SQM research downgrades 2026 housing forecasts amid elevated inflation and rate risks

Key drivers of the downgrade include:

- Energy price pass-through lifting household bills (e.g., petrol potentially to $2.57/L at $150 oil) and eroding affordability.

- Limited wage growth amid AI adoption curbing labor demands, contrasting with 1970s-style spirals.

- Potential government rebates providing some offset, but not enough to fully revive momentum. (Source: SQM Research, March 2026).

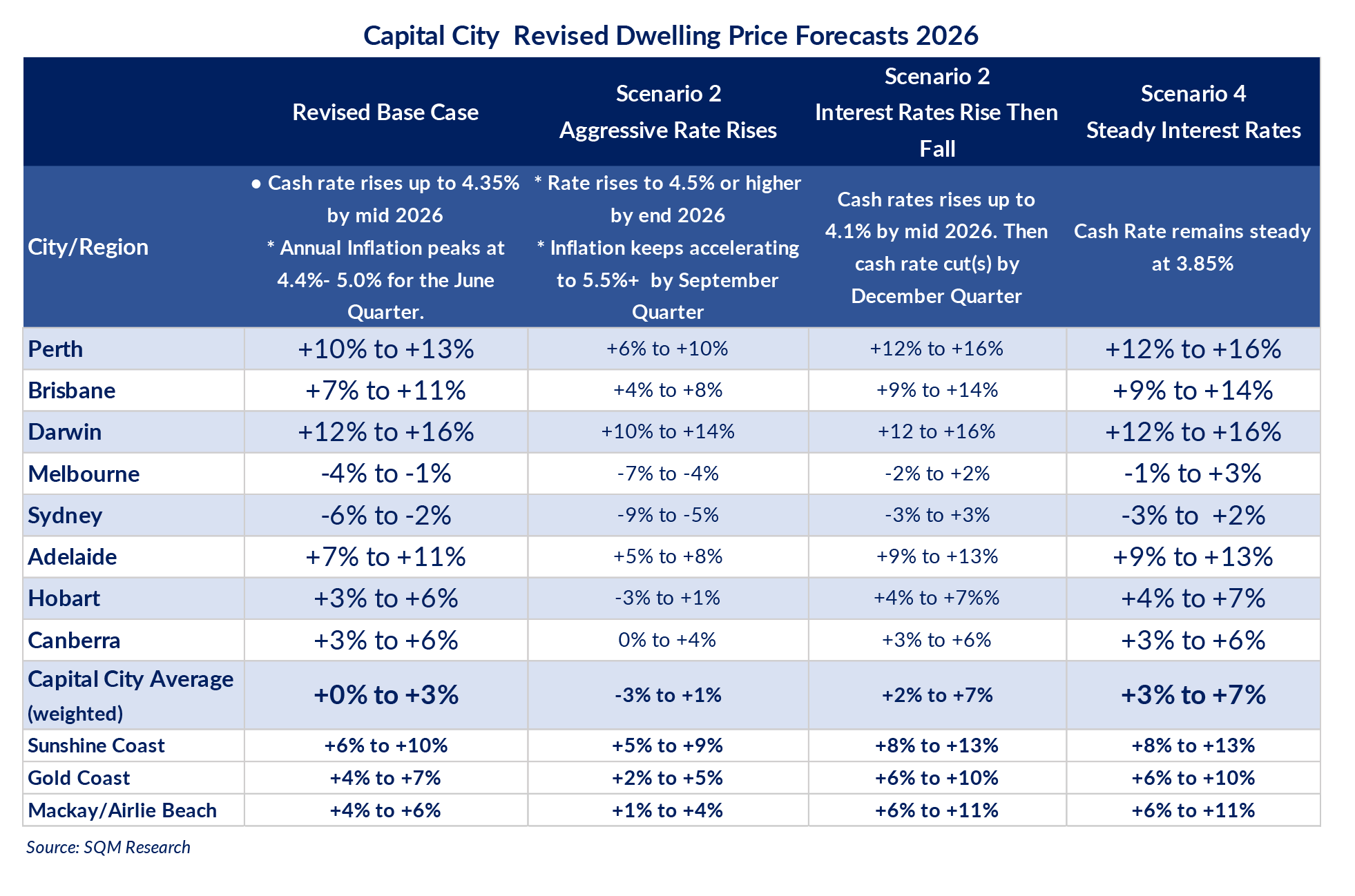

Forecasts are annual percentage changes in dwelling prices. Scenarios incorporate RBA outlooks, energy shocks, and economic sensitivities.

