Adviser expertise – the value of advice (part three)

Maximise the value of client relationships and your expertise.

The value of financial advice isn’t always easy to measure. While helping clients grow their wealth is certainly important, the true value extends beyond financial returns. This article, sponsored by Russell Investments, explores the value of financial advice.

Financial advisers provide essential support to their clients. They help them to assess and reassess their evolving goals, needs and circumstances. Their role becomes even more critical during periods of transition and uncertainty. In today’s environment, which is characterised by geopolitical instability, market volatility, interest rate uncertainty and the rising cost of living, clients face challenges at both personal and broader economic levels.

Effective wealth management requires a comprehensive approach. This includes an in-depth discovery process, ongoing strategic planning and continuous coordination. This can be especially difficult when emotions run high and uncertainty dominates the conversation.

Advisers who guided their clients through recent periods of market volatility and worked with them to reassess their goals in the face of a myriad of uncertainties can take pride in knowing they delivered real value. To help you articulate that value, a recent paper[1] detailed five factors that measure and quantify the value advisers bring to the table. These factors are:

- appropriate asset allocation

- behavioural coaching

- helping clients through choices and trade offs

- expertise

- tax savvy planning and investing.

Part one and part two of this series examined the importance of appropriate asset allocation and understanding investor behaviour – and your important role as a behavioural coach – as key inputs into the measurement of adviser value.

Asset allocation can have a significant impact on whether a client achieves their investment goals; analysis has found that it drives more than 85 percent[2] of the investment outcome for an individual.

Understanding investor behaviour and related coaching will help you to keep your clients focused on the big picture and to avoid falling prey to common investor emotions during periods of market volatility and general uncertainty. In this article, which is part three of the series, the remaining three factors will be unpacked: helping clients through choices and trade-offs, demonstrating your expertise and tax savvy planning and investment.

Choices and trade-offs

Not everyone understands the extent to which advisers act as financial coaches for clients, guiding them to the best decisions as regulation, social security and their own situations change over time.

