Client first – ethics and best interests

What is the intersection between meeting clients’ best interests obligations and running an ethical advice practice?

When providing financial advice, acting in a client’s best interests isn’t just a regulatory requirement, it is the cornerstone of a trusting and successful advisory relationship. This article, proudly sponsored by GSFM, examines the strong links between clients’ best interests and running an ethical advice practice.

Consumers seek financial guidance from professional financial advisers to navigate complex decisions that can significantly impact their ability to meet their shorter and longer term financial and lifestyle goals. They rely on the expertise and integrity of their advisers to provide advice that aligns with their unique objectives, values and circumstances, and establishes them to thrive in future years. Prioritising each client’s best interests builds trust, fosters long-term relationships and enhances the adviser’s reputation. In an industry where trust and confidence are crucial, putting clients first is not only the ethical thing to do but also the foundation for client satisfaction and sustainable business growth.

The best interests duty, as defined by the Australian Corporations Act 2001, requires financial advisers to act in the best interests of their clients when providing personal financial advice. This duty is enshrined in Section 961B of the Act and requires that advisers must take reasonable steps to ensure that the advice they provide is appropriate to the client’s individual circumstances, including their financial situation, needs, and objectives.

The best interests duty is designed to ensure that financial advisers provide advice that is objective, unbiased and is tailored to the client’s needs. This fosters trust and confidence in the financial advisory industry and is of critical importance in the regulatory framework that governs the delivery of financial advice.

Best interests obligations

ASIC describes the best interests duty and related obligations as:

“…designed to ensure that retail clients receive advice that meets their objectives, financial situation and needs, and that you act in the best interests of your clients when providing advice.”

In financial planning, it can be distilled into acting in the client’s best interests at all times, acting with competence, honesty, integrity and fairness. In summary, the way any one of us would expect to be treated by a professional service provider.

The Future of Financial Advice Reforms (FOFA) introduced an amendment to the Corporations Act 2001, one which enshrined the best interest duty into law. It was an extension of the existing fiduciary duty owed to clients by financial advisers, the one which covered the need to ‘know your client’, know the products you recommend and always act with the interests of those clients front and centre.

This amendment included that the ultimate responsibility for complying with the duty to act in the client’s best interests falls to the licensee, who will be financially responsible for any breaches. Individual authorised representatives of that licensee may be subject to administrative penalties, such as banning and disqualification orders.

Section 961B of the Corporations Act 2001 (as amended) lists the steps an adviser must take to satisfy the ‘best interests’ standard. In summary, these are[1]:

- To identify the client’s financial situation, objectives and needs; these should be provided to the adviser by the client.

- To identify the subject matter of the advice sought by the client (whether explicitly or implicitly).

- To identify the client’s relevant circumstances – the objectives, financial situation and needs that would reasonably be considered as relevant to the advice sought on the identified subject matter (i.e. the client’s relevant circumstances).

- To ensure this information is complete and correct and make reasonable enquiries should be made if gaps or inconsistencies are apparent.

- To assess whether you have the expertise required to provide the client advice on the subject matter sought and, if not, declined to provide the advice.

- When considering the advice sought, whether it would be reasonable to consider recommending a financial product. If a financial product is deemed relevant, a recommendation should only be made after thoroughly investigating the most appropriate products relevant to the client’s circumstances.

- When advising the client, the financial adviser must base all judgements on the client’s relevant circumstances.

- Take any other step that, at the time the advice is provided, would reasonably be regarded as being in the best interests of the client, given the client’s relevant circumstances.

Number eight is a last catch-all statement that encapsulates the spirit of the legislation; regardless of the client’s requirements, the advice must be underpinned by knowledge of the client and their circumstances. While the best interest duty applies to retail clients, a similar fiduciary duty is required for dealings with wholesale clients. To meet obligations under section 961B of the Corporations Act 2001, is indisputably to act ethically in all dealings with clients.

