China is already at the forefront of humanoid development.

Key takeaways

- Building on its success in electric vehicles (EVs), China is now shifting its attention towards humanoid robotics as the next frontier for technological leadership.

- This transition draws on deep parallels between the supply chains of humanoids and EVs, allowing China to leverage its expertise in batteries, motors and large-scale manufacturing.

- While Chinese original equipment manufacturers (OEMs) are pursuing task-specific industrial humanoids, Western developers are prioritising high-end, general-purpose models.

China’s rise to dominance in EVs, from batteries to motors to mass production, is a testament to the nation’s success in evolving an innovative endeavour into a full-fledged industry. This achievement has set the stage for China’s ambitions in the humanoid robotics sector, sparking industry-wide debate on whether the same formula can be applied?

At the most recent CES 2026 – one of the most influential technology exhibitions of the year – many Chinese companies seized the opportunity to unveil their latest humanoids. Humanoids were, in fact, a standout theme at this year’s event, with 38 exhibitors showcasing humanoid robotics. Of these, 21 hailed from China, underscoring the country’s intensifying focus on this emerging domain. US-based Boston Dynamics made headlines by presenting the first commercial, all‑electric iteration of its Atlas humanoid. The Atlas demonstrated remarkably fluid movement, fully rotational joints and could handle payloads of up to 50 kilograms, signalling a shift from laboratory testing to practical industrial applications. In comparison, Chinese exhibitors revealed a variety of taskoriented humanoids developed for specific roles within factories and warehouses, such as robots designed for material handling, sorting and inspection tasks. These examples illustrate both the push for general-purpose adaptability, as seen with Atlas, and the targeted, pragmatic approach favoured by Chinese manufacturers.

Promise or paradox?

Humanoids are machines designed to move and act like humans. They are envisioned for a range of uses but are currently being piloted in factories and warehouses to do labour-intensive and repetitive tasks like moving materials, sorting goods, or performing inspections. Longer-term, humanoids could even assist in health care and elder care, perform domestic chores alongside humans and tackle labour shortages as the working population shrinks.

Bold visions come from bold thinkers with bold numbers. Tesla CEO Elon Musk has mused that by 2040 there will be more humanoids than people[1], which implies a massive trillion-dollar global opportunity. Meanwhile, Nvidia’s CEO Jensen Huang proclaimed “the ChatGPT moment” for general robotics is just around the corner, alluding to a scenario where rapid AI development and proliferation could soon drive a similar breakthrough in the field of robotics.

More conservative projections estimate that the humanoid robotics market could reach approximately US$51 billion by 2035, contingent on a substantial decrease in robot prices from current levels.[2]

