Amy Xie Patrick

In a world without bank hybrids, investors should re-consider their income plan, says Pendal’s head of income strategies Amy Xie Patrick.

- Hybrid securities can suffer meaningful shortfalls

- It’s “unwise” to rely solely on hybrid income through all market environments

- Find out more about the Pendal Monthly Income Plus Fund

FOR years, Australian investors have flocked to bank hybrid securities as a cornerstone of income-generating portfolios.

Hybrids — debt instruments issued by banks that can convert to equity in times of trouble — have been popular with everyday investors due to their accessibility.

But investors will soon need to find alternatives, after the Australian Prudential Regulation Authority announced plans to phase them out[1] from 2027 (see more in our recent quarterly update)[2].

ARPA wants to “simplify and improve the effectiveness of bank capital in a crisis” and replace hybrids with “cheaper and more reliable forms of capital that would absorb losses more effectively in times of stress”.

Below we examine whether hybrids truly delivered on their promise to investors — and we discuss an alternative that could help fill the gap.

The myth of defensiveness

Hybrid securities, as their name suggests, sit somewhere between the asset classes of fixed income and equities.

They serve as one of the first lines of defence in a bank’s capital structures in times of turmoil, and outside of those times pay regular coupons, like bonds.

Though the coupon feature means they are often classed as “defensive”, their purpose as a capital instrument makes them inherently ill-suited to serving a defensive role in portfolios.

Through multiple market cycles, bank hybrid securities globally have exhibited a positive correlation with equity markets.

When things are fine, these securities pay their coupons and may even deliver some mark-to-market capital gains should their credit spreads tighten.

In times of severe market stress, hybrids can behave more like equities than bonds. During the collapse of Credit Suisse in April 2023, the bank’s hybrid securities were written down to zero – a worse outcome than Credit Suisse shares.