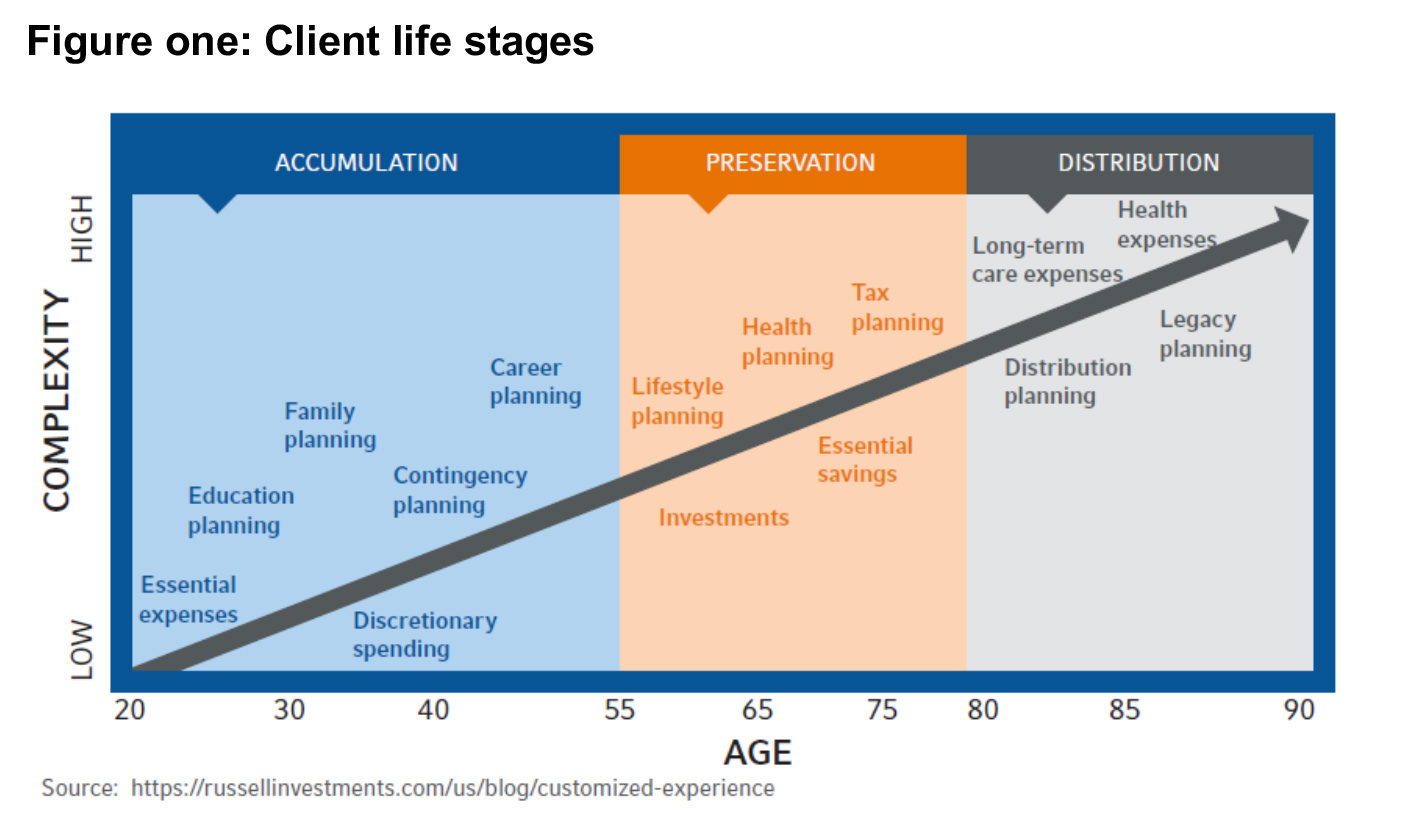

Advisers are there for clients from early adulthood, when they are accumulating assets, to late middle age when they are planning retirement. Advice flows through to older age, when care requirements and funding may be significant. The number of people entering the latter category dominates headlines with the number of Australians aged 65 and over forecast to more than double over the next 40 years[3].

However, it’s not just older Australians who must juggle difficult life decisions. Younger generations are increasingly faced with trade-offs that may be necessary to achieve their long-term goals, given the rising cost of living and housing and for many, HECs debts to service.

Quarterly increases in living costs for employee households – those whose primary source of income is salary or wages – have been higher than the Consumer Price Index since September 2022. Rising mortgage interest rates hit this group hardest, jumping by seven percent in the March quarter as more people rolled over from fixed to variable mortgages and following a Reserve Bank of Australia rate hike in November last year[4].

In such a difficult environment, advisers can reinforce the benefits of implementing financial plans early in life and then identify opportunities or compromises to achieve the desired outcome.

In 2024, this might include advice to invest tax cuts, in superannuation or elsewhere, or to use cash freed up by the Federal government’s energy bill relief to maintain dollar cost averaging into investments.

Such decisions are indicative of the choices and trade-offs that a broad cross section of the community faces. For example:

- Single retirees, particularly women, can be significantly underfunded for retirement and at risk of losing their homes at a later age.

- Younger generations have the advantage of higher compulsory super payments than their parents but must grapple with the increased difficulty of buying a home and other costs such as HECS repayments.

- The so-called sandwich generation must juggle the needs of elderly parents with those of their own children – including sometimes paying for a parent’s aged care costs or forgoing an inheritance to do so.

- Older parents can be faced with ‘impatient inheritors’ – adult children or grandchildren who want a bequest early.

- The so-called ‘bank of mum and dad’ has grown rapidly, as adult children ask parents to fund mortgage deposits. Some estimates suggest ‘the bank’ has seen the transfer of $2.7 billion over the past year[5]. Alternatively, parents are allowing their offspring to live at home longer to save more or to help them meet living expenses.