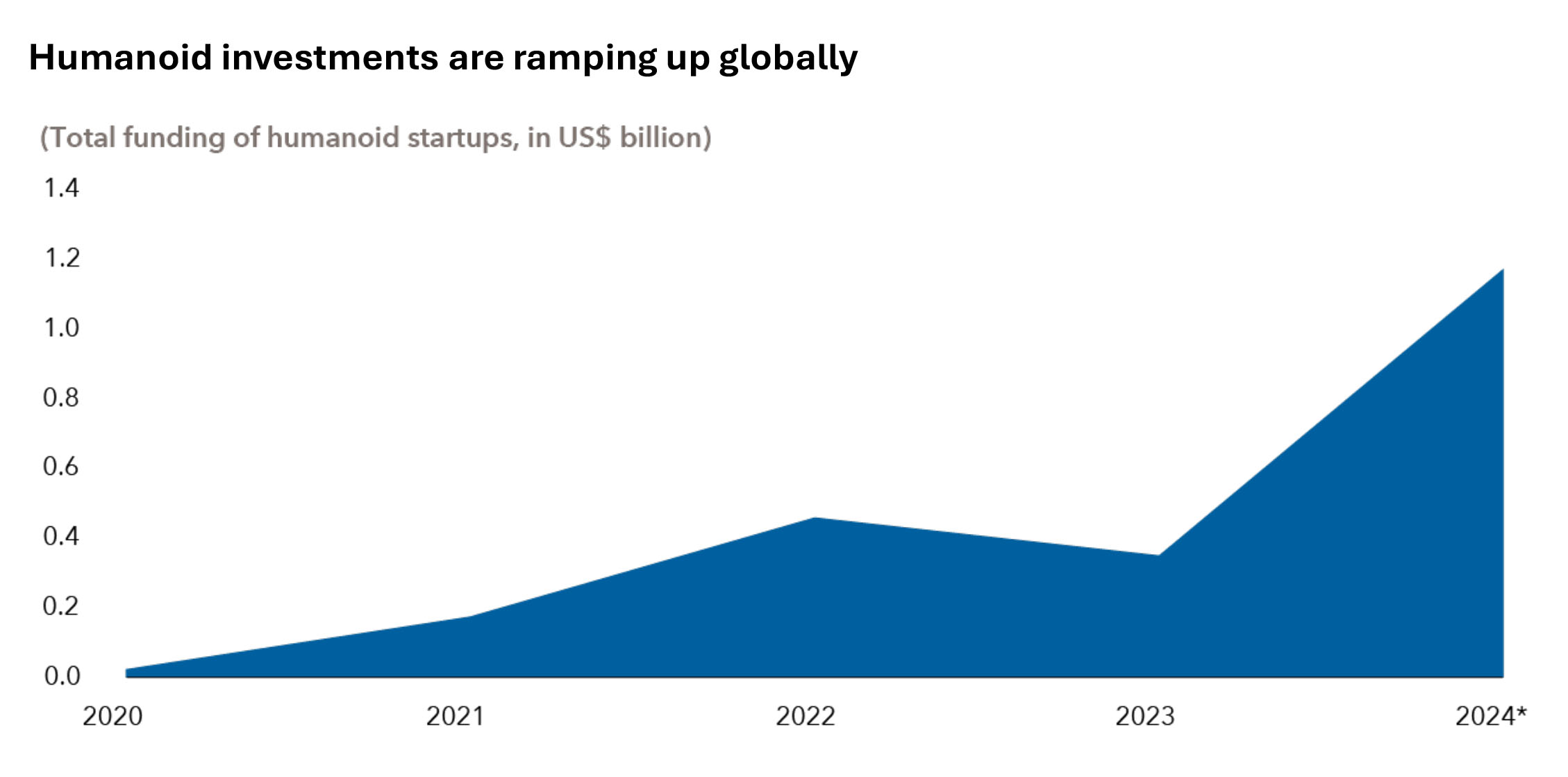

While estimates may differ, what is clear is that investments into humanoids are increasing exponentially. Global funding of humanoid startups was almost inconsequential at the turn of the decade but has since gone on to reach US$1.2 billion in 2024. DroidUp, Robot Era and X Square Robot are just some of the many humanoid companies to have been founded in China since 2020. Notably, a number of these start-ups have been spun out of universities or maintain close affiliations with academic institutions and many have secured funding from major corporations such as Alibaba Cloud, Tencent and Huawei.

Challenges facing humanoid deployment

Challenges facing humanoid deployment

Key tech hurdles: Although advancements in AI have accelerated progress, key hurdles remain for humanoids to be adopted widely.

Training data and robot intelligence: Humanoids must rely on vast amounts of real-world data to learn through trial, error or imitation. Although simulated data can be useful, the gap between virtual and real-world conditions means many robots still struggle in real-life scenarios.

Software and control constraints: Most existing humanoids are semi-autonomous, carrying out preset tasks under human or system supervision. Achieving full autonomy requires advances in real-time perception, planning and safe learning.

