As the global economy continues to evolve and expand, the potential for capital appreciation and increased income is promising.

With the next move in interest rates likely to be downward, the importance of dividend income will be reinforced. And while Australian investors love their income producing blue chips – and the franking credits attached to dividends – income generating global stocks provide an opportunity to diversify clients’ income sources.

At the end of September, Australians had more than $270 billion[1] sitting in cash. While it’s not uncommon for investors to seek the safe haven offered by cash during periods of market volatility, with 12-month term deposit rates at around 4.40 percent[1], the return barely covers inflation. This is why investors – especially self-funded retirees – need to examine all income options available to them.

Why go global for dividends?

Investing in global equities for income offers a range of compelling benefits, particularly for investors who wish to diversify their portfolios and who seek long-term capital growth as well as income. Global equities provide investors with access to a broader set of opportunities beyond the Australian market – even when investing for income.

Advantages of investing in global equities for income include:

- Diversification and risk reduction: by investing in global equities, investors can spread their capital across different geographical regions and sectors. This diversification helps reduce the risk associated with a downturn in any one country or industry. Economic conditions, market cycles and political factors vary from country to country, so when one market underperforms, another might thrive. This balance can help stabilise income and returns over time.

- Access to dividend paying companies: global equities include companies with strong histories of paying dividends, often from industries less represented in the Australian markets. Many large multinational companies, especially in sectors like utilities, healthcare and consumer goods, have consistent dividend policies. This regular income stream is especially attractive for income-focused investors.

- Income and capital growth: many dividend paying companies, particularly those with ample free cash flow that return cash to investors in the form of dividends, also deliver capital growth to investors.

Components of equity returns

The rationale for investment is to grow wealth – ideally, without having to experience any significant losses along the way. Investing in equities has, historically, been the best way to grow wealth.

There are two ways to make money from equities: through capital appreciation of a company’s share price and through dividends paid to investors. The price of each company can be calculated as its earnings times its price/earnings (P/E) multiple. Therefore, any change in a company’s share price results from the change in earnings multiplied by the change in the P/E multiple.