- Grandparents are more often pitching in to support grandchildren, by providing childcare or funding private education.

- Second marriages can cause family disputes unless there is an extra layer of estate planning that caters for two sets of children.

- Downsizers, whether couples or singles, have a range of options to consider – including downsizer contributions to super.

Each of these scenarios can require detailed arrangements to achieve an optimal outcome and ensure family relationships aren’t fractured.

Couples, for example, can be encouraged to adopt strategies that give them a degree of financial independence within a relationship – so that neither is left without assets if their partnership ultimately breaks down.

Advisers can assist in striking loan agreements for parents providing mortgage deposits to adult children. By working closely with other specialists such as lawyers and accountants, they can develop solutions that protect the interests of clients. This process includes explaining implications which a lay person may not contemplate, helping to avoid situations in which important decisions are put aside or made incorrectly.

Even if the above scenarios are not applicable, each client has their own unique circumstances, preferences and considerations, all of which require countless decisions over a lifetime.

Things to consider include:

Personal circumstances

When young and accumulating assets, people tend to focus on the big picture by establishing a career, buying a home and in many cases, raising a family. As they move through life, there may be school fees to factor in and new priorities that arise.

As clients near retirement and enter the preservation stage, building their retirement savings, as well as their own health and that of their parents, increase in importance. It’s also the time that lifestyle goals come to the fore. Finally, the distribution phase can involve decisions related to estate planning and funding for health and long-term aged care.

Personal preferences

Each individual has personal preferences that must be reflected in a financial plan. These may include an appetite for exchange traded funds, an interest in alternative assets or a desire to invest in ESG products.

Advisers can suggest appropriate options and explain any trade-offs required to implement those decisions. For example, they can explain the risks of alternative investments or help price-conscious investors understand that passive investments may be in conflict with ESG principles – and, of course, suggest other ways to achieve their objectives.

When it comes to retirement planning, clients will have a range of preferences. Some might have lifestyle aspirations that include extensive travel, while others may have health concerns and want to ensure they are financially able to meet those costs as they arise.

External considerations

External considerations can have as much impact on financial affairs as personal preference. In 2024, this is clearly seen in the higher interest rates and high inflation that is forcing people to reconsider their financial situations.

It is also evident in the ageing population – in terms of both social security for the elderly and in bequests made to the younger generations. For the former, advisers can ensure elderly clients take advantage of available benefits such as the Commonwealth Seniors Health Card, which provides cheaper prescriptions and medical appointments to those who pass an income test but are not receiving Centrelink benefits. Clients can also check eligibility for lower cost banking and state based seniors’ cards.

A recent report[6] estimates the potential intergenerational wealth transfer in Australia to be close to $5 trillion, significantly more than the $3.5 trillion estimated by the Productivity Commission. For those who inherit assets, an adviser’s role is to craft a strategy that considers both short-term tax impacts and long-term wealth goals.

Articulate and demonstrate expertise

Advisers’ expertise extends beyond financial matters to human behaviour. This latter skill allows them to forge the trusted client relationships that are necessary to deliver on their recommendations. In good times, this is an easier task. Advisers help clients attain the goals that matter most and celebrate their successes with them. But they support clients in difficult times too – providing counsel as people negotiate challenges such as job loss, relationship breakdowns, ill-health and death. This unique combination of technical skill and emotional expertise provides a priceless form of value to clients.

In terms of technical expertise, advisers are at the frontline of the regulatory changes and product innovations that are a constant in the Australian market. They interpret changes to ensure clients both meet their regulatory requirements and seize opportunities as they arise.

The complex superannuation system is an obvious example where professional advice can make a real difference. The 1 July 2024 increase in compulsory super to 11.5% and another hike in concessional and non-concessional super caps are compelling reasons for people still working to revisit their retirement strategies.