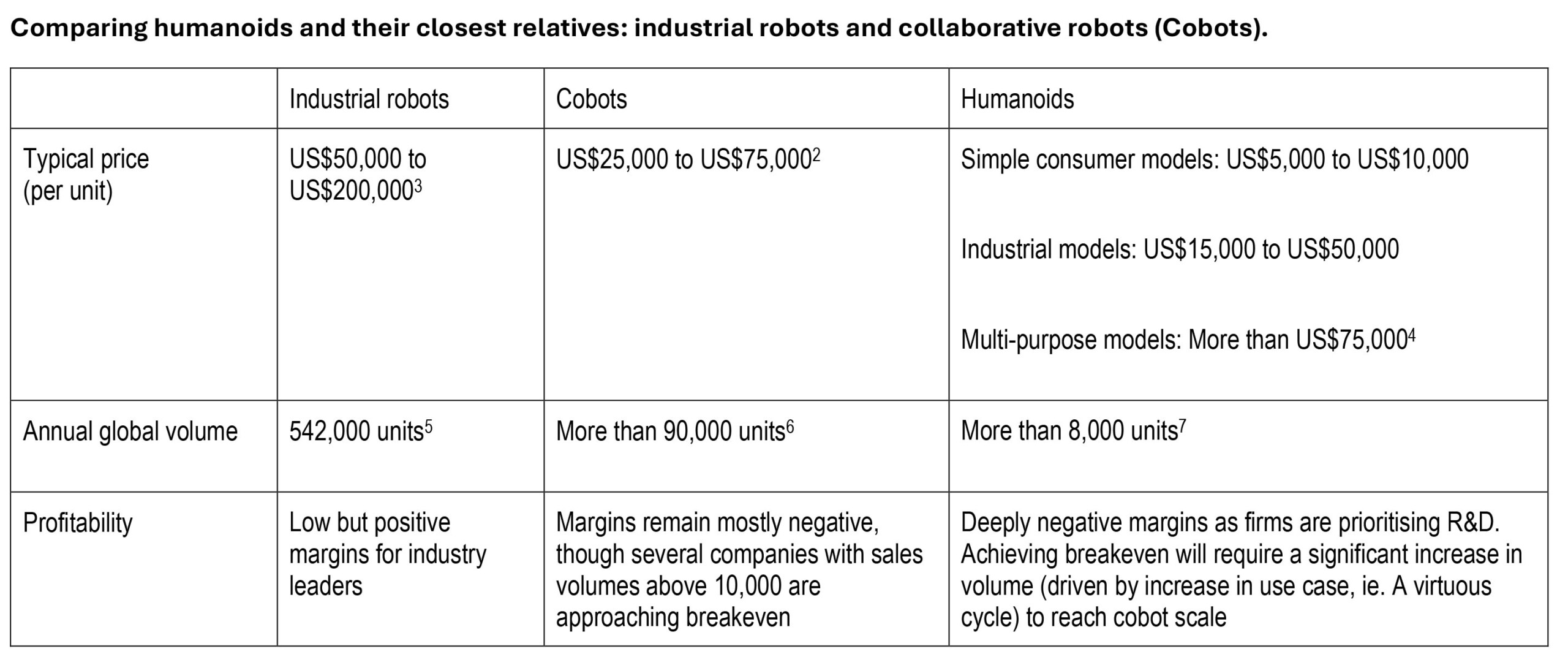

Power and battery life: Humanoids generally weigh between 50 and 70 kg and operate only for one to two hours per charge. Batteries continue to be heavy and costly, which affects practical deployment.

Mechanical reliability and design trade-offs: Walking and object manipulation require motors and joints that can withstand various operational demands. Early models are prone to overheating and mechanical wear.

Expensive price tags: An advanced unit such as Boston Dynamics’ Atlas has been reported to cost up to US$150,000. Humanoids built for specific tasks also typically cost several tens of thousands of dollars per unit.

Considering the significant investments and high costs associated with humanoids, a critical question emerges: what must happen for humanoids to become financially viable to kickstart a self-reinforcing flywheel that can lead to the advancement and proliferation of humanoids?

The key takeaway is clear: scale is everything. For the humanoid industry to break even, they will likely need to achieve annual sales of at least 100,000 units, mirroring the threshold that recently brought cobots close to profitability. To move beyond breakeven and enjoy the solid profitability seen in the industrial robot market, which operates at over 500,000 units a year, humanoids would have to match these far higher volumes.