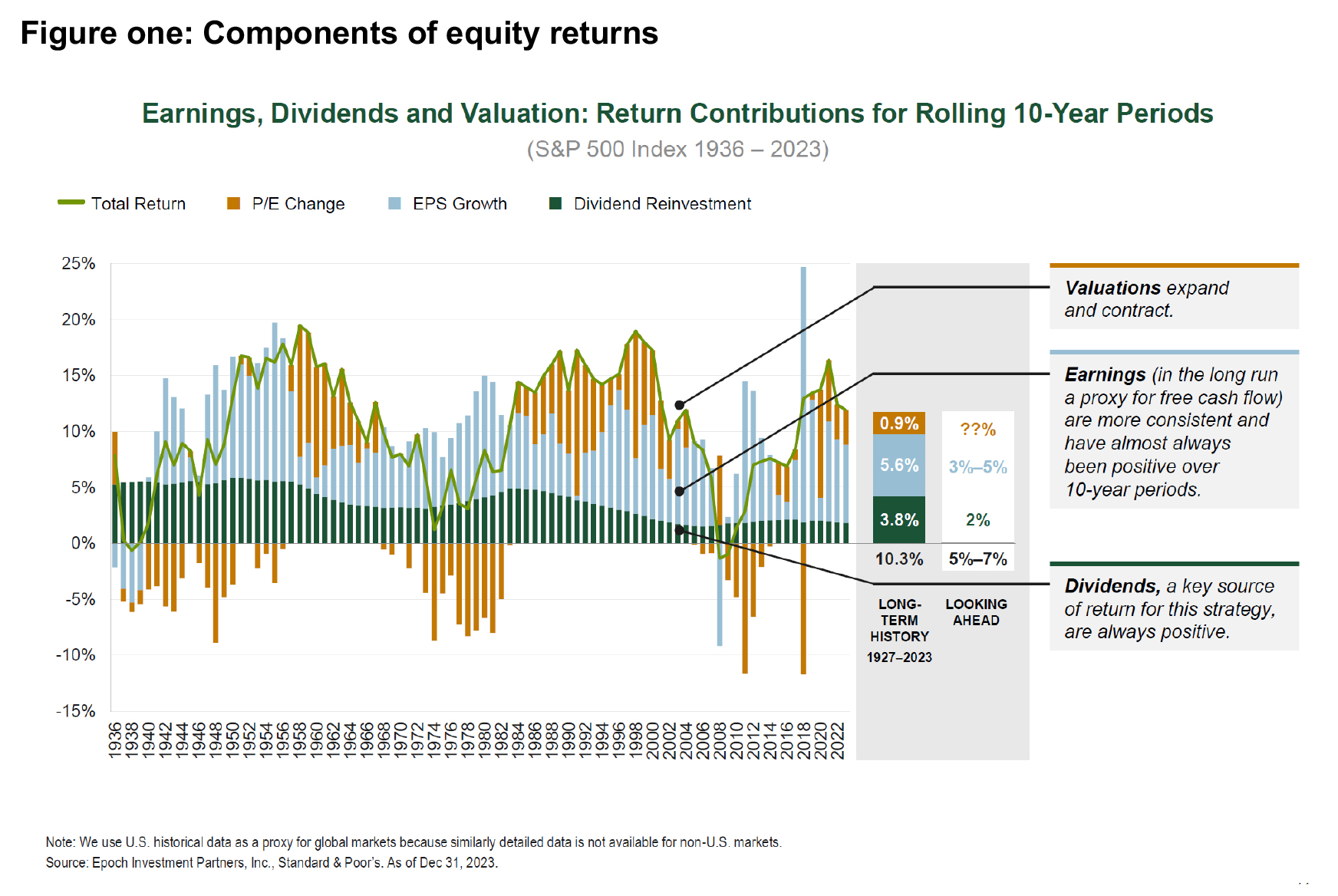

As such, the return from equities is the result of three factors: dividends, the change in earnings and the change in the P/E multiple. Of these, history shows that earnings and dividends are the key drivers for share price valuation (figure one).

Figure one illustrates how the rolling 10-year return for the S&P 500 Index is broken down between those three components going back to the 1930s. Dividends have consistently been a positive contributor in every 10-year time period, and earnings have contributed positively in all but five of the 87 rolling 10-year periods.

The contribution from dividends appears to have decreased starting in the early 1990s; this is due to regulatory changes made ten years earlier which made share buybacks an attractive and tax-efficient alternative to cash dividends. Consequently, companies increasingly used share buybacks as a mechanism for returning cash to shareholders.

Because buybacks reduce the outstanding share count, they tend to drive up earnings per share, so some of what used to show up in this analysis as the contribution of dividends has more recently been transferred to the earnings contribution.

Of particular note, it is exceptionally rare for one component to be the dominant driver of returns and even more rare for that component to be the company’s valuation. According to Epoch Investment Partners (Epoch), in the period 1927-2023, the S&P500 delivered an average return of 10.3 percent. Of this, valuations accounted for just 0.9 percent of this return, while earnings and dividends accounted for 5.6 percent and 3.8 percent respectively.

The change in P/E multiples shown in figure one have constituted the biggest “swing factor” between those periods when shares have performed particularly well (as they did in the 1980s and 1990s) and when they have performed particularly poorly (as they did in the 1970s). Over the long term, these swings in P/E ratios have almost completely netted out, and the contribution of P/E changes to the cumulative return for the S&P 500 over this time period has been less than one percent per year. Dividends and earnings have driven the vast majority of the returns.

Dividend policies matter

The saying “profits are a matter of opinion, but dividends are a matter of fact” encapsulate the reason that dividend paying companies tend to hold up well during volatile times. Profits are calculations based on a range of real and estimated data and have been known to be overstated; dividends are tangible, paid to investors from corporate earnings.