Advisers can also reinforce the benefits of super to people who remain sceptical about its benefits by explaining other forms of contributions, such as catch-up contributions, spouse contributions and small business sale contributions.

Additionally, the Melbourne Institute has found that only approximately half of all Australians think their superannuation works well for them. Those most likely to think it worked well were married and outright homeowners. Renters were more likely to think the system doesn’t work well for them[1].

Pre-and post-retirement planning is another example where professional advice can add considerable value and comfort to clients. The impending retirement of most of the Baby Boomer generation – some 5.6 million individuals – means more people than ever need help to establish retirement income streams, make aged care decisions and undertake robust estate planning.

All this requires much more active decision-making than many people ever applied to their default superannuation while working. The decisions involved are not always technical in nature either – each involves a multitude of emotions as people leave the workforce and plan their final decades.

The same applies to Australia’s complex social security system. The available benefits are not just financial as they also offer the emotional security of a government safety net. Advisers can ensure their clients access legitimate entitlements such as childcare rebates or the Age Pension and related entitlements, thereby helping people when they are most vulnerable.

Technical skills only get part of an adviser’s job done – the ability to gain the trust of a client is critical to establishing a successful relationship and achieving the best outcomes for the client. This is where advisers draw on their essential interpersonal skills: empathy, caring and genuine curiosity.