Given that current humanoid shipments are well below these figures, it would be at least five years before the industry even approaches breakeven levels, with true profitability remaining a longer-term goal. That said, this should be seen as a feature rather than a flaw. It mirrors the early stages of previous major technological shifts, where progress depended on continued innovation, the development of practical use cases (and data), growing demand and, ultimately, profitability.

“Bots” at a glance

Industrial robots

- Design: Large, rigid robotic arms or gantry systems.

- Purpose: High-volume, highspeed automation in manufacturing environments.

- Common applications: Coating, chassis and engine assembly, welding.

Cobots

- Design: Typically arm-like, smaller than industrial robots, designed for safe interaction with humans.

- Purpose: Work alongside humans in shared spaces without heavy safety barriers.

- Common applications: Food packaging, component sorting, machine tending, quality inspection.

Humanoids: EV 2.0?

Despite the nascency of the industry, the Chinese government has identified humanoids as a strategic priority. In January 2024, China’s Ministry of Industry and Information Technology unveiled the ‘Guidelines for the Innovative Development of Humanoid Robots’, setting out a framework to foster robotic innovation. This strategic focus is further demonstrated by the nation’s organisation of high-profile events, such as the World Humanoid Robot Games, and its active encouragement for state-owned enterprises (SOEs) to engage in pilot projects and facilitate data collection. This echoes with China’s strategy for EVs, which integrated policy coordination, capital investment and industrial development.