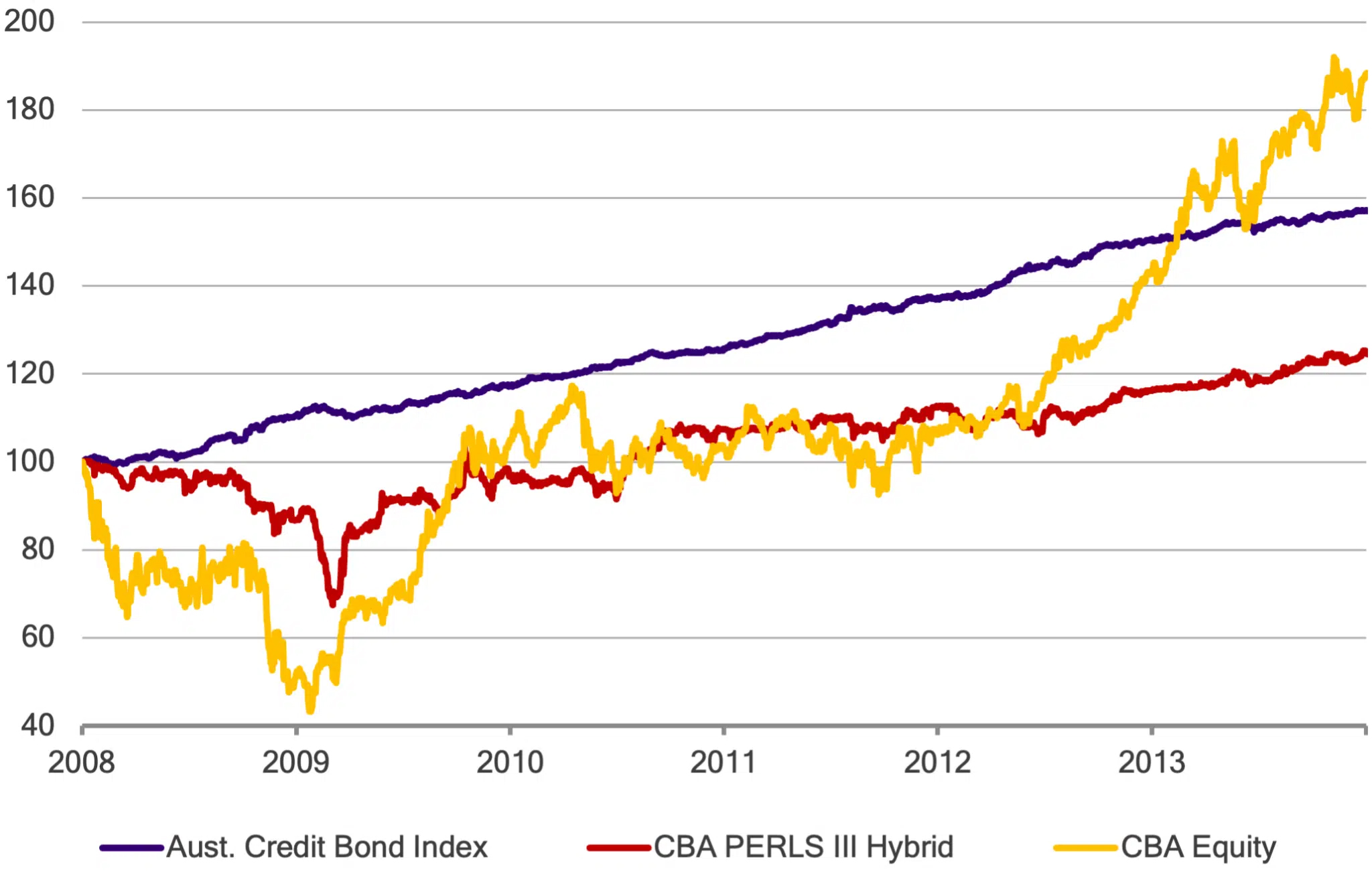

As the figure 1 graph below highlights, using the example of CBA, the long-term performance of hybrids has lagged even more senior bonds.

These securities tend to behave like high-quality bonds when all is fine, and like equities when all is not.

The capped potential for capital growth in hybrid securities means they are not capable of generating levels of reward commensurate with the likely volatility investors will experience along the way.

Figure 1: All the risk without the reward

Long-term returns of CBA equity, CBA hybrids (“Perls”) and major bank senior bonds

Source: Bloomberg, Pendal

Exchange-traded ≠ liquidity

Another selling point of hybrids has been their exchange-traded status.

Many investors assume this means that hybrids can be easily bought and sold.

In reality, market liquidity for hybrids has always been contingent upon the ability of brokers to match buyers and sellers in the market. In such a retail-dominated asset class, costly buy-sell spreads can also be a feature.

The fallacy that “listed equals liquid” has been exposed in times of crisis, when the exit doors for hybrids can become very narrow.

Repeatable income? Not so fast

Since hybrids come with a higher risk of capital loss than senior bonds, these securities compensate investors with a higher credit spread, translating ultimately into higher coupons than more senior bonds.

Unlike senior bonds, hybrid coupons can be reduced, delayed or completely switched off. This feature of hybrid securities is a benefit to the issuers as it offers a lifeline in times of need.

For investors, it’s a reminder that the higher income potential in hybrids is far from guaranteed.

Figure 2: More risk should command more reward

Risk and reliability of income through the bank capital structure

While Australian bank hybrids have not experienced any volatility in coupon payments in recent history, both the events of the Credit Suisse crisis in 2023 and that of many other European banks during the European Sovereign Crisis in 2012 have shown that it has been unwise to rely solely on income from hybrids through all market environments – particularly considering that the majority of income-seeking investors tend to be conservative in their risk tolerance.

A smarter way to use the capital structure

We’ve uncovered that hybrid securities suffer meaningful shortfalls.

Their contractual terms allow issuers to skip coupon payments. Investors’ ability to access their capital is likely to be variable and limited when they most need it. Their potential for capital growth does not compensate for the meaningful volatility that investors can experience along the way.

But what if there has always been a smarter way to use the capital structure?

Figure 3 expands on the bank capital structure to a broader set of asset types. More importantly, the diagram looks at what jobs these assets are good at doing that could be important to any investor.

Figure 3: Asset utility through the eyes of the investor

The key revelations from Figure 3 are as follows:

- Different assets are good at doing different things

- No single asset class can satisfy all investment objectives

- Hybrids satisfy none of the basic requirements

The idea that different asset types need to be employed may seem daunting, but Figure 4 illustrates that the idea is simple.