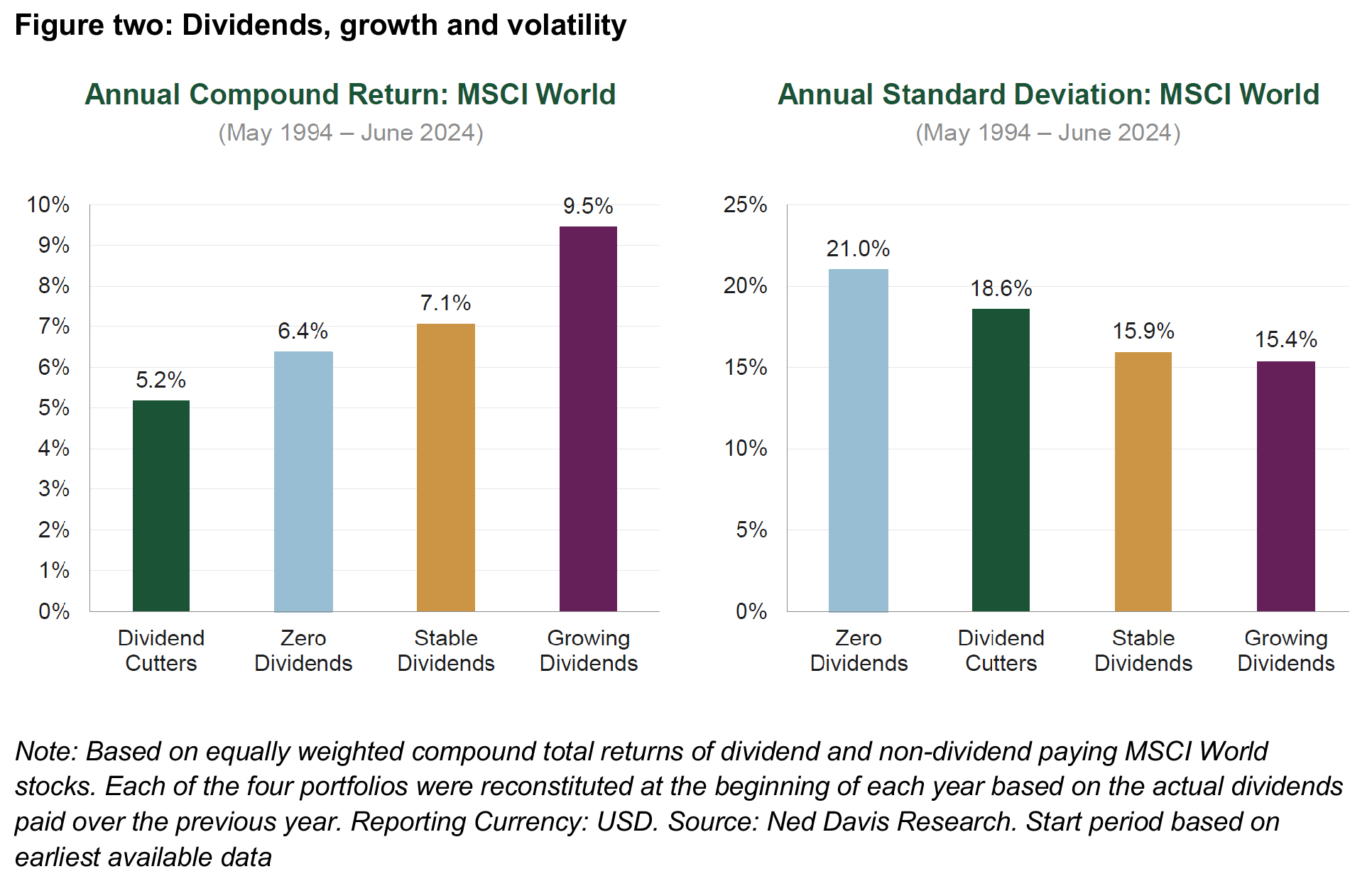

Consequently, dividend paying companies generally provide investors with tangible returns on a regular basis, irrespective of market conditions. As well as being a sign of good corporate health, as illustrated in figure two, companies with growing dividends tend to deliver better returns with lower volatility.

Aside from the obvious income benefit, over the long term, companies that pay a consistent dividend tend to outperform those that either cut or cancel announced dividends or don’t pay any at all, as illustrated in figure two. From May 1994 to June 2024, companies in the MSCI World Index that paid stable dividends returned 1.9 percent per annum more than those companies that cut dividends. Those companies that consistently grew their dividends over this period did better, outperforming the dividend cutters by 4.3 percent per annum.

Importantly, the companies that were consistently ‘dividends payers’ achieved better returns with lower volatility. Dividend growers had a standard deviation of 15.4 percent per annum, and those with stable dividends experienced 15.9 percent per annum. The dividend cutters (18.6 percent per annum) and those companies that did not pay a dividend at all (21.0 percent per annum) delivered lower returns with higher volatility.

Investment managers focused on companies that pay dividends may experience an ‘unintended consequence’. For example, Epoch’s focus on companies paying out high levels of dividends as part of its shareholder yield strategy has resulted in a portfolio that tends to experience less volatility than the market. Because the total return that these companies generate over time is more ‘front loaded’ than that of the average company, there is less uncertainty around it, and the price movements over time reflect that lower uncertainty.