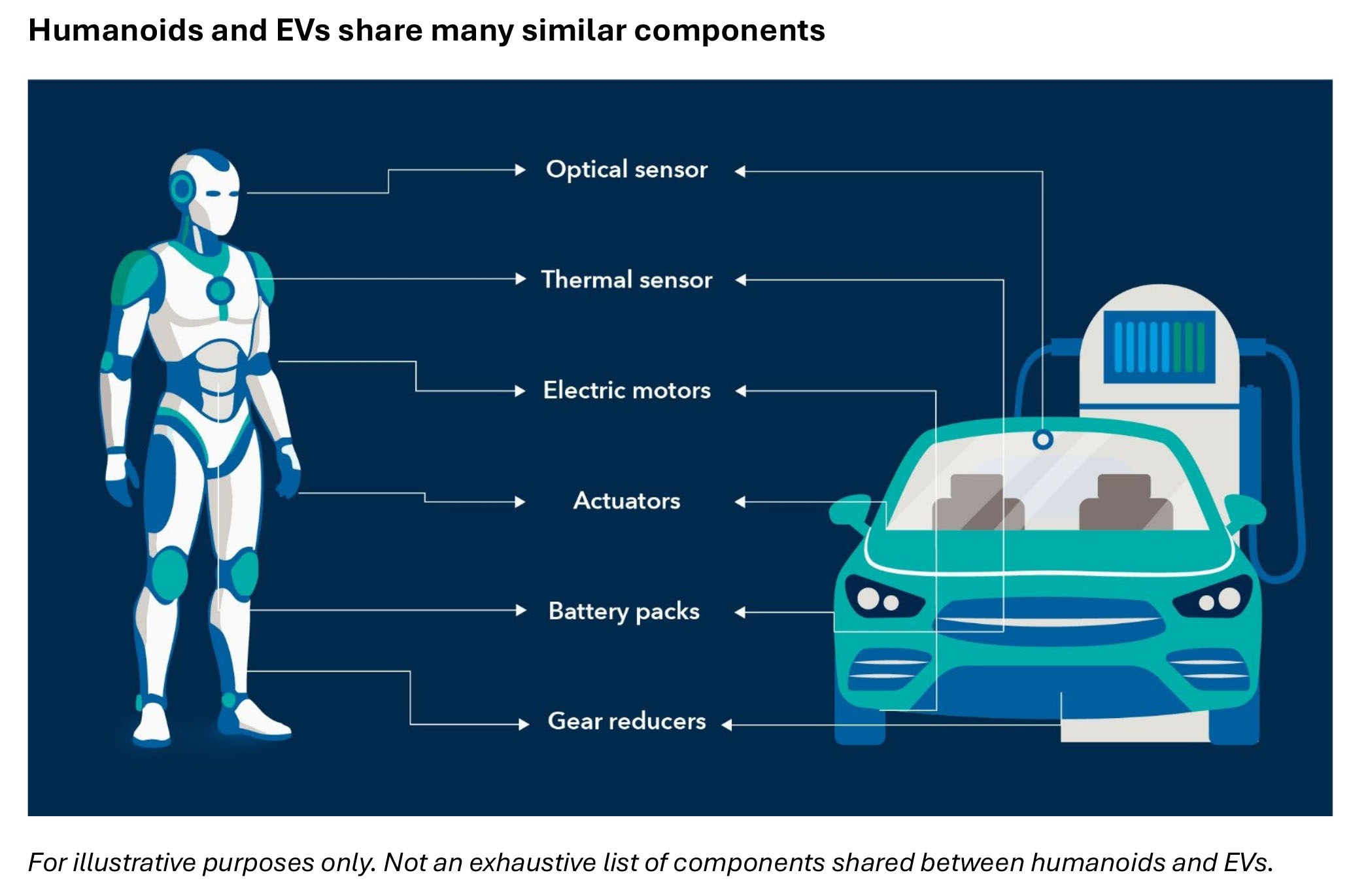

Another reason why China’s dominance in EVs could potentially translate into humanoids is the significant overlap in the supply chain of the two products. Both rely on electric motors, power electronics, batteries and sensors, areas where China has built formidable capacity and know-how. For example, the lightweight electric actuators that move a robot’s limbs are cousins to EV drivetrain motors and high-density battery packs for robots draw directly on advances from EVs.