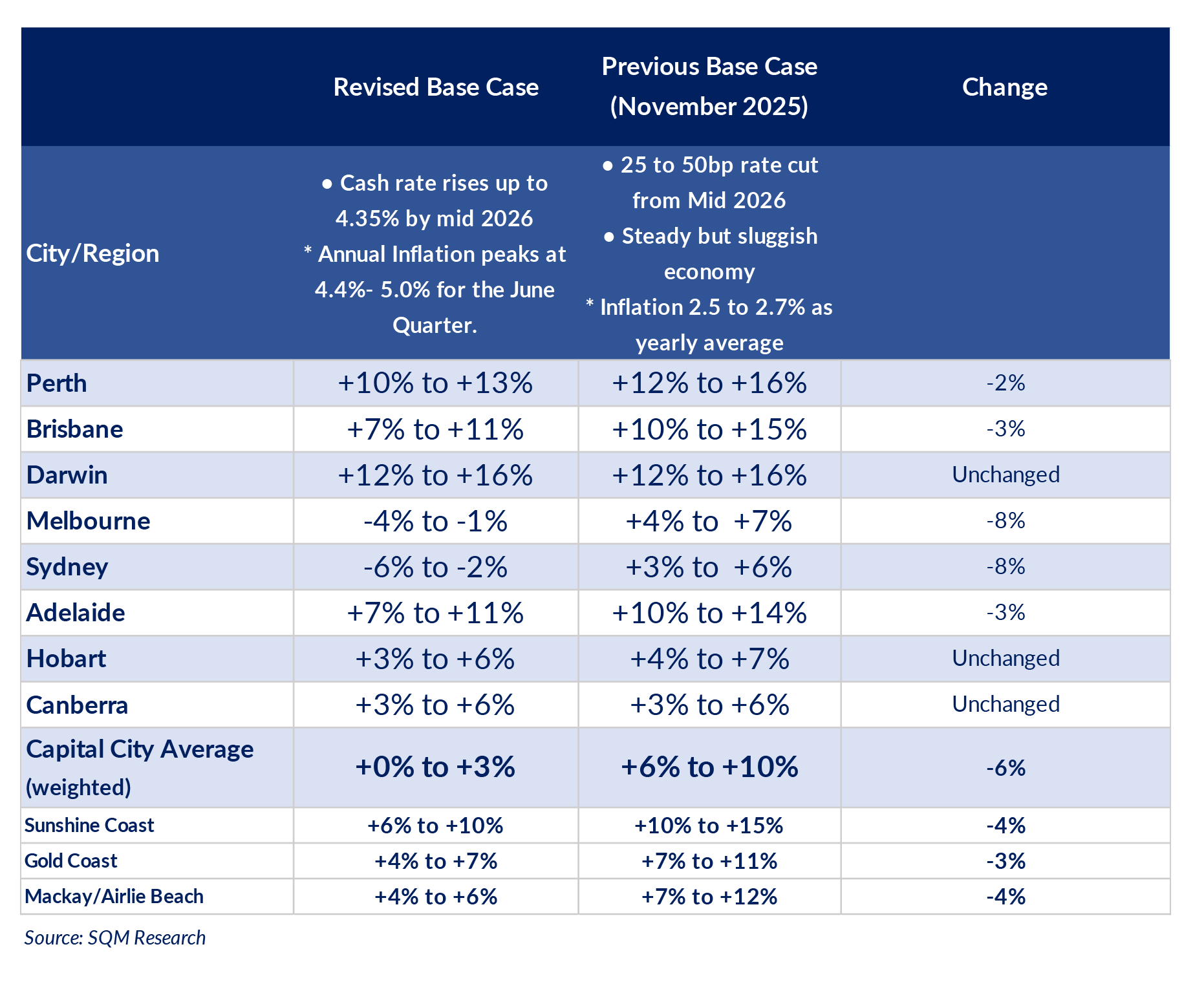

Revised Base Case Sees Weighted Capital City Growth of 0% to +3%, down from Prior +6% to +10% Sydney, 10 March 2026 – SQM Research has revised its 2026 dwelling price forecasts downward, reflecting heightened risks from persistent energy shocks, reaccelerating inflation, and potential further RBA rate hikes. Under the updated base case— assuming the cash rate rises to 4.35% by mid-2026 and annual CPI peaks at 4.4%-5.0% for the June quarter—weighted capital city prices are now expected to rise by just 0% to +3%, a significant downgrade from the November 2025 projection of +6% to +10%.

The revisions account for escalating Middle East tensions disrupting oil supplies (Brent crude above $92 per barrel, with upside to $150), which could amplify cost-of-living pressures, suppress buyer sentiment, and force tighter monetary policy. While Perth and Darwin retain strong outlooks (+10% to +13% and +12% to +16%, respectively) due to resource-driven demand, major eastern capitals like Sydney (-6% to -2%) and Melbourne (-4% to -1%) face steeper headwinds from higher borrowing costs and subdued migration.

Alternative scenarios highlight the sensitivity to inflation and rates: In an aggressive hiking path (cash rate to 4.5%+ by year end, CPI to 5.5%+ by September), growth weakens further to -3% to +1% weighted average. Conversely, if rates peak at 4.1% then ease later in the year, or hold steady at 3.85%, outcomes improve modestly to +2% to +7% or +3% to +7%.

Louis Christopher, Managing Director of SQM Research, commented: “Our revised forecasts reflect a more cautious outlook as energy-driven inflation risks mount, potentially delaying rate relief and weighing on housing demand. While resource-heavy markets like Perth and Darwin hold firm, the downgrades in Sydney and Melbourne highlight vulnerability to higher rates. If shocks persist, we could see even softer outcomes, though fiscal measures like energy rebates might provide a buffer. Investors should monitor RBA signals closely amid these uncertainties.”