How lower volatility can add value

Low volatility can mean greater wealth for investors over time. This comes down to the power of compounding.

As every investor knows, if you earn 50 percent one year but lose 40 percent the following year, the ‘average’ annual return may be positive (the average of +50 and -40 is +5), but you have 10 percent less money than you started with. The dollar you started with grew 50 percent to $1.50 at the end of the first year, but a drop of 40 percent from that level means a loss of 60 cents, leaving the investor with just 90 cents.

Meanwhile, an investor who earned 20 percent in the first year and lost 10 percent in the second year will have the same average annual return – i.e. 5 percent – but will have $1.08 compared to 90 cents; that invested dollar first grew to $1.20, and then fell 10%, or 12 cents, to $1.08.

The lesson is that if a portfolio can generate the same average annual return as the market, but does so with less volatility, the investor ends up with a higher annualised return than the market – in other words, the investor will have more money than if they simply matched the index return each year. Like dividends, low volatility is a tangible benefit.

Not all dividends are created equal

Identifying companies with the highest dividend yields is easy. Determining which of those will be able to sustain dividends over the longer term is another matter. A high dividend yield can sometimes be a sign of a company in distress. When a company’s share price falls, its yield rises, assuming the dividend hasn’t changed.

Often the developments that led to the fall in share price will eventually force the company to cut its dividend, often with a lag. Where payment of dividends becomes unsustainable, companies may reduce or eliminate dividend payments.

Therefore, when investing for dividend income, it is important the manager is focused on those companies that are paying sustainable dividends that can be increased over time.

Dividends in the current environment

Epoch views the current environment – and outlook – as very supportive for dividends. Further, the investment manager believes it’s a positive environment for all forms of shareholder distributions, including share buybacks and debt reduction.

As the global economy has continued to improve post-COVID, there has been a rebound in growth and resilient demand, leaving companies in strong positions to continue to generate healthy levels of free cash flow, which in turn enables increased return of capital to shareholders. Further signalling an improved environment and expanding opportunity set for income focused investors are developments such as recent dividend initiations from traditional ‘growth’ sectors of the US market.

On a longer-term basis, Epoch believes the current monetary policy setting in the US does not herald a return to the zero interest rate, easy money world of the 10+ years preceding the pandemic. The normalisation of monetary policy will see an elevated cost of capital, which means that companies will need to be more disciplined in their capital allocation decisions, especially with respect to directing cash towards growth initiatives.

Dividend initiations from US tech giants

Although dividends from US tech giants may appear to be a departure from the norm, Epoch believes they look more normal than novel. Most of these companies are well known growth stories that are mature and highly profitable leaders in their respective sectors – the types of companies one would generally expect to pay dividends.

While it is possible that the decision to initiate dividend payments was driven by the changing monetary policy landscape, it is also likely that management teams within these corporates have concluded that they are now generating significant enough free cash flow to support their growth initiatives while also reaping the benefits of paying a dividend – benefits such as a show of confidence toward future earnings, attracting a new segment of investors and more stability in share price returns.

Many of these companies are not looking to simply maintain their level of growth investment alongside a dividend payment; rather, they have actually expanded their near-term capex guidance, signalling immense confidence in their long-term cash generation ability.