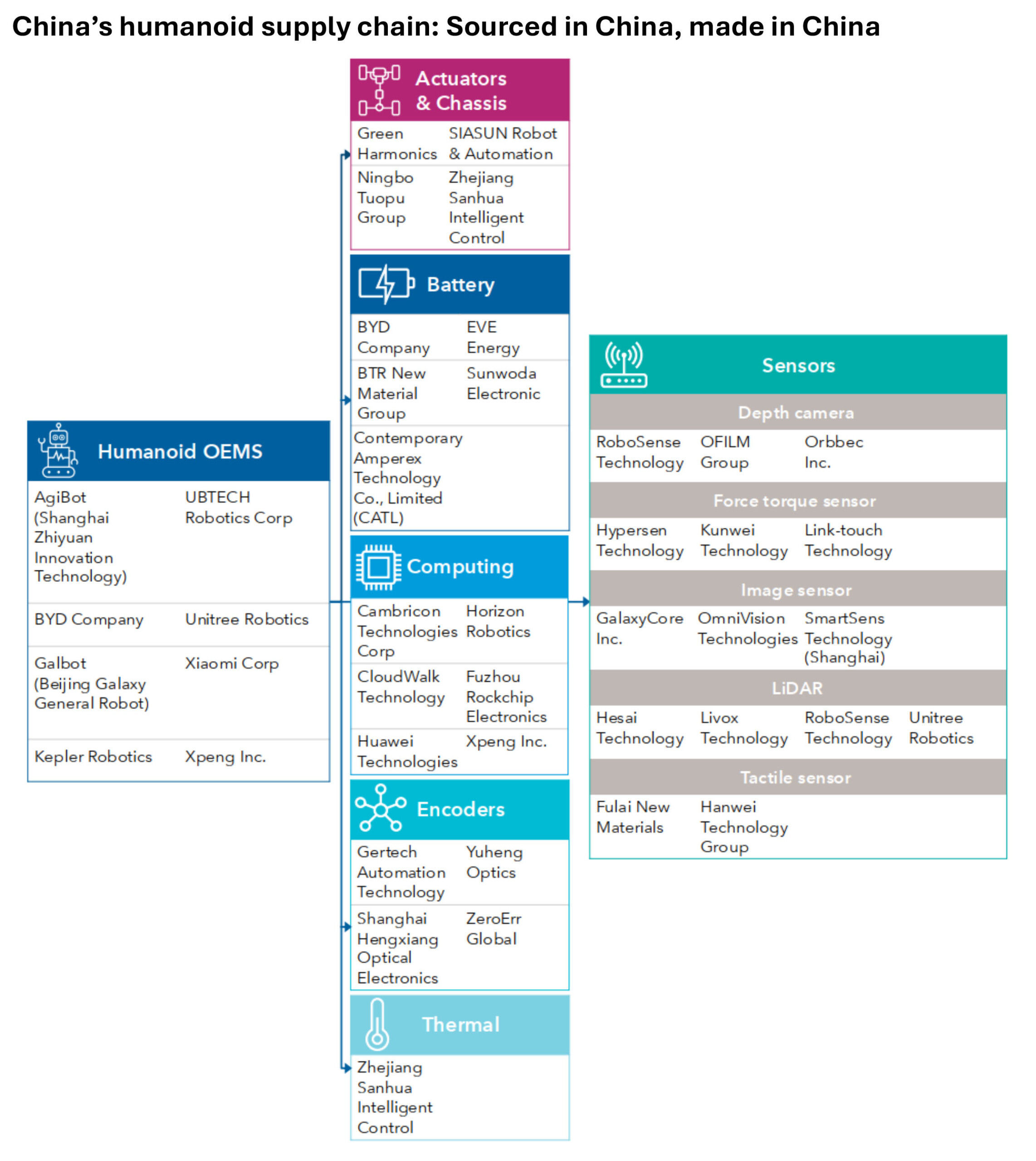

As a result, many Chinese auto suppliers are repurposing their products for humanoids. Companies like Zhejiang Sanhua Intelligent Control and Ningbo Tuopu Group, originally making EV thermal and chassis parts, are reportedly assembling joint modules for Tesla’s Optimus humanoid. 8 China’s extensive electronics and automotive ecosystem (motors, gear reducers, lithium batteries, camera modules, etc.) means much of the humanoid “body” hardware can be sourced locally and at scale.