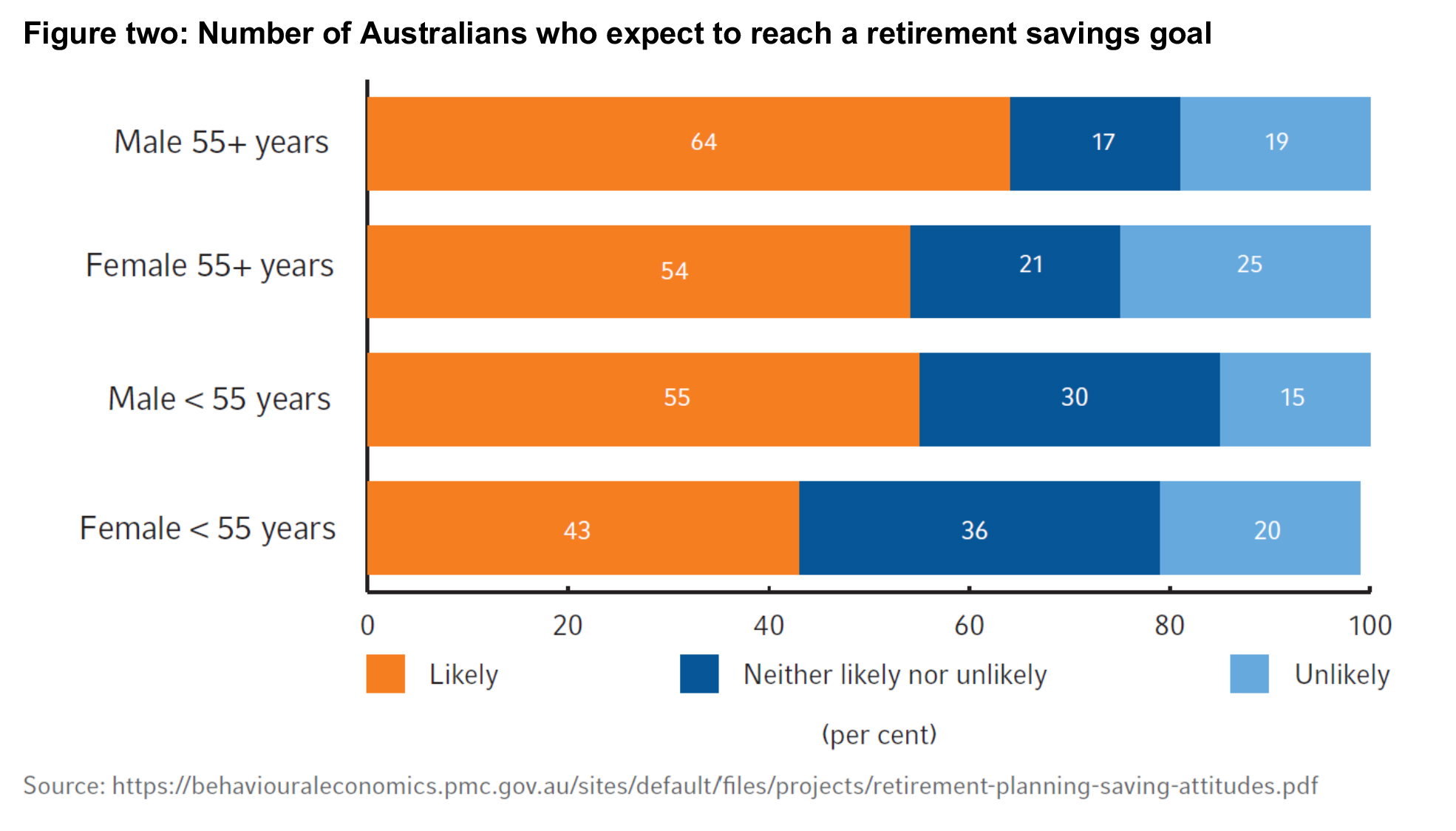

As illustrated in figure two, there’s a large number of Australians who do not expect to reach their retirement savings goals. Financial advisers can play a crucial role to help such individuals with personalised strategies and expert guidance. By offering insights into tax-effective strategies, superannuation options and portfolio diversification, advisers can help their clients make informed decisions that align with – and help them to meet – their long-term objectives.

Elsewhere, understanding financial markets and portfolio construction is key to advisers’ training and experience. Advice teams are consistently researching investment solutions by decoding technical terminology to determine what is appropriate for different clients.

The value of working with an experienced adviser is about tapping into the accumulated expertise they’ve developed over their career. Together with ongoing education, this insight grants them problem-solving skills that can be leveraged by clients at all stages of their lives.

The adviser’s role

Through good times and bad, as clients’ needs evolve an adviser can play a different role when providing expert advice.

Guide

Advisers can shoulder the practical and emotional burden of decision-making for clients in different ways, depending on individual needs. Clients who are overwhelmed by their financial affairs may rely almost entirely on their advisers. Others may opt for more control and instead use advisers as a coach or sounding board.

One example may be a situation in which a couple with $1.2 million in superannuation wanted to gift $100,000 each to their three children on retirement. The gesture, while generous, would reduce their own capital to $900,000 – or even lower if it coincided with a market downturn. An adviser can brainstorm the implications of such a move, balancing the parents’ intentions with the impact on their own standard of living.

Guru

In some situations, advisers stand tall as both an expert and voice of reason. This includes imparting technical knowledge that can sway clients’ decisions or simply using their judgement built over a career to foresee potential consequences of certain actions.

This is perhaps most evident in tax planning and structuring of financial affairs to reach the most optimal outcomes. Alternative retirement savings vehicles to superannuation such as investment bonds and company structures, for example, are worth considering as the proposed implementation of an additional tax on earnings on super balances above $3 million draws closer.

Gladiator

Advisers are well equipped to advocate on a client’s behalf if the need arises. This could mean challenging a refused insurance claim, solving social security hiccups, or managing administration of finances. In all instances, it allows a client and their family to focus on themselves during periods of stress.

Elder financial abuse is an example where advisers can stand up for their clients, preventing the most difficult ‘impatient inheritors’ or others from controlling an aged person’s money and assets. Six in 10 Australians are worried that someone they know will fall victim to this abuse, and in absolute numbers the figure could grow significantly as the population ages[8].

Advisers can maximise the value of their expertise in three key ways:

- Have a clear value proposition, advice philosophy and service model that helps illustrate the service you provide.

- Have existing client case studies that highlight how elements of your expertise helped the client and the outcome you delivered. Share these with new clients so they can better understand the intangible value you deliver.