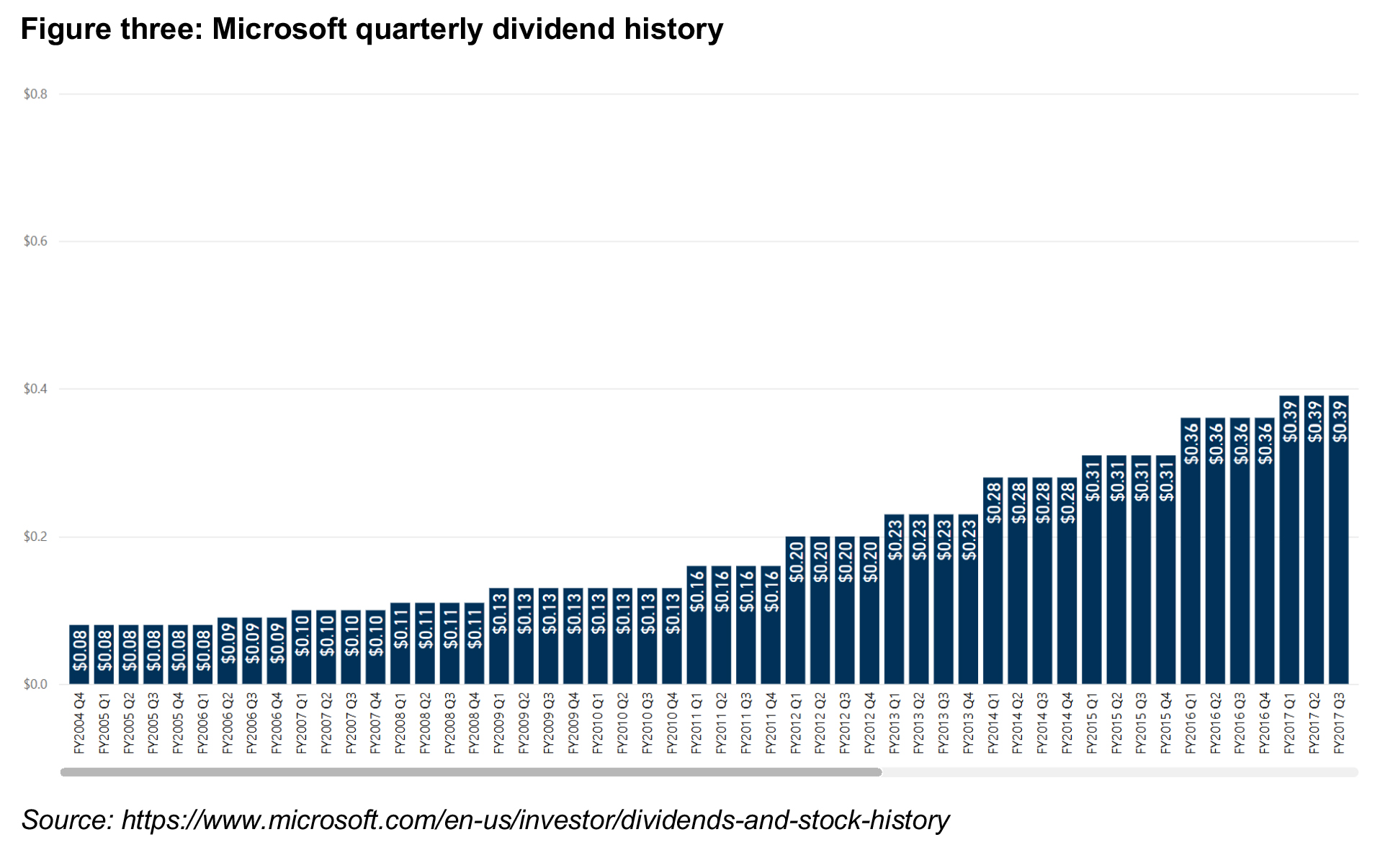

The more ‘old guard’ members of the ‘big tech’ cohort – such as Microsoft – initiated dividends many years ago and have continued to grow rapidly. Microsoft declared its first dividend for shareholders on 16 January 2003 and has consistently increased its dividend payment to investors (figure three). The introduction of the quarterly dividend has not dampened Microsoft’s share price performance (figure four).

This example demonstrates that dividend payments do not spell the end for business growth.