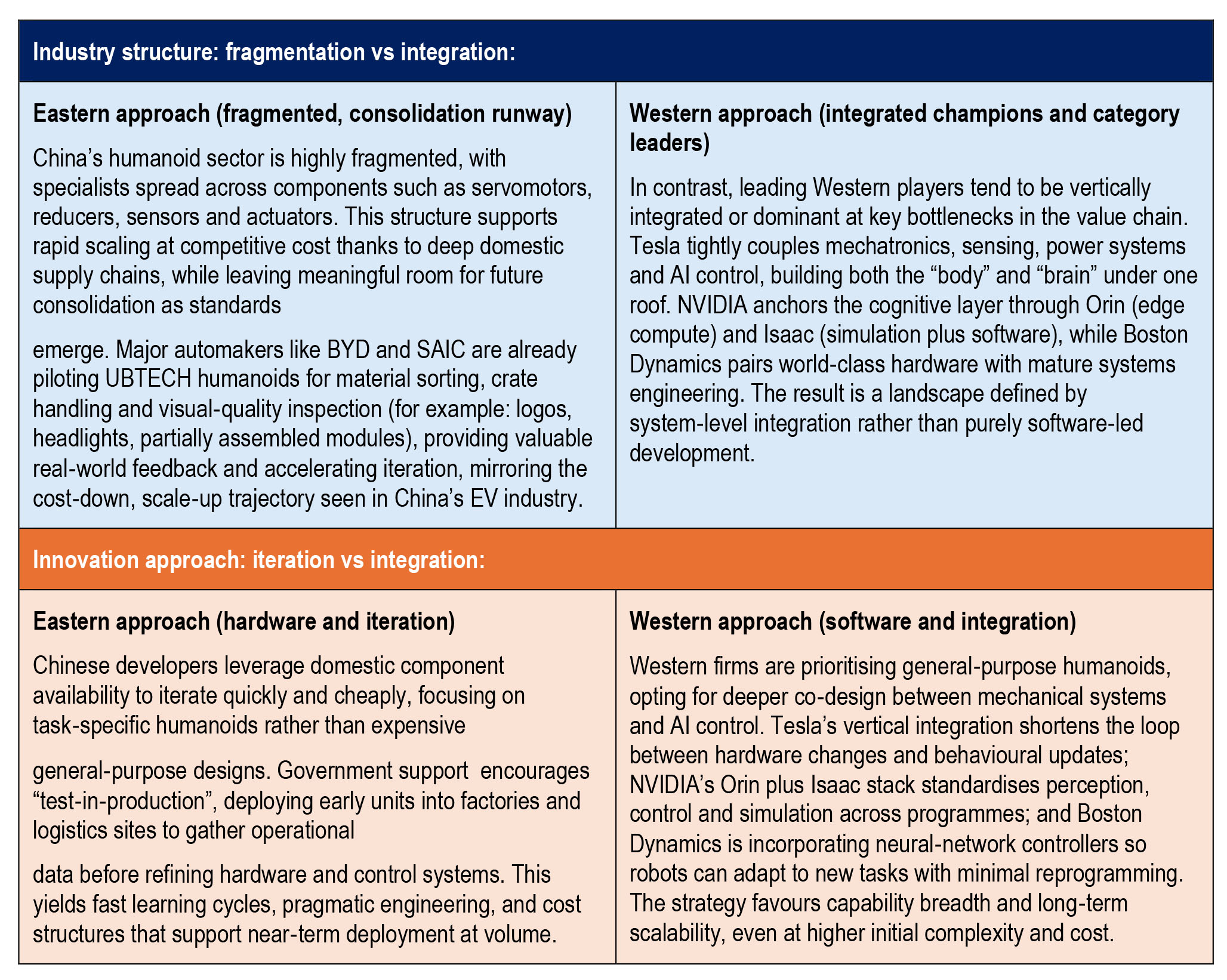

The east vs. the west

As more companies are showcasing their humanoid prototypes globally, a clear emerging theme is the divergence between Eastern and Western development philosophies. Both are racing toward similar goals, but they have chosen different routes.

Conclusion: A shifting global landscape

In summary, China’s momentum in the humanoid sector is underpinned by its formidable strengths in innovation and execution, evident by the success in its electric vehicle dominance: an extensive, skilled manufacturing workforce, a focus on cost efficiency, robust government backing, an increasing focus on technology innovation and the capacity for rapid prototyping as well as iteration. Conversely, Western initiatives are distinguished by leading-edge AI research, advanced systems integration and software development. These complementary capabilities ensure that both regions will play critical, interdependent roles in shaping the humanoid robotics market.

Instead of a simple rivalry, the future could point towards a complex, globally interconnected value chain. It is conceivable that Chinese factories could one day produce hundreds of thousands of humanoid units, each powered by an AI operating system licensed from the US, with a blend of Chinese actuators and American-designed chips. Investors and stakeholders should pay close attention to trends in hardware commoditisation, where China holds a competitive advantage and software or intellectual property development, where Western firms excel.