- Understand the different motivations for seeking advice and have examples to use with new clients that describe how you deliver sometimes intangible, yet highly valued, advice.

Tax savvy planning and investing

Tax expertise sits alongside market knowledge and estate planning as among the central pillars of financial advice. It is required to deliver on all aspects of the services that advisers offer – from superannuation advice to investment strategies and social security assistance. In fact, the importance of tax know-how becomes more critical every year as changes to tax matters and how they intersect with super, social security and other investments is subject to constant change.

Super power

Salary sacrifice is one of the most potent tax-effective investment strategies advisers can implement across a majority of their working-age client base.

A hypothetical investor, Rashmi, provides a good example of its benefits. Her salary is $120,000 and if she sacrifices $16,200 to super[9], she will pay $2,430 in contributions tax instead of $5,184 in income tax[10] . This means an additional $2,754 is invested in her superannuation fund, providing an initial boost that will also increase the power of compounding over time.

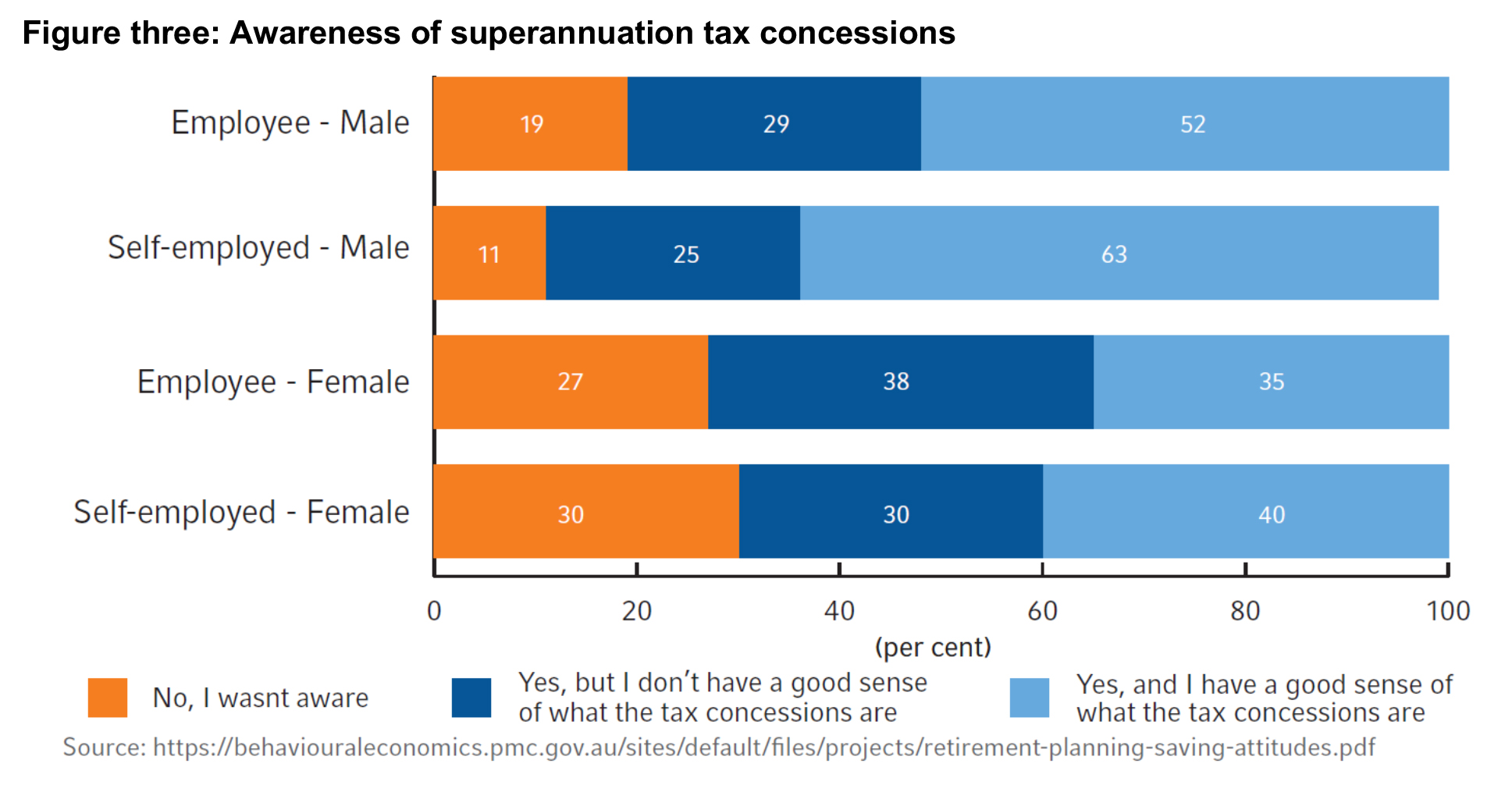

Voluntary contributions to super appear to have increased over time but a survey in advance of the Federal Government’s 2020 Retirement Income Review showed there was still mixed awareness of these benefits. Roughly similar proportions of the self-employed (52 percent) and employees (43 percent) stated they were aware of the tax concessions and understood them (figure three).

Transition to retirement strategies can deliver similar benefits when clients get older. These popular – but sometimes misunderstood strategies – allow people to add extra to super without reducing their take-home pay. This is not just beneficial for anyone who wants to work part-time but can also help people to boost their savings while the cost of living remains high.

But such strategies can prove complicated to arrange without the help of an adviser who can explain the pros and cons – and then implement a chosen course of action.

Advisers can walk clients through a range of sometimes complicated alternatives – explaining both the upsides and downsides – and undertake any implementation on their behalf to ensure the agreed strategy is implemented in an optimal fashion.

Beyond super

Advisers can provide expert guidance on many tax issues outside superannuation. Examples include:

- Investment solutions that optimise results for clients, such as low turnover strategies that minimise capital gains tax, tax minimisation overlays or centralised portfolio management that mitigates inefficient after-tax outcomes.

- Insurance strategies that allow clients to hold policies in superannuation, generating tax benefits that can be reinvested into super or elsewhere.

- Entitlement to social security payments such as childcare rebates, family tax benefits and other concessions that can make a real difference to a household balance sheet.

- Eligibility for small business grants and incentive payments that time-poor proprietors might miss.

The high cost of error

Individuals can easily be caught out by tax rules. It may be because they misinterpret requirements or push boundaries without properly understanding the consequences. There can be onerous penalties in both cases – penalties that astute advisers would foresee and prevent.

The potential for such errors is evident in research for the Australian Taxation Office that found most people recognised the benefits of the tax system – but it was “not top of mind and did not prevent them from being inactive, avoiding or leaving it all with the ‘experts’.”[11].

The fact that only 12 percent of people consider overall tax effectiveness as among the top three considerations when making investments[12] further highlights a lack of understanding, and the important role advisers play in helping to resolve this.

By no means is tax just the realm of the accounting profession. Neither is it limited to the typical items included in an individual’s tax return. Actions advisers can take to maximise value when it comes to tax matters include:

- know each client’s marginal tax rate, tax sensitivities and opportunities

- provide access to solutions that have tax-savvy strategies for your clients

- explain the different tax-smart decisions you include in your advice and ongoing implementation.

By showcasing their expertise, financial advisers can truly solidify their reputation as invaluable partners in managing their clients’ financial affairs. From retirement planning to investment management and beyond, an adviser’s ability to provide tailored solutions not only helps clients meet their financial goals, but also enhances the adviser’s role as a trusted, long-term guide in all aspects of financial wellbeing.

Read the full series:

Asset allocation – the value of advice (part one)

Understanding investor behaviour – the value of advice (part two)

Adviser expertise – the value of advice (part three)