A shareholder yield approach

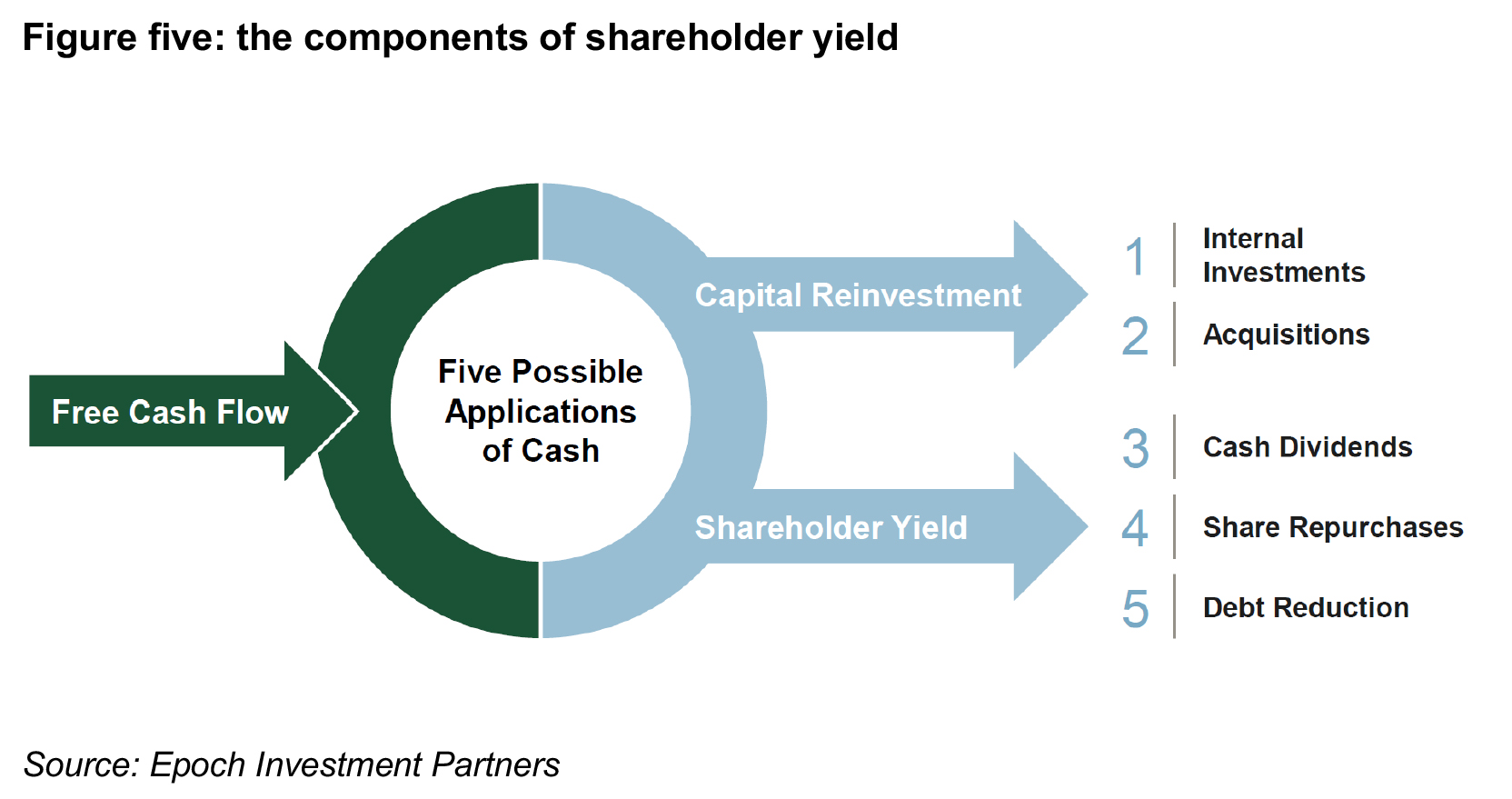

The idea that dividends contribute to business growth is highly aligned with the core shareholder yield philosophy, as growth is an important component of the strategy’s return framework. A shareholder yield strategy requires portfolio holdings to be both growing their free cash flow consistently and returning much of that cash to shareholders.

Companies maximise returns through disciplined capital allocation and a shareholder yield strategy is premised on a belief that companies should reinvest capital if the expected return on invested capital is greater than the company’s cost of capital. Remaining free cash flow should be returned to shareholders via shareholder yield (figure five).

A more normalised monetary policy environment will likely make shareholder distributions a more attractive use of capital for companies…although dividends are not the only avenue through which cash can flow to shareholders.

While cash dividends are the most obvious and direct way to return capital to shareholders, taking a broader view and recognising that share repurchases and debt reduction increase shareholder’s claims on company cashflows. Dividend payments are far more committal than share repurchases, as dividend cuts are often viewed as a signal to investors that a business is under pressure. Consequently, many companies, especially in the US, have opted to focus more on share buybacks as a mechanism for returning cash to shareholders, requiring the flexibility to dial distributions up and down without spooking the market.

Investing in global equities for income offers significant advantages for investors seeking both diversification and growth opportunities. By broadening the investment set to include international markets, investors can access a wider array of high-quality companies, many of which offer attractive dividend yields and long-term growth potential. Global equities can also provide a hedge against domestic economic downturns and reduce risk through geographical diversification.

As the global economy continues to evolve and expand, the potential for capital appreciation and increased income is promising. While global investing does come with risks such as currency fluctuations and geopolitical challenges, a diversified global equity portfolio can offer a balanced approach to achieving steady income and long-term wealth creation. As such, global equities should be considered an integral part of any income-focused investment strategy.

———