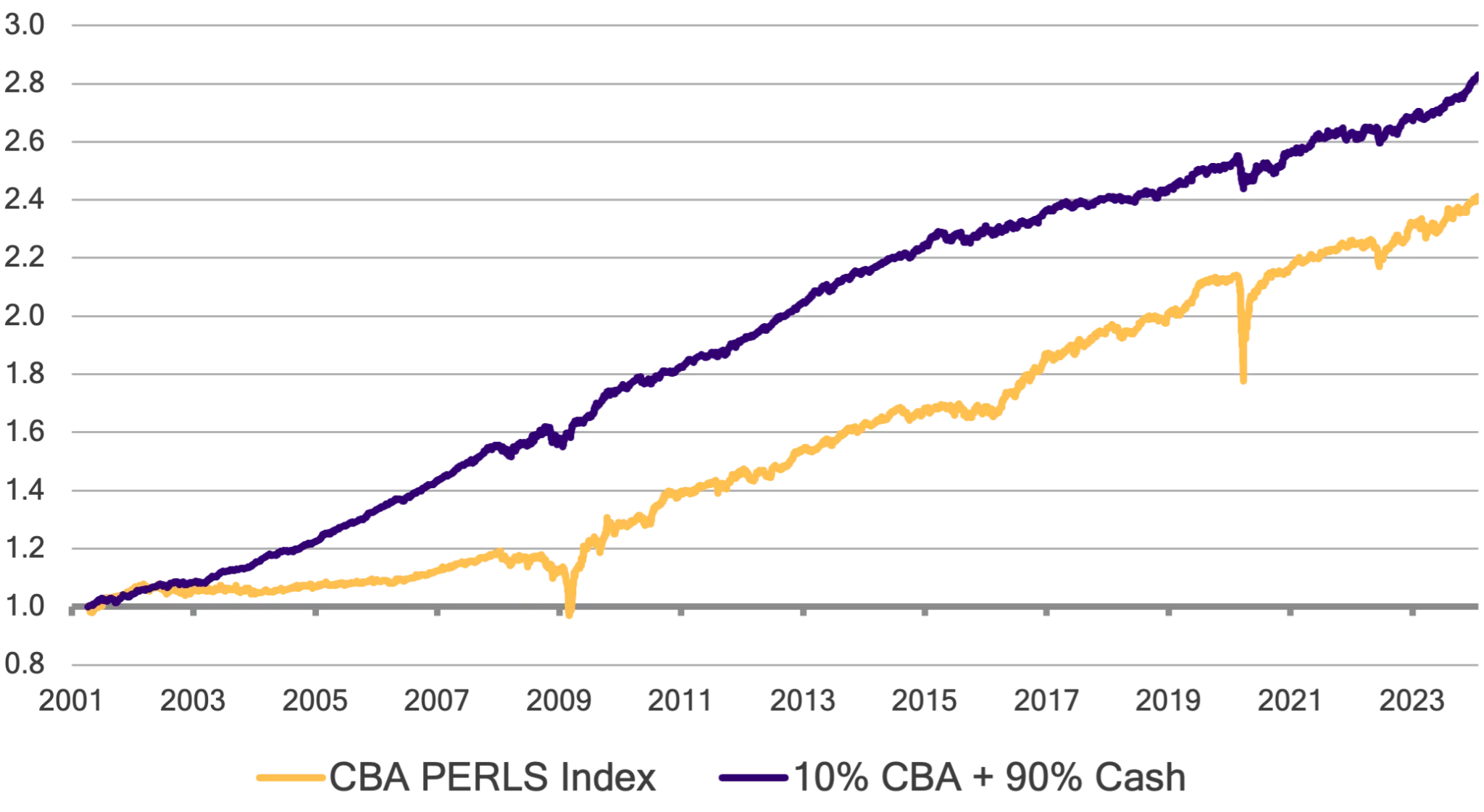

In the graph below, we compare the long-term return outcomes of holding CBA hybrids, versus holding most of your capital in cash and putting only 10% into CBA shares.

Nothing beats equities for generating capital growth. And a cash-heavy portfolio has significantly diluted adverse volatility events along the way.

Figure 4: A little bit of equities goes a long way

Comparing long-term returns of CBA hybrids versus a portfolio of 90% cash and 10% CBA shares

Source: Pendal, Bloomberg

Pendal Monthly Income Plus Fund – a solution for defensive income

As Australian bank hybrids face extinction, our Pendal Monthly Income Plus Fund provides a compelling alternative for investors.

We start from investment objectives and map them to the assets that have a proven track record of delivering against those objectives.

That means we don’t have to accept market narratives about hybrids (or any other asset types) that have not been entirely accurate.

We don’t have to run for narrowing exits when others stampede. And we don’t have to face a mismatch between the liquidity we offer our investors versus the liquidity we are able to access in the market.

The components of the strategy are simple.

We use high-quality investment grade bonds to generate income. We actively allocate to equities to help our investors’ capital grow, with a track record of avoiding market chaos.

And we use government bonds or interest rate exposure more broadly to manage the portfolio through the rates cycle.

Since the portfolio is 100% Australian, investors also get a healthy franking credit benefit through the portfolio’s equities exposure. And since the portfolio is 100% liquid, investors are also able to access daily liquidity.

The fund’s strategy recognises the broad aims of all income-seeking investors: a regular, stable and repeatable income stream, and capital growth to help offset the effects of inflation over the medium term.

These aims help ensure that the Fund’s investment objectives align with its investors. These objectives and how we’ve measured against them are illustrated in Figure 5.