A failure to act in a client’s best interests would not only breach section 961B of the Corporations Act 2001, it would also breach several of standards in the Financial Planners and Advisers Code of Ethics (Code) notably:

Best interests and the ethical practice

In any profession, most people set out to act ethically. And while ethical practice is not always black and white, putting the client first and acting in their best interests is generally clear cut.

The best interests duty is a fundamental ethical obligation for financial advisers and is enshrined in the Code of Ethics (figure one). It requires advisers to prioritise their clients’ needs and interests above their own or those of their practice or licensee. This duty ensures that any advice given is appropriate, tailored to the client’s financial situation, goals, preferences, and is devoid of conflicts of interest.

Acting in the best interests of clients is a cornerstone of ethical financial advice. This legal requirement ensures that financial advisers prioritise the needs and goals of their clients above all else when providing advice. Financial decisions often have long-term impacts on individuals’ lives, so clients rely on their advisers to provide guidance that genuinely benefits their financial wellbeing.

The importance of the best interests duty also extends to protecting clients from conflicts of interest and potential exploitation. The obligation to act in the client’s best interests ensures that recommendations are made based solely on what is most appropriate for the client’s situation. This protection fosters confidence in the financial advice industry and ensures that clients can make informed decisions based on unbiased recommendations.

Acting ethically and in every client’s best interests strengthens the integrity of the financial services industry as a whole. When advisers consistently put their clients’ interests first, it reduces the risk of misconduct and enhances the reputation of the profession. It also ensures that the advice provided is aligned with broader regulatory goals of consumer protection, fairness and transparency.

Simply, acting in clients’ best interests means being transparent, honest and diligent in all interactions with clients, thoroughly understanding their circumstances and recommending strategies and where appropriate, financial products, that genuinely benefit them. It also involves advisers continuously educating themselves to provide competent advice and adhering to regulatory standards and professional guidelines.

While enshrined in law and in the Code of Ethics, there are actions all advisers can take to support practice-wide ethical behaviour, maintain a strong ethical business culture and ensure client’s best interests always come first. These include:

- Establish a practice-wide code of conduct, one which encapsulates your business’s values and the Code of Ethics. Your code of conduct should set clear expectations about your employees’ behaviour when carrying out their duties, including a focus on putting each client’s best interests first, always. You need to ensure all staff understand each of the twelve standards in the Code of Ethics and how each standard may specifically intersect their role – and how each may affect the way they put their clients’ interests first.

- Lead by example. Employees will look to the key individuals in the practice to understand what conduct is and isn’t acceptable. Senior advisers and personnel will set the tone for ethics in the practice; accordingly, they need to demonstrate your business’s code of conduct in all they say and do. When the team sees you putting your clients’ best interests first, they are more likely to do the same.

- Workplace training is a positive way to ensure all staff understand both the practice’s values and the obligations of the Code. Provide regular training sessions on ethical behaviour, regulatory compliance, conflict of interest and integrity. Training should cover both theoretical aspects and practical, real-world scenarios. The use of case studies to discuss scenarios where a client’s best interests may be compromised reinforce the practice’s standards of conduct and clarify behaviours and practices that do and don’t work within your code of conduct. Workshops and role-playing exercises can be used to simulate situations where ethical dilemmas may arise and guide employees on how to resolve them according to the Code of Ethics. Training could also be incorporated as part of regular team meeting and incorporate a variety of case studies that could address common issues that arise across the financial planning industry. The AFCA website[2] is a good source of cases and decisions made by AFCA to form the basis of discussion. You can search specifically for decisions related to failing to act in a client’s best interests, as well as other issues not aligned with ethical behaviour. It’s important that ethics training is not a one off; ideally, training should teach team members to make good decisions that are compliant with the law and consistent with your practice’s values.

