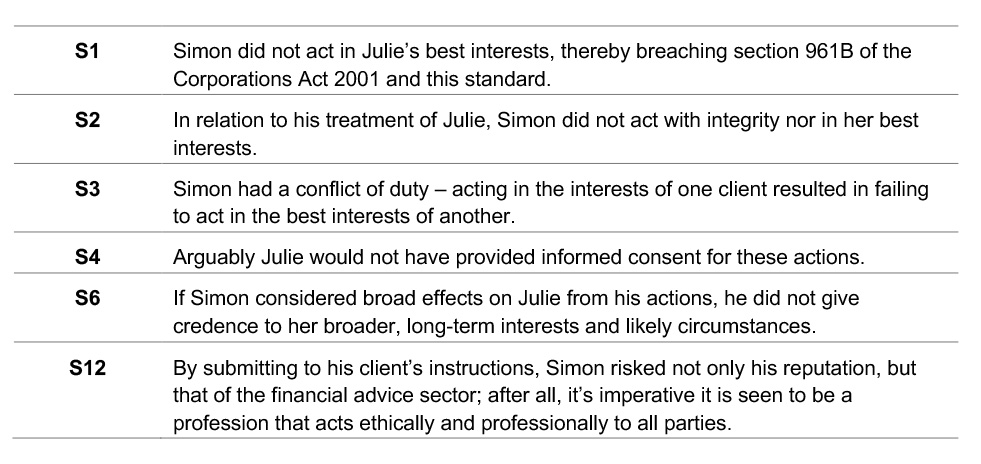

Case study four: When divorce turns two clients to one

Julie and Carl have been married for 22 years and have two children. As a partner in a law firm, Carl works long hours; Julie was a stay home wife and mother. Carl was able to take advantage of income splitting with Julie and paid her an annual ‘salary’ of $42,000.

Carl and Julie’s financial adviser, Simon, worked with ACME Financial Planning. Simon and Carl had been at school together and played football for the ‘old boys’ school team for many years. Their sons now continue the tradition, and both Carl and Simon remain heavily involved with the club.

Most of the meetings with Simon were attended solely by Carl; while Julie occasionally attended a meeting, she had little to do with the financial decisions and typically signed what she was asked to.

When it became apparent that he and Julie were going to separate, Carl instructed Simon to set up a managed account in his name only. Carl realised that Julie would be likely to be awarded a larger than 50 percent portion of their family home, so he withdrew $650,000 of equity from the home and deposited it into his managed account. He and Simon then worked out the best way of investing the money, so it was as inaccessible as possible.

While Simon was acting per Carl’s instructions and in what he believed was his friend’s best interests, Julie was also his client until such time she was advised otherwise. Facilitating transactions and investments without her knowledge (and to her detriment) potentially breached the following standards of the Code:

Financial advisers are required to act ethically and in the best interests of their clients at all times. The decisions and recommendations they make daily impact their clients’ lives, both today and in the future. Ethics in financial advice is an integral part of a complex system, involving regulation, education, professional bodies and the integrity of each adviser and licensee working in the industry.

When faced with an improper request from a client or prospect, two key principles will serve you well. Firstly, always present a professional image that reflects your integrity and the values of both you and your company. Secondly, respond clearly and confidently to improper or unethical requests.

Dealing with ethical dilemmas can be challenging. Seek advice from your peers, practice manager or licensee. Maintain your ethical awareness and practice sound judgment as you decide on the best course of action. By doing so, you ensure that you uphold the highest standards of professionalism and protect the trust placed in you by your clients.

———