Figure 5: Monthly Income Plus Fund: our three investment objectives

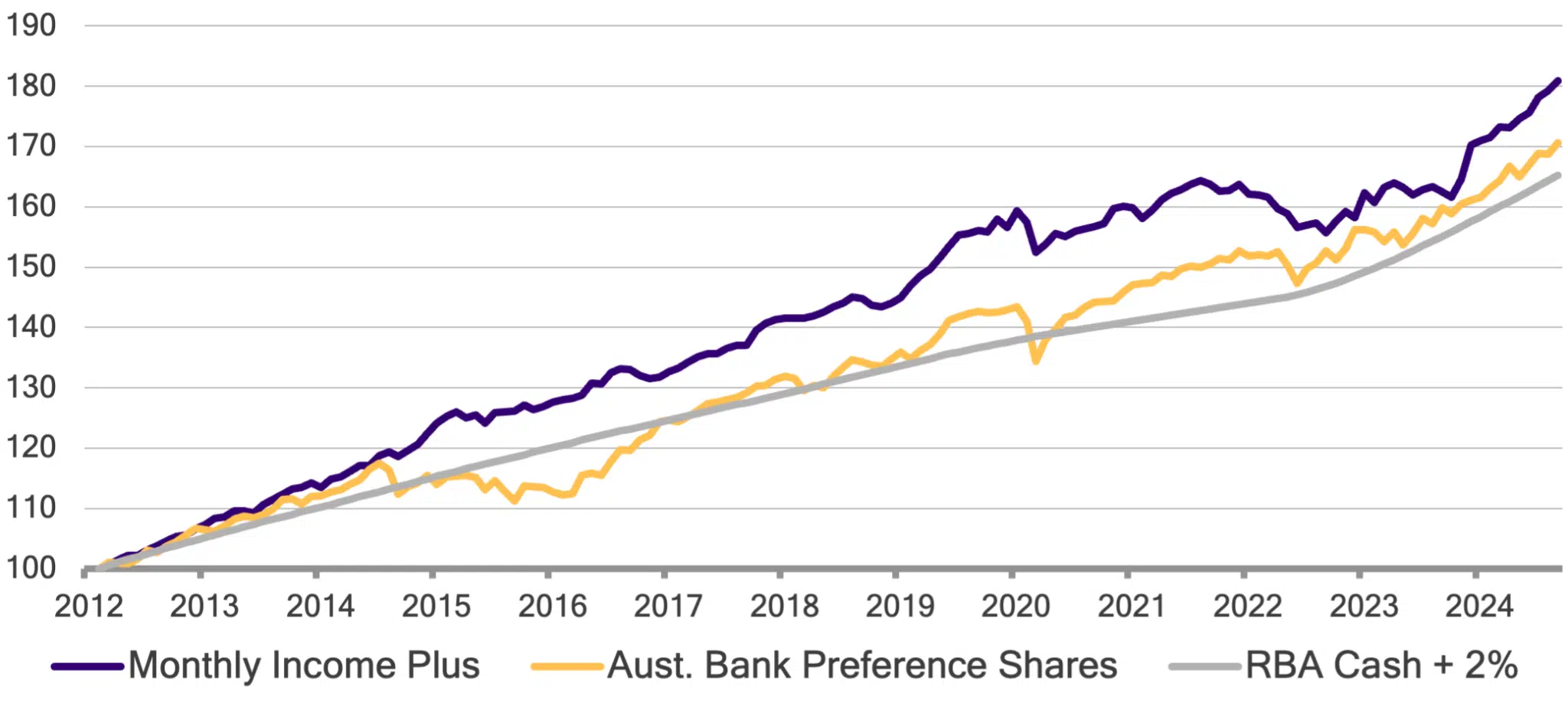

The fund pays distributions monthly and, since inception 15 years ago, has never missed a payment.

While equity and bond markets the world over suffered double-digit losses in 2022, this strategy’s drawdown was limited to 5%.

And alongside regular income with limited drawdowns, the portfolio’s capital has grown every year bar one since inception.

The longer-term track record of the Pendal Monthly Income Plus Fundcan be seen in Figure 6.

Here, we’ve illustrated performance against a hurdle of RBA Cash + 2% (consistent with the risk tolerance of conservative income investors), and against an index of Australian bank preference shares as a generous proxy for hybrid instruments (since shares have greater potential for capital growth than bonds).

The Monthly Income Plus portfolio could have been a replacement for hybrids all along.

Figure 6: Long-term track record

Why wait?

In early September, prior to the APRA announcement, the average gap between bank hybrid and subordinated bond credit spreads tracked around 60 basis points.

This gap was at the tighter end of the historical range of this relationship. Today, this gap stands at less than 10 basis points.

Scarcity has been the main factor behind this compression.

Since banks will no longer be issuing these higher-yielding securities, but investors still like higher yields, the demand has far outstripped supply in recent weeks.

Scarcity, however, does not change the nature of hybrid instruments.

They remain on the frontlines to take losses and cease paying coupons in times of stress.

They will still mature at par (100 cents on the dollar), so cannot offer capital growth to hold-to-maturity investors.

And they will likely be hard to sell (at least at the price investors would like) in times of market turmoil.

It is time to look for better opportunities elsewhere.

——–