- Ethical behaviour should be a key performance indicator (KPI); by reinforcing and potentially rewarding staff for embodying your values, adhering to your practice’s code of conduct and behaving in a way that makes ethical behaviour central to their work will create an ethical practice. Although a values driven KPI can be harder to quantify than one with specific and measurable outcomes, it will highlight to staff the importance of values and ethics to your business.

- Ensure clear communication channels within your practice. Encourage open dialogue to create a culture of transparency where employees can discuss ethical concerns without fear of retaliation. Create regular feedback loops, whereby employees provide honest feedback about the processes, conversations and client interactions to ensure you are aware of all issues as they arise. Surprises can potentially compromise your business. Bringing your peers on the ethical journey is important. The licensee and adviser will carry the responsibility of any breach of the Code, but by implementing strategies such as those outlined above can help mitigate the risk of a breaching ethical standards.

- Enforce a zero-tolerance policy for ethical violations to demonstrate they are taken seriously. Consider relevant disciplinary actions for employees who engage in unethical behaviour and apply it consistently across all levels of the practice to maintain credibility and fairness.

By fostering a culture of integrity, education, transparency, and accountability, you can create an environment where all colleagues are aligned with the ethical standards needed to run a successful and trustworthy financial advice business, one where each and every client’s best interests always come first.

Case studies

The following case studies are based on real events; however, the names of people and organisations have been changed, and some details altered. The case studies have been drawn from ASIC or AFCA (or its predecessor organisation). For each, potential breaches of the Code of Ethics are identified. These case studies represent examples of those that would be of value for the business to discuss as part of its workplace training.