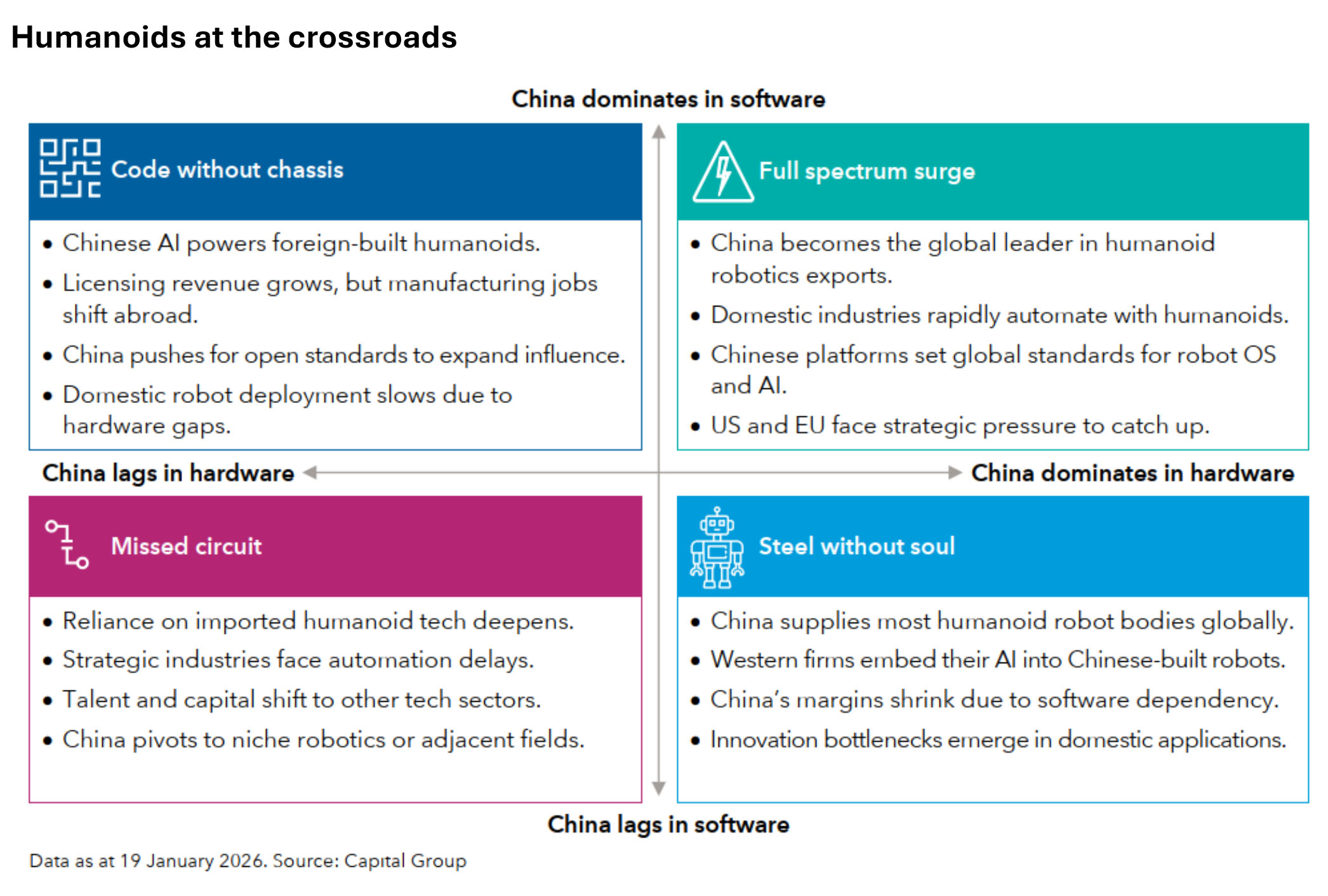

However, this dynamic could shift significantly if China manages to close the gap in software and services. Recent progress in generative AI, exemplified by initiatives like DeepSeek, coupled with the rise of domestic AI chip production and China’s proven track record of innovation in the EV sector, indicate the potential for the country to extend its influence well beyond manufacturing.

Given these factors, it is therefore also essential to consider a range of scenarios in which China may emerge as a dominant force across both hardware and software segments of the humanoid robotics industry. This scenario analysis will help investors and industry leaders anticipate future developments and strategically position themselves within an evolving global landscape.

Given how early humanoid development still is, it remains anyone’s guess how the industry will evolve over the long term. But one thing is clear: China is ready and already at the forefront of humanoid development. With its dominance in hardware manufacturing and continued investments in software and AI, China has the potential to replicate its success in EVs with humanoids.

————

————