Case study one: Failure to act in clients’ best interests #1

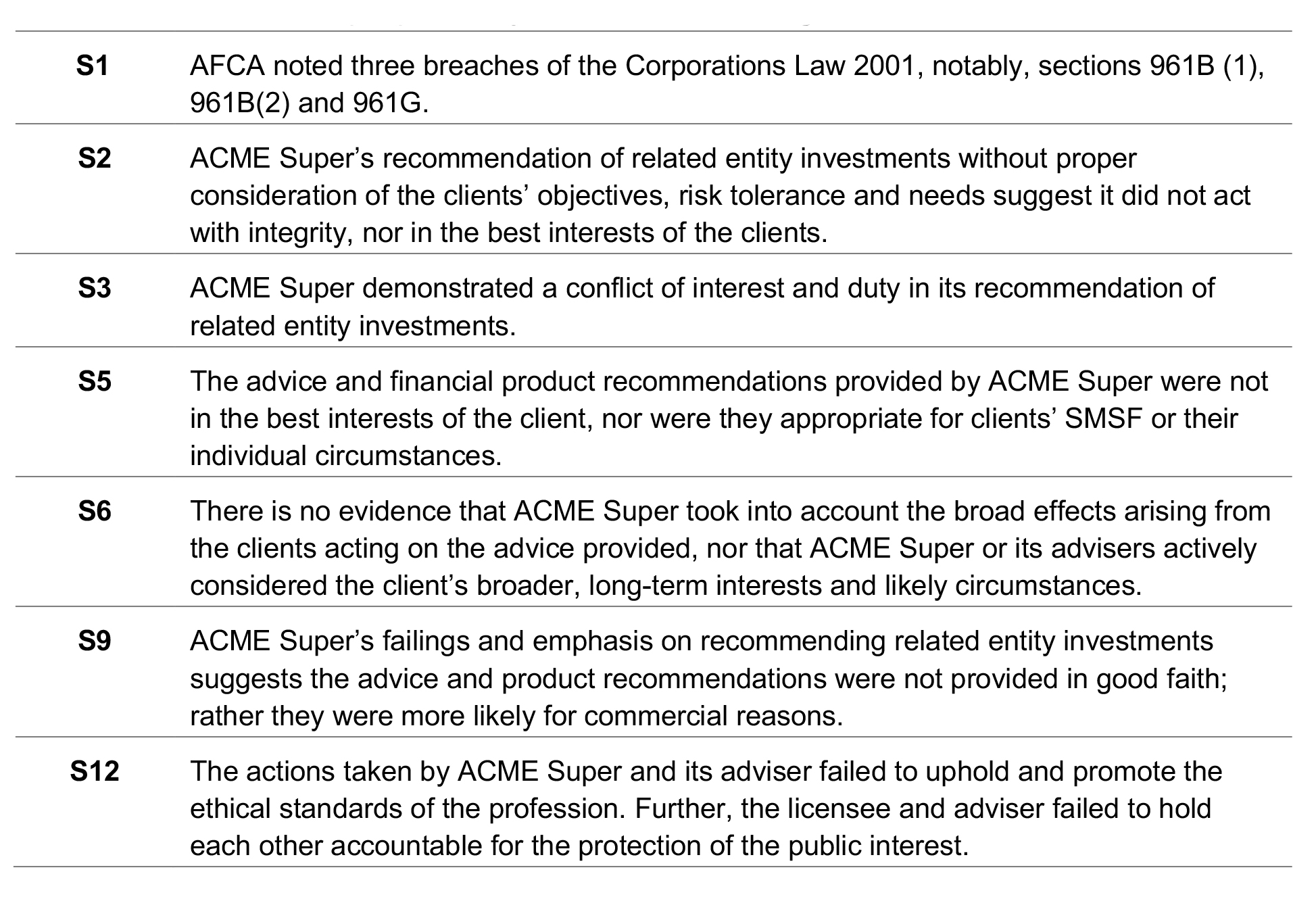

The complainants are corporate trustees of a self-managed superannuation fund (SMSF), directors Joan and Peter. The couple sought and received personal advice from the financial firm ACME Super. They were a client of ACME Super from March 2011 to January 2022, during which time the couple received advice on managing the SMSF’s investments.

Joan and Peter claimed that ACME Super’s advice was not appropriate because the financial firm was conflicted in making its investment recommendations; the SMSF has suffered significant losses as a result.

An AFCA investigation found that ACME Super did not provide appropriate advice, nor did it act in the complainant’s best interests. Further, the firm:

- failed to provide advice within the risk parameters it set

- failed to diversify the portfolio’s “growth” assets, with the portfolio too heavily weighted towards property

- recommended an overly high proportion of related entity investments without justification.

Further, ACME Super failed to establish that it prioritised the complainant’s interests over its own. The proportion of related entity investments compared to non-related entity investments was excessive. These related entity investments recommended by the firm carried more risk than the complainant understood or needed. Finally, the fees were also excessive when compared to alternative investment products.

AFCA found that the financial firm’s failure to provide appropriate advice and act in the complainant’s best interests resulted in Joan and Peter’s SMSF being $875,435 worse off.

Accordingly, AFCA’s determination was that in the circumstances, ACME Super should compensate the complainants for the losses incurred because of its advisers’ inappropriate advice and was required to pay them $542,500 in compensation, plus interest. Note: this reparation represents the maximum AFCA can award for this complaint.

It was noted in the determination that ACME Super failed to act in the best interests of their clients and breached the following sections of the Corporations Act 2001 – 961B(1) best interests duty; 961B(2) failure to demonstrate best interests by following ‘safe harbour’ steps; 961G that it would be reasonable to conclude that the advice is appropriate to the client had the provider satisfied the best interests duty.

The adviser and ACME Super potentially breached the following standards in the code.

Case study two: Failure to act in clients’ best interests #2

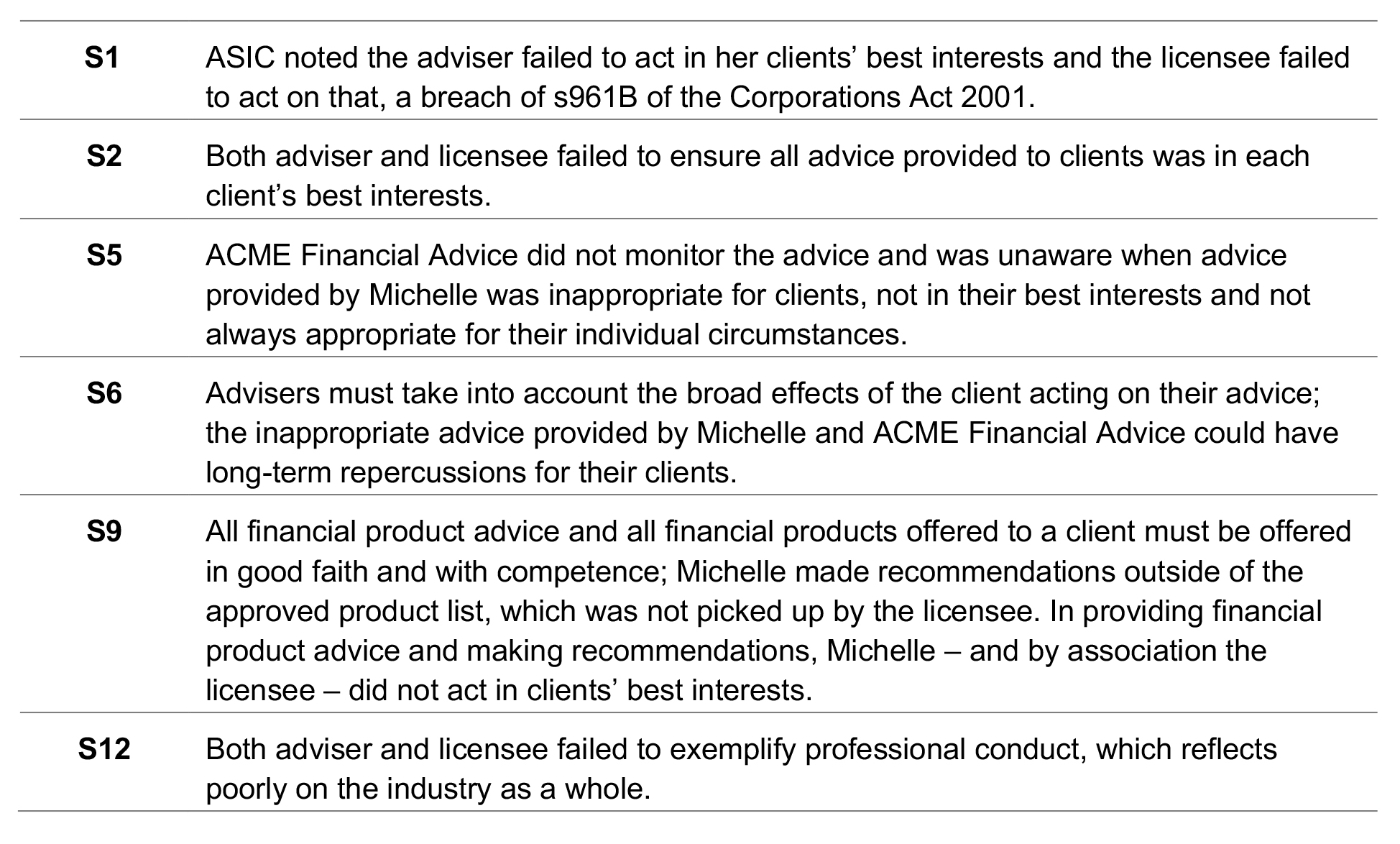

Following several client complaints, ASIC commenced an investigation into adviser Michelle, an authorised representative of ACME Financial Advice. An ASIC investigation found Michelle had breached her best interests obligations by providing clients with inappropriate advice and failing to put her clients’ interests first.

Michelle’s case was heard in the Federal Court, where it was found that ACME Financial Advice failed to take reasonable steps to ensure that Michelle provided appropriate advice to clients, acted in the clients’ best interests and put the clients’ interests ahead of her own. The Court found ACME Financial Advice did not have adequate processes to monitor the advice provided by their authorised representative. They could not identify when these advisers avoided advice quality checks or recommended non-approved financial products. The Court described these as ‘serious flaws’ that should have been apparent to the licensee.

Commenting on the case, an ASIC representative stated: ‘Financial advice licensees need to understand that they can be liable if their advisers do not act in the best interests of their clients and do not prioritise their clients’ interests over their own.’

In this case, the licensee ACME Financial Advice was potentially in breach of the following FASEA standards:

Case study three – inappropriate trading of client MDA

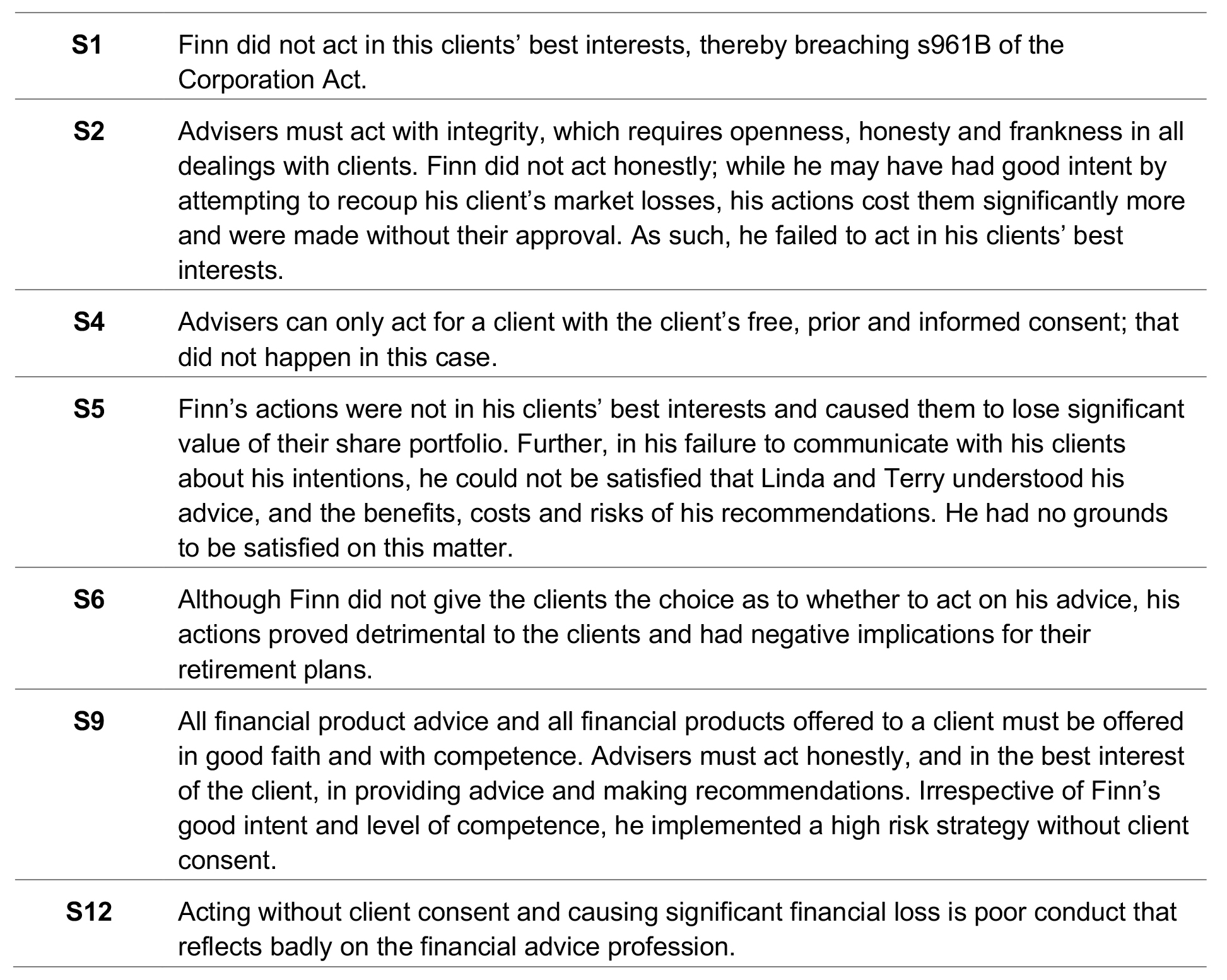

Linda and Terry had been clients of ACME Advice for 15 years. They are in their late 50s, both work, and had planned their retirement for when Terry reached age 65 and Linda age 63. In 2019, their adviser retired and was replaced by Finn, a new graduate with an impressive set of academic qualifications.

Linda and Terry were advised to establish a Managed Discretionary Account (MDA) for their investments. Finn explained the benefits of an MDA to their financial situation and life stage, and they agreed to take his advice.

Over the following years, they witnessed periods of market volatility but were not too concerned. Although they had a significant equity portfolio, they were prepared to wear a high degree of risk and were confident their equity portfolio would gain ground before they retired. However, they kept an eye on it and were in regular telephone and email contact with Finn.

During a period of sustained market volatility and portfolio drawdowns, Terry expressed mild concern that the portfolio might not recover before they retired and needed to draw on the capital.

Several days later, Terry looked at the account and saw some trades – and a significant deficit – that concerned him. In an attempt to build up the portfolio, without consulting with his clients, licensee or fellow advisers, Finn conducted trades in breach of the MDA’s investment policy, namely:

- trades in naked options (naked trades); and

- trades which exceed 5% of the complainant’s trading capital in any one trade (excess capital trades).

The excess capital trades caused a portfolio loss of $127,000. The portfolio also suffered a loss of $53,000 because of the trades in naked options.

Linda and Terry stated they would not have approved the investment strategy implemented by Finn. From the details provided in the case study, Finn potentially breached the following of the Code’s standards.

Case study four: Referral fees

Paul and Luke had been to school together and then attended the same NSW university. Paul completed a Financial Planning degree and became an authorised representative of ACME Financial Advice. Luke studied business and decided to move into insurance broking. Once Paul and Luke completed their respective degrees, they decided to set up business together and benefit from the synergies of financial advice and insurance.

The two worked from the same office in Sydney’s eastern suburbs but operated completely separate businesses. Paul’s business was fee for service, whereas Luke was compensated by upfront and ongoing commissions from the insurance companies with which he wrote business. Both operated within the bounds of the respective laws governing their professions.

Both Paul and Luke were believers in the value of advice and the importance of adequate insurance cover and as such, had an arrangement whereby they would refer clients to one another. They decided such referrals would attract a scaled fee, based on the estimated worth of each individual client over a forward ten year period. Low value clients would be referred at a basic fee of $100 and this fee would scale up to $1,000 for a higher value client.

Paul and Luke each saw an increase in clients – and revenue – as a result of this arrangement. Paul spent more time talking to his clients about the importance of a range of insurance policies, making Luke’s job much easier; it tended to result in clients being more open to a broader range of insurance policies which, in turn, meant more commission for Luke and a higher referral fee for Paul.

While both parties were providing advice and financial product recommendations that were in their client’s best interests, referral paperwork was not updated to include the fee, and clients were not informed verbally. As a result, Paul – bound by the Code of Ethics – potentially breached the following standards.

Acting in a client’s best interests is the cornerstone of any ethical financial advice practice. It fosters trust, builds long-lasting relationships and safeguards the integrity of the profession. An ethical approach ensures that clients are empowered to make informed financial decisions, which ultimately leads to sustainable success for both the client and the business. In a competitive industry, placing client interests first sets ethical financial advisers apart and solidifies their reputation as trusted